Good morning from Paul & Graham, and a very happy new year!

There's little news today, so Graham's going to be writing a year end roundup type section today, and I might cover something similar but not overlapping. So we should have something interesting up by 13:00. Leave it with us!

Agenda

Paul’s Section:

Hotel Chocolat (LON:HOTC) (156p pre-market, mkt cap £214m) [quick comment] - we had previously been told that HOTC was trying to salvage something from its disastrous Japanese joint venture. A new arrangement for 21 Japanese stores is announced today, with HOTC owning a reduced 20% stake, but set to receive brand royalty revenues (not specified at what rate). There’s not enough information for me to assess how good this deal is, but anything is better than what looked previously like it might be a total write-off. As yet, there doesn’t seem to be any information from brokers. I reviewed its FY 6/2022 results here, and remain of the view that the investment story looks stale, the product tastes completely ordinary to me (and seems overpriced), and aggressive forecast profit growth for FY 6/2024 and beyond doesn’t look credible. Which leaves us with a share that’s probably over-priced, and vulnerable to more profit warnings in the current climate. Solvency/liquidity look fine though, with a sturdy balance sheet. For me, overall it’s an avoid, based on current information. (no section below)

Bidstack (LON:BIDS) (2.8p pre-market, mkt cap £36m) [quick comment] - another worrying announcement from this speculative, jam tomorrow, in-game advertising company. There were previous signs that its key relationship with partner Azerion was going wrong. Today we’re told it’s now become a legal dispute, with Azerion withholding payment for invoices from BIDS, and terminating the agreement. This is clearly a major blow for BIDS, however they try to gloss over it today. The interim accounts commentary showed how significant this $30m 2-year deal was for a company with previously negligible revenues. Without it, BIDS shares look too high risk, as it looks like the wheels are coming off. I don’t imagine FY 12/2022 results will be out any time soon, due to disputed invoicing, and how long will the last £10m fundraise keep it funded for? I’d vigorously avoid this share now, to be on the safe side, and salvage whatever you can. (no section below)

Here's the link to my New Years Eve podcast. As usual it was a run through the SCVRs, and also some wider thoughts about the market generally. I see a lot of small caps being very attractively priced right now, so am long-term bullish for decent companies on bombed out valuations. Shorter term? Who knows? It looks like a minefield of profit warnings, and also dilution/solvency issues for companies with too much debt, and/or cash burning junk that needs to raise more cash, so it's very clear what we should be avoiding in the meantime. There's one mystery share, my best idea for the week, which is a micro cap special situation called Rotala (LON:ROL) which I covered here on Weds 28 Dec. It needs deeper research, but the refinancing from sale of a large freehold has greatly improved its financial position. Very small and illiquid though, with a wide bid/offer spread, so this one will only appeal to special situations micro caps investors.

Aptamer (LON:APTA) (47p, down 8% - mkt cap £32m) [quick comment] - a life sciences business that floated in Dec 2021, raising £9.6m. Lost £(2.6)m PBT on £4.0m revenues for FY 6/2022. Today it says H1 (to Dec 2022) is only £1.0m revenues, and with expanded overheads, I expect to see cash considerably depleted from the £6.7m held at 6/2022. Says bullish things about the outlook for H2, but I reckon there’s not enough cash headroom to make this a safe investment. Very concentrated shareholder register, with little market liquidity. I’d steer clear of this, as risk:reward strikes me as unappealing at this stage.

Cineworld (LON:CINE) (3.4p - mkt cap £46m) [quick comment] - the extended death of this company continues. It's obviously bust, with a vast debt pile, created by reckless acquisitions. I don't understand how the shares continue to trade, despite the company repeatedly telling the market that there's little to no value in the shares, as it confirms today - "As previously announced, it is expected that any restructuring or sale transaction agreed with stakeholders will result in a very significant dilution of existing equity interests in Cineworld and there is no guarantee of any recovery for holders of Cineworld's existing equity interests." It looks to be an almost certain 0p in my view, so people gambling with the shares now are taking on a lot of risk.

Graham's Section:

Year-end review of Indices - see section below.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Graham’s Section:

Index Review

Good morning, and Happy New Year!

Today, since there isn’t much company news to cover, I’d like to give you an overview of some of the most relevant UK stock indexes: their performance in 2022, their current valuations, and their top components. Hopefully we’ll be able to draw some useful conclusions when we’re done!

Let’s start with the AIM All Share Index (AXX), since it includes so many of the small companies which we cover in the Small-Cap Value Report.

