Good morning, it's Paul & Graham here.

Here's the written summary of last weekend's podcast.

Agenda

Paul’s Section:

Trackwise Designs (LON:TWD) - Horrendous news for shareholders, with a 92% discount on a fundraise at just 1p. More details below, to avoid cluttering up this section. No.1 priority right now - we need to avoid holding anything that has run out of cash, as existing shareholders are lambs to the slaughter, as demonstrated by this news.

SThree (LON:STEM) - one of my favourite value shares - a decent quality business, on an attractively low valuation, with a strong balance sheet and no debt. Although today's year end update does mention softer market conditions emerging in Q4, so I ponder whether we might have seen peak earnings for the time being? Thumbs up for the long-term, but shorter term, we might see a wobble in 2023 possibly?

Billington Holdings (LON:BILN) [quick comment] - shares are up 26% to 290p on a strong trading update for FY 12/2022. Trading has “continued to improve”. Adj PBT now “significantly ahead of the Board’s previous expectations”, on unchanged revenue. Order book & pipeline give confidence for 2023, also now expected to be ahead of expectations. Says it has made efficiency gains. This looks an impressive turnaround, I haven’t looked at it since a profit warning a year ago, so didn’t spot that things were on the mend. Good balance sheet, with net cash. Looks interesting, but I’m wary of the economic cycle, which could cause trouble ahead. Severfield (LON:SFR) looks similar, but larger.

Mirriad Advertising (LON:MIRI) [quick comment] - this has come up on the top fallers list, down 24% today on a trading update, so we just need to get a quick comment into the system here, for future reference. I can scarcely believe the numbers - guidance for FY 12/2022 is revenues c.£1.6m, EBITDA loss of £(15.5)m! Cash remaining is £11.5m (down from £24.5m a year ago). Costs to be trimmed by £2.5m in 2023. Unless something drastically changes for the better, this share looks to be heading to zero before 2023 is out. This is one of the worst things I’ve ever seen, based on these numbers.

Loopup (LON:LOOP) [quick comment] - a positive-sounding update, as usual from LOOP, but it glosses over the vital bits of information we need - how much are the losses, and how much cash is left? Figures from Cenkos (many thanks) show heavy losses, and negative cashflows (it capitalises a lot of the payroll into intangibles). This share will almost certainly need another fundraise, and/or be taken private, or go bust, in my opinion. So it goes into the category similar to Trackwise - i.e. the products sound a good idea and are intriguing, but it needs more cash, hence is uninvestable unless it manages to refinance. Could easily be a wipe-out I think, so why take the risk?

Getbusy (LON:GETB) [quick comment] - up 6% today on a positive trading update - FY 12/2022 expected to be “slightly ahead of market expectations”. Impressive revenue growth of +24% to £19.1m (at least). Loss-making though, c. £(1.0)m for 2022, if I’m interpreting the announcement correctly. Net cash of £2.2m, and undrawn £2m facility, so liquidity looks OK. My view - quite an interesting share. It has a reliable cash cow software business, that is generating the funding for some blue sky projects. We don’t know at this stage if the new projects will work or not, but at least investors have the value of the core business to fall back on.

Cyanconnode Holdings (LON:CYAN) - lousy H1 numbers (loss-making, again, same every year), but it claims big orders are kicking in, and Q3 will see much higher revenues. Balance sheet doesn’t look good to me. Tight for cash, and receivables of £4.6m is over 3x H1 revenues - how does that make sense? Although it says £2.3m has been collected since the period end. Shareholders here have to hope that management is telling the truth, because on the basis of the historic numbers, I would value this share at nil. Too risky.

Graham's Section:

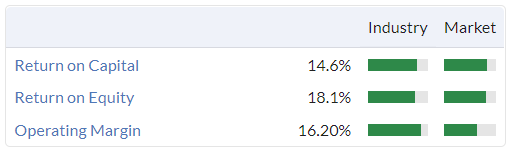

Volution (LON:FAN) (£700m) - today’s AGM statement lets us know that Volution continues to achieve an adjusted operating margin of over 20%, which is consistent with its long-term goals. I like this KPI so I’m enthused by its continued success on that front. The company’s organic revenue growth rate of 5.5% is not bad, but I’d like to see some improvement there, considering the pace of general inflation. Overall, this stock continues to strike me as potentially offering decent value, having sold off significantly since mid-2021. Of course, the same can be said about quite a few other stocks!

