Good morning! We have some backlog sections from Mark to start us off today.

13:30: all done for the week, have a nice weekend!

Spreadsheet accompanying this report (last updated to: 23rd Jan 2025)

UK Rate Cut

The big economic news this week has been the reduction in interest rates from 4.75% to 4.5%, the third rate cut in six months, accompanied by dovish sentiment at the Bank of England where some members believed that an even bigger cut was in order.

Governor Andrew Bailey describes the cut as “good news” - the plight of borrowers is always of slightly greater concern than the needs of savers!

However, inflation is still above the 2% target. It only very briefly fell below it in September:

This is before the impact of higher NICs, which many predict will lead to a rise in consumer prices as businesses are forced to pass on higher costs to customers.

The Bank of England itself says that it expects inflation to rise to 3.7% this year, before falling again.

So with inflation already slightly higher than the Bank’s 2% target, and expected to rise further from here, it’s a brave move to pre-emptively cut rates. After all, the Bank’s primary mandate is price stability, and other objectives are supposed to be secondary. But they say there has been “sufficient progress” when it comes to reducing inflation, to allow them to cut rates - and there has indeed been remarkable progress on that front.

On the subject of price stability, the Bank is of the view that energy and utility prices will be the main driver of inflation in the short-term, and that “underlying domestic inflationary pressures are expected to wane further”. I hope they are right, but I’m concerned that the incoming tax changes could upend that prediction.

In the Bank’s defence, it is only a 0.25% cut, and they say they will be “careful” with next steps, not committing to further cuts.

All of this was expected. However, the news that caught the market by surprise yesterday was the discovery that two members of the Monetary Policy Committee wanted to take a more radical step and to cut Bank Rate by 0.5%.

For these members, and perhaps for the committee as a whole, they now feel that the Bank must pay more attention to GDP growth and economic activity. There is an argument that weaker activity and a slightly looser labour market can in themselves fuel inflation. But at the same time, the Bank has said that the labour market is “in balance” overall, and that there is only “a small margin of slack”.

And if the economy is already producing close to its maximum capacity, there is a limit to what rate cuts can do to boost economic activity,

Even with the economy operating close to its maximum potential, GDP fell by 0.1% in 2024 Q4 and is only expected to rise by 0.1% in 2025 Q1, barely avoiding an official recession. Low productivity was singled out as the reason for this.

NICs: the bank is monitoring the NIC issue. It says that according to economic literature, “more of the adjustment is likely to come through real wages or employment than profits”, i.e. that employees are likely to bear the brunt of the cost, either through lower salaries or fewer job opportunities.

They say that labour costs are increasing by over 5% for the bottom 50% of earners, and that the elasticity of demand is higher for lower skilled workers. In other words, employers are most flexible when it comes to the number of lower skilled workers they employ. This means that these workers are the most vulnerable to changes in demand for their services, arising from higher NICs.

Here are the Bank’s conclusions:

Survey evidence and Bank staff analysis since the November Report continues to support the judgement that firms are likely to use a number of different margins in response to the change in NICs… The increase in NICs is expected to have a marginally larger impact on prices in the near term than at the time of the November Report.

…employment may be more affected than in the central assessment in the forecast. There remain considerable uncertainties around how firms will respond, however, which the Committee will continue to monitor.

And yet the Bank has set out on a rate-cutting path, despite all of the uncertainty around this issue and with price rises looming.

What this means for investors: markets are now pricing in another 50 basis points of rate cuts in 2025. I don’t see anything to get in the way of the FTSE-100 making new all-time highs this year. For homebuilders, mortgage lenders and construction companies, they can look forward to slightly easier conditions than they may have been expecting. But for importers, watch out below:

(GBPUSD)

Today's news: this afternoon, we'll have non-farm payrolls data from the United States, with a further 169,000 jobs expected and an unemployment rate of 4.1%.

