Happy Valentine's Day,

Mark has given us a view on TATE to get us started.

1pm: hanging up my pen there for the week, have a nice weekend!

New research piece by Alex: Can brokers outperform simple algorithms in the world of investing?

The Week Ahead has been written by Keelan this time, including an in-depth look at Jet2 which will publish a full-year trading update next week.

Share price movements today

At the Investors Chronicle, Simon Thompson has published his bargain shares for 2025. These include my largest holding Volvere (LON:VLE) in addition to Crystal Amber Fund (LON:CRS), Gattaca (LON:GATC), Creightons (LON:CRL), Agronomics (LON:ANIC), Assetco (LON:ASTO), Carr's (LON:CARR), K3 Business Technology (LON:KBT) and Tavistock Investments (LON:TAVI). Several of these shares have risen in response to being tipped in this way.

My attitude to this is as follows: if I was already thinking about selling, then the day of a tip is a fabulous day to sell, as I'll probably get a higher price with extra liquidity.

On the other hand, if I wasn't thinking about selling, then I take no action. I haven't sold any of my VLE shares yet but as they approach my estimate of fair value I may start thinking about it!

In general, the people who react to a tip by buying are very unlikely to have the patience to stick around for the long haul, as they don't have real conviction of their own in the idea. So in the end, I don't think that tips make much of a difference: you get an initial spike of buying activity, but then it quickly dissipates. The new buyers will probably sell and move on to something else before too long.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Natwest (LON:NWG) (£35.2bn) | Annual Results | EPS 53.5p, up 12%. RoTE 17.5%. TNAV per share increases to 329p. Outlook: RoTE 15-16%. | AMBER/GREEN (Graham) [no section below] Outlook for 2025 suggests a small deterioration in return on tangible equity (ROTE) but income is expected to rise >4%. Possible small rise in impairments to 20 basis points. CET1 stable at 13-14%. I think it's ok to be moderately positive on the major banks although they are not the bargains they once were. PER 8x. |

Coca-Cola Europacific Partners (LON:CCEP) (£30.3bn) | Preliminary Results | Rev +3.5%, operating profit +8% (heavily adjusted figures). Guidance: rev +4%, op profit +7%. | |

SEGRO (LON:SGRO) (£9.8bn) | Results for FY24 | 5% growth in earnings and dividends. £91m in new headline rent. Confident outlook for 2025. | |

XPS Pensions (LON:XPS) (£719m) | TU | FY March 2025 materially ahead. Rev £226-229m, +15-16%. Efficient delivery, op. leverage. | AMBER/GREEN (Graham) Downgrading this as valuation is starting to make me nervous. But it's a very impressive growth story and I remain generally positive on it. |

John Wood (LON:WG.) (£452m) | TU | FY24 in line. Prior years may need to be restated. Outlook: EBITDA in line but with negative free cash flow and additional cost reductions needed. | RED (Graham) Totally uninvestable. Admits it has problems with its financial culture. Terrible balance sheet, debts expiring next year. Needs to fix a range of problems before I'd consider changing my stance. |

Distribution Finance Capital Holdings (LON:DFCH) (£69m) | Authorisation to conduct consumer lending | Plans to launch asset finance/hire purchase in H1, having received FCA authorisation. | |

Fiinu (LON:BANK) (£34m) | Equity fundraise | Raised £1.25m at 10p (last night’s SP: 12.5p). Use of funds: develop “Plugin Overdraft” product. | |

Transense Technologies (LON:TRT) (£22m) | Strategic partnership | Ohio-based Haltec becomes a formal distributor of TRT’s advanced tyre inspection tools. | |

Totally (LON:TLY) (£13m) | Outlook update | Profit warning: FY March 2026 expectations assumed the renewal of an NHS contract. | AMBER/RED (Graham) Low-margin service providers deserve modest valuations. This one may offer some speculative upside but I don't see it as a solid investment opportunity. |

Backlog

Tate & Lyle (LON:TATE)

Down 9% to 575p - Trading Statement - Mark - AMBER

This statement starts off well:

Tate & Lyle delivered another quarter of solid operating performance, with volume and EBITDA growth and continued strong cash delivery.

