Good morning from Paul & Graham! Today's report is now finished.

We've hit the ground running today, as Graham had a second wind yesterday afternoon & has prepared some extra sections for today's report.

Agenda

Paul's Section:

OnTheMarket (LON:OTMP) [quick comment] - announces a new share dealing facility, which looks designed to match up buyers with sellers from the expiry of 5-year lock-ins from the IPO in Feb 2018. This relates to both management, and estate agents that are also shareholders (some were given free shares in return for signing paying contracts). Zeus and Shore Capital will be looking to find buyers for the loose shares which might cause an overhang in the market, if holders try to sell individually. Sounds a sensible plan to me, but it is a reminder of the unusual shareholding structure with this company, which could suppress the share price next year if there are not enough ready buyers to absorb sellers’ shares. (no section below)

Sosandar (LON:SOS) - breakeven interim results (the slower half), and in line with expectations (PBT £2.0m) for FY 3/2023 outlook comments. Things look very good to me. Superb organic growth of +72% in H1 revenues. Big increase in inventories should unwind in H2, and cash looks fine - little if any risk of any more placings. Seems to be shrugging off the consumer downturn. Looks very good to me, as a long-term hold, so a thumbs up. More detail below.

React (LON:REAT) [quick comment] - says that trading in Q4 of FY 9/2022 was “especially strong”, and this has continued into the new financial year, where mgt sees an “optimistic outlook”. Today’s update seems to be a repeat of the TU on 26 October, but with less detail, so what’s the point? Maybe they want to get the share price up, to do another placing? This is the fundamental problem with REAT - it’s too small, and shares too cheap, to add value from acquisitions funded by discounted placings. The business itself actually looks potentially interesting. So if they can crack the problem of excessive dilution in discounted placings, then it might work. Worth keeping an eye on, I reckon. (no section below).

Access Intelligence (LON:ACC) [quick comment] - down 27% to 64p, on a badly received trading update. I took a dim view of this company when last looking at it in Jan 2022 here. Guidance for FY 11/2022 says it's ahead of expectations, with £65.6m revenues, and adj EBITDA of £2.3m. Although bear in mind its breakeven H1 adj EBITDA became a £(4.3)m adjusted loss, and a £(7.6)m statutory loss, so we can take EBITDA with a pinch of salt, as it’s capitalising a lot of costs (£3.5m development spend in H1 alone). Cash position looking tight now at £4.8m (down from £9.3m at end May 2022). Waffly commentary talks about slowdown in order intake in USA, and difficulty converting pipeline into contracts. Weakish balance sheet. Looks risky to me, I’d steer clear. (no section below)

Dianomi (LON:DNM) [quick comment] - this is a new one for me, but it’s come up on the top fallers list today, down 15% on a trading update. It’s another 2021 float that’s done badly - down almost 80% from Sept 2021. Dianomi provides digital advertising services. Adj EBITDA for FY 12/2022 is expected to halve vs LY (LY: £3.1m). That should translate into an actual profit, as the only reconciling item between EBITDA and operating profit, was £250k in share based payments in H1. Cash is £10.8m at end Nov 2022. The last balance sheet was excellent, and it’s not burning cash. This actually looks quite interesting, with about a third of the market cap being net cash. Accounts look clean, with no capitalised development spend. Might be worth a look, if you understand digital marketing. (no section below)

Zytronic (LON:ZYT) [quick comment] - only £14m mkt cap, so we’ll keep this brief. FY 9/2022 results are out today. This bespoke touch-screen maker has suffered from legacy contracts winding down, so £12.3m revenues are now only about half historic levels. Despite that, it remains (modestly) profitable at £0.7m, paying divis too, and has done big share buybacks. Fantastic balance sheet, with freehold & long leasehold property, plus £6.4m net cash. Some supply chain issues persist, but it’s rebuilding the sales pipeline. Risk:reward looks excellent with the balance sheet protecting the downside, and potential upside if new orders are won, which are coming through again in some sectors. Thumbs up from me, if you can cope with something tiny & illiquid - so it’s not one to trade, more a long-term value, special situation I’d say. (no section below)

