Good morning! It's very quiet for news again today. Although the floodgates are about to open next week, as we start to get the 31 Dec year end results coming through.

Naibu Global International Co (LON:NBU)

(shares suspended since 9 Jan 2015)

Update - there's never really been any doubt in my mind about the likely outcome with this small Chinese company which listed on AIM. For starters, there was no logical reason why it needed to list on AIM at all - why would a profitable company, with plenty of cash, which operated on the other side of the world, need to list its shares in London?

Also, there was wave after wave of selling from insiders - numerous large blocks of shares were dumped on the market in secondary placings, at below the prevailing market price, irrespective of how irrationally low the valuation got. Again, a massive warning sign that things are not what they seem.

The answer seems to have been that the company realised that listing its shares in London would be a good way to extract money from gullible investors. The truth is, if you buy shares in a Chinese company, you don't really know what you're getting at all. You are just getting a piece of paper (or electronic equivalent) which purports to show that you own part of a business in China that you have never seen, and can't even be sure exists at all.

Anyway, after today's announcement I suggest that shareholders get their Naibu share certificates framed, and put them on the loo wall as a reminder not to be so gullible in future.

As for shares in any other UK-listed Chinese companies, my stance is totally clear - I would dump the lot. You can't rely on the accounts, you can't rely on management, and one should be highly suspicious of why these companies came to list in the UK. All too often I'm afraid the reason is far from honourable. Maybe there are some legit Chinese companies in the UK market, but how on earth do you identify which ones are, and which ones aren't? And why take the risk at all?

This statement today makes it abundantly clear that the game is up;

I had a lot of abuse thrown at me due to my consistently bearish view on this share, on bulletin boards. Therefore the culprits may now form an orderly queue, and apologise. Of course they won't apologise, that type never does. Not that it matters to me - helping to safeguard readers' interests here is more important than anything else, and on that front I can pat myself on the back and say "job well done!"

Mi-Pay (LON:MPAY)

Share price: 25p

No. shares: 34.0m

Market Cap: £8.5m

Placing & trading update - this company is a new one to me. It describes itself as providing, "fully outsourced payments solutions to digital ecommerce clients". That sounds a bit like PayPal to me. There are lots of payment companies around, so it's difficult to see how something this small can compete, or become profitable.

Although this is a peculiar area of the market, where investors seem to completely disengage from normal scepticism about loss-making companies, and attribute very high valuations to companies which consistently lose large amounts of money, e.g. Monitise (LON:MONI) or Earthport (LON:EPO) . Jam tomorrow seems to attract a big premium in this sector for some reason.

Looking back, Mi-Pay seems to have come about from a reverse takeover of a cash shell called AimShell Acquisitions, back in Apr 2014. Clearly the £2.8m cash in the shell company, and a further £1.3m raised in equity and loan notes, has proven to be inadequate, as another Placing has been announced today to raise £1.75m (before expenses, so probably closer to £1.5-1.6m after expenses) at 23p per share.

Note that, as is so often the case, the share price began to plunge just before the Placing was announced. I wonder why?!!! Clearly news of the company needing to raise more cash has leaked out (it usually does sadly with smaller caps). Anyone trading the shares with knowledge of a Placing coming, is insider dealing - breaking the law. It's scandalous how so many cases of possible/probable insider dealing seem to occur without the regulators even noticing, let alone doing anything about it. This is yet another aspect of the London market which makes me despair.

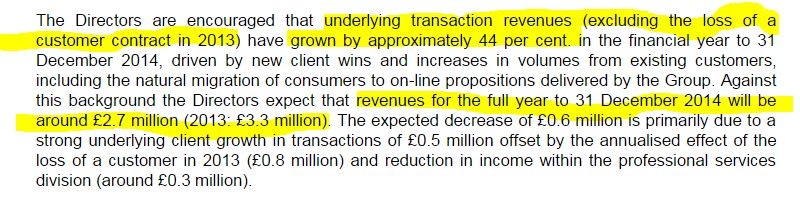

Top marks for creative accounting go to Zeus, where they manage to turn an 18% fall in turnover into 44% growth, by ignoring the loss of an existing client!! Brilliant stuff!

I bet all companies wish they could ignore all contract losses, and only report growth! That way you would never see sales decline!! Even if sales fell to zero, you would still be flat against last year, on underlying revenues, by this definition! Bonkers - but if people believe it, and are happy to put money into the fundraising, then that's their call.

Outlook - the company says it is targeting a cashflow breakeven monthly run rate by the end of 2015. The company also mentions a contract win with Sun Cellular in Asia, with 20m pre-pay users, which they say has significant potential, although they say "take up ... to be gradual".

My opinion - I don't really understand why people punt on early-stage, loss-making companies like this, unless there is a clear route to profitability which is likely to succeed. Otherwise it's just punting. This fundraising looks to be EIS qualifying, which greatly improves risk/reward, so perhaps it might make sense to people investing on that basis (where you get tax relief against the money going in, and more relief against losses, and CGT-relief on profits).

However, I can't see any appeal about this share for people buying in the after-market, who are not getting EIS relief.

Generally I would say that small loss-making companies which pop up on AIM in sectors which are fashionable, so mentioning buzzwords like the cloud, or mobile, etc, are usually a dismal failure. The overwhelming majority of them do not work out. Why take the risk of giving them the benefit of the doubt?

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.