Cohort (LON:CHRT) (£183m) - good H1 numbers from this small defence group. Adjusted operating profit bounces back after last year’s H1 disappointment. The outlook for the full year is unchanged but management are very positive about the demand for their systems from NATO countries and in the Asia-Pacific. I can’t find much to criticise here - the main question for investors is perhaps whether they believe in the long-term demand story, and if they are happy to underwrite the risks involved with low-ish margins and lumpy orders.

PROCOOK (LON:PROC) (£30m) (+0.35%) [no section below] - these shares have fallen by a third since July. They had another profit warning last week. They are now down by over 80% since their IPO, which was only thirteen months ago! Today’s interim results show revenues down by 14.5% to £27.4m, a reduction in gross margin from 66.6% to 61%, and an underlying loss of £2.8m. This is despite growing their customer base by over a third (customers on their database who made a purchase in the last year). Their sales numbers have underperformed the UK kitchenware market, which itself is shrinking. Additionally, cost pressures have hurt margins: the company has chosen not to, or been unable, to raise prices sufficiently to offset increased shipping costs. While the net debt position is modest at only £1.3m, I don’t view this company as having much credibility after I discovered that it spent £9.4m on its IPO, and included nearly £7m of employees bonuses within its “IPO costs”. In the latest H1 period, it has made another £0.6m of IPO awards to employees, and included them within “non-underlying operating expenses”. For that reason alone, I would avoid this one with vigour.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul's Section:

Trackwise Designs (LON:TWD)

Horrible news today, of a massively discounted fundraise.

It’s doing a placing to raise £3.65m (before fees) at just 1p per share. The price last night was 12.65p, so the fundraise is a 92% discount.

The share count will rise from 37.5m in issue now, to 402m after this placing, an increase of 972%.

Then there’s likely additional dilution of 150m new shares if the open offer is fully taken up, so 552m shares in total.Existing shareholders can participate in an Open Offer, with 4 new shares (also priced at 1p) for each existing share. So that’s something, although it would still cause significant dilution even if shareholders do take up the open offer, because the placing is bigger.

PLUS there’s more potential dilution from warrants being issued, although I wouldn’t worry about that, because the exercise price is 6p, which would be a delight to achieve a share price of 6p or above. Management express “deep regret”.

As we keep discussing here, you don’t want to be holding anything that needs to raise fresh cash. Balance sheet strength is absolutely key right now, as it's so tough to raise fresh cash. This announcement is another reminder of the risk of being almost wiped out if the institutions don’t really want to support a fundraise. Be careful out there, conditions are really grim for small caps that run out of cash.

Graham flagged the high risk of a funding shortfall here in July, and marked it as uninvestable, so a hat tip there to Graham. Management reassurances about being able to find funding, turned out to be worthless.

The other question is whether this is going to be enough fresh cash? Will it need to raise again? Still too risky I think, even at 1p/share.

SThree (LON:STEM)

385p (down 3% at 08:34)

Market cap £518m

SThree plc (‘SThree’ or the ‘Group’), the only global specialist talent partner focused on roles in Science, Technology, Engineering and Mathematics (‘STEM’), is pleased to issue a trading update for the financial year ended 30 November 2022.

Record performance for the year with double-digit growth across all regions

There’s a lot of detail in this update, but it’s ambiguous about whether or not it’s hit market expectations. Liberum’s update note today helps clarify things (many thanks), leaving both FY 11/2022 and FY 11/2023 forecasts unchanged.

Note from the Stockopedia graph below how estimates for FY 11/2022 have been gradually rising, although next year’s forecasts (the lighter line) are now dipping down below this year. I think that’s sensible, given the macro picture and tough comparatives, and am wondering whether we need to be taking a more cautious view for earnings in FY 11/2023? We might have seen peak earnings in FY 11/2022 possibly? Especially as there are also well flagged increased costs which have been taken on in the last 6 months.