Synthomer (LON:SYNT) [quick comment] - I’ve been meaning to look at this for a while. Today it announces the disposal of a division for £199m (net), a substantial amount. However, the last H1 accounts show that what looks like a spectacularly badly-timed acquisition was done earlier this year for £760m, increasing net debt from £114m to £993m. Its banking syndicate relaxed covenants to end 2023 (announced 20 Oct 2022). H1 PBT fell by more than half, to £115m. A trading update within today’s disposal announcement doesn’t sound good, with customers de-stocking. It also mentions deteriorating macro conditions originally impacting European operations, now extending to outside Europe. Dividends have been suspended until end 2023. Risk of a dilutive fundraise strikes me as high. This share looks complicated & risky, so I’ll steer clear. (no section below)

Global Ports Holding (LON:GPH) [quick comment] - up 9% to 120p today after interim results announced, which means it’s now bounced c.50% from recent lows. This is another special situation. It owns ports for cruise ships, so revenues have strongly bounced back, and there’s a decent operating profit of $21.9m in H1. The trouble is, finance charges exceed that, at $(27.5)m, so overall it’s loss-making. The group structure looks odds, with a large “Non-controlling interests” line below the P&L. The balance sheet looks horrendous, with large negative NTAV, and mountains of debt. So it looks a high risk:high reward type share, where the equity looks little more than a call option, in the hope that lenders remain docile. The auditors have given it a clean going concern statement today, which is interesting. The main research area would be investigating the terms of the debt mountain. The major shareholder owns 63%, an additional risk. Could be an interesting speculation, for high risk punters. (no section below)

Frp Advisory (LON:FRP) [quick comment] - this is another business advisory services group, like BEG, but higher up the food chain in terms of clients & deals. Hence its shares have been buoyant this year as a counter-cyclical business, benefiting from more insolvencies. H1 results today show adj EPS up slightly at 3.35p (H1 LY: 3.25p). About half is paid out in divis. Net cash of £21.0m, and sound balance sheet. Cenkos has 7.8p adj EPS for this year forecast FY 4/2023. At 159p per share, that’s a PER of 20.4x, which strikes me as over-priced, although in a recession it might out-perform. In line full year outlook. This type of business has a structural conflict between the interests of the partners, and the outside shareholders - e.g. partners were invited to sell 20% of their holdings in a secondary placing, in return for a lock-in extended to June 2024. The risk is, at some stage, the big earners might leave, and outside shareholders are left with the bathwater. It’s not for me. [no section below]

Synectics (LON:SNX) [quick comment] - a £20m mkt cap CCTV company. Today’s update says FY 11/2022 is now expected to be “slightly ahead of market expectations”, due to H2 improving on H1. Says it’s coping OK with inflation & supply chain issues. Net cash roughly flat, at £4.1m. LAst balance sheet at interims looks OK. It sounds as if the business is recovering from the last couple of years’ problems with the pandemic & supply chains. Could be a recovery share from here, quite good value. Thumbs up from me, on the basis that it’s not the best business in our universe, but does look cheap for a recovery that seems to be quite credible. (no section below)

Graham's Section:

Coral Products (LON:CRU) (£17m) - this plastics manufacturing and distribution group announces solid H1 results. It can’t prove organic revenue growth, due to some bad luck in China, but four acquired companies have all performed according to plan so far. There is potential for synergies to start kicking in over the next year, and this could boost the quality of financial performance. Overall, I see more to like than to dislike and think it could be worth researching in further detail.

Sigmaroc (LON:SRC) (£365m) (+3%) [no section below] - this construction materials quarrying group has announced an update for FY December 2022. Revenues year-to-date are up 20% on a like-for-like basis to £498m, and full-year underlying EPS is now expected to come in 10% higher than expectations (these expectations were at 7p). This has been achieved with the help of strong industrial demand, and through cost management. Importantly, the FY December 2023 outlook is unchanged, as visibility is “challenging”. If you’re interested in carbon capture technology, Sigmaroc has released an impressive-looking video on YouTube today - here. This company strikes me as being probably a good, reputable business but operating in a difficult industry, where many important prices and factors are beyond its control. It’s also carrying a heavy debt load that stood at £234m (excluding leases) as of June 2022. Nevertheless, this stock will be of interest to those who are comfortable investing in the construction materials industry. (no section below)

