Good morning! Timings are very tight for me today, so there's not likely to be that much posted here this morning, but I'll try to do some more this evening, and I need to circle back to review Snoozebox Holdings (LON:ZZZ) in yesterday's report too - it's on the to do list!

Norcros (LON:NXR)

Share price: 17.0p (up 4.5% today)

No. shares: 597.1m

Market Cap: £101.5m

(at the time of writing, I hold a long position in this share)

Trading update - for the year ended 31 Mar 2015, from this bathroom fittings and tiles company, which operates mainly in the UK, but also S.Africa.

Key points;

- Most importantly, underlying operating profit is "expected to be in line with market expectations"

- Turnover C.£221m - up 1.1% on prior year, and 1.8% below broker consensus

- Sales growth accelerated usefully in H2 (up 5.4% in H2, up 1.5% for the full year)

- UK housebuilding sales were strong, offsetting "challenging" (why?!) UK retail sector

- S.Africa - strong local currency sales (up 19.1% in H2)

- Impact of S.African Rand depreciation now stabilising, so growth is feeding through into sterling terms too now

- Closing net debt lower than market expectations at c.£15m

- Pension fund & deficit not mentioned

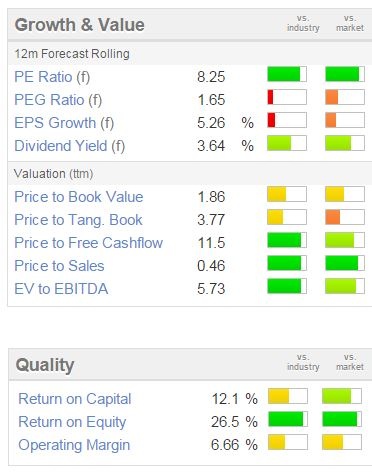

Valuation - this share has a high StockRank of 92. Also there is plenty of green on the usual Stockopedia graphics - in particular the forecast PER is very modest, at 8.25, especially considering the company has little debt now (which in any case is more than offset by remaining freehold properties). I also like the growing divis, yielding about 3.6%.

My opinion - this is a strange share. There seems a permanent overhang in the market, but for the patient investor that doesn't really matter. What is more important is that the shares look good value, and the company is trading well. I particularly like the low PER, and there should be favourable macro tailwinds too (with increasing housebuilding), especially in the UK.

The only issue on trading that concerns me a bit, is the lack of progress in the UK retail sector. This suggests competitive pressures may be problematic perhaps?

Also, the pension fund here is huge, which wasn't much of a problem in the past, as it was quite well funded. However, recent lower bond yields has probably increased the deficit. So investors should be braced for potentially higher deficit recovery payments in the next few years. However, longer term, the deficit should come back down again when interest rates eventually normalise.

The Fed is now talking about tightening, so where the US leads, everyone else follows. Therefore I think there is a good chance that investors will begin to look through pension deficits at some stage over the next year or two.

So after today's announcement, I remain a happy holder. We get reasonable divis whilst we wait for the selling overhang to clear, which it will eventually. The chart also suggests to me that the worst is over now, it's formed a base in recent months.

Renold (LON:RNO)

Share price: 56.6p

No. shares: 223.1m

Market Cap: £126.3m

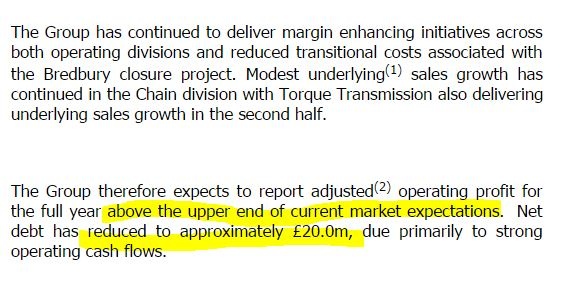

Trading update - this reads well, with the key bits highlighted by me, using the wobbly highlighter;

Stockopedia shows broker consensus for the y/e 31 Mar 2015 as being EPS of 4.37p per share, so I make that a PER of 13.0, which sounds about right if the company had a clean balance sheet. Trouble is, it doesn't.