AIM All Share Index (AXX)

Price change in 2022: minus 32%

Components above their 200-day moving average: 26%

Largest components:

HUTCHMED (China) (LON:HCM)

Keywords Studios (LON:KWS)

Jet2 (LON:JET2)

RWS Holdings (LON:RWS)

Burford Capital (LON:BUR)

An unusual feature of this index is that it has a very long tail of tiny companies, so it can sometimes feel like there is a mismatch between the average performance of an AIM stock and the performance of the index as a whole, whose performance is guided by its largest components.

But this index fell 32% in 2022 and that seems to resonate, unfortunately, with the performance of many AIM portfolios held by private investors.

What I find surprising is that its median trailing P/E ratio is still in the mid-teens at 16.6x, according to the IndexReport. After a 32% fall, I would love to see a very cheap trailing P/E ratio on offer, to give me confidence that the index has fallen into value territory.

More positively, the median forward P/E ratio is only 12.7x, and forecast EPS growth is strong at 15%.

Is that unrealistic? Probably - analyst earnings forecasts do tend to overshoot in terms of optimism. Any EPS increase at all for AIM stocks in 2023 would, I am sure, do wonders for sentiment and for this index.

The companies in this index are some of the most sensitive to economic conditions: many of them are effectively binary bets on success or failure, and their smaller, weaker balance sheets make them especially vulnerable to difficult financing conditions. 2022 saw the IPO market close up completely and placings were also much more limited, compared to prior years. Companies needing cash had few places to turn.

So where do we go from here? As usual, I expect that the AIM Index as a whole will, on average, perform poorly compared to other indexes. This is a structural issue: AIM simply has too many poor-quality companies to do well. Think of the junior miners and all of the blue-sky enterprises, many of which eventually wind up worthless.

That makes AIM a stockpicker’s market requiring individual stock selection and I do expect we have now reached a point where many of its quality and value shares are severely undervalued. We have talked about many of these candidates in this report. Sorting the wheat from the chaff, and having the patience to wait for recovery, as always, is the challenge.

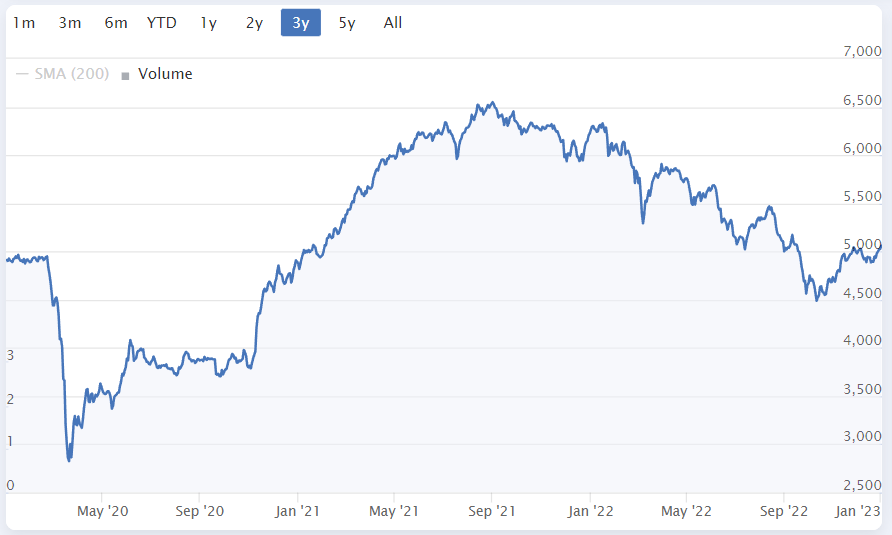

Smallcap Ex Investment Trusts Index (SMXX)

Price change in 2022: minus 20%

Components above their 200-day moving average: 30%

Largest components:

Fuller Smith & Turner (LON:FSTA)

A G Barr (LON:BAG)

Keller (LON:KLR)

Bakkavor (LON:BAKK)

Hunting (LON:HTG)

The performance numbers above show that this index performed significantly better than the AIM All-Share.

That shouldn’t be too surprising: this index consists of much safer, more “respectable” and well-known companies, who tend to have stronger balance sheets and more financing and strategic options than their AIM brethren.

It includes some ambitious small companies who want access to the larger pool of institutional investors on the main market. It also includes some larger companies who, perhaps temporarily, have fallen on hard times and fallen out of the FTSE-250 Index. The market caps in this index range from £30m up to around £600-700m.

