Good morning and Happy Friday! The Agenda is very short today.

My colleague Alex has published a new research piece on the value of broker price targets and whether or not they are worth following: here's the link. The answer did not surprise me! But it's great to see the verification.

12.30pm: Hanging up my pen there for the week. Have a nice weekend!

Spreadsheet that accompanies this report: updated to 14/2/2025.

I've updated this and found the following statistics.

In the first 15 weeks of the new format, we have given views on:

- 340 unique companies

- 92 companies at least twice

- 19 companies at least three times

- 5 companies four times! (BOO, FTC, SQZ, TIME, VLX)

Cheers!

The Week Ahead has been published by Keelan this time - check it out for a preview of next week!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Standard Chartered (LON:STAN) (£27.5bn) | FY24 Results | Return on tangible equity 11.7%, up 160 basis points. CET1 ratio 14.2%, above target range. | |

Ceres Power Holdings (LON:CWR) (£156m) | Statement regarding Robert Bosch GmBH (yesterday) | Bosch ending its partnership with CWR and selling its 17% stake. No change to FY25 expectations. | AMBER/RED (Graham) It still has enough cash to fund its losses without external help for at least a few years, but not as long as I thought it did the last time I covered this stock. |

Litigation Capital Management (LON:LIT) (£79m) | Judgement delivered in class action investment | Invested $13.2m in a class action case that has been unsuccessful. Considering the merits of appeal. | AMBER (Graham) I think this is still trading at a discount to book value. Potentially interesting but difficult to analyse. |

Videndum (LON:VID) (£57m) | TU | FY24 was in line. Won’t meet March 2025 bank covenant. Banks “supportive”. Discussions ongoing. | RED (Graham) The existing equity is not secure. Bank covenants were already loose but the company still can't meet them. |

Ceres Power Holdings (LON:CWR)

Down 38.5% yesterday to 81p (£156m) - Statement regarding Robert Bosch GmbH - Graham - AMBER/RED

We probably should have covered this yesterday, but better late than never I hope!

I looked at CWR in January, taking a neutral view as the company had cash and short-term investments of £102m, which I figured might be enough to fund it through to profitability.

I generally take a negative view on unprofitable start-ups, but the main reason for that is the risk of dilution when they run out of funding.

For a fully-funded start-up, I can take a more relaxed view. I still greatly prefer to invest in established, profitable businesses, but I don’t feel the need to be negative on a company that is trying to establish itself, if there is little risk of dilution.

So I took a neutral stance on CWR.

Unfortunately, that was too optimistic as yesterday’s news shattered confidence.

One of the attractions of CWR is its blue-chip partnerships with companies like Bosch and Shell.

The partnership with Bosch is now dead as the German engineering and technology company has decided to focus on hydrogen from now on, instead.

Bosch says:

Bosch is realigning its activities and investments in stationary hydrogen technologies. In future, the technology company will focus more on technologies for hydrogen production…

Against this background, activities related to the industrialization and series development of systems for decentralized energy supply based on solid oxide fuel cell technology (SOFC) will be terminated.

The partnership with CWR will be terminated by Bosch “in an orderly manner while fulfilling its contractual obligations”.

The explanation given is that “the market has developed differently than expected in the recent past”. I'm afraid that chemistry was my worst subject at school, and I’m not going to be able to explain why hydrogen has a better outlook than solid oxide fuel cells.

Shareholding: the news is extra painful for CWR as Bosch is their second-largest shareholder. This stake will now be considered as a “non-core financial investment”, and possibly sold.

The Bosch representative on the CWR board has resigned with immediate effect.

CWR says that the Bosch decision does not change expectations for FY December 2025. As pointed out in the comments yesterday, this may be due to Bosch fulfilling its contractual obligations for the year, but estimates for future years should see an impact.