Market conditions - are softening, hardly surprising, but adds weight to my hunch that earnings may have peaked for now -

“Towards the end of the year we started to see a softer trading environment, reflecting the uncertain macro-economic conditions, and we continue to monitor the trends across our regions. However, the strength of our contract order book, robust balance sheet and a diverse customer base underpins our business. Our well-established strategy focused on STEM skills and flexible talent is supported by global megatrends, reaffirming our belief that we have the right vision with a unique and resilient business model for the mid to long-term.”

Financial strength - is excellent, with £65m net cash at Nov 2022 year end.

I’d like all companies to report average daily net cash/debt, which is much more meaningful than a one day snapshot at the year end.

For more detail, I reviewed STEM’s interim results in some detail here on 26 July 2022. It passes my balance sheet testing with flying colours, so there’s little to no solvency rise in my opinion - a safe share to hold in a downturn, although obviously the share price might fall temporarily if there’s a nasty recession, as with almost everything.

Some other key points -

- Geographical spread - I like this, with Germany, USA, and Netherlands being the 3 largest markets, totalling 73% of revenues. That means it’s not too dependent on any one country, or currency.

- Repeating revenues - STEM mainly earns it revenues/profits from contractors, being 78% of net fees. I see this as higher quality income, because it repeats for the length of a staffing contract, rather than being a one-off placement fee.

- Order book looks good, being up 19% vs a year ago, hence decent visibility.

My opinion - I remain positive about this company. It looks a quality outfit, reasonably priced (fwd PER of about 10), paying decent divis of about 4%, and with very good financial strength including net cash.

That said, it sounds as if earnings have probably peaked for now, with softer market conditions noted for the first time today, in Q4. It’s now up against very strong comparatives too, so the next few quarters could prove challenging.

It’s forecast to achieve c.39p EPS for FY 11/2022, a PER of only 9.9, but what if that’s peak earnings, and 2023 delivers say 30p? The PER would only rise to 12.8, which still looks good value for a decent quality, well-run business.

Overall then, I’d say for patient, long-term investors, this share should do well. Shorter-term? It’s possible there might be some bumps in the road, if economies slow sharply, and earnings forecasts are lowered. Just a suggestion - it might be a good idea to hold a smallish position for the long-term, and keep some powder dry to buy any dips which might occur in 2023? But that’s up to you obviously, your money, your choice!

Consistently very high StockRank too, as you can see from the StockRank chart below the share price chart -

EDIT: I spoke to the CEO & CFO here on 6 Oct 2022 - audio here.

Graham’s Section:

Volution (LON:FAN)

Share price: 354p (+1%)

Market cap: £700m

This is “a leading international designer and manufacturer of energy efficient indoor air quality solutions”.

It has a year-end in July, so today’s AGM statement covers trading in the first four months of the financial year (August to November).

Group revenue for the four months to 30 November 2022 increased by 7% year-on-year at constant currency ("cc") to c.£112 million with organic growth of 5.5% (cc), delivered through a combination of both volume and price increases. All three geographic regions grew organically.

In inflationary times, and even in normal times, it would be helpful if more companies broke out how their revenue was growing. Is it mostly through volume increases, or mostly through price increases? But normally we are left to figure that out for ourselves.

With organic revenue growth of 5.5%, the price increases at Volution are very unlikely to be keeping up with consumer price inflation, but at least they are moving in the right direction.

UK: organic growth 3.8%. Weakness in the commercial market.

Continental Europe: organic growth 6.4%.

Australasia: organic growth 8.5%, with “market share gains in Australia”.

Performance overview:

Our excellent levels of customer service, focus on operational excellence, strong brands, attractive product portfolio and pricing power have all underpinned our ability to deliver on the Group's operating margin target. Given the economic environment it is pleasing that since the year end we have continued to see sales and profits track ahead of the same period last year.

Note that Volution’s long-term target is to achieve an adjusted operating profit margin of greater than 20%. It did this in FY July 2022 (21.1%), and is doing it so far in FY 2023, too.

I agree with the company that this is a good financial KPI, so this definitely gets the thumbs up from me.

We should note that the actual (unadjusted) operating margin is not quite at the 20% level:

Regulatory drivers - “We continue to see strong regulatory initiatives driven by the need to decarbonise buildings, drive improvements in air quality, and reduce damp and mould in residential homes.”.