Agenda

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Legal & General (LON:LGEN) (£14.8bn) | Sale of US Protection | Buyer also takes 20% interest in US Pension Risk Transfer, strategic partnership. Combined value £1.8bn | AMBER (Graham) An excellent deal that will keep L&G shareholders in clover for the next few years. No opinion on the stock due to complexity. |

Ashmore (LON:ASHM) (£1.1bn) | Half-Year Report | AUM $48.8bn, “broadly unchanged”. Net outflows improve to $1.1bn. | GREEN (Graham) The balance sheet remains very attractive. Watch out for a dividend cut if earnings remain under pressure. |

Victrex (LON:VCT) (£866m) | AGM & TU | Full year expectations unchanged. “Solid start”. Q1 revenue +9%, volume +20%. | |

| Vertu Motors (LON:VTU) (£174m) | TU (yesterday afternoon) | Profit warning. Adj. PBT significantly below exps. Dislocation in new car market. | AMBER/GREEN (Graham) Quantitatively "cheap" for those who can look past the industry issues. |

Ingenta (LON:ING) (£10m) | TU | 2024 revenues (£10.2m), EBITDA (£1.8m) in line. Sales/marketing spending to reduce 2025 EBITDA. |

Backlog

AstraZeneca (LON:AZN)

Up 5% yesterday to 11,650p (£221bn) - Final Results - Mark - AMBER

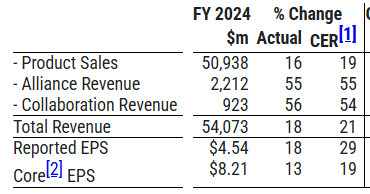

When I previewed the results in The Week Ahead, I said that the company had shown rapid growth in EPS over the last few years, but with the 2025 P/E of 15 and a forward PEG above 1, investors will be looking for signs that these forecasts are conservative. The consensus was for $53.1b of revenue and 815c of EPS. Here’s what they came in as:

So that’s a very slight beat on revenue and EPS. However, it is worth noting that the beat would have been much bigger if they hadn’t faced currency headwinds during the year. These moves are largely unpredictable, so it is understandable that they provide their guidance at constant currency:

Guidance for FY 2025: Total Revenue is expected to increase by a high single-digit percentage and Core EPS is expected to increase by a low double-digit percentage, both at CER

So it seems that growth is expected to moderate but still be at reasonable levels. Putting these figures into my calculator, it looks like the implication is for a likely beat to the $56.6b revenue forecast, but with Core EPS in line. If this is the case, the PEG remains above 1:

Mark’s view

I don’t see the attraction here. When Megan looked at this following the announcement of an escalating insurance fraud investigation in China, she noted that the PEG ratio was below one and hence rated it GREEN. That is no longer the case based on current guidance, so it is an AMBER for me.

Ra International (LON:RAI)

Down 86% yesterday to 0.9p (£1m) - Delisting - Mark - RED

This provider of construction and IFM services to governments and NGO’s in difficult places just scrapes into our £10m lower market cap limit. At least it did until the shares fell almost 90% today on the news that it is delisting:

As announced today, the Directors have, after a period of review, concluded that it is in the best interests of the Company and its Shareholders to seek Shareholder approval for Cancellation of the admission of the Ordinary Shares to trading on AIM.

This is always a risk in a stock where founders own 80% of the shares. It is an ignominious end to a company that listed with strong growth plans. The problem was that growth in their industry is capital-intensive. When they raised cash on listing, management didn’t cash out but held on to a high proportion of the company. They presumably saw the business growing and thought they would be able to raise further capital while diluting down their stake. The growth failed to materialise, though:

COVID delays hit profitability:

And while they generated much higher gross margins of around 20% by operating where others wouldn’t, there was a reason that others didn’t operate there. An insurgency in Cabo Delgado in Mozambique highlighted this risk, and led to further losses, including the death of an employee. At this point, the share price presumably seemed too low to raise more money without severely diluting management, so they limped on, restricted in their ability to grow out of their predicament by their lack of capital.

Today, this comes back to bite them, as along with the delisting announcement, they issue an update on trading:

For the year ended 2024 and based on unaudited management accounts, we expect to report a marginal year on year revenue increase compared with 2023. Despite this, a (pre exceptionals) loss is projected at Operating and EBITDA level primarily as a result of delayed contract commencements and mobilisation issues, which have already adversely impacted our invoicing schedule.

To strengthen our financial position, we will be initiating several cost reduction measures in 2025, including the potential divestment and closure of certain subsidiaries, in particular those that are loss making. These actions aim to maintain operational efficiency, preserve cash, and sharpen our focus on strategic contracts and key client relationships.

There is the potential for divestments to keep the show on the road, but ultimately, they say:

However, any positive impact the potential divestments may have on the Company's cashflow and profitability is expected to be offset by the reduction in revenues and resulting margins from ongoing delays in mobilisation and decreased scope of a number of key contracts.

