Good morning! It's Paul here with Monday's SCVR.

Timing - today's report is now finished.

** Newsflash! Reminder that Ed will be doing a presentation at 18:15 tonight at Mello Monday. The other speakers & company ( Gaming Realms (LON:GMR) ) are all really interesting, so this one is probably the best so far. I've been roped into the panel discussion (again, I hear you sigh!!) at the end. I'm going to focus mainly on investing ideas & themes for 2021, so it's not duplicating my recent PIWorld chat **

I'm hoping it might be a bit quieter for company news this week, as I need to take some time out to buy the food for Xmas Day from ASDA. Reports of logjams at channel ports, mean we could run out of parsnips any time soon. Obviously completely unconnected with Brexit negotiations! ;-)

Covid - we're getting bad news about case numbers & deaths, but good news on the vaccine. My mother had her first vaccine dose yesterday. She reported back that it was very well organised, quick, and completely painless - she didn't feel a thing. No side effects. The booster jab is scheduled for 3 weeks. You might like to pass that on to your relatives & friends, to reassure them that it's not at all daunting. Mum came out of the health centre a little later (they make people sit for 15 minutes, to ensure there's no adverse reaction), got into my car, and commented, "Everyone in there was decrepit! They must be doing the over-90's today!"

To start off on companies, here’s one I prepared earlier (!!!)

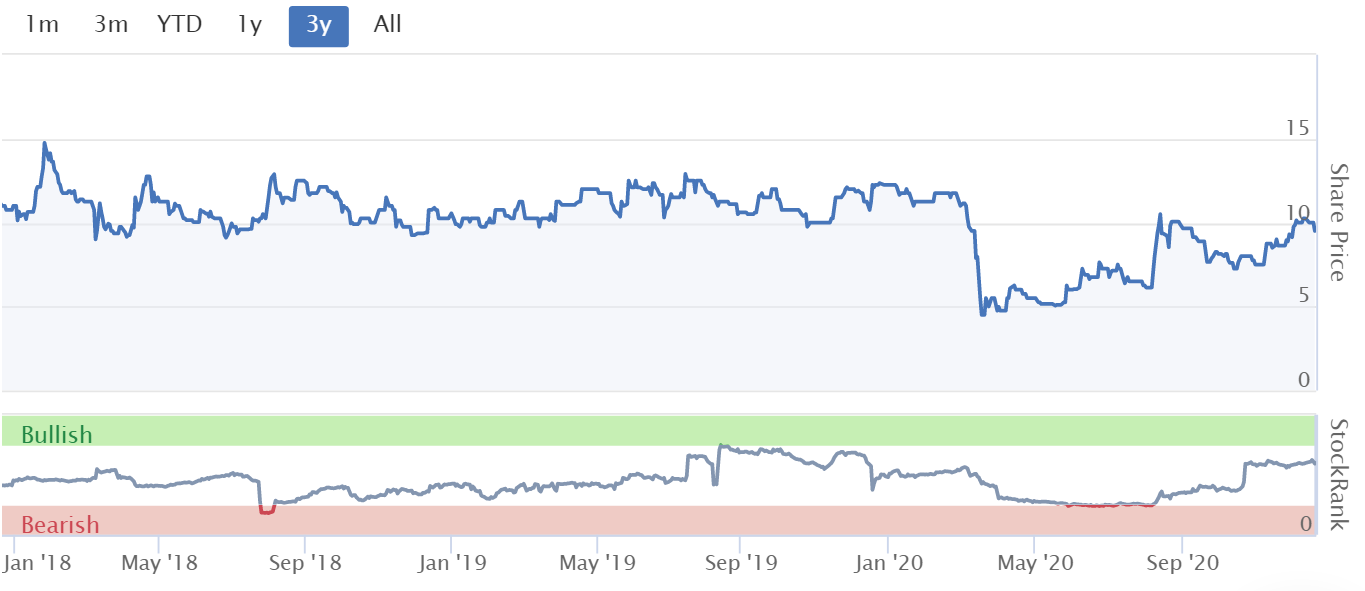

Fulham Shore (LON:FUL)

9.5p - mkt cap £58m

Half-year Report (published 18 Dec 2020)

The operator of Franco Manca pizza restaurants, and the smaller chain “The Real Greek”, both being casual dining formats. Both are excellent, popular, and nicely differentiated, i.e. not just copy-cat pizza restaurants like all the others.

