Good morning! It's Paul here with the SCVR for Wednesday.

I had a lie in today, so the first section won't be up until about 11am.

There isn't any company news of interest today, so I've just had a think about M&A instead.

Today's report is now finished.

Mergers & Acquisitions

I was a bit bored over Xmas, so started clicking on cars for sale, always enjoyable but dangerous. Anyway, I've agreed to buy a classic Daimler Double-Six (1990) - in my view the most beautiful saloon car ever made. It will be lovely to just enjoy owning it, to me it's art. I justify the V12 engine on the basis that I'll probably drive it less than 500 miles p.a. therefore the environmental damage is minimal, and offset by my using entirely renewable electricity in my flat.

Here she is - a Japanese import, so in mint condition, only 35k miles from new. The service history is all there, but in Japanese script, so I had to take it largely on trust!

.

.

Anyway, the chap selling it works in the city, for a large overseas bank, doing leveraged buyouts with private equity firms. We were chatting about it, and he told me something interesting. Namely that banks & private equity generally think that they were too cautious in 2008-9, and missed a lot of stunning opportunities to pick up great assets on the cheap. They're determined not to make the same mistake this time, and the deal pipeline is incredibly busy he said.

Particularly with the main Brexit uncertainty now removed (although plenty of loose ends still to be tied up), he reckons there is likely to be a large wave of takeover bids in 2021. A fund manager said something similar in a recent newspaper article, but I can't remember which one.

People sometimes ask me how to identify takeover targets. A good place to start is obviously undervalued shares like Redde Northgate (LON:REDD) (I hold). Even though it's gone up a lot in the last 2 months, it's still irrationally cheap in my view - fwd PER of 8.5 (we can rely on forecasts because it's recently confirmed trading in line), and a divi yield of 6.0%. Combined with a strong balance sheet - what's not to like about that? It's historically been a very cash generative business, paying large divis, which is attractive to private equity. There are existing plans to reduce gearing, by leasing vehicles from manufacturers, instead of buying them. That would free up room on the balance sheet for a private equity acquirer to load it up with debt, which could be gradually paid down from cashflows.

Cloudcall (LON:CALL) (I hold) is another one that might attract interest from a US buyer. It's already got several US investors on the major shareholder list, and does about 40% of its business there. As a reader pointed out yesterday, tech valuations in America are incredibly high, so it makes sense for them to buy in growth from cheaper UK companies.

Boohoo (LON:BOO) (I hold) is growing its sales in America very rapidly, so it would make obvious sense for it to list on NASDAQ or the main market in New York, where it would probably get a much higher rating than here.

Intercede (LON:IGP) (I hold) is a tiddler, but does nearly all its business in the USA, with huge clients, like branches of US Govt, and major aerospace companies. A house broker note did suggest earlier this year that private equity might come sniffing around, who knows?

Victoria (LON:VCP) is another one where the Chairman has made it clear that the business would be sold once it reaches sufficient scale. A huge US private conglomerate recently made a strategic investment in Victoria, and that can often be a precursor to a full takeover bid later on.

French Connection (LON:FCCN) (I hold) is on the pending list. Hopefully at some point we'll be taken out, since the founder probably wants to retire & get the best price he can for it.

Best Of The Best (LON:BOTB) (I hold) - the takeover talks are still ongoing, but as Leon Boros said in a recent interview, when talks drag on this long, it usually falls through. I'm hoping the bid talks do fail, as I want to buy more BOTB shares, and there could be a spike down on a bid falling through.

I can't think of any others off the top of my head, but basically everything is potentially up for sale, if it doesn't have a controlling shareholder to block it.

I normally get 2 or 3 takeover bids in my portfolio each year. Sometimes they can be very lucrative, if the premium is high, and the position size is large. Mccarthy & Stone (LON:MCS) was a cracker - the price was irrationally cheap (way below NTAV, for no reason), and I had a fairly chunky position in it. Unfortunately, I got a margin call and sold a third of them a couple of days before the takeover bid was announced, so I threw away tens of thousands of pounds. However, I'm very much a glass two thirds full type of person, so I was just grateful for the profit on my remaining holding, and tried to block out the lost opportunity from my thoughts. We just have to accept that we'll get some investments right, and others wrong. Learn from each experience, then move on, is my approach.

