Good morning!

I don't know about you, but I'm finding it harder to spot obvious bargains in these markets. There are still certain stocks that appeal to me, they are just... rarer.

One stock that does appeal to me at the moment is B.P. Marsh & Partners (LON:BPM), and I have now added it to my portfolio (again - I have held it before). For my latest writeup of the stock, see here: BP Marsh - Profiting from an unglamorous but lucrative niche.

We are trying to make stock pitches a more regular feature, which is possible if we keep them snappy and to-the-point. So any feedback you might have on their format is very welcome - cheers!

Today's report is complete. There was very little to report on today, but I did provide a backlog section on Netcall in response to a reader request. I'll look forward to seeing you on Monday, which should be much more exciting! Cheers.

Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

IMI (LON:IMI) (£6.8bn | SR64) | Organic revenue growth 5%, adjusted basic EPS +8% (132.3p). ROIC up 60 basis points to 14%. £500m share buyback. 2026 outlook: “we expect full year adjusted basic EPS to be between 136p and 142p, representing our sixth consecutive year of mid-single digit organic revenue growth." | ||

Avon Technologies (LON:AVON) (£545m | SR46) | Avon Protection has received a new order for 'MILCF50' CBRN filters from a Middle Eastern customer. The order is worth approximately $12.7 million and “further underpins the Group's expectations for FY2026, in line with the guidance provided at the full year results in November 2025”. | ||

Hargreaves Services (LON:HSP) (£254m | SR99) | Exchange of contracts for the unconditional sale of the second tranche of the renewable energy land portfolio. Gross cash consideration £6.8m. | ||

Amedeo Air Four Plus (LON:AA4) (£143m | SR57) | Under the agreed terms, AA4+ Shareholders will be entitled to receive 73 pence in cash per AA4+ Share. 33% premium to yesterday’s close. | PINK (Graham) | |

Proservice Building Services Marketplace (LON:PRO) (£58m | SR39) (formerly HSS Hire) | The new CFO has been with PRO since 2018. | ||

Helix Exploration (LON:HEX) (£56m | SR14) | Helix has expanded its strategic footprint at the Rudyard Helium Project in northern Montana to nearly 8,000 acres. Has acquired additional State of Montana mineral leases at public auction. | ||

Blencowe Resources (LON:BRES) (£51m | SR16) | A maiden JORC (2012) Mineral Resource Estimate Statement for the recently discovered Iyan deposit, part of the Company's 100% owned Orom-Cross Graphite Project in Uganda, has been completed. Confirms Iyan as a high-tonnage, near-surface extension of the wider Northern Syncline graphite system. | ||

Various Eateries (LON:VARE) (£24m | SR72) | Has agreed to acquire a portfolio of premium pubs with rooms: four sites, with a further agreement to potentially acquire a fifth site. These sites will be known collectively as The Linwood Collection. Price for the first four sites: £11.25m. There is also a proposed name change for Various Eateries: Coppa Collective plc. If agreed, the stock ticker will change to COPC. | AMBER/RED ↓ (Graham) [no section below] This is a very large acquisition relative to the current size of Hugh Osmond’s Various Eateries. It previously had 20 locations and an £8m cash balance (see our coverage of the full-year trading update), although the net cash balance was more modest at £4.6m (and this is before mentioning £25m of lease liabilities). This acquisition of at least four very expensive properties does thankfully include the freeholds, which will serve to minimise the risk. On the other hand, it will wipe out the company’s net cash balance and leave it reliant on new debt facilities with HSBC. All of which would be fine were it not for the fact that the company has heretofore been allergic to making real profits. Zeus recently upgraded their FY26 forecasts, but the company is nevertheless expected to remain loss-making until at least FY27. I was previously neutral on this stock, but that was predicated on its cash position. As such, I think that a modest downgrade is now in order. |

Graham's Section

Amedeo Air Four Plus (LON:AA4)

Up 29% at 70.8p (£184m) - Recommended Cash Acquisition - Graham - PINK

Takeover news has been a little quiet recently, and much quieter than it was during the small-cap bear market.