The management here always prided themselves in doing the right thing, and I genuinely believe they aimed to do so in the past. This makes it galling that despite owning 80% of the equity, they are not making any tender offer to allow minority holders to exit at a reasonable level. The non-execs have allowed the founders to vote their shares which, with 80%, means that this is a done deal. The reality seems to be that the cost saving of delisting is now vital, and the founders don’t have the money and no one is willing to lend it to them, given where the business has ended up.

Mark’s view

The trading update highlights the risks and suggests that even those who can hold unlisted equity shouldn’t be holding on here. The 90% fall in share price looks justified. RED

Anglo American (LON:AAL)

Up 6% yesterday to 2440p (£33bn) - Q4 Production Report - Mark - AMBER

Anglo American rose yesterday on marginally better than expected Q4 copper production, which is up 9% on the previous quarter. They guide 2025 copper production at 690 Kt-750 kt, slightly below 2024 production of 773 kt, and 760 kt-820 kt in 2026. However, they have reduced their forecast for rough diamond production due to lower demand from the market.

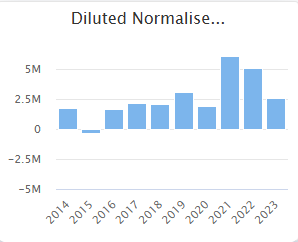

There is a theory that you should buy miners on a high P/E and sell on a low P/E as they are cyclical stocks, and by doing so, you are acting countercyclically. However, I see little sign of this in AngloAmerican’s long term EPS figures:

It seems to me that current forecasts are about normal for the company, and 2021/2022 were the anomoly:

And the broker trend isn’t particularly encouraging:

This makes paying these sorts of multiples for flat production look out of place:

Mark’s view

It is hard to get excited about flat production forecasts and declining broker forecasts, especially at these sorts of multiples. AMBER.

Graham's Section

Vertu Motors (LON:VTU)

Down 7% yesterday, latest price 52.4p (£174m) - Trading Statement - Graham - AMBER/GREEN

One of the few things that is virtually guaranteed to annoy investors is the release of market-moving news in the middle of the day.

Normally, we get just an hour to digest a vast quantity of information, before the market opens. I’d prefer a system where news was released after-hours, enabling us to read at our leisure before the market opens the next day.

But then you have a situation like Vertu yesterday, where the news comes out at 2.30pm.

It’s a profit warning, with adj. PBT for FY Feb 2025 anticipated to be significantly below current market expectations.

The expectation was for adj. PBT of £34.5m.

The reason: “primarily due to dislocation in the new car market”.

Let’s pick out some of the key bullet points:

New cars: LfL volumes at VTU were ahead of market trends in the past five months, but the market trends are terrible as “UK volumes overall in the new retail channel were the lowest for 25 years including the pandemic period”.

Used: suffering from subdued consumer confidence and heavy discounting of new cars.

ZEV mandate: there is a 28% ZEV target for 2025, that “is likely to lead to further ongoing discounting activity in the new car market, continuing the margin pressure seen during the current year”. Volumes also under pressure.

Reading a little further into the ZEV issue, VTU notes that the industry failed to hit the government’s 22% ZEV target in 2024, but attempts to hit these targets are affecting the industry. The current weakness in higher-margin private channel sales (as opposed to low-margin fleet sales) reflects “consumer hesitation toward BEVs, affordability issues and more limited availability of petrol and diesel vehicles as Manufacturers prioritised compliance with percentage targets of the ZEV mandate.”

As things stand for 2025, “the increased target is likely to lead to continued pressure on new car volumes and margins as the market is increasingly distorted in favour of BEVs.”

Aftersales are still doing fine, and £10m of cost increases arising from NICs/NMW will be “fully offset” by headcount reductions, increased use of technology, and Sunday closures.

Buyback: one of the main attractions at Vertu has been the strong balance sheet that has enabled large buybacks.

Checking the most recent interim report, I see tangible net assets per share reported at 73.7p. From the balance sheet I calculate the corresponding value as £232m. The company has made a small-ish (£12.5m) acquisition since then.

That level of asset backing gives the company the confidence to plough money into buybacks and the company softened the blow of yesterday’s profit warning by announcing an additional £12m to the ongoing buyback programme. £4m has been spent already on buybacks in FY25.

They are confident they they are buying below fair value:

The Board determined that Vertu Motors plc shares are mispriced and trading at a material discount to our own assessment of intrinsic value.

