Good morning from Paul and Graham.

We will cover whatever small caps news there is this week, and if it's too quiet for news, then I'll look back at one or two interesting companies I've been meaning to report on over the previous weeks/months. So I'm sure we'll come up with something interesting each day. Plus we might get some bombshell profit warnings of course this week, for companies that fail to close those year-end deals, or otherwise don't manage to catch up with their shortfalls against budget.

Your ideas - there's hardly any news today, so Graham came up with the idea that we could invite suggestions from you (in the reader comments) for interesting companies for us to write about this week. We'll do say 4 of them (2 each), based on which get the most reader votes (hit the thumbs up button for the one you like the most), and also please give a (at least) one line pitch for why you think the share looks interesting.

Agenda

Paul's Section:

Polarean Imaging (LON:POLX) - FDA approval is announced, after a disappointment & delay in Oct 2021. I'm told this is very significant news, so the share price could be in for a big increase possibly. EDIT at 08:12 - share price up 43% to 71p, well done to holders!

Rotala (LON:ROL) - a detailed update. The key thing is a major property disposal, which wipes out most of the debt. Remaining debt is asset-backed, HP on buses. So there's now ample liquidity for more acquisitions, or maybe divis/buybacks? Looks an interesting, and undervalued special situation. Worth a look, thumbs up from me. Very small and illiquid though.

Graham's Section:

Argo Blockchain (LON:ARB) (£38m) - the Argo share price has more than doubled this morning thanks to the announcement of a new financing agreement that secures the company’s future in the short-term. It should now have plenty of liquidity to work with and will have a reduced debt load moving forwards. The downside of the agreement is that it’s no longer going to own its major facility in Texas, and will have to pay hosting fees to the new owner from now on. Furthermore, the agreement achieves only a partial deleveraging. Given that prior to this agreement the company repeatedly warned it was going to become cash flow negative in the short-term, and that the bitcoin price has not improved, I expect that the company’s financial performance will remain disappointing in the short-term. However, it does at least now enjoy the possibility that the bitcoin price might bail it out, before it starts to run out of cash again. (more detail below)

DP Eurasia NV (LON:DPEU) (£79m) (unchanged) [no section below] - this Domino’s master franchisee has released a short update in response to what it calls “market speculation”:

DP Eurasia is evaluating its presence in Russia, the impact of sanctions and its continuing ability to serve its customers in Russia… Consequently, the Company is considering various options which may include a divestment of its Russian operations. Whilst work on a potential transaction is ongoing, there can be no certainty as to the outcome.

Trading in these shares has completely dried up, so it’s hard to know what investors will make of this news, but I imagine that most of them will reluctantly accept it. As I wrote recently, this company’s debt load has looked overbearing for some time. Depending on the sale price achieved, this problem could be addressed. Furthermore, the political situation is uncomfortable with a Commons MP naming DP Eurasia in parliament this month as a UK company that continues to do business in Russia (he appears to have missed the fact that DP Eurasia is not a UK company - it is registered and has an address in the Netherlands). For me, it’s all about the price achieved for the 170-odd Russian stores. I guess it’s possible that, given the political situation, they may be worth very little at this stage. But without more info I can’t form a strong view on the investment merits of DPEU shares at their current level. But it’s good to know that the company is considering all of its options in a situation that is about as bad as investors could have reasonably envisaged a few years ago. (no section below)

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Polarean Imaging (LON:POLX)

50p (pre market open) EDIT: up 43% to 71p at 08:12, on heavy volume of 2.5m shares printed so far.

Market cap £107m

I’ve covered this share here several times before, even though it’s a blue sky project, because several shrewd investors told me it’s the real deal, and FDA approval would see the shares soar. It also has backing from credible shareholders who refinanced it a while back. Then the unexpected happened in Oct 2021 - the FDA denied approval, causing the share price to plunge 60% - as you can see on the 3-year chart below.

Although it seems investors have kept the faith that approval would eventually follow, as the share price has held up well, given that this brutal bear market for speculative small caps has almost wiped out many similar jam tomorrow type companies.

.

Today’s announcement is headed up -

FDA Approves Polarean's XENOVIEW™ (xenon Xe 129 hyperpolarized) for use with MRI for the evaluation of lung ventilation

I don’t understand the detail, so have asked my network of shrewd investors, and am told that this is very significant positive news today.

So we could see a decent-sized, positive, share price reaction today, if anyone is at their computers!

Rotala (LON:ROL)

34.5p

Market cap £17m

This bus operator listed on AIM in 2005, and its shares haven’t really gone anywhere. So I’ve not reported on it here since a brief look in 2016.

However, an interesting announcement was issued at 12:30 on 23 December, which caught my eye as seeming significant. Subscribers davidallen77, and jimrog64, have posted interesting comments below, thanks for those.