The FTSE All-Share Index 3-year chart shows how sentiment towards UK stocks has turned:

And the FTSE Smallcap Index shows how small-caps have participated strongly in the rally:

Incidentally, the red square in the chart above shows when Ed published his article “The AIM Market is at its most oversold since the Global Financial Crisis - an opportunity for the brave” (link).

Given how small-caps have performed since then, that appears to have been a rather prescient take - and I think we were all pretty excited about the value on offer back then.

However, I should acknowledge that the AIM Index itself has not performed so well:

The poor performance of AIM is typically due to the quirks of how it’s composed, with two main reasons: 1) heavy concentration at the top, where mid-sized and large companies crowd out the performance of hundreds of micro-caps; and 2) the presence of many poor-quality and blue-sky companies (the majority of which we don’t cover in this report) is a permanent drag on performance.

Personally, I no longer use the AIM All-Share Index as a benchmark for anything. If I want to measure small-caps, I’ll look at the FTSE Smallcap Index. If I want to look at mid-caps, I’ll look at the FTSE 250. It’s true that they are much more challenging benchmarks, but I would never be satisfied to earn the returns generated by AIM over the long-term, so AIM is simply not relevant.

Amedeo Air Four Plus Limited - recommended cash acquisition

Let’s get back on topic, and check out the latest takeover.

AA4 is a main-market listed, Guernsey-based company. Its objective: “to obtain income returns and a capital return for its shareholders by acquiring, leasing and then selling aircraft.”

It’s a stock that we covered only very rarely, which I would say is due to the fact that it is technically a fund, not an operating business.

Roland did cover it in December. He took a neutral stance, sensibly arguing that sector expertise was needed to understand the potential outcomes when AA4’s A380 aircraft come off lease to Emirates this year.

Some of the key points around this recommended takeover:

Takeover price: 73p per share.

Premium: 33% vs. last night’s close.

The buyer: Lesha Bank, “a financial institution based in Qatar and listed on the Qatar Stock Exchange with a market capitalisation of approximately QAR 1.9 billion” (£400m).

Lesha Bank has a division that can manage this sort of business:

The Lesha Aviation Capital division of Lesha Bank… is a global aviation leasing and investment platform and operates as a full-service platform providing investment management capabilities to global aviation investors. The platform focuses on resilient asset-backed investments across the aviation sector.

Rationale

AA4 management argues in favour of the deal on the grounds of the 33% premium, the immediate liquidity and certainty it provides, and (quoting this part extensively as it is key, and emphasis added):

The Acquisition has reduced execution risk relative to alternative strategic outcomes.

Through a detailed, comprehensive and extended strategic review process, the AA4+ Board has assessed a broad range of options for the Company, including asset disposals and other strategic transactions. The AA4+ Board has noted a number of factors which contribute to a material uncertainty in the level of value that could be delivered to AA4+ Shareholders…

certain of the leases held by AA4+ are approaching maturity;

the nature of the aircraft owned by AA4+ and the limited range of options to realise capital value on the disposal of the assets; and

the cyclical nature of the global aviation industry, the potential for extended down cycle periods, and, given the nature of the Company as a closed-end investment fund, the ability to manage through such parts of the aviation cycle.

In this context, the Acquisition is expected to deliver greater risk-adjusted value to AA4+ Shareholders than other options considered by the AA4+ Board.

Shareholder support: there are “irrevocable undertakings” and letters of support for the takeover from shareholders owning 19.5% of the company, which is a good start to get it over the line (although it is still not guaranteed of course).

Two of the top three shareholders already support the deal, excluding Royal London, and I’d be a little surprised if Royal London attempted to block it:

Graham’s view

There are two elephants in the room.

Firstly, there is the war in the Middle East, which has caused 11,000 grounded flights according to a recent count. The AA4 share price has been reacting to this over the past week:

In the context of that war, almost anything that can relieve the company and its shareholders of major uncertainty might be seen as a welcome development.

But the second elephant in the room is the company’s official net asset value. A persistent discount to NAV had seen AA4 management searching for strategic options in recent years: management clearly hoped to narrow this discount. This deal, while perhaps offering the best outcome in the circumstances, does abandon that ambition. NAV per share at September 2025 was 107.39p.

