Good morning! We have another takeover offer to round out the week, this time for Alliance Pharma.

1pm: this report is finished! Have a great weekend, and keep an eye out for our weekly podcast!

Spreadsheet accompanying this report (updated to 3/1/2025).

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

J Sainsbury (LON:SBRY) (£6.6bn) | TU | Q3 LfLs +2.8%. Won market share. FY25 adj. operating profit to be in line (£1,010-1,060m). | AMBER/GREEN (Graham) |

Clarkson (LON:CKN) (£1.2bn) | TU | Results for FY Dec 2024 to be slightly ahead of expectations, adj. PBT not less than £115m. | AMBER/RED (Graham) |

Glenveagh Properties (LON:GLV) (£704m) | Full Year TU | Rev +43% (€869m), EPS +112%. “Positioned for further growth in 2025”, favourable mkt conditions | |

Team Internet (LON:TIG) (£297m) | Statement of intention not to make an offer | One of the possible buyers pulls out of the race. | PINK |

Alliance Pharma (LON:APH) (£240m) | Recommended acquisition of APH | 62.5p in cash, 41% premium to yesterday’s close. | PINK (Graham) |

| De La Rue (LON:DLAR) (£218m) | Receives takeover offer (per Sky News) | According to Sky News there is a “full cash offer” at 125p. A partial cash offer was proposed in Oct. | PINK |

Anpario (LON:ANP) (£75m) | Full year TU | Stronger than expected H2 performance. Rev £37.5m, EBITDA ahead of exps. | GREEN (Graham) |

Equipmake Holdings (OFEX:EQIP) (£15m) | Results for six months to Nov 2024 | Rev +19% to £2.5m, adj. operating loss £3.95m, in line with exps. | |

One Media IP (LON:OMIP) (£9m) | TU | FY Oct 2024: rev £5m, EBITDA £2.1m (+15%). Strategic disposal: “much stronger position for 2025”. |

Summaries

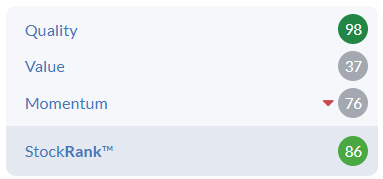

Alliance Pharma (LON:APH) - up 38% to 61p (£330m) - Recommended Acquisition - Graham - PINK (takeover)

It's a 40%+ premium takeover offer from APH's largest shareholder, although they point out the shares have more than doubled since they originally approached the APH board. It's a shame to lose another decent company from the UK market, but at the same time reassuring of the value that is probably still available!

Short Sections

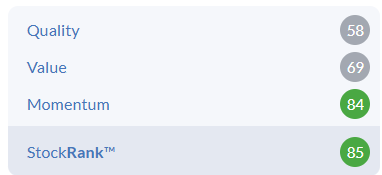

Anpario (LON:ANP) - up 9% to 400p (£83m) - Full year trading statement - Graham - GREEN

It’s a positive update from this provider of animal feed additives: year-end sales were higher than expected, so that full-year revenue is now thought to be c. £37.5m (consensus: 35.25m). Higher sales, operational gearing and fortunate foreign exchange movements result in EBITDA being ahead of expectations: Shore Capital have consequently boosted their adj. EBITDA forecast by c. 18% to £6.6m, and they note that this is the fifth upgrade to 2024 forecasts, with four of these coming from positive trading and one coming from an acquisition.

The acquired Wisconsin-based company Bio-Vet “had a strong final quarter due to heightened demand for its products, which support the health of dairy cows affected by avian influenza”, while ANP’s Middle East and Africa segment “delivered an outstanding sales performance”.

And ANP’s year-end cash balance is virtually unchanged on last year at £10.5m, despite spending USD $6m on that Bio-Vet acquisition.

Graham’s view: I’m happy to leave the prevailing GREEN stance unchanged here after yet another positive trading update. If there’s a lesson today, maybe it’s not to fight momentum! Although ANP’s strongest feature according to the StockRanks is its quality. Anpario’s growth over the long-term has been unimpressive but it has built up a head of steam over the past two years and may be worthy of further investigation.

Clarkson (LON:CKN)

Up 8% to £42.20 (£1.3bn) - Trading Statement - Graham - AMBER/RED

The briefest of updates from this shipping company:

Clarkson PLC, the world's leading provider of integrated shipping services, today announces that results for the year ending 31 December 2024, are now anticipated to be slightly ahead of current market expectations.

