Good morning, it’s Paul & Jack here with the SCVR for Thursday.

Timing - This report is now finished.

In case you missed it, I added another section on Science In Sport (LON:SIS) to yesterday’s report in the afternoon. It looks potentially interesting. Here’s the link. The InvestorMeetCompany results webinar recording is now live for SIS, here. I've only watched a bit of it so far, but will report back if there's anything interesting in it.

My diary for today includes a webinar from Eve Sleep (LON:EVE) (I hold) at 13:30 on InvestorMeetCompany.

Empresaria (LON:EMR) is also doing a webinar on IMC at 16:15 today.

I’m so enjoying all these results webinars, it’s great to “meet” management for lots of companies. Small company investing is really all about backing the right people, with the right business models.

EVE has a pretty awful track record, but what’s interesting is that it’s got plenty of net cash, and has pared losses by cutting back on the previously huge marketing spend. It’s trying to develop internet sales. We’re in a bull market, so I thought it could be an interesting punt - very speculative though.

Agenda -

Paul -

Portmeirion (LON:PMP) (I hold) - Review of its FY 12/2020 results.

Eve Sleep (LON:EVE) (I hold) - quick review of FY 12/2020 numbers - a big reduction in losses, and plenty of cash.

Empresaria (LON:EMR) - fairly resilient in 2020, but 2021 recovery sounds hesitant.

Jack -

Gym (LON:GYM) - Full year results dominated by fact that sites were closed for 45% of full year trading days; set to reopen from 12th April

Capital (LON:CAPD) - strong results from this mining services provider, with an equally encouraging near-term outlook

Paul’s Section

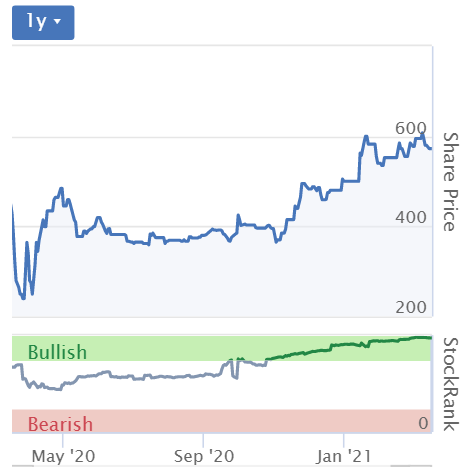

Portmeirion (LON:PMP)

(I hold)

572p (pre market open) - mkt cap £80m

The share price chart here looks the same as everything else - plunging on covid in March 2020, then a bounce, flat over the summer, then a 50% gain since Nov 2020. I do sometimes wonder if there’s much skill in stock-picking, when you could have been long practically anything and made a similar gain in the last 6 months!

.

Results webinar - is being held tomorrow (19 March) at 11:30. Open to all, just click on the link.

Strong recovery in H2, ahead of market expectations

To be fair, I think the bar was set very low, so beating expectations isn’t particularly enthralling. Looking at the graph below, we can see how the darker blue line denotes EPS forecasts for FY 12/2020. When introduced pre-covid, the forecast was for nearly 82p EPS. That was then reduced to practically zero after covid struck.

.

Seasonality is important with PMP - it makes most of the profit in H2 each year, because a lot of its products are linked to Christmas & gifting.

See the table below, which I was delighted to discover buried in Stockopedia’s “Accounts”, then “Income Statement” area, which you then toggle to “INTERIM” and you then see sequential half years, enabling us to easily spot the seasonal trends for any company.

I’ve highlighted the H2 figures, to demonstrate how much more profitable H2 is than H1 -

.

In H1 2020, the company suffered, but not as much as I had feared, with revenues down about 8%, and instead of the usual £0-2m H1 profit, it made a “headline” (i.e. before some (small) adjustments) loss of £(2.67m).

H2 2020 was better, as expected, due to the seasonality, but still impacted by covid lockdowns. It made a headline profit before tax in H2 of £4.1m.

Full year 2020 figures, adding those two halves together, arrives at a modest £1.4m headline profit before tax, down 81% on 2019. Pretty bad, but that’s to be expected in the circumstances.

Online sales - this is a key area of focus, and is one of the main reasons I’m holding this share in my personal portfolio. Companies that are pivoting towards online sales, is a key area of focus for me, because the potential rewards are stellar if they get it right. Look at Best Of The Best (LON:BOTB) (I hold) where it gradually closed down the airport physical sites, to focus on growing its internet revenues. The closure of airport sites masked the decent growth online. It took them a few years to crack the digital marketing side of things, but the results this year have been staggering. When I started buying at about 120p per share, I never imagined it would be a 25-bagger in about 7 years! But given that an internet-based competition opens up potentially an almost unlimited global market, then the upside really is open-ended.