Two things can be true: Lesha Bank might be getting a great deal, buying aircraft on the cheap and at a big discount to their normal value. But at the same time, this might be the best outcome for UK-based shareholders who lack the local expertise and connections of a Qatari bank.

I’m therefore inclined to give this proposed takeover my personal endorsement. AA4 was already a risky investment before the conflict broke out in the Middle East. AA4’s management have today explicitly endorsed the reasons given by Roland for caution a few months ago, before missiles were fired.

Throw in a major international conflict in the Middle East causing thousands of cancelled flights, and this stock becomes far riskier than I’d personally be willing to tolerate. In that context, accepting a 30%+ discount to NAV becomes an unfortunate but perhaps the most logical option. Sometimes it's not possible to achieve NAV, and this strikes me as one of those instances.

Netcall (LON:NET) (Backlog stock)

Up 3% to 100p (£170m) - Half-Year Report - Graham - AMBER =

Netcall plc (AIM: NET), an enterprise software company that unites automation and customer engagement in one AI-powered platform, today announces its unaudited results for the six-month period ended 31 December 2025.

Although the Netcall share price is up today, it’s got nothing to do with these results, which were published on Wednesday .

We don’t cover Netcall very often: the last time was in March 2025, when I was neutral. I seemed to like the company, but the valuation seemed rather “hot” to me.

Over the past year, the market cap has cooled from £190m then, to £170m today.

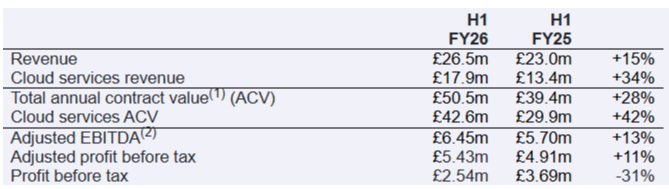

These latest results show slower top-line growth rates than we saw in the corresponding report a year ago, with acquisitions having played an important role both this year and last year.

The company would of course point to the fast growth in various “annual contract value” measures. For example, £50.5m of total ACV refers to “the total of the value of each cloud and support contract divided by the total number of years of the contract”.

That’s a perfectly good KPI and if investors wish to focus on that, I have no problem with it.

To keep things simple, my main port of call would be the revenue forecasts for the next few years.

The researchers at Edison published on Netcall this week (many thanks to them) and they provided the following forecasts:

FY June 2026 revenue £57.6m, PBT £9.8m.

FY June 2027 revenue £67.2m, PBT £12m.

Singers published on the stock too, with very similar (in fact slightly more bullish) numbers, and reiterated their growth forecasts.

In revenue terms, therefore, the market is expecting growth of about 20% this year, and then further growth of about 17% next year.

Regardless of what happens with ACV, these are the headline growth figures I would be inclined to focus on, as they are simpler and more difficult to adjust.

Organic rates: all of the above growth rates are based on performance including various acquisitions. In last year’s interim report, the company said that organic growth was at “double-digits” (i.e. more than 10%). In this year’s interim report, they are more specific, saying that organic growth was 11%. In the most recent annual report, it was observed at 10%. So this is the real, underlying growth rate in my book.

Operating leverage? The adjusted pre-tax profit margin, having been 17% last year, is seen remaining stable in the current year and perhaps improving to 18% next year. So there is no major increase in profitability expected in the short-term.

Recurring revenue: this has increased from 79% in H1 last year to 83% in H1 this year. I said last year that seeing this approach 100% would help me to take a more constructive position on the stock.

Net cash/balance sheet

Net cash is £15m, down from £22m a year ago, with £13m having been spent on acquisition-related payments since then.

I should also point out that there are contract liabilities of £28m, meaning that customers have paid upfront for Netcall’s services. So the cash on Netcall’s balance sheet does come with certain strings attached.

Also, and this will be largely due to its acquisition activity, Netcall’s balance sheet remains in negative tangible equity. The total net asset figure of £48m includes nearly £70m of intangibles. This is not really a problem, but it does mean that there isn’t all that much balance sheet support for the stock to fall back on.