Any ideas on possible takeover candidates from readers? It would be good to bounce more ideas around. Any sectors that are worth focusing on in particular?

.

No company news today, other than a rambling update from £pos which reads like a sales brochure, telling us why its wellhead gripping system is the best thing since sliced bread walked through the door. It concludes;

While the ongoing COVID-19 pandemic may continue to impact energy consumption levels and timings into 2021, we are confident that the best days for Plexus' proprietary technology lie ahead. Our confidence is based on the combination of the momentum behind the energy transition, the higher level of scrutiny operators are under to avoid and tackle emissions, and the growing pressure to manage costs in the current volatile oil and gas price environment where margins are under pressure. POS-GRIP delivers on all counts. With a capital-light licensing model, a debt-free balance sheet and a proven track record, Plexus is well placed to succeed for the benefit of all stakeholders in the energy transition."

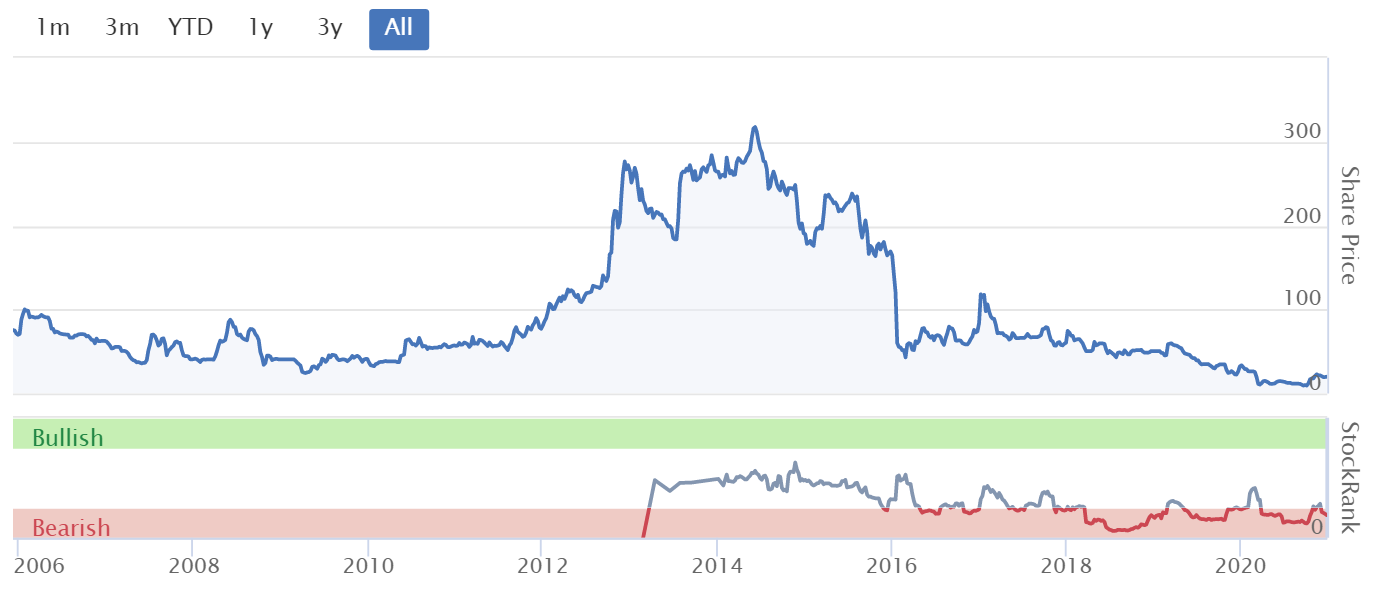

Plexus has been listed for 15 years now, and performance has been poor, as you can see;

.

It would take a lot to convince me that future performance is suddenly going to be good, given this track record.

All done for today, sorry there wasn't anything more interesting to cover.

Obviously it's wonderful news that, as expected, the Oxford/Astrazeneca vaccine has now been approved & will be rapidly rolled out.

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.