With that in mind, I very much like the more ambitious strategy of PMP’s new CEO, with particular focus on driving direct internet sales - which are higher margin too, because PMP gets both the wholesale and retailer’s margin. Although some costs are also higher, holding more stock, picking & packing, postage, customer returns, etc.

In particular, we have continued our transformation to a more online and digital based business and were pleased to see 69% sales growth in our own online website sales and that 47% of total sales in our core UK and US markets now go through all online channels (2019: 30%). We will continue to invest in this area and our capabilities and expect to see further growth in the years ahead.

That’s a good enough reason for me to continue holding PMP shares - the internet strategy is working, and delivering strong growth. Lockdowns will have helped drive up internet sales obviously, as physical retailers will have been closed at various times. Most companies seem to be saying that lockdowns probably accelerated existing trends to move business onto the internet, so I reckon this growth could continue, even when the shops have re-opened.

I bought some lovely “Botanic Garden” pottery from PMP, to test out the product & service, as mentioned here before. The product is lovely, and arrived well packed & unbroken. I now get (probably too many) emails from Portmeirion, with special offers, etc. I’ve subsequently bought more Botanic Garden products from them, twice. The point being that online sales create a direct relationship with the consumer, which PMP can then exploit for potentially many years. Its products are collectable, and of course get broken from time to time, so customers would I think have a good lifetime value. It would be interesting to find out what the key eCommerce statistic of LTV/CAC is (estimated lifetime value, divided by customer acquisition cost).

Balance Sheet - looks very good to me. Note that PMP raised £11.2m in a placing in June 2020, which greatly strengthened the balance sheet. However the dilution means the share count has gone up from 11m to 14m shares, which is a pity, as future EPS is not likely to reach previous levels due to that larger share count.

Net cash is £0.7m

There’s a small pension deficit, but it’s costing £0.9m pa. in recovery payments, which is material to profits, but should recede as a percentage of profits/cashflow when trading improves. Unhelpful though, and it needs to be factored into our valuation calculations.

Valuation - EPS was a statutory loss of (6)p, vs 54.6p in 2019. Ouch!

The “headline” EPS was only 4.95p (2019: 56.24p). So technically the PER is a nonsensical 115 times. Of course it doesn’t make sense to value the shares on a one-off bad year. It’s more logical to calculate what earnings the company might generate once more normal conditions pertain.

Many thanks to analyst Sahill Shan at N+1 Singer, who has crunched the numbers for us, and published an update note today on Research Tree. He has pencilled in only a modest increase in revenues of 2.5% for 2021. That looks eminently beatable to me. He’s assumed higher margins I think, so EPS shoots back up, from 5.0p in 2020, to forecast 36.4p in 2021 and 56.8p in 2022. His commentary indicates “upside risk” (i.e. forecasts could be beaten) if current recovery momentum is maintained.

Hence the forward PERs are 15.7 and 10.1 - good value in particular on the 2022 forecast, if it is achieved. Although I can see how some investors might want to wait for more evidence that the recovery is indeed underway, before committing.

Dividends - this used to be a high yielding share. What a pity they didn’t keep more financial reserves, as then we wouldn’t have suffered c.27% dilution in the equity fundraise in 2020. I hope companies learn from the pandemic, and beef up their balance sheets, rather than running up debt and paying excessive divis, which then leaves them in a mess when something unexpected goes wrong.

There are no divis for 2020, but PMP says today that it intends to re-commence divis in FY 12/2021. Personally I’d prefer them to grow the business faster, rather than resuming divis.

Outlook -

Covid - continues to disrupt in Q1 due to lockdowns - no surprise there.

This bit looks really good -

However, the strong growth we have experienced in online sales channels has mitigated much of the impact of retailer shutdowns and we are pleased by the improving trend of sales performance we saw in the second half of 2020. Encouragingly, we have continued to see this improving trend in the first quarter of 2021 and therefore remain confident of returning to sales growth in 2021.

My opinion - I’m happy with this overall, and will continue to hold for the long-term.

There seems good recovery potential in 2021, and I particularly like the strong online growth, which is now almost half all business.

I think PMP’s brands have untapped potential, with scope to widen the product ranges beyond just pottery & candles - e.g. hand and body care ranges are being introduced, which is a terrific idea. I’d like to see PMP’s brands become more lifestyle brands, and sell them mainly online, maybe even create a “marketplace” as leading fashion brands are doing, to become a portal selling lots of things from other companies too, earning commissions, without having to hold any stock, or handle/despatch the goods at all.