Investors generally should look at least 6 months ahead, therefore we really should now be focused on how businesses are likely to trade post-covid. That’s why so many cyclical shares have rallied strongly in recent weeks. Therefore, FUL’s interim results during the covid period are only of passing interest. I’m more interested in balance sheet strength, liquidity, and the outlook.

The Directors of The Fulham Shore PLC ("Fulham Shore", the "Company" or the "Group") are pleased to announce unaudited interim results for the six months ended 27 September 2020.

During this period we saw lockdown 1, then re-opening, and the big boost in August from EOTHO scheme, and reduced VAT. H2 will see continued disruption from lockdown 2 (and 3 possibly, the way things are going currently?). So this financial year, FY 03/2021 is likely to be grim, but that’s information the market already knows, so should be baked into the price.

Funding - FUL only raised a small amount from shareholders, a £2.25m placing at 6.25p, in August. Enlarged bank facilities were also put in place. FUL has unusually large debt facilities for a company of its size, in my opinion. The latest picture is this;

As at 17 December 2020, the Group had net debt (excluding lease liabilities) of £3.7m with undrawn debt facility of £11.5m out of total facilities of £25.75m

H1 revenue was £19.9m, down 45% on LY, obviously due to covid/lockdown enforced closures

Loss before tax was £4.3m, although there are numerous alternative profit measures given, so take your pick!

Net debt - fell from £9.5m at 29 March 2020, to only £3.3m at 27 Sept 2020 - which suggests to me there must be considerable creditor stretch.

Headline EBITDA - this number looks meaningless now, because IFRS 16 inflates it by stripping out a lot of the rental cost of properties. So I am ignoring this artificially high figure of £3.7m positive headline EBITDA. More meaningful is the old (IAS 17) headline EBITDA figure, which is exactly breakeven. It may seem off that the company has managed to perform at breakeven EBITDA in a period when its restaurants were closed for a considerable time. Bear in mind that these figures are boosted by Govt support schemes;

We have, during the Half Year, benefited from certain UK Government support schemes including, amongst others, the Coronavirus Job Retention Scheme ("CJRS"), Coronavirus Large Business Interruption Loan Scheme ("CLBILS"), VAT deferral, hospitality business rates relief at applicable locations and the Eat Out to Help Out Scheme.

Balance sheet - NAV: £37.0m, less £24.6m intangibles, and eliminating £1.77m of deferred tax liabilities, gets me to NTAV of £14.2m.

Lease assets and liabilities should be shown separately on the balance sheet, instead they are lumped together with fixed assets, and “borrowings”, which is poor presentation.

I feel that FUL should have done a larger placing, and relied less on debt.

Expansion - this is a wonderful time to be opening new restaurants, as the deals on offer from landlords are very attractive;

The ongoing damage to the property and restaurant sectors will allow us to prospect for new sites at much reduced rents and with lower capital costs per site. The two restaurants we have recently opened cost us less than half of the typical outlay of a year ago.

As such, over the next few years and once normal trading conditions return, we will target a higher return on capital than we have historically achieved.

Therefore, investors who look beyond covid, to a world (currently indicated by Govt to be from April/May 2021) where consumers can return to normal, then the future could be bright for popular restaurants to once again prosper, and with less competition. This sector has been over-supplied for years, so we are now seeing a much-needed reduction in capacity, as other restaurants close their doors. Sad for everyone involved, but we have to be realistic, that we need fewer restaurants, so that the survivors can prosper.