CWR’s CEO comment:

Whilst Ceres is disappointed that Bosch will discontinue its operations relating to the industrialisation and preparation for production of decentralised power-supply systems using Ceres' solid oxide technology, we recognise that this decision is part of a broader revised strategic direction from Bosch and does not reflect its confidence around Ceres or our technology.

Graham’s view

This may surprise readers but I’m not sure I want to take a very negative view on CWR today!

The reason is simply that £102m cash balance which it held at the end of 2024.

The company’s financial losses have been enormous, however, so I do need to try to understand how vulnerable the cash is to drying up.

I also think the decision by Bosch is damning in the sense that Bosch will have an intimate understanding of the industry dynamics at play. If they don't see a compelling opportunity here, I fear that they might be right.

But let's get back to the finances.

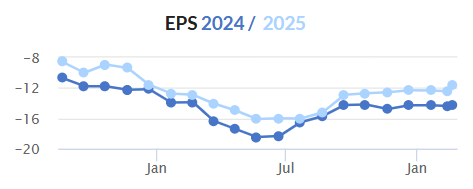

CWR is forecast to make an accounting loss of £28m in 2024, £23m in 2025, and £17m in 2026.

I will use the forecast accounting loss as a proxy for cash flow. But note that CWR burned through cash of £38m in 2024 despite an estimate for the accounting loss of only £28m. So cash flow can be much worse (or better) than cash performance.

The forecast losses for the next two years add up to £40m.

Historic earnings momentum hasn’t been great:

Combine that track record with the loss of the Bosch partnership, and I think it’s reasonable to assume that the losses over the next two years will add up to materially more than £40m. I don’t know how much higher they might be - shall we say £50m? And who knows what the cash performance might be over that timeframe!

Therefore, while I don’t really want to downgrade my stance on CWR, I feel obliged to.

If its accounting losses are worse than existing forecasts and if they do convert to negative cash flow, half of the cash balance would be gone in two years.

It does still have time to improve performance and I'm also sure there is every chance that investors would want back it again, if necessary, to extend its journey to profitability.

However, as I no longer have confidence in CWR being able to fund its losses without external help for an extended period of time, I’m going to move my stance on this lower, to AMBER/RED.

The StockRanks got this one right, while I didn’t. Here is CWR’s StockRank as of two days ago:

Videndum (LON:VID)

Down 33% to 41.7p (£39m) - Trading Update - Graham - RED

The risk of VID getting into financial difficulty was apparent from previous company announcements, so I hope that the only people left holding it are those who can afford to withstand this sort of share price volatility.

In September, on the day of a profit warning to go with the interim results, I noted that the previous annual report included a going concern warning. The leverage multiple was still very high, and banking covenants had been relaxed to weaker levels.

In December, we had another profit warning. Net debt was rising and the covenants for Dec 2024 were relaxed even further. The company said it was working on an extension or refinancing of the facility (due to expire in August 2026), and was now seeking amendments to the Feb 2025 and March 2025 covenants. The company went into cash conservation mode: cutting costs, merging divisions, and raising prices.

This brings us to today.

The good news is that FY24 results are in line and the amended Dec 2024 covenant was met.

And the February 2025 covenant test has been waived altogether.

The bad news is that the March 2025 covenant test has not yet been waived.

The company acknowledges that it will not be able to pass this covenant.

So without a waiver or further amendment, we could be looking at a technical default on the March test.

Remember that this facility expires completely in August 2026:

The work required to refinance the Revolving Credit Facility, set to expire in August 2026, continues and our lending banks remain supportive of the Company.

Restructuring is ongoing with a new 2025 cost-saving target of £15m (previously: £10m). But there are also restructuring costs of £15m. So we might not see much of a benefit in the short-term.

Exec Chairman comment: I’m fully negative on this share, so let’s counterbalance that by posting the Exec Chairman’s comment in full.