In the background, I think there’s always the chance a bidder from the USA could come knocking on our door. That’s fine by me, if they offer 1000p+ then I’d happily accept!

Has the strong share price in the last 6 months been justified? I think so, yes. For now, I think this share looks priced about right, and for me is a long-term hold.

Stockopedia really likes it - a very high StockRank, and it has a “Super Stock” classification too.

.

.

Eve Sleep (LON:EVE)

(I hold)

6.1p (down c.2%, at 11:57) - mkt cap £17m

As mentioned above, this company sells mostly memory foam mattresses, mainly online now I think.

It seems to be popular with traders, as the volume is surprisingly high for a micro cap - e.g. 17.3m shares have already printed so far today, that’s over 6% of all the shares in issue, just this morning! Hence expect price volatility here, as hoards of traders stampede in & out, sometimes after ramping/deramping it online.

We keep things fact-based here, so here are my notes from reading the accounts out today for FY 12/2020 -

- Revenue £25.2m (up 6% on 2019) - helped by lockdowns & home improvements trend

- Gross profit margin is high, at 57.3% (up from 53.1% in 2019)

- Various new definitions of profit are presented! Let’s stick with real profits, i.e. profit before tax - this is a loss of £(2.4)m in 2020, dramatically improved from £(12.5)m in 2019

- Marketing budget halved, but still substantial at £6.1m - giving further cost flexibility if needed

- Exited from selling on Amazon (too costly), and simplified IT by moving to Shopify - management seem to be doing lots of common sense things to focus on achieving profitability

- Current trading strong in Jan & Feb 2021, up 16% on 2020, due to easing of supply constraints

- Growth rate expected to slow in May 2021, as tougher prior year comparatives kick in (good transparency by disclosing this)

- Balance sheet - quite good, with NTAV of £6.2m, and a cash pile of £8.4m - looks ample, so probably won’t need to raise more equity. Note extremely low inventories, which would need to normalise at some stage.

- Retained losses of £(43.9)m means it won’t be paying corporation tax, if it does achieve profitability

- Share based payments of £522k in 2020, and £1,111k in 2019 - why? Call me old fashioned, but I wouldn’t expect to see share giveaways to management at all, at a loss-making company

- Cashflow statement - self-explanatory. Note £12.0m equity raised in 2019, and it capitalised £291k into intangibles - insignificant.

My opinion - we’re in a bull market, so that can be a good time to do some trades on micro caps that might attract a stampeding herd of punters. Judging by the high volumes traded, it looks like EVE is already on their radar.

With a cash pile about half the market cap, meaningful sales at a decent gross margin, and flexible overheads, this share could do alright.

Webinar starts on IMC shortly, at 13:30.

Overall, after going through the numbers, I feel that holding this share is not as daft as you might think (that’s a new classification, I quite like it, so will use that again, for speculative shares!). I think this share is best seen as a speculative special situation. So not for widows or orphans.

Note the Altman Z-score is terrible at the moment, I presume because it thinks the cash burn is still horrendous, but as the results today show, it has been almost eliminated. Therefore this score should improve when the data is updated.

.

.

Empresaria (LON:EMR)

49p (down c.3% at 13:02) - mkt cap £24m

Very small and illiquid, so I’ll keep this brief.

Empresaria, the global specialist staffing group, reports its unaudited preliminary results for the year ended 31 December 2020.

It’s obviously been a hugely disrupted year, so I think these highlights look quite good in the circumstances, and adj EPS of 4.1p seems to be slightly above the 3.98p broker consensus, so a small earnings beat -

.

Signs of recovery, as we’re hearing from other staffing companies too.

· 2021 guidance reinstated

· Resumption of dividend with a final dividend of 1.0p per share proposed (2019: nil)

Outlook comments seem surprisingly hesitant - I was expecting something much better than this -

Early indications of trading in 2021 are positive and although, due to our strong start to last year, adjusted profits for the first half of 2021 are likely to be behind the first half of 2020 we expect for the full year to deliver adjusted profits in line with or better than 2020. We enter 2021 well positioned to exit the pandemic stronger than we entered it and to take advantage of recovery in our markets."

It’s a concern that EMR is not expecting to beat H1 2020, given that Q2 would have been battered by covid lockdown 1 last year. Maybe lockdown 3 is having an impact this year? Ah yes, here we are -

... The increased level of national lockdowns and restrictions in several of our markets at the start of 2021 means we remain cautious on the immediate outlook, but believe we are well placed to take advantage as and when markets recover.

Balance sheet - looks rather weak. Take off the goodwill/intangibles, and NTAV is negligible, at £(0.6)m.