Clarksons' underlying profit before tax, subject to audit, is now expected to be not less than £115m.

This one was last covered in August, and there haven’t been any other results since then. Those interim results published in August showed a small reduction in H1 revenues and underlying profits, but H2 is seasonally more important than H1.

The latest update from Panmure, published today, raises forecasts by 3%: they are now suggesting that FY24 EPS will be 285.4p (FY23: 275p). FY25 is expected to come in slightly lower than that at 279.3p.

That puts the shares on a forward PER of 15x. Maritime/shipping is not my area of expertise but I am struggling to see the opportunity here - shouldn’t this trade at a low-ish PER, to reflect cyclical shipping demand? I think I’ll leave AMBER/RED unchanged for now.

Backlog

SIG (LON:SHI)

Flat yesterday at 15p (£179m) - Trading Update - Megan - RED

Building supplier SIG can blame the poor macroeconomic environment for another year of disappointing results as much as it likes. But it’s hard to find a period of time when it was delivering positive results, regardless of what was going on in the wider economy.

In 2024 the company will report annual revenues of £2.61bn, which is almost exactly what they were ten years ago. In that time SIG has only managed to report revenue increases three times and it’s never managed to string together two consecutive years of sales growth. The 2024 numbers are 4% lower than 2023.

It’s a bleak picture for a company which also suffers from ridiculously low margins. In the first half of the year, SIG incurred £992m of sales costs off £1.3bn of revenues. Operating expenses of £314m left only a sliver of operating profits and the company reported interim net losses.

Yesterday’s trading update indicates that there has been no turnaround in fortunes in the second half of the year. Although SIG is expected to report underlying operating profits of £25m, it is likely to be loss making at the bottom line and will report a free cash outflow of £39m.

It’s also worth being wary of the balance sheet. After refinancing €300m of its borrowing in October, the company’s net debt position stands at £496m, which is almost three times the company’s current market capitalisation and 4.7 times its equity.

Megan’s view:

There could be a value argument to be made for a company which is valued at less than 10% of its annual sales. Even if you add in the debt the EV/Sales ratio is just 0.25.

It’s also worth noting that it has been a very difficult period for companies in the construction sector and SIG’s products are well placed to benefit from rising demand under Kier Starmer’s environmentally-friendly building pledges.

But there is no getting away from the fact that even in the good times, SIG struggles to generate a decent profit. And that debt is alarming. I would stay away. RED

Fast Retailing Co (TYO:9983)