My opinion - the share price has now recovered back up to the lower range of where it was before covid. So where is the upside from here onwards going to come from? New site openings, on lower rents maybe, but why would I want to pay for that up-front?

By remaining solvent, and performing relatively well, you could argue that FUL is at a disadvantage. Competitors can do CVAs to force down their existing rents, and exit under-performing sites, but what can FUL do? It seems to be stuck with pre-covid rents, making it potentially less competitive.

To my mind, there’s probably better recovery upside on other shares right now. I'd want a significantly lower share price to tempt me into this share.

.

.

Boohoo (LON:BOO)

(I hold)

New auditor appointed

As expected, it looks a mid-tier firm, PKF Littlejohn. Its website says PKF is the 7th ranked auditor of listed companies in the UK, and has more than 21,000 partners and staff globally (of which 2,030 in the UK). So it's not a mickey mouse outfit. I don't really care who audits the accounts, as long as it's a reasonable-sized firm with a good reputation (which this is), and not some local backstreet outfit.

Audit work always used to be the entree, with little profit, to get a foot in the door for more lucrative tax & deal advisory fees.

KPMG is helping Sir Brian Leveson, in cleaning up & follow-up reporting on the extensive supply chain measures that have been taken. Once everything is sorted out there, maybe KPMG could become the auditors in future? Does it really matter? The auditing sector seem to be frequently engulfed in their own scandals & failures, so I find it a bit rich that they're reported as being sniffy about not wanting to audit BooHoo!

It will be interesting to see what happens to the Arcadia brands. Newspapers are reporting that BOO is seen as the front-runner to acquire the jewel in the crown, TopShop. That would certainly be an exciting move, but Mike Ashley is also sniffing around apparently. With 9 existing brands, BOO has plenty to be getting on with.

Over the weekend, I thought it would be interesting to compare the number of Instagram followers that BOO's brands have, and this was the result;

| PrettyLittleThing | 12.9m | |

| BooHoo | 7.0m | |

| NastyGal | 4.9m | |

| MissPap | 2.5m | |

| BooHooMan | 1.4m | |

I didn't look at the smaller, more recently acquired brands (Oasis, Warehouse, Karen Millen, and Coast), as they're probably not significant at this stage (e.g. Oasis was only 355k).

In the table above, the numbers that really surprised me are PLT, which seems to be smashing it, at 12.9m followers, and NastyGal doing surprisingly well - which could be behind the very strong growth in American revenues reported in recent interims. If BOO brands continue growing strongly in America, then a listing in New York would make a lot of sense & could trigger a serious re-rating - look at FarFetch for example.

By way of comparison, Manchester fast fashion competitor MissGuided has the same number of Instagram followers as BooHoo, at 7.0m. Press reports say it is having a big resurgence, with sales up 45% (same as BOO group) this year, to c.£300m annualised, according to recent press reports, and is considering a stock market flotation.

Did you see the TV mini-series about MissGuided? It almost went bust in 2018, but has since managed to recover, but is still loss-making, in both 2019 & 2020. How do they manage to lose money in a booming sector? The TV series suggests they're not very good at managing stock intake & ended up with a lot of terminal stock (buying the wrong things basically). The whole point of test & repeat is that that shouldn't be able to happen. The foul-mouthed narrator/creative woman at Missguided was really rubbing me up the wrong way by episode 3. How is it empowering for women to shout & swear all the time? Maybe I'm just getting old, but I prefer it when all people act with a bit of decorum in the workplace.

EDIT: Evans, the plus-sized brand of Arcadia has been sold for £23m - details here. End of edit.

.

Sanderson Design (LON:SDG)

(I hold)

Trading update

Sanderson Design is the new name for Walker Greenbank, a purveyor of fine wallcoverings & furnishings.

Very positive update, we should be in for a good day today.