Like many businesses at the moment, they are cost-cutting:

We delivered further productivity savings during the quarter, with good progress against our five-year US$150 million productivity target.

But this doesn’t seem to be enough, as the rub is:

For the year ending 31 March 2025, excluding CP Kelco and in constant currency, we now expect revenue to be mid-single digit percent lower and for EBITDA growth to be towards the lower end of our guidance range of 4% to 7%.

Perhaps not surprising when they have revenue down 6% in the first 9 months of the year. Last year they generated £328m EBITDA, so 4% growth works out to be £341m. It is a seasonal business, but they say:

While market demand remains broadly stable, we have not yet seen the acceleration in demand we expected in the second half of the 2025 financial year

As always seems to be the case with these things, they have completed their buyback program just before a profits warning and share price drop!

On 9 January 2025 we completed our £215 million on-market share buyback programme to return the net proceeds from the sale of our remaining interest in Primient to shareholders.

They probably can’t afford another buy back in the short term, as the acquisition of CP Kelco leaves them with significant leverage. In October, following the CP Kelco acquistion, they said:

Net debt to EBITDA leverage anticipated to be approximately 2.3x at the financial year-end following completion.

But this is presumably now a bit higher due to EBITDA coming in at the lower end of guidance.

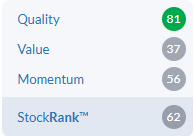

Mark’s view

The CP Kelco acquisition makes it really hard to value this as it impacts the EBITDA, net debt and share count. So, in this case, I defer to the StockRanks of the pre-acquisition business:

These suggest that it is a reasonable business but one that is hard to be excited about. Particularly when many other UK-listed stocks look cheap at the moment. AMBER

Graham's Section

XPS Pensions (LON:XPS)

Up 11% to 385p (£802m) - Trading Update - Graham - AMBER/GREEN

Let’s start with the good news story of the day. Performance at XPS is materially ahead of expectations.

XPS Pensions Group plc ("XPS" or the "Group") is pleased to provide an unscheduled trading update (unaudited) for the year ending 31 March 2025.

Revenues are now expected at £226-229m, vs. consensus forecast of £226m.

Revenue growth will be pushing 16% at the higher end - and with only a month and a half left until year-end, surely the company must believe that it is likely to get close to £229m?

However, beating the revenue forecast by less than 2% is not enough for performance to be materially ahead. There must be conversion into higher profits. Let’s read on:

High levels of demand for our services from continued regulatory change, new clients, and the inflation-linkage of our contracts, combined with the resilience and predictability of our business model has driven a strong performance for the year. Growth drivers in the year include GMP [guaranteed minimum pension] equalisation, rectification projects following the McCloud judgement, and the impact of new business wins in the Risk Transfer market.

Thanks to XPS’s cost management, efficient delivery and operational gearing, full-year results are therefore anticipated to be materially ahead.

Estimates

Thanks to Canaccord for spelling this out for us in a new research note. Their new PBT forecast for FY March 2025 is £57.9m (previously £54.7m).

At first glance, it seems that this might be a case of an additional few million pounds of revenue dropping through very efficiently into profits.

However, according to Canaccord, who are the company’s broker, the main driver is work relating to the McCloud judgement being delivered more efficiently than previously expected. So it is mostly on the cost side of the equation that XPS has succeeded.

For FY March 2026, there is a smaller increase in expectations, with the adj. PBT forecast rising from £58.3m to £58.9m. And there is another, even smaller increase in expectations for FY March 2027.

CEO comment:

"We are pleased to be on course for another year of strong financial performance. There has been strong demand for our services, as clients have needed support to respond to market and regulatory changes. At the same time as achieving strong growth, we have been delighted with the results of our annual client survey, which were extremely positive. At XPS our culture is at the heart of what we do, and I would like to thank all our people for the way they support each other and our clients."

Graham’s view

I’m a little perplexed by the 11% increase in the share price today.