"The gradual improvement in our markets has continued. We are seeing improving signs, particularly in Cine and Broadcast, in terms of quantity and quality of projects and enquiries. These should start turning into stronger order momentum once we get past the traditional doldrums of January and early February. While we are not planning on a strong uptick in orders and revenues as we drive the business forward, we are gaining increasing confidence that the direction of travel is for improved strength in revenues as we move through the year.

"There is still work to do, but I am confident that we are on the right path - building a stronger business, well positioned to capitalise on the market recovery".

Graham’s view

The company says that its brands are “leaders in defensible niche markets”. That may be true, and perhaps current management can turn it around. It has apparently been unlucky - affected by Covid, the Hollywood strikes, and perhaps some poor decisions by previous management. Maybe with all of these events out of the way, it can move on to better times?

However, while the company’s finances are in disarray to such an extent that it cannot meet very loose bank covenants, it’s an automatic RED from me.

If someone really liked this business, it might make sense to buy fresh equity from the company at a deep discount, or to buy the debt off the banks, if either of those options became available.

But as things stand, with £100m+ of net debt excluding leases and unable to pass covenants, the existing equity is not secure.

My main surprise today is that the share price has reacted so negatively to this announcement - is it really surprising that VID won’t meet its March covenant, or that the banks are taking their time in approving a waiver?

Litigation Capital Management (LON:LIT)

Down 14% to 66.9p (£76m) - Judgment delivered in class action investment - Graham - AMBER

LIT is “an alternative asset manager specialising in dispute financing solutions internationally”. Its headquarters are in Sydney, Australia and it has offices in various other locations including London.

It can be compared with Manolete Partners (LON:MANO) and Burford Capital (LON:BUR).

Today’s news is that a case in which LIT invested $13m (Aussie Dollars) of its own capital has been lost. That’s just under £7m.

They do have a right to appeal, and are considering the merits of it.

I don’t think the specifics of the case are very important to us. It was a class action lawsuit on behalf of the shareholders of an Australian company.

CEO comment:

… It is an unusual outcome that the court found that the financial statements in question were misleading, but that this did not result in loss for the shareholders in Quintis. Our focus now is on assessing the Judgment and determining the best course of action alongside our legal team. We remain committed to our disciplined approach in managing risk and capital across our portfolio."

I tend to stay away from this sector. Companies like this can sometimes have very large exposures to particular lawsuits. When they work out, it’s terrific, but I don’t know if I’d be able to sleep at night!.

This attitude kept me out of Burford, which has multi-bagged for its long-term shareholders.

I think it’s reasonable to value them relative to book value. LIT had net assets of $188.9m (£95m) as of its most recent year-end (June 2024).

Since then, it published a trading update in January 2025 which said that its aggregate wins and losses in H1 had realised $52m from cases in which it had invested only $14m.

However, the uplift in terms of balance sheet gains would only be $4m, as these cases were already valued on the balance sheet at $48m.

I was wondering if the valuation of the Quintis lawsuit on LIT’s balance sheet might have been substantially higher than the $13m invested in it, in anticipation of a win.

However, according to broker Cavendish, responding to today’s news: “At most, this will lead to a $13.2m write-down from the investments made from its balance sheet”. That sounds reassuring.

Cavendish also says that LIT’s concentration risk with respect to individual cases is “now reducing as its co-investment model matures”.

Graham’s view

With some back-of-the-envelope calculations using the full-year results (to June), the H1 trading update (to December) and today’s update, I think that LIT’s balance sheet might now be worth c. $165m (£82m). I’m not sure of course, but something in that ballpark seems about right, after taking into account the loss announced today.

Net debt was $40m as of Dec 2024.

I’m on the fence between AMBER and AMBER/GREEN. I think that a discount to book value is still on offer, even after today’s news. LIT’s peers seem to be trading at a premium to book. And LIT’s overall track record seems pretty good.

But at the same time, it’s not easy for me to trust the valuations of legal cases.

To be careful, I think I’ll stay AMBER for now. I would be willing to upgrade my stance if a larger gap appears between the share price and book value.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.