My view

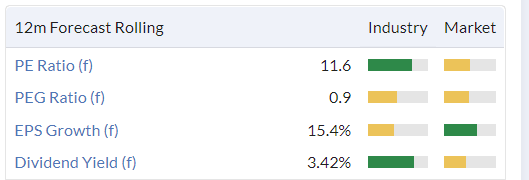

Every time I come across this one, it strikes me as a decent-quality business. Stockopedia computers agree:

Before the crash in small-caps, it was trading at 550p. It is now down at a PER of 15x, offering the prospect of nice returns if it continues to execute. What’s not to like and what have I missed?

As I noted last time, net debt has risen to £85.8m, but the company considers this to represent “leverage at historically low levels, providing us with opportunity for potential earnings enhancing acquisitions”.

Net debt to EBITDA (the leverage multiple) was less than 1x for FY July 2022, so I can see where they are coming from. At that multiple, they will feel free to do more deals.

I’ll continue to keep an eye on this one, as it seems to have good potential for a recovery:

Cohort (LON:CHRT)

Share price: 443p (+8%)

Market cap: £183m

This is a small defence group - its businesses can be reviewed here. They provide surveillance, communications, sonar and data management systems.

Let’s see how the company has performed in H1 (the period to October 2022). The key point is that the current year outlook is unchanged.

- Revenue +29% to £77.5m

- Adj. operating profit £5m (last year: £1.7m).

The sharp increase in H1 adj. operating profit stands out. Covering the company exactly a year ago, Paul noted that H1 adj. operating profit had collapsed. It fell from £4.3m to £1.7m. But now it has bounced back again.

But we also need to bear in mind the strong H2 weighting. Last year, the full-year result was £15.5m.

This year, we have a recovery in H1 profits, with the help of a great increase in revenues, so maybe the full-year result is going to be stronger again?

In the last few days, the researchers at Edison have terminated their coverage of this company - I don’t know why. But for what it’s worth, their most recently published forecast was for Cohort’s FY April 2023 adj. operating profit to be £18.5m. This forecast is considered redundant now, since it can’t be updated, but I thought I would mention it anyway.

If that forecast remained valid, then the stock would be trading at about 10x its adjusted operating profits - not bad.

Order intake is smaller than last year but is still higher than revenue. So the order book keeps growing and hits a new record high (£304m). “Over £80m of revenue deliverable in the second half”, so that over 95% of this financial year’s revenue is already baked in.

Net funds: £7.6m (as of last week).

Outlook is unchanged for the current year, and there is “a positive outlook for organic growth in the medium term”.

Chairman comment:

"The Group's order book has steadily increased over the last few years to what is now a record high. Its longevity has also increased with revenue now deliverable out to 2032. The pipeline of order opportunities for the remainder of the year also looks strong. Demand for our solutions and services continues to be driven by the UK's increased spending on defence and security and by international tensions in the Asia-Pacific region and Europe.

Unadjusted results - I’d like to mention that the amortisation of intangibles and other factors cause a significant difference between adjusted profits and actual profits:

- FY April 2022: adjusted operating profit £15.5m, actual operating profit £11.1m

- H1 of the current year: adjusted operating profit £5m, actual operating profit £1.6m.

My view

I’ve skimmed the performance of Cohort’s subsidiaries, but there is too much detail in them to share with you here. With six subsidiaries, there is quite a lot of work required for investors to study each of them in turn. The big picture is that order intake remains broadly very strong, and the pipeline of opportunities is good, but there are challenges when it comes to margins, the revenue mix and supply chain delays.

Personally, I don’t invest in defence shares. This is not for philosophical reasons: I simply found that I had no clue what defence companies would earn in any given year! I tried investing in Chemring (LON:CHG) during a period of takeover rumours and when the takeover fell through, I was left holding shares in a company whose EPS might as well have been produced by a random number generator.

That having been said, the signals from management here are positive and the valuation does not look terribly stretched. Demand from NATO countries and from Asia-Pacific countries concerned about China is perhaps going to remain strong for the next several years. And the balance sheet looks ok: £10m of cash has been sucked into inventories, but a similar amount has been released from receivables.

Overall, therefore, this looks priced about right to me, and perhaps on the cheap end of the spectrum, given the positive trading momentum.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.