My opinion - the 2020 PER is 12.0, which looks about right to me.

For that reason, the weak balance sheet, and given that it sounds like 2021 might be about the same profits as 2020, I don’t see any reason to chase up the share price any higher for now.

The StockRank is strong though, so maybe I’ve missed something?

.

.

Jack’s section

Gym Group (LON:GYM)

Share price: 246.8p (+2.8%)

Shares in issue: 165,977,131

Market cap: £409.6m

Gym (LON:GYM) operates 186 low-cost gyms across the UK.

Pre-Covid, this was a promising Leisure sector roll out tapping into huge demand for affordable gym facilities. It’s only other real rival in the budget space was Pure Gym.

Then Covid happened and Gym’s sites were required to close for 45% of the trading days in the year. So these full year operating numbers will be ugly.

Given the pretty unique events of the past year, I’m not sure the risk:reward has ever been that attractive here over the pandemic period. I’ve found that with a few Leisure stocks actually, and I’ve been on the look out.

That’s less of a comment on the quality of any one operator and more a nod to the immense, existential risks that these companies have faced down, the debts they’ve taken on, and the equity they have raised. And, in some cases, the equity that they might still need to raise. Prices never got quite as low as I thought they might for some operators.

But, on the other side of the equation, we probably have a lot of pent up demand for gyms, pubs and the rest - so perhaps a normalisation boom in trade could paper over the cracks and justify the recovery in share prices.

Full year results for the year to 31 December 2020

- Revenue -47.4% to £80.47m,

- Adjusted EBITDA less normalised rent -120.9% to -£10.17m,

- Adjusted profit before tax -433.1% to -£46.53m,

- Statutory PBT -858.8% to -£47.19m,

- Basic adjusted EPS -397.4% to -22.9p; basic statutory EPS -988.5% to -23.1p,

- Free cash flow -151.2% to -£16.54.

The fact that these adjusted losses come after significant government help is quite sobering and the readacross for smaller, less well funded businesses remains a concern.

But assuming The Gym Group makes it through to the other side, which is increasingly likely now at least for most affected listed entities, then the results of the past year are obviously exceptional.

Debt is manageable, dividends have been cut, and cash flows should return once people can come back to gyms. But I also wouldn’t rule out another placing, especially at these share prices.

Eight new gyms opened in the period, increasing the total estate to 183. The company will also be hoping it can recover membership levels from today’s 547,000 to the 794,000 average for FY19. So there is cause for optimism.

The group also gives some useful guidance on the outlook:

- Gyms in England are expected to re-open on 12 April 2021 with gyms in Scotland re-opening 26 April 2021,

- Lockdown have seen successively higher customer retention rates. As at 28 February 2021 Gym’s membership level was 547,000 (31 December 2020: 578,000, and 794,000 at the start of 2020)

- 97% of current members say they expect to return to the gym as soon as possible, with 75% stating that fitness will be more important to them than it was pre-COVID,

- Focus on cash management; as at 28 February 2021, Non-Property Net Debt was £58.2m versus total bank facilities of £100.0m,

- Three new sites opening in April and one in May, with an additional four starting on-site imminently,

- A growing pipeline with six leases exchanged and several more in advanced negotiations.

Conclusion

I like The Gym Group but the main sticking point is valuation.

A lot of recovery is baked into the share price. In fact, a lot of growth is baked in. Meanwhile, paying members have fallen from 794,000 at the start of 2020 to 547,000 today and the group has raised £39.9m from shareholders, diluting the share base.

Harking back to the FY19 results, which were generated from 796,000 members rather than today’s 547,000, and with around 138m shares in issue rather than today’s 166m, the group generated net profit of £3.6m. Using the new shares in issue number, that would make for about 2.2p of FY19 EPS.

So getting back to that point would value Gym at 109x FY19 basic earnings per share. Taking the significantly higher FY19 ‘normalised income’ figure of £9.02m gives diluted normalised EPS of 5.4x with the newer shares in issue number, which means a recovery to FY19 levels would value the group right now at 44x normalised earnings. It just seems too expensive.

That said, I imagine quite a lot of lapsed customers will return to gyms and bring membership numbers closer to the FY19 average of 796,000 in relatively short order once gyms open up from 12 April. And it's also worth noting that operating cash flows typically far exceed the group's earnings per share figures.

Maybe some investors are more certain of the group’s growth prospects going forwards but, given the above and the recovery in share price, I don’t see too much of an opportunity here for now.

I do think the group has some good trading ahead of itself over the next year or two and budget gyms remain an attractive proposition. Providing affordable fitness is even more relevant as society is encouraged to improve health and recover from a global economic shock. The longer term growth thesis is sound.