Balance sheet - this is the problem. It's not just net debt, but a nasty pension deficit too. Overpayments into the pension fund are about £2.5m p.a., and for that reason the company doesn't have surplus cashflow to pay proper divis. So there is only a tiny dividend yield of 0.35%.

My opinion - the company seems to be recovering well, so there could be more upside possibly? However, the burden of the pension deficit, and the lack of meaningful divis, rule it out as a potential investment for me. I'd want a PER of perhaps 6-7 to get me interested. Big pension deficits can rule out takeover bids too, thus greatly reducing the chance of a nice surprise one morning with a bid.

Scapa (LON:SCPA)

Share price: 154p (up 10% this morning)

No. shares: 147.2m

Market Cap: £226.7m

Trading update - for the year ended 31 Mar 2015, from this supplier of bonding materials. It's a beat against expectations;

Pity about the people losing their jobs in Switzerland - I suppose this is due to the appreciation of the Swiss Franc, making it uneconomic to manufacture there.

My opinion - the company seems to be trading well, but there's not much of a divi, only 1.0% yield. The valuation looks about right to me, although after today's announcement clearly broker forecasts are likely to be raised.

There's a pension deficit here too, so watch out for that. It was last reported at £37.3m on the balance sheet, so the actuarial deficit is probably worse than that now.

Matchtech (LON:MTEC)

Share price: 527.5p (down 1.4% today)

No. shares: 30.4m (NB. includes new shares admitted on 2 Apr 2015)

Market Cap: £160.4m

(at the time of writing, I hold a long position in this share)

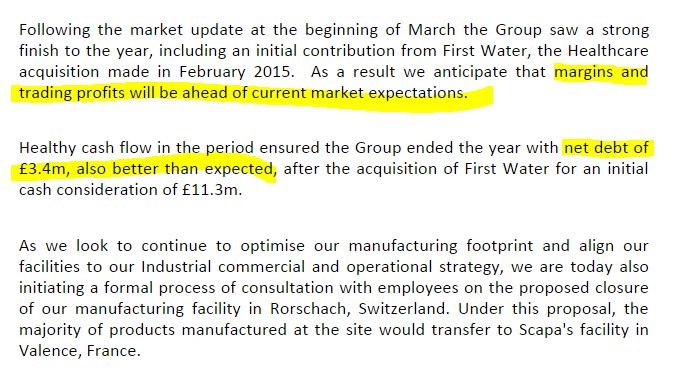

Interim results - for the six months ended 31 Jan 2015. This period does not include any contribution from the acquisition of Networkers, which was a large acquisition, so will materially increase profits from the date of acquisition, which was 2 Apr 2015.

So today's interims are really only of passing interest, to check that the original business is performing as it should be. They're not great actually - underlying profitability is only flat against H1 last year, with underlying basic EPS up 2% to 19.9p.

Net debt was almost eliminated, down by £6.7m to £1.9m, which is good because it clears the decks before the significant new debt (a £30m term loan provided by HSBC) used to part-fund the acquisition of Networkers is added to the balance sheet.

I reported here on 28 Jan 2015 about the acquisition of Networkers.

Shorting/overhang - note that Matchtech shares are one of the most heavily shorted in the UK market. This is probably not because people hate it, but rather because I suspect Networkers shareholders wanted to lock in a sale of their new Matchtech shares, in advance of receiving them. So I believe the big short position in Matchtech should unwind now the new shares have been issued.

There may however be some continued selling of Matchtech shares, by former Networkers shareholders, who are grateful for the improved liquidity, hence are using this as an opportunity to exit, where they were perhaps not able to exit the less liquid Networkers shares.