The PBT forecast for the current year has only increased by 6%. I get that this is “materially ahead” of expectations, but when it’s delivered through cost management rather than incremental revenues, this is not the most exciting way to beat forecasts. Cost management cannot be relied upon to deliver growth indefinitely!

This is borne out in the fact that broker PBT forecasts for future years have barely budged.

So I would have thought that a more modest share price increase this morning would have been justified.

Thinking about the company more broadly, this is a stock that we’ve liked for some time.

I was GREEN on it in June 2023 at 170p, thinking that it was a little expensive relative to earnings at the time, but that it had the potential to keep growing. I liked the high rate of organic growth (17% at the time) and inflation-proof, recurring revenues. There seems to be no shortage of demand for pensions-related services.

The June 2023 review was followed up by more GREEN reviews in November 2023, June 2024 (by Paul) and October 2024 (again by Paul).

Not only have earnings grown substantially, but the multiple attached to those earnings has grown too - from about 14x to 18x. The compound effect is that the share price has more than doubled.

Based on the latest share price and Canaccord’s update, the latest P/E ratio is about 20x. And that’s using adjusted EPS - the actual P/E ratio will be higher than this.

So perhaps I should downgrade this to AMBER/GREEN now, on valuation grounds?

In 2023, the earnings multiple was 14x and organic growth was 17%.

Now, the earnings multiple is 18x and there is only revenue growth of up to 7% pencilled in for next year. PBT is only forecast to grow by 2%.

However, as it has in the past, I believe that XPS is very likely to beat these expectations:

So we might be able to assume with some confidence that XPS will beat the latest set of expectations.

But I fear that it will be much harder to prove that it is undervalued, now that it is already trading at an adjusted PER of 20x. And at this sort of rating, any disappointment could lead to a sharp reversal.

I am therefore going to downgrade my stance this to AMBER/GREEN. I’m still very impressed by its growth and I like it as a candidate for a long-term hold. But the valuation is starting to worry me a little.

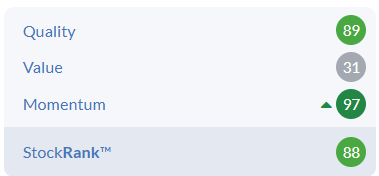

The StockRanks see the same thing:

John Wood (LON:WG.)

Down 33% to 43.5p (£302m / $380m) - FY24 Trading Update - Graham - RED

There is a lot to unpack with this trading update but firstly can I say commiserations to anyone holding this overnight. A 33% fall would be enough to unsettle anyone.

We last covered this in November, a day when WG shares fell 44% in response to the previous major profit warning.

I’m relieved to see that I was fully RED on it then due to its “extraordinarily high risk and a lack of redeeming features”. Problems included:

horrific interim results

continued exposure to losses from historic risky contracts

the need for an independent review of contracts, seemingly instigated by WG’s auditor

Negative tangible book value

Extremely high receivables

Net debt of nearly $700m excluding leases.

Today’s update tells us that FY24 EBITDA of $450-460m is “broadly in line with guidance”.

FY23 EBITDA was $423m, so full-year growth will be 6.4% to 8.7%. This is indeed close to previous guidance for “high single digits”

However, the bad news starts here.

There was weaker-than-expected Q4 trading, and the company mitigated that by cancelling executive and employee bonuses and “actively managing working capital at year end”.

Net debt excluding leases is still nearly $700m and that’s the year-end figure. Kudos to the company for publishing its average net debt figure, even if it’s an unsettling one: $1.1 billion.

Independent review: this is ongoing. WG are “evaluating the extent of prior year adjustments which the company expects will be required”.

Given prior results, it has become pretty obvious that the numbers here are a mess. So it’s no surprise that more adjustments are needed. The only question is how big they might be. We’ll have to wait to find out.

WG admits to having serious problems. It’s rare that we see “financial culture” being acknowledged as a weakness:

The Company is initiating steps to strengthen significantly the Group's financial culture, governance and controls in light of material identified weaknesses and failures

Transformation: as we knew already, WG is not doing any more “lump sum turnkey” work, as they are the riskiest type of contract.