Here’s the latest announcement -

Business Developments, Trading Update & Prospects

Rotala (AIM: ROL.L), an operator of bus routes in the UK for businesses, local authorities, and the general public…

Contracts - details are provided for contracts tendering in Manchester & West Midlands. It’s won some smaller contracts, but not 2 larger contracts. The net effect is to reduce future revenues by £3.5m - not a big deal, in the context of £96.5m revenues for FY 11/2021.

ROL has “agreed in principle” to sell its Bolton depot to Manchester council (GMCA), and most of its buses there will be sold to the successful contract bidder.

Trading for FY 11/2022 is said to be “in line with its budget”. The wording is vague on this, but seems to be saying that FY 11/2022 resulted in a loss of £(1.3)m or better, similar to last year.

One-off gains from fuel hedging, and a leasehold disposal, will produce a hefty boost of £3.2m additional profit, to be reported as exceptional items.

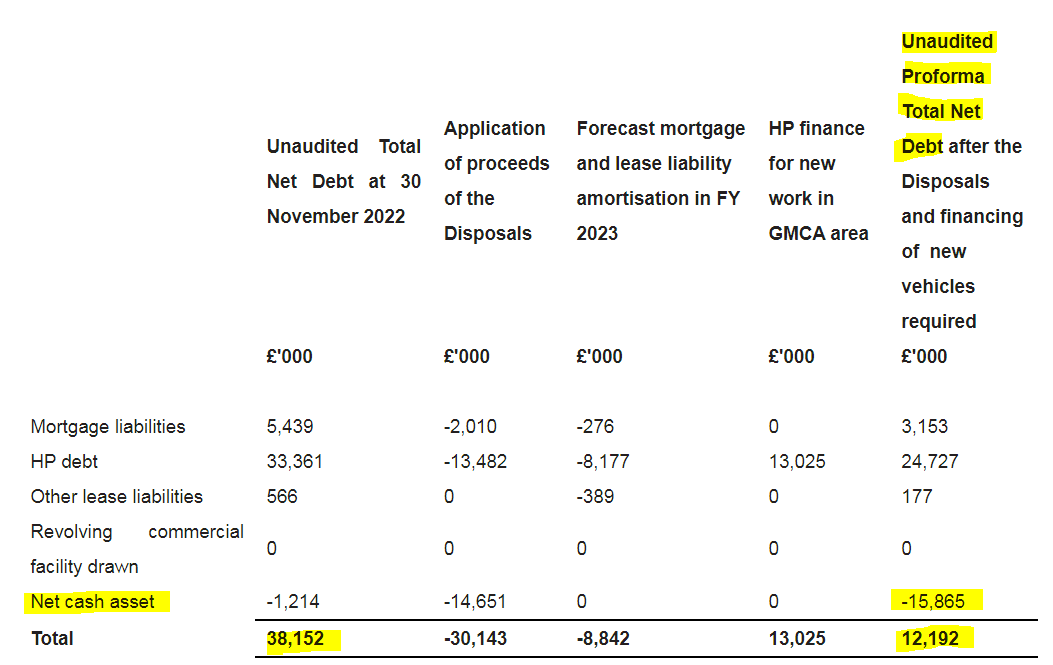

Net debt - below £40m (meeting its target) at year end (but much lower if anticipated disposals complete post year end, more detail below)

CEO comments are upbeat, saying the company is “in a much better place for the year ahead”.

Outlook - expecting to return to pre-covid profitability.

Fuel cost has been 38% hedged for FY 11/2023 at below current market price.

“despite the increased cost of living, fluctuating fuel prices and general rise of inflation, the Board remains very confident about the future prospects of the Company.”

Disposals - subsequent to the 11/2022 year end, disposal of the Bolton depot & buses, will raise cash of £30.1m (very large, for a £17m mkt cap company). Of this, £8.8m will be used to pay down other debt. Then new HP finance of £13.0m will be drawn down for the purchase of new buses. Complicated, but this table below explains it well. Note that there will be a new gross cash pile of £15.9m, which looks like it will give the company flexibility - special divis/buybacks maybe? Or more acquisitions?

.

Gain on disposals - the assets being sold for £30.1m have a net book value of £22.7m, so that’s a £7.4m profit on disposal, which will strengthen the balance sheet (but presumably might also be taxable maybe?)

Passenger volumes - on buses are nationally at 85% of pre-covid. ROL’s operations are doing better, at 95%. Pensioners are reluctant to go back to pre-covid bus use, it says.

Government initiatives for the bus industry are said to be positive, but there is “continued turbulence” in the sector - seen as providing opportunities for ROL.

Takeovers - of the 2 largest companies in the sector are noted. Could ROL become a bid target too?

Bank facilities are described as “ample”, including an undrawn HSBC facility.