Begbies Traynor (LON:BEG) (£217m) - Begbies releases H1 results and confirms that it still expects to hit its sales and earnings estimates for the current financial year (FY April 2023). I take a look at the organic growth here - which is not bad - and make some broader comments on the state of the insolvency market. Zombie companies are at last being liquidated as the economy cleans itself up after many years of zero interest rates and Covid-related support schemes. When it comes to Begbies shares, I still think that the valuation is at risk of becoming over-cooked. The market possibly agrees with me as the shares have come off a few percentage points this morning, despite an in-line outlook statement from the company.

finnCap (LON:FCAP) (£27m) (-1%) [no section below] - this boutique investment bank announces H1 results in line with expectations. Despite the lack of IPOs, it has been busy with public and private M&A advisory work, debt financing mandates and placings. All of these, however, are at much lower levels compared to last year. Revenue is down 48% to £16.4m. There is an adjusted pre-tax loss of £0.6m and a statutory pre-tax loss of £2.6m. From an investor perspective, I always look for these types of companies to control their cost base in such a way that they can avoid making a loss, even in the bad times. Over this H1 period, however, Finncap has failed to do this, even though its advisory business model has developed to become in theory less cyclical than pure equity broking. I’d be much more impressed if it had reached breakeven: wage inflation for customer-facing staff, insurance and IT costs are all mentioned. Headcount has now been reduced and the interim dividend is cancelled. At around tangible book value and at a paltry multiple of what this company can earn in a bull market, the shares do look undervalued to me, although my first preference is for banks and brokers that can show a small profit even in bear markets. [no section below]

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul's Section:

Sosandar (LON:SOS)

22.5p (pre market open)

Market cap £50m

Sosandar PLC (AIM: SOS), one of the fastest growing fashion brands in the UK, creating quality, trend-led products for women of all ages, is pleased to announce its financial results for the six months ended 30 September 2022 and an update on current trading.

Company’s summary -

Continued revenue growth of +72%, delivering the Company's second six-month period of positive PBT. Momentum has continued into the second half of the financial year with record sales months in October and November, trading in line with market expectations* for the full financial year.

H1 key figures -

Revenue £21.0m, up a remarkable +72% (all organic growth too)

Gross margin 54.4% (down from 56.5% H1 LY) - due to more discounting in the end of summer season sale.

Profit before tax a whisker above breakeven, at £77k (H1 LY: £(1.08)m loss)

H1 tends to be seasonally slower than H2 remember, so we should see a more profitable H2 and hence FY 3/2023.

Balance sheet - huge increase in inventories to £13.5m, but cash position still looks OK, at £4.2m - that should improve as they de-stock over the peak selling period now.

The commentary says autumn/winter stock was brought in early, to avoid supply chain issues, and using slower (but much cheaper) sea freight.

Cashflow statement - absorbed cash of £2.8m, due to increased working capital, £6.2m increase in inventories, partially offset by £3.1m in trade payables. I’d expect to see this reverse in H2, so not a concern.

Overseas - this is the next logical growth area, and could propel the shares much higher (I remember years ago when Asos shares went ballistic after it began overseas expansion). Today SOS says -

Looking ahead, we will continue to invest in our own site, the bedrock of the Sosandar lifestyle hub, whilst also exploring additional third-party partnerships in the UK and abroad.

Current trading & outlook - sounds positive, but light on detail. SOS often refers to record months, but that’s a given, when the company is growing so fast, so doesn’t actually tell us very much!

However, this is the most important bit, confirming market expectations, with a useful footnote too -

We continue to trade in line with market expectations for the full year and remain confident in the longer-term outlook for the business."

* Sosandar believes that market expectations for the year ending 31 March 2023 are currently revenue of £42.8 million and PBT of £2.0 million.

That would represent a very strong H2 performance, with nearly all that £2.0m PBT being made in H2. Also note that SOS accounts are very clean, with no adjustments to profit, so this is real profit. H2 should also be highly cash generative, as those inventories turn into cash, so I could imagine year end FY 3/2023 net cash being close to £10m. Hence the days of placings now look well behind us.

My opinion - it’s lovely to see what was originally a blue sky project actually work (very rare)! Despite this, shareholder returns have so far been quite limited. It floated at 15p, and is now only 22.5p. That’s partly because with hindsight the IPO valuation was way too high for a startup, and also because the number of shares in issue roughly doubled through a series of placings needed when the cash ran out several times during the growth phase.