CEO comment

We delivered a strong first half, with double‑digit revenue growth, improved profitability and clear progress across our key metrics. Cloud momentum remained a key driver, lifting Cloud ACV by 42% year‑on‑year and increasing recurring revenue to 83% of the total, enhancing revenue quality and visibility.

"Customer adoption of the Liberty platform continued to deepen, reflected in consistently strong Cloud net retention. Adoption of AI capabilities accelerated across agent‑assist, voice automation and self‑service, contributing to higher customer value as organisations expand their use of Liberty…

"We enter the second half with positive momentum, a strong pipeline and a record contracted order book, and the Board remains confident in delivering ongoing progress in FY26."

Liberty is the flagship solution at Netcall. It’s an “AI-powered contact centre solution that helps you deliver faster, more personal service… It connects teams and systems to streamline journeys, reduce costs and improve customer experience across every touchpoint.” For more, see here.

Outlook: we know that forecasts have been reiterated, which is the most important thing, but here’s what the company said in the half-year report.

Trading momentum has continued into the second half, supported by demand for Netcall's cloud‑based automation and AI solutions across core public and private sectors. Building on the 42% year-on-year increase in Cloud ACV in the first half, the ongoing shift towards Cloud subscriptions and broader adoption of Liberty modules, including AI, are expected to remain key drivers of ACV growth and increasing revenue visibility.

Adjustments

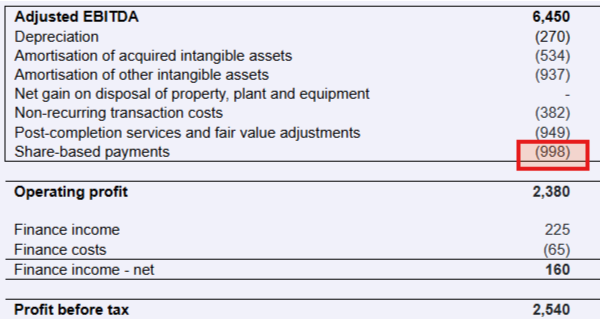

There are significant adjustments to be aware of. Compared to adjusted PBT of £5.4m in H1 this year and £4.9m in H1 last year, the actual PBT results were £2.5m and £3.7m, respectively.

I would draw your attention in particular to £1m of share-based payments in H1 this year. That’s a large percentage of profits lost to employee compensation.

In the US, Nvidia shocked the market this week when it stopped adjusting stock-based compensation out of its results. Hopefully this will be the start of a trend in which more companies start to acknowledge the real cost of SBPs.

The other adjustments are largely to do with acquisition activity and I have no major objection to adjusting them out, but for now they do mean that Netcall’s results are not what I’d consider clean.

Graham’s view

I was AMBER on this last year and am again drawn to a neutral position here.

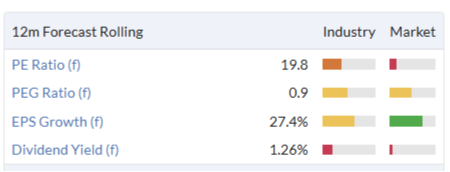

As before, it continues to appear expensive:

I have no problem with expensive software companies that can tick various boxes on my checklist. For example, ideally we’d have as many of these as possible (the list is not exhaustive, just a few things that come to mind):

High organic growth

High recurring revenues

Powerful competitive positioning

Strong balance sheets

Clean financial results

As you can see, Netcall is hit-and-miss when it comes to this sort of checklist.

The competitive positioning is the most difficult to assess, but I’m inclined to think it’s decent based on operational metrics such as net retention of 115% in Cloud-based services - this indicates a high degree of customer satisfaction.

Recurring revenue at 83% is good, and moving in the right direction.

Overall, however, I don’t think I can move away from a neutral stance on this yet. A real underlying organic growth rate of 10% is perfectly good but the market is already pricing this generously, in my book, with a P/E multiple of 20x and a PEG ratio of less than 1x.

So in summary: I still like the business, and the stock, but I think a neutral stance remains fair on valuation grounds

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.