Main bull points -

- V high StockRank of 96

- Discount to NTAV

- Major property disposal at a substantial profit.

- Director buying - lots of smallish Director buys over several years. No big sales.

- Greatly de-geared now, and ample borrowing facilities (plus £15m gross cash)

- Strong finances now, creates opportunities.

- Sector consolidation - could be a bid target?

Possible bear points -

- Competitive contract tendering, so margins not great.

- Tightly held by top shareholders, limited liquidity - delisting risk? (note Nigel Wray holds 15.5%)

- Govt regulated sector = uncertainty of future policy?

My opinion - there’s lots of information in this update, and more detailed research & analysis of the numbers is needed.

However, on a quick review from me, I think this share seems potentially interesting, and is well worth micro cap investors taking a closer look. It seems excellent value to me, especially as the share price has barely budged, despite a key announcement on 23 Dec, which should result in a much improved financial position. I think this share looks undervalued now.

Graham’s Section:

Argo Blockchain (LON:ARB)

Share price: 8p (+123%)

Market cap: £38m

The troubled bitcoin miner Argo Blockchain has released a major refinancing announcement this morning, that appears to stave off any immediate bankruptcy concerns.

Key points:

Argo sells its Texas-based facility for $65m (£54m) to an organisation called “Galaxy Digital Holdings”.

Argo maintains ownership of the mining machines at this facility, and will pay a hosting fee to Galaxy to continue to operate them.

Galaxy will also provide a new $35m (£29m) asset-backed loan to Argo, collateralised by the mining machines at the facility.

This is indeed a transformational deal. It replaces existing lenders with a new one, partially deleverages the balance sheet, and changes the fundamental position of Argo in Texas from a facility owner to a renter.

Out of the $100m received, $84m will go to pay off existing lenders (for context, total borrowings on the most recent interim balance sheet were GBP £118m, with net debt of £109m).

New mining strategy - the new owner of the facility is perhaps more sophisticated than Argo, who allowed themselves to trade at the mercy of a floating electricity price. The new owner will enter into a fixed-price power purchase agreement, and Argo will have access to electricity at the fixed price.

They will also need to have a “curtailment strategy”, which I presume means shutting down operations temporarily when there is too much demand on the power grid:

Argo will pay Galaxy a hosting fee and will collaborate on designing a curtailment strategy in order to participate in certain demand response programs offered by the Electric Reliability Council of Texas, which manages the Texas power grid.

Canadian operations

An interesting side note in today’s RNS:

Initially, Argo plans to refocus its efforts on growing and optimizing operations at its two data centers in Quebec, which are powered fully by low-cost hydroelectricity.

Argo’s CEO is, I understand, based in Canada, so perhaps he’d like the company to do something more local to him. But Argo’s existing Canadian operations have very low capacity compared to what the company is doing in Texas. Heavy investment in new machines would be needed to enable the Canadian operations to move the needle.

CEO comment

This transaction with Galaxy is a transformational one for Argo and benefits the Company in several ways. It reduces our debt by $41 million (£34 million) and provides us with a stronger balance sheet and enhanced liquidity to help ensure continued operations through the ongoing bear market. It also allows us to focus on optimizing our operations with significantly lower capex and opex requirements."

My view

The reduction in debt clearly gives the company more breathing room, and today’s share price movement reflects this relief.

The company now has enough liquidity to continue trading, and will enjoy some protection from rising electricity prices in future,

However, I’m not sure I would conclude that the company is completely safe, from a solvency perspective. Based on the comment by Peter Wall above, the debt reduction achieved is only roughly a third of the total that was outstanding as of last summer.

The new asset-backed loan has an initial term of 36 months and it will be up to Argo and Galaxy to decide what happens at the end of that period.

Also, I don’t see any mention of interest rates in today’s announcement but we can presume that Galaxy are charging healthy rates for taking on this exposure. And Argo will have to pay rent (the “hosting fee”) in Texas from now on - a fresh hurdle to short-term profitability.

Bitcoin currently trades at $16,600, down 65% year-to-date. I suspect that the company’s financial performance will remain poor at this price:

As usual, this share, thanks to the strategy pursued by management, continues to look like a highly risky punt on bitcoin, with little equity value available for shareholders unless that price rises very significantly from its current level.

The new deal with Galaxy will see a stream of fees and interest going in the direction of their new financing partner, while Argo shareholders and management wait for the bitcoin price to bail them out one last time.

CEO Peter Wall continues to believe that what we are seeing is just a temporary “bear market” in crypto, not the permanent popping of a bubble. He may be right. Argo might get bailed out again. But at current crypto prices, I suspect that it’s only a matter of time before Argo gets into trouble again. At least they now have a chance of survival - and some time to come up with a more sustainable strategy.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.