A combination of market share gains, a post-lockdown surge in applications, and more readily available quality sites selling for cheaper could lead to pretty striking results over the next year or two.

But it’s my view that more attractive risk:reward opportunities lie elsewhere in the market right now. In some quarters, the ‘reflation’ trade looks a little overdone.

Capital (LON:CAPD)

Share price: 67.7p (+10%)

Shares in issue: 188,780,903

Market cap: £127.8m

Capital (LON:CAPD) provides ‘full-service mining, drilling, maintenance and geochemical analysis solutions’ to miners with operations in Africa. It has a young and expanding fleet of bulldozers, dump trucks, and mining shovels, as well as a fleet of 99 rigs.

There’s a lot of talk about commodities at the moment and it probably shouldn’t come as a surprise that business is good right now for Capital.

Can this continue? If so it might not be too late to climb on board here, even after today’s 10% rise.

- Revenue +17.5% to $135m,

- EBITDA +24% to $33.8m,

- Net profit after tax +138.6% to $24.8m,

- Cash from operations +34.6% to £36m,

- Diluted earnings per share +130.9% to 17.6c,

- Total dividend per share +57.1% to 2.2c,

- NAV per share +68.3% to 106c,

- Year end net cash balance of $5m ($35.7m of cash and $30.7m of debt).

EPS growth has been driven not just by strong operating performance but also by ‘substantial realised and unrealised investment gains’ across a portfolio of junior and mid-tier exploration and mining companies.

The year end investment portfolio was valued at $27.2m (2019: $12.5 million), recording investment gains totalling $13.6m, comprising $13.2m unrealised and $0.4m realised.

Capital's portfolio of long-term mine-site based operations increased to ten sites, comprising 18 individual contracts with the addition of the new contracts with Barrick in Tanzania and Firefinch in Mali. Partners include some familiar names like Barrick, Centamin, and Hummingbird.

There’s a lot of detail and contract activity here so I won’t go into the weeds too much. Suffice to say business is booming right now. Capital was awarded multiple new exploration contracts over the year, mostly in the West African region.

One specific contract worth flagging is the December 2020 award of a ‘transformational’ 120Mt waste stripping contract including load and haul and ancillary services, and an expansion and extension of the existing drilling contract at Centamin's Sukari Gold Mine, Egypt.

Together, these are expected to deliver US$235 - $260m of incremental revenue over a four-year term. It is Capital’s largest award of new business since inception, marking a ‘step-change in the scale of the business,’ and is expected to be earnings accretive by the end of the year.

Capital also completed an oversubscribed equity fundraising back in December that ‘introduced a new roster of quality institutional investors’. Gross proceeds of approximately £30m are being used to support the Sukari contracts together with key debt financing facilities.

Capital has also successfully agreed a further debt facility for up to US$17.0m of which US$6.5m is committed and available subject to finalisation of security.

Clearly, the group is scaling up. This is promising, but mining is also cyclical and so this brings risks should the industry suffer a downturn. Debt levels are probably worth keeping a close eye on.

For now the momentum looks good. Post year-end contract awards include:

- Three-year contract for surface delineation and open pit grade control for AngloGold Ashanti, Tanzania (previously announced);

- Three-year contract for underground delineation and grade control drilling for AngloGold Ashanti, Tanzania (previously announced);

- Initial six-month delineation drilling contract for Allied Gold Corp, Mali;

- Exploration drilling contract for new client Cora Gold, Mali;

- Exploration drilling contract with Perseus Mining in Côte d'Ivoire;

- Initial six-month delineation drilling contract with Aya Gold and Silver Inc in Mauritania; and

- Six-month exploration drilling contract for Endeavour Mining Corporation, Burkina Faso.

Conclusion

These are strong results and Capital looks well placed for a continued pick up in Africa-based mining activity. I don’t think we’ve missed the boat here.

Some big institutions have been buying in and, given the results and outlook, the share price looks cheap. Diluted EPS of 17.6c puts the group on about 5.4x FY20 earnings.

Capital guides to revenue of between $185m-$195m for FY21 and demand for drilling services ‘has increased strongly from Q4 2020, building further in Q1 2021’. MSLABS is working at near full capacity across all major laboratories.

MSLABS also sounds interesting - this is a global provider of geochemical lab services serving the exploration and mining industries. There could be growth potential here.

Given the buoyant outlook the shares do look cheap at the moment and I think it’s well worth spending a bit more time getting to know this company.

True, at some point there could be a downturn in mining activity, but there seems to be a disconnect between the positive outlook and today’s share price even accounting for the 10% rise.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.