Good morning! I have to rattle through things this morning, as there's still some more preparation to be done for the ShareSoc Masterclass this afternoon, where I've been asked to join a panel and talk about one of my favourite topics - balance sheets!

Tungsten (LON:TUNG)

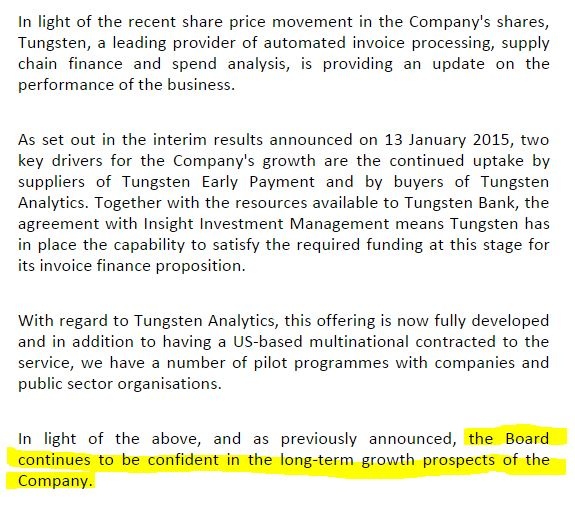

After the shorting attack, this stock appeared to be bouncing yesterday, so I tentatively dipped my toe back in the water at 150p (more as a short term trade, for a bounce, rather than me having particular confidence in the company longer term). They closed at 160p last night, so far so good. I thought it likely that the company would put out an update to the market, given the big share price decline, and they did - but I'm afraid it seems a damp squib to me - market update:

My opinion - as reported yesterday, I have listened to the bear arguments on this share, and whilst some seem irrelevant, others do resonate - especially concern over what take-up there is likely to be for the invoice discounting service. I suspect the target of 10% of all invoices flowing through their system might prove to be wildly optimistic, but that's just my hunch.

I ditched my trading position (opened yesterday at 150p) in the opening auction this morning, at breakeven, so am now back safely on the sidelines, and will watch developments with curiosity. Will the share price go up or down? I have absolutely no idea, that's entirely driven by market sentiment (since this company is impossible to value reliably on fundamentals at this stage), which can ebb and flow unpredictably. Although I suspect there might be more downside from the current price of 147p unless TUNG is able to put out a much more convincing rebuttal re the shorters. There again, other companies which put out detailed rebuttals of shorting attacks have found that it just opens up an even bigger can of worms. So perhaps ignoring it & letting the figures do the talking in due course is the best course of action from the company?

I suspect TUNG may need to raise more share capital, given the large short term losses it is incurring to bring new clients on board.

AO World (LON:AO.)

A profit warning this morning has whacked the shares of this online electricals retailer.

I am not allowed to comment on it, under the editorial rules here, as I have held a short position in this share for some time.

Coms (LON:COMS)

Share price: 0.9p (down 60% today!)

No. shares: 973.3m

Market Cap: £8.8m

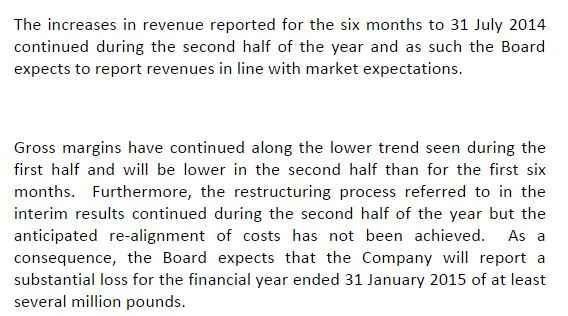

Profit warning - oh dear, things seem to be unraveling rapidly here. Here is the key part of today's statement;

My opinion - after reviewing its last balance sheet, this company doesn't have several million pounds to lose. There was only £974k in the kitty when last reported, at 31 Jul 2014, and a deferred consideration payment of £825k made on 10 Nov 2014 will have used up most of that.

By my calcs that deferred consideration payment would have taken the current ratio down from a weak 1.01 to a weaker 0.95. That's before accounting for what sound like substantial losses in H2.

Worse still, there are management issues - in an embarrassing gaffe the first announcement today says that the CEO has requisitioned an EGM to boot out two Directors (one of whom has just become the acting FD!) and replace with 3 other people. Then another announcement came out this morning saying that EGM requisition had actually been withdrawn yesterday, so should not have been mentioned.

EDIT: I mis-read the second RNS, my apologies. It turns out that only one of the resolutions for the EGM has actually been withdrawn, so the EGM is still going ahead for the other resolution(s). Thanks to the two readers who pointed this out to me.

You couldn't make this stuff up. It's clearly a company in chaos, with weak finances, so I think the risk of insolvency must be extremely high now. Hence it's gone on my bargepole list.

This has been a disaster for investors, and I suspect it won't be long until it becomes a 100% loss.

Tristel (LON:TSTL)

Share price: 82.2p (up 6% today)

No. shares: 40.7m

Market Cap: £33.5m

Interim results - for the six months to 31 Dec 2014. I don't have time to read all the narrative, to this will just be a very quick skim.

Right, have done my quick skim, and it all looks fine to me. Good progress on sales (up 15.1% vs last yr's H1), and EPS is up 85% to 1.91p for H1. Although note that is flattered by there being no minority interest this year - so it looks like the company has bought out a minority shareholder in a subsidiary.

Balance sheet - looks great, with net cash of £2.9m, and an excellent current ratio of 3.13, so very much a sleep soundly at night share.

Valuation - looks about right to me. It's not cheap, but the quality scores are good, balance sheet is strong, divis are not bad now (nearly 3% yield), and the company has a good track record of delivering solid growth.

My opinion - I like it. In my view this is the sort of small growth company that could make a good long-term hold for a SIPP. Although there's probably not that much immediate upside, I imagine this share will probably do well in the long run.

The products are consumables, so demand should be predictable, with hopefully a low risk of a profit warning. International growth seems steady, and the outlook statement sounds reassuring to me (see below);

Molins (LON:MLIN) - this tobacco machinery company reports prelims for the year ended 31 Dec 2014 today. Shares are down 10% to 81p.

Avingtrans (LON:AVG) - Interim results to 30 Nov 2014 are out today, and have triggered a 10% share price fall here too, to 104.5p.

Thorntons (LON:THT) - I see these have fallen further, to 68p so am glad I've avoided this.

RTC (LON:RTC) - good news here from this tiny recruitment company, with the shares up 36% to 54.5p on a very positive-sounding contract win announcement with Network Rail, and upbeat Directorspeak. A 5-year contract with a value of £80-100m suggests £16-20m p.a., although this is low margin work remember, because the contract value will include the subcontractor wages. Who knows what the net margin to RTC is? Even if it's only say 3%, then that's a £480-600k boost to annual profits, which looks material given how small the company is.

Gotta dash, see you tomorrow!

Regards, Paul.

(of the companies mentioned today, Paul has no long positions, and is short of AO.)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.