Valuation - I did some back of envelope sums recently, and arrived at a pro forma EPS of c.50p for the combined Matchtech & Networkers group. An Equity Development note today arrives at an almost identical forecast of 49.9p EPS for the year ending 31 Jul 2016.

Therefore these shares appear to be on a forward PER of just over 10, which looks good value.

Outlook - comments today say how excited they are about combining the two businesses, and that they see "major opportunities". Trading is in line with expectations for the year ending 31 Jul 2015.

There is a separate RNS today detailing contract wins, however since it contains no financial details, and doesn't change performance against expectations, then I'm taking it with a pinch of salt. Companies win & lose contracts all the time, that's the normal course of business.

My opinion - I think this is a decent share, at a reasonable price. Flat results today were a little disappointing, so there's probably not much of a catalyst for an immediate share price rise, but I could see this share rising steadily to 600-700p maybe later this year, or next year. So reasonable potential upside perhaps.

NetPlay TV (LON:NPT)

Share price: 9.0p (down 4% today)

No. shares: 296.6m

Market Cap: £26.7m

Final results - for calendar 2014 don't look good, for this interactive gambling company. Revenue was down 3.9% to £27.4m, but adjusted EPS fell sharply, down 35% to 1.09p per share - and remember adjusted figures are the company putting the best gloss it can on the results.

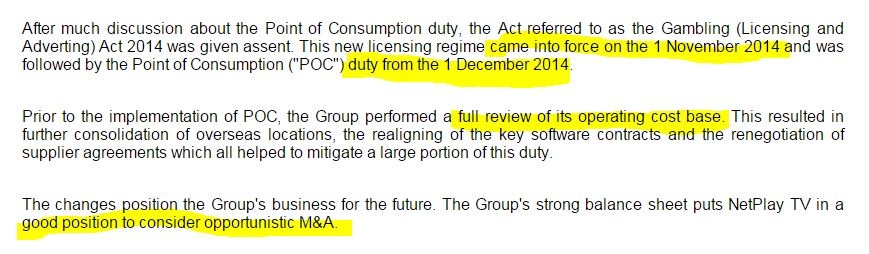

The PER looks low, but as we've known for some time, this is because the new Point of Consumption betting tax is going to reduce profits.

Point of consumption tax - this is not an area I've looked into in any great detail, as I decided some time ago that Netplay management's reassurances about its impact being manageable, were nowhere near as convincing as their multi-million pound personal selling of Netplay shares! If in doubt, always follow the money, is my view - and they were taking out millions of their own money at higher share prices than today.

This section from today's commentary says the new tax has been implemented;

However, another part of the commentary suggests the impact of regulatory change is not yet fully known;

Outlook - muddy waters, due to the regulatory/tax issues mentioned above, although Q1 seems to have been alright;

Strange that they don't say performing well in Q1, but instead say performing well into Q1. Does that imply that Q1 started well, but then deteriorated?

Dividends - total of 0.55p per share has been either paid (0.22p interim) or declared (0.33p final), giving a yield of 6.1%. Very good, but I'd want certainty that earnings can be maintained to support that payout level, as divis which are eating into cash reserves should not be relied upon. The company could have declared a special divi with its surplus cash, but hasn't.

Cash - this is the best bit, with a nice net cash balance of £14.2m. I'm not sure if this includes player deposits or not?

My opinion - this share is certainly worth a closer look, as the cash underpins just over half the market cap. However, I want to sit on the sidelines and wait to see what sustainable earnings are like under the new tax/regulatory regime.

Management seem to want to spend some or all of the cash pile on acquisitions, possibly from distressed competitors who are not able to generate cash any more.

This share certainly needs more careful research, but I wouldn't rule it out as a special situation, if you are able to get comfort about future profitability being sustainable.

All done for today, I'm heading into London for a meeting now.

Regards, Paul.

(of the companies mentioned today, Paul has long positions in NXR, MTEC, and no short positions. A fund management company with which Paul is associated may also hold positions in companies mentioned)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.