Up 1% yesterday to 52,100yen (£81.6bn) - First quarter results - Megan - GREEN

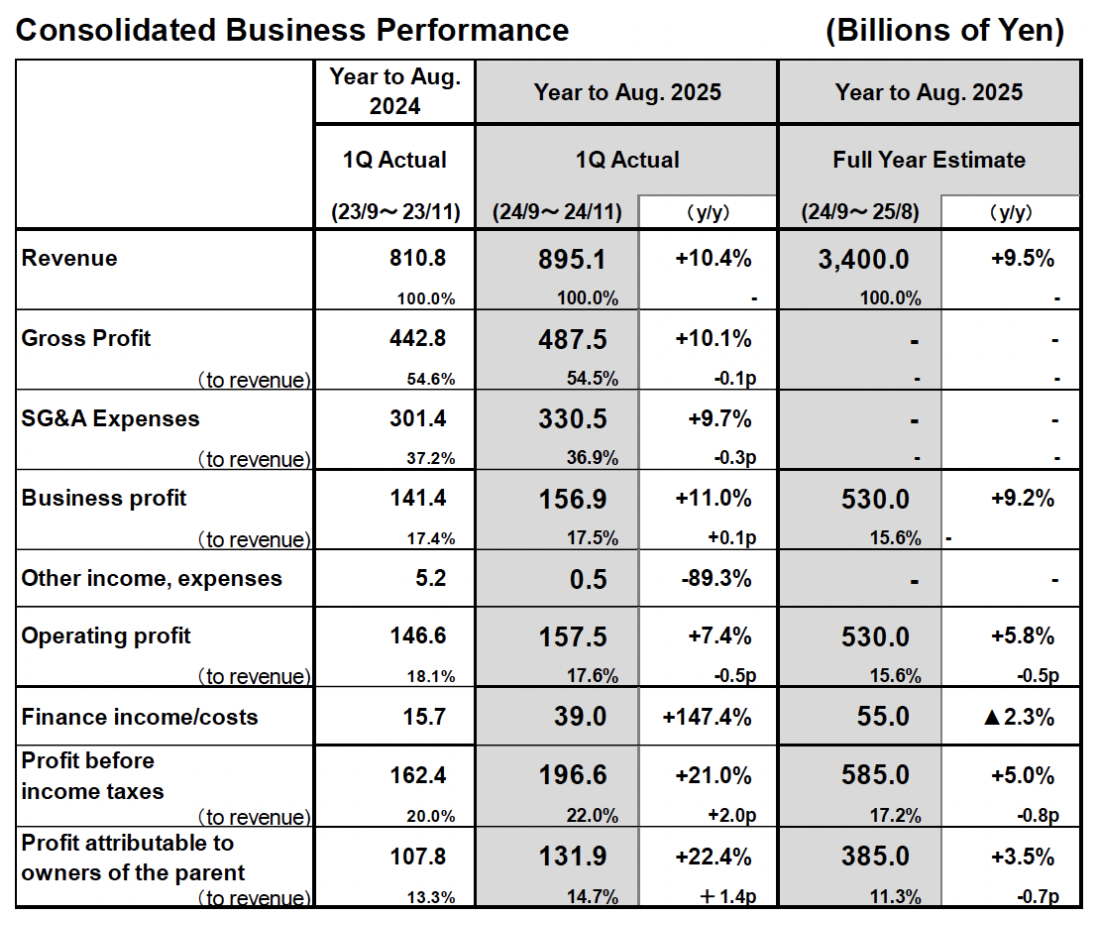

Investors who appreciate a nicely laid out set of financial results might enjoy a scan over the numbers at Fast Retailing.

The Japanese company, which is best known for its Uniqlo brand, reported numbers for the three months to November 2024 (the first quarter of the 2025 financial year which ends in August) which opened with this table:

Management goes on to clearly lay out the divisional performance and explain how each part of the business has done well or badly.

And overall, there are definitely more examples of ‘done well’ than ‘done badly’ After reporting its first ever year of 3trn yen in revenues in FY2024, Uniqlo has continued to deliver growth this financial year. Sales were 9% higher in Japan at 266bn yen and 14% higher in international markets at 502bn yen.

Margins are slightly lower than in 2024 and that is expected to persist for the rest of the year, but it reflects the company’s move into its next phase of growth. At the annual results, chief executive Tadashi Yanai said that the focus for investment would be in human resource development and that this would help stimulate further expansion.

It’s a fascinating comparison to executive reports from western companies, where management teams don’t need much excuse to talk about automation and robotics. Human resource development is a far cry from the tech-focused spending that is going to help enhance margins at US and European retailers.

There is something quite refreshing about Fast Retailing’s attitude to growth, which has certainly worked wonders in the past. The company listed 30 years ago and its share price has risen nearly 100-fold in that time.

Megan’s view

I recently acquired my first ever Uniqlo product - a fleece given as a Christmas present. I also browsed my first Uniqlo store (they have been popping up like crazy in the UK) and it was packed. The brand is certainly gaining traction in the UK and the US and it looks like there is more room for growth.

The shares aren’t that easy to come by for UK investors and for those who are interested, they are very expensive, trading on almost 40 times forecast earnings. But I like the company a lot and so for purely illustrative purposes, my rating is green.

Graham's Section

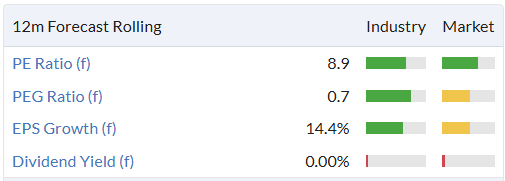

Alliance Pharma (LON:APH)

Up 38% to 61p (£330m) - Recommended Acquisition - Graham - PINK (takeover)

Another day, another acquisition of a UK-listed stock.

It’s an early win for Ed’s 2025 QVM Portfolio, which included Alliance Pharma as one of its healthcare entries. Strong momentum was the main clue that things were going well:

The share price found a floor over the past year:

In June, Paul gave the company a big upgrade after it reduced its leverage multiple and restated its intangible assets to more accurate (lower) levels.