All credit to management though, for pulling off this huge challenge of creating an entirely new brand.

Shares look attractively priced to me, with a PER of 26.8x for FY 3/2023, and 16.5x for FY 3/2024, based on Singers forecasts (many thanks for making those available). It's unusual to see such rapid growth at a relatively sensible PER.

I’d be inclined to sit tight, and let this success story run. There is fashion risk, and key person risk due to the importance of the joint-CEOs. Apart from that, everything looks very positive to me.

The low StockRank is a flag for us to double-check the bull case, but in this situation I'm happy to ignore the low StockRank, because the balance sheet is fine, and this is a breakthrough year, when the relentless losses of the past are turning into a decent profit for the first time. We know that, but the computers don't (yet)! Hence the StockRank should gradually improve, as momentum and profits flow through into the numbers in due course. We can get in ahead of that.

Graham's Section:

Coral Products (LON:CRU)

Share price: 18.25p (+4%)

Market cap: £17m

We don’t normally cover this one: “a specialist in the design, manufacture and supply of plastic products”. Its website is here.

H1 results issued on Monday show an almost 150% increase in revenues to £17.6m, as newly-acquired businesses now account for most (£10.3m) of its sales.

Impressively, it made both a positive adjusted operating profit (£1.4m) and a positive reported PBT (£0.9m), despite making four acquisitions in 2022. We often see deal-related costs eating up any available profits in at least the first year or two, but not in this case.

Amazingly, all four acquisitions are said to have gone to plan so far.

Organic growth at a group level is not immediately obvious. The company reports that two of its existing businesses saw combined organic growth of 11.1%, but acknowledges that this was offset by weakness elsewhere. Logistical difficulties in China are holding things up.

Based on the level of H1 sales last year (£7.1m), I have the impression that overall H1 organic growth at CRU was low. If not for the problems in China, it might have been a better result on that front.

Capex - the company isn’t resting on its laurels and plans to spend £2.5m on capex, including additional manufacturing capacity of 5000 sq. feet.

Cash - £3.8m, offset by borrowings of £7.5m. So I make that net debt of £3.7m, excluding lease liabilities. The unchanged interim dividend of 0.5p will cost around half a million pounds.

Outlook is upbeat.The company is looking for efficiencies in H1 at the acquired business, has fixed its energy costs (for how long?), and will consider further M&A.

Comment from the Exec Chairman:

Our objective is to build a specialist UK plastics business of scale, targeting profitable, high-demand sectors. We aim to drive growth both organically and via acquisitions, whilst maintaining our commitment to sustainable objectives… We remain prudent with a strong balance sheet, backed by freehold assets and cash, and we look to return value to shareholders via dividends and capital growth.

Investor Meet Company presentation - on Wednesday morning. Here’s the link.

My view

As a manufacturer and distributor, the gross margins at Coral Products are modest. Indeed, gross margins have reduced to 27.1% following the addition of the acquired businesses (last year: 35.7%).

They now have seven subsidiaries, of which four are recent additions. The potential for synergies sounds promising, e.g. sharing expertise and other resources. I don’t see any plans for outright integrations.

The overall quality seems ok. Some quick back-of-the-envelope calculations suggest that the company might be earning a reasonable return on its invested capital. Although it’s too soon to tell - it all depends on management’s ability to manage four newly-acquired businesses, in addition to the three they already had!

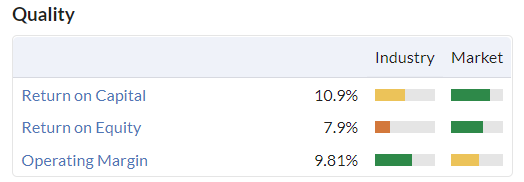

Stockopedia’s calculations like it a lot: it gets a QualityRank of 94.

I’m also impressed that it hasn’t diluted its shareholders much in recent years, has a track record of attempting to pay dividends when it can afford to, and is led by its largest shareholder in the form of the Executive Chairman.

I’ve not seen anything here that makes me want to run away. Even the valuation is reasonable: it looks like shareholders can do well, if management executes their plans. Might be worth tuning in to the presentation on Wednesday.