WG has been in the worst of both worlds: on the one hand being aggressively pursued by some customers in relation to the work done, while at the same time having to pursue other customers who have failed to pay. It seems that lump sum turnkey contracts have a tendency to create this situation.

On the cost front, WG are looking to achieve savings of $60m in FY25 and then a further $85m in FY26. There will be one-off costs involved in this.

They say in bold:

Following these actions, the business will be on a firmer operational footing, but cash generation has yet to materialise and financial strength needs significant improvement

Updated 2025 outlook

We expect double-digit adjusted EBITDA and adjusted EBIT growth (excluding the impact of disposals) in 2025

This remains in line with market expectations, though our pathway to this now includes taking additional cost reduction measures as outlined above

So they will only achieve their EBITDA/EBIT targets by cutting themselves down in size.

And the costs of cutting - redundancy, etc. - will be categorised as exceptional items. So there is little hope of clean accounts any time soon.

Negative free cash flow is expected, at minus $150m to minus $200m. The company plans to balance this with disposals. Average net debt is again expected at $1.1bn, before taking disposals into account.

Graham’s view

This is totally uninvestable in my view.

There is a $1.2bn RCF expiring in October 2026, and a $200m term loan expires then, too. The clock is ticking. WG has managed to pass its covenants up to this point, but my worry is that they have only done this by resorting to extreme measures, and that more extreme measures may be required.

They are not allowed to have a leverage multiple (net debt to EBITDA) of more than 3.5x, and they are not allowed to have interest cover of less than 3.5x.

At the interim results, they reported a leverage multiple of 2.5x and interest cover of 3.9x. So they were in compliance then.

My sense is that they are now running the company on the basis of keeping a compliant EBITDA figure, as they have no other choice. But successful businesses do not operate this way.

I don’t know if there is any price at which I could turn positive or even neutral on this share. The list of problems and red flags just goes on and on. From an investment point of view, my stance is the same: it’s extraordinarily high risk, with a lack of redeeming features.

Totally (LON:TLY)

Down 23% to 5.1p (£10m) - Outlook update - Graham - AMBER/RED

This health service provider was well-summarised by Paul in 2023:

The fundamental problem with TLY, is that it’s doing quite big, low margin contracts for the NHS, but seems to have a fair bit of risk within those contracts - both cost over-runs, and uncertainty over renewal.

Today we learn that TLY’s NHS 111 contract has not been renewed by NHS England. It’s not a reflection of TLY’s work, but of a change in strategy at the NHS.

Revenue from the existing £13m contract was already going to be mostly recognised in the current financial year (FY March 2025).

For this financial year, TLY is still in line with expectations (£85m revenue, £3.5m EBITDA - note the very low EBITDA margin!)

Here is the profit warning:

The Board's financial expectations for the year ending 31 March 2026 did assume a renewal of the NHS 111 Contract, however at a reduced level. Work will commence to redeploy workforce where possible along with securing new contracts with new providers, although exceptional costs are expected. Based on the current revenue run rate of the Company, new contract wins and the current new business pipeline the Board now expects the financial performance of FY26 to be at a similar level to that which is expected to be reported for FY25.

Estimates: with many thanks again to Canaccord who have released a new revenue forecast of £85m for FY March 2026 (down from £95m) and a new FY March 2026 EBITDA forecast of £3.5m (down from £4.5m). So the loss of this contract is resulting in the loss of c. £10m of revenue and £1m of EBITDA. The implied EBITDA margin on this lost contract is unfortunately much higher than the average EBITDA that TLY earns across its business.

The new FY March 2026 forecasts now perfectly match the forecasts for FY March 2025.

Canaccord value the stock based on an EV/sales multiple. Using an earnings-based multiple isn’t appealing, as profits aren’t at a meaningful level - adj. PBT is expected to be less than £1m.

Graham’s view

The low margins here are very unappealing. I suppose this could be interesting on a speculative level as it’s perfectly possible new contracts (as resources are redeployed) and small changes in the revenue/cost equation could lead to profits spiking in the next year or two. But for now the company is bobbling around, not far above breakeven. I think that low-margin service providers such as this do deserve modest valuations. I’m AMBER/RED.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.