The buyer: DBAY Advisors, an Isle of Man-based investment manager. DBAY previously acquired Finsbury Foods (FIF), and it already owns 28% of Alliance Pharma.

The price: 62.5p in cash, a 41% premium to yesterday’s close. Not overly generous, as 30% is typically the bare minimum that I look for in a takeover bid. The announcement points out that it’s a 113% premium to the price before DBAY’s initial approach to the board of Alliance Pharma.

Rationale: DBAY says that Alliance’s public listing has “potential for management distraction” and there has been “limited recent liquidity of Alliance Shares”, so that the listing “does not currently offer significant benefits for the business”.

More positively:

DBAY is supportive of Alliance's leadership team and believes in Alliance's future prospects but considers that Alliance needs to implement a range of operational and strategic initiatives, in conjunction with a period of accelerated investment and selective acquisitions of complementary products, in order to fulfil the growth potential of the business. It has become apparent to DBAY that Alliance needs time away from the public market to allow it to fully deliver these initiatives in a reasonable timeframe.

Irrevocable undertakings: I don’t see much in the announcement in relation to shareholders who have already pledged to support the takeover. The CEO supports it, and I can only presume that Slater Investments (13% shareholder) supports it. On that basis, I presume that it will go ahead.

Graham’s view: it’s a shame to lose yet another company from the UK market but at the same time, it’s reassuring that there is probably still a great deal of value out there available to us!

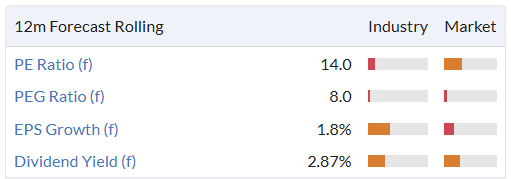

DBAY are getting a good deal on a 1-year P/E basis, and if their investment plan for the business works out, they could do extremely well:

J Sainsbury (LON:SBRY)

Down 3% to 255.3p (£6.0bn) - Trading Statement - Graham - AMBER/GREEN

We don’t cover SBRY very frequently but after giving TSCO a mention yesterday and with this stock appearing on today’s “Most Viewed” list, I thought I would take a quick look.

The market doesn’t seem to like this update, despite a reaffirmation of guidance for FY Feb 2025.

CEO comment opens positively:

"We have won grocery market share for the fifth consecutive Christmas, with more customers choosing Sainsbury's for their big shop. Driven by our leading combination of quality, value and service, we have achieved seven consecutive quarters of volume performance ahead of the market and further accelerated our two-year volume growth.

The figures:

Like-for-like retail sales +2.8%, excluding fuel.

Sainsbury’s +3.7%, Argos minus 1.4%.

Grocery (+4.1%) outperforms General Merchandise & Clothing (-0.1%).

FY Feb 2025 outlook: retail underlying operating profit in line with consensus and the midpoint of the guided range £1,010-1,060m, growth of 7%.

Financial services is much smaller with underlying operating profit of £30m but this is ahead of guidance (£15-25m).

Graham’s view: as with TSCO, I can’t get too excited about shares in this mature, below-average quality sector. However, as with Tesco, I am inclined to also give SBRY an AMBER/GREEN stance.

Like many UK blue-chips, this is likely to be of most interest to dividend gatherers who also want the possibility of some growth:

With Tesco and Sainsbury both claiming to win market share, it must be coming from somewhere and that “somewhere” apparently includes Asda and Aldi (external link), although Lidl has continued to grow.

Figures from September:

Asda’s share plummeted to 11.8% in the 12 weeks to 7 September, from 13.1% a year ago. Meanwhile, Aldi’s share also slipped from 10.7% to 10.3% over the same period.

The decline of Asda tallies with rival analyst Kantar’s data, which found that its share had fallen 1.2 percentage points to 12.6% in the 12 weeks to 1 September.

Competition is inherently intense in this sector, which is one of the reasons I stay away from it. Having said that, I don’t have any particular criticisms to make of either TSCO or SBRY. If I was only interested in maximising income without taking on too much risk, their shares would definitely be up for consideration.

One major factor to consider is of course the increase in NICs and whether they could take a meaningful bite out of profits. CEO Simon Roberts is quoted by the BBC today as saying “We’ll have to look very carefully at all hiring decisions”. Price rises for customers look inevitable, as part of mitigation efforts. But all supermarkets are in the same boat as they attempt to deal with this issue.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.