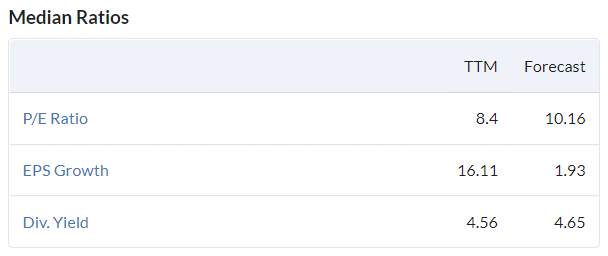

Valuation: the trailing (8.4x) and forecast (10.16x) median P/E ratios here jump out at me, screaming value!

Scrolling through the list, I see that many of the cheapest stocks are financials and property stocks, and of course there are good arguments to be made that the outlook for lenders and for the property sector are bleak. There is almost no EPS growth pencilled in for this index in 2023.

As a contrarian and a value investor, however, I can’t help but think that a trailing P/E ratio of only 8x for this entire index may be excessively pessimistic, for long-term investors, and that many of the components here are likely to be undervalued. This has always been one of my favourite indexes, and I like the pricing it offers here. Note that the dividend yield is also very chunky, and in value territory, at 4.6%.

FTSE 250 Index (MCX)

Price change in 2022: minus 20%

Components above their 200-day moving average: 39%

Largest components:

Carnival (LON:CCL)

Investec (LON:INVP)

Beazley (LON:BEZ)

Weir (LON:WEIR)

Johnson Matthey (LON:JMAT)

We are firmly in mid-cap territory with this index. This index includes some large global companies, including some that are leaders in their specific niche.

As with the small-cap index, this one significantly outperformed AIM in 2022.

Also, I note this index is showing signs of broad stabilisation with 39% of components currently trading above their 200-day moving average.

Valuation: this one is not offering the same low P/E ratio as the small-cap index SMXX, which I expect is fair since there are many excellent and unique stocks included here: think of the likes of PZ Cussons (LON:PZC) and Cranswick (LON:CWK) and Games Workshop (LON:GAW) .

At a forecast P/E ratio of 13x, for a quality index, I think this also looks very interesting.

Consistent with offering more quality and less value than the small-cap index SMXX, this offers higher forecast EPS growth (5% instead of 2%) and a lower dividend yield (4% instead of 4.6%).

So for investors who are willing to pay a slightly higher earnings multiple, and accept a lower yield, this index probably offers a safer and better set of companies in which to invest.

FTSE 100 Index (UKX)

Price change in 2022: plus 1%

Components above their 200-day moving average: 49%

Largest components:

AstraZeneca (LON:AZN)

Shell (LON:SHEL)

Unilever (LON:ULVR)

HSBC Holdings (LON:HSBA)

Rio Tinto (LON:RIO)

Wow! As Ed noted in his latest New Year NAPS article, 2022 was a year in which UK stocks seemed to perform better, the bigger they were. And the largest stocks performed best of all.

FTSE-100 Investors finished 2022 higher than they started it, and also collected the dividends for which this index is famous.

AstraZeneca had a good year, with strong contributions expected from its cancer and diabetes drugs.

The large banking groups muddled through a period of rising interest rates.

And large resource companies did very well as broad inflation saw many commodity prices increasing. Oil and gas producer Shell is back near the top of the FTSE-100 league.

Valuation: after a year of sturdy performance, the forecast P/E ratio here is steady at 13x.

This index is seen as low-quality by many investors - myself included - but perhaps we should give it more respect? It trounced many other indexes and asset classes in 2022, proving its worth as a defensive basket of stocks.

I would still expect the FTSE-250 and other indexes to outperform it over longer time periods, but perhaps the FTSE-100 remains an attractive asset for risk-averse investors who still want some equity exposure.

Conclusions

In summary, I think this analysis helps to prove what an unusual year 2022 was. It was very much “risk-off” with the largest companies holding up well and the smallest companies struggling badly.

Even the “quality” small companies performed badly in 2022, but I think this may now provide opportunities in both the Smallcap and FTSE-250 indexes, where valuation multiples and dividend yields have in many, many cases fallen into value territory, especially in small-caps.

There are also undoubtedly opportunities in AIM too, but the large concentration of low-quality companies there makes it harder to discern that from the index metrics.

Of course the more pessimistic you are on the economy, the less enthused you’ll be by the value on offer. Investing is at the end of the day a matter of opinion, as it concerns the future and the future is uncertain! But I hope this article has helped to clarify some of the big-picture issues for you, and leave you with some hope that 2023 performance could be significantly better! Cheers.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.