Begbies Traynor (LON:BEG)

Share price: 140.7p (-4%)

Market cap: £217m

Begbies is “the business recovery, financial advisory and property services consultancy” that many of us are familiar with. Today it releases H1 results for the period to October, confirming the numbers we saw in the recent H1 update.

- Revenue £58.5m up 12% (last year: £52.3m)

- Adjusted PBT £9m (£8m)

- Actual PBT £5m (£2.7m)

Note that Begbies has been busy on the acquisition front, so it’s important to clarify organic vs. non-organic growth.

We can do this by looking at the breakdown of performance at each division:

Business Recovery & Financial Advisory

Revenue in the period increased by 10% to £42.4m (2021: £38.7m), reflecting organic growth (£2.6m) and acquisitions (£1.1m).

Property Advisory and transactional services

Revenue in the period increased by 18% to £16.1m (2021: £13.6m), reflecting the first-time contribution from acquisitions (£1.8m) and organic growth (£0.7m).

By my calculations, organic growth is in the region of 6%, accounting for slightly over half of the reported revenue growth.

For such an acquisitive company, the level of net debt is reassuringly low at just £2.4m. The interim dividend is raised from 1.1p to 1.2p.

Current trading and outlook

As before, they remain confident of delivering full year results in line with expectations.

Begbies helpfully discloses that it believes these expectations to be revenues of £117.7m - £121.4m and adjusted PBT of £19.7m - £20.6m.

Every division appears to be performing well.

Business recovery - many investors appreciate the counter-cyclical nature of a business that thrives during periods of broad financial distress. The order book at this division is up 15% in only six months (i.e. growing very quickly on an annualised basis). It is seeing a “higher level of enquiries and increasing economic headwinds”.

Financial advisory - “encouraging pipeline of engagements across all service lines”.

Property advisory and transactional services - “resilient income streams, continuing flow of new instructions and potential to continue developing its mix of services”.

My view

I think I’ll start to wrap this section up, since little appears to have changed for Begbies and its shareholders. One important observation, however, is the size of the broader insolvency market (and this has read-across to other companies and the economy as a whole):

The number of corporate insolvencies in the 12 months ended 30 September 2022* increased to 20,731, following the removal of the Government's Covid support measures and are now 23% higher than in the comparable pre-pandemic period (2019: 16,836, 2020: 13,781, 2021: 12,492).

Some investors - myself included - have been predicting and betting on an increase in financial distress for what feels like a very long time.

The first and main reason to do this in recent years has been the belief that ZIRP created “zombie companies”, i.e. companies that were ultimately doomed but which could be kept alive temporarily so long as interest rates remained on the floor.

Then, during Covid, support measures such as the job retention scheme provided another mechanism for keeping failed companies alive.

Bank rate is still only 3% but that’s a significant increase from where it was before. The bottom line is that monetary and fiscal supports for zombie companies have now effectively been removed and this is showing up in insolvencies, as you can see from the above figures.

Interestingly, Begbies notes that administrations are still 35% lower than pre-Covid levels. The rise in insolvencies has been seen in the form of much higher liquidations. This is the form of insolvency that’s appropriate for small companies when there is no prospect of the business continuing in any form.

It would make sense for the so-called “zombie companies” to choose liquidation, but administrations are more lucrative for Begbies. So I wonder if it’s actually possible for administrations to recover back to pre-Covid levels?

Overall, I remain a fan of Begbies and I believe that its share price gains in recent years are justified. However, I would return to what I said last time: I would be cautious about paying a very large earnings multiple for a people-based professional services business.

If you’re willing to give the company the benefit of the doubt when it comes to its acquisition-related earnings adjustments, then the PER doesn’t appear overly expensive yet. But those adjustments do have a real effect on the company’s balance sheet, and thus the Begbies balance sheet only has a tangible worth of £8m.

Stockopedia’s calculations also struggle to find much value here, with a ValueRank of only 23. The price to sales multiple is now around 2x.

Don’t get me wrong: I think that Begbies has excellent prospects, and that its share price gains in recent years are well-justified. But I do think we may be reaching an upper limit for its valuation, based on its current size. I’m neutral on the stock at current levels.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.