Trading has been "substantially ahead" of management previous expectations. Pity there's no footnote to give us some guidance. But I won't quibble over that, given that the share price should rise today.

The improvement in sales during October and November 2020 was also reflected in profitability, which has also benefited from the programme of cost reduction measures implemented by management in the current and last financial years.

Outlook -

The Company's balance sheet remains robust, with improved cash levels and a stronger liquidity position, as compared with 31 July 2020. This further improvement in the Company's financial position prepares the business for a very uncertain trading outlook in the remainder of the current financial year and in the next financial year.

My opinion - an encouraging update.

.

Angling Direct (LON:ANG)

Share price: 76.5p(down c.3%, at 12:15)

No. shares: 77.3m

Market cap: £59.1m

Update re. Tier 4 Restrictions

Angling Direct plc (AIM: ANG), the largest specialist fishing tackle and equipment retailer in the UK, provides an update on its operations in relation to the UK government's enforced closure of non-essential retail stores in England's Tier 4 areas from Sunday 20th December.

Here are my notes from 14 Oct 2020, when I looked at ANG’s interim results - not bad in the circumstances was my conclusion, and I very much liked its cash-rich balance sheet.

Today it says -

- 12 stores are closed but still doing call-and-collect service

- 26 other stores & websites remain fully operational

- Positive sales momentum reported in Dec has continued

- Remains on track to deliver FY 01/2021 adj EBITDA of at least £3.8m - NB before IFRS 16, i.e. this is a reliable figure for our purposes

- Balance sheet & liquidity remain strong

- Angling is a health & wellbeing activity, which can safely continue

Broker update - many thanks for N+1 Singer for making available an update today, see Research Tree. Forecasts are unchanged, but note they were raised not long ago.

Adj EBITDA of £3.8m sounds good, but that only translates into 2.8p adj EPS, so a PER of 27.3 times - not cheap, but I wouldn’t expect it to be cheap in such a chaotic year.

Matthew, the N+1 analyst suggests EV/EBITDA as a valuation metric, and it looks to be rated at 11.9 times on that metric for the current (nearly ended) year.

Nobody knows how next year is likely to progress of course, but it’s good to see that N+1 has at least put some cautious-looking numbers out.

Having a mix of physical stores and websites hedges ANG’s bets either way.

My opinion - I don’t have a strong view either way on this one. I do like its strong balance sheet, and cash pile. That could allow it more acquisition opportunities, to roll up Mom & Pop type operators, if they want to exit, e.g. for retirement.

The balance sheet strength, and solid trading despite covid, combined with a market cap that’s still quite low, make me probably lean more towards being positive on this share.

.

Universe (LON:UNG)

3.75p (down 12%) - mkt cap £10m

This supplier of EPoS and loyalty systems has been listed for donkey’s years, but never seems to go anywhere. So I really can’t see the point in it being listed. Hence the de-listing risk (instant 50% loss if it announces an intention to de-list) is too big a risk for me.

Today it updates on FY 12/2020.

This reads as a profit warning - a project delay means costs are in 2020, but revenue now deferred into 2021. That sort of thing happens with micro caps, and in a covid year, we can’t really blame management.

Despite this delay, the costs of maintaining COVID-19 resilience, and an increased level of investment, the Company still expects to report a modest level of adjusted EBITDA profitability for the full year.

It says a small and temporary net debt position will exist at the year end.

My opinion - the only reason I would invest in this company, is if it launched a new, game-changing product, that was in very strong demand. Otherwise, why put your money into something that could be a lobster pot, i.e. difficult to exit from?

.

Here's Leon's end of year update from PIWorld - as always with Leon, some stand-out comments (e.g. that formal sales processes usually don't end with a bid). I hadn't thought about that before, but he's right!

.

.

That's it for today! Now I have to prepare something sensible-sounding to say at Mello Monday this evening.

Best wishes, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.