Please note that a high level of asset backing is not the same thing as saying that the company has a net cash position: it had net debt at the interim results of £175m (includes £91m of leases, so the figure is £84m excluding leases). Without the use of vehicle stocking loans to help fund inventories, most car dealers would be unable to earn an acceptable ROE: VTU’s inventories are a staggering c. £800m.

CEO comment snippets:

…the Government's ZEV Mandate is causing severe disruption to the UK new car market, and the consumer environment is subdued. Despite these headwinds, the Vertu team is delivering, as seen by our significant market share gains in BEV new cars in the final quarter of the year….

Vertu's strong balance sheet, underpinned by over £320m of freehold and long leasehold property, is a comfort to our colleagues, Manufacturer partners and shareholders in these times.

Estimates: the new adj. PBT estimates at Progressive are £29.6m (FY Feb 2025) and £26.5m (FY Feb 2026).

Graham’s view

I’m inclined to leave this at AMBER/GREEN because VTU offers: a) a reasonable single-digit PER, b) a discount to tangible NAV, c) a declining share count, and d) profitability (albeit at a lower level) even in terrible market conditions.

What are the downsides? Very limited organic growth prospects. And probably a lot more market disruption to come, until/unless ZEV mandates are relaxed. If that happened, then I imagine that VTU shares would soar. But if most of the pain seems to be falling on dealers rather than consumers, perhaps that’s not very likely.

Ashmore (LON:ASHM)

Up 2% to 174.4p (£1.2bn / $1.5bn) - Half-Year Report - Graham - GREEN

This emerging markets fund manager has achieved nothing for its shareholders for many years when it comes to share price appreciation, but it has paid out enormous dividends. The yield is almost 10% currently.

Today’s interim results are consistent with a share price in a state of long-term malaise:

Continued net outflows ($1.1bn) which are described as a “significant reduction in redemptions”.

AuM almost stable at c. $49bn, helped by positive market performance. However, average AUM was lower than before, which puts downward pressure on fees.

Net management fees are down 17%, with performance fees (a separate category) stable.

I’ve been positive on this stock despite underwhelming progress because of its ability to churn out profits in all conditions. For H1, it reports an adj. EBITDA margin of 42%, not much lower than last year’s 46%.

Overall profits do decline, with adj. PBT falling from GBP £54m in H1 last year, to GBP £44m in H1 this year.

Equities: ASHM is traditionally a debt investor but equities AUM have grown to $7bn (a year ago: $6.5bn) and are now 14% of total AUM ($48.8bn).

Macro outlook: I no longer pay too much heed to commentary from ASHM on the macro outlook as, while interesting, it never seems to have any bearing on their inflows/outflows.

Additionally, for as long as I can remember, ASHM has been saying that investors are underweight EM and in need of rebalancing into it.

I guess it’s not really possible for them to say anything else, as the whole point of the business is to convince allocators to put money into emerging markets:

Robust fundamentals, resilience and reforms evident across emerging markets, delivering superior economic growth.

Meaningful upside to asset prices in EM if US policy implementation is more measured than campaign rhetoric.

Significant rebalancing required to address investors' cyclically low EM allocations and to capture the potential upside to asset prices.

Graham’s view

Perhaps I should downgrade this to AMBER/GREEN as it’s seriously lacking in growth. However that is true of most fund managers I cover in this report, and I’m GREEN on most of them.

Turning to the Dec 2024 balance sheet, I see total equity of GBP £818m, backing up a very large portion of the market cap.

Nearly all of this value is tangible (only £88m of intangible assets), and a large part is in the form of investments that are capable of growing in value. ASHM has nearly GBP £350m of seed capital in its own funds. In total it has excess capital of GBP £550m, over and above its regulatory requirements.

All of that seed capital does serve an important operational purpose in relation to ASHM’s funds but it’s also a meaningful part of the balance sheet and the overall package that shareholders are buying into here.

There are also cash, cash equivalents and term deposits of nearly £350m.

When it comes to shareholder income, the interim dividend is unchanged at 4.8p, matching H1 adjusted earnings per share of 4.8p. The final dividend is usually 12.1p, and H2 EPS is not going to be able to fund that.

I’m going to stay positive on this with the warning that the dividend is not supported by earnings, and so a dividend cut should not come as a surprise, if it happens. I think the company can afford to continue making the payment using its balance sheet, if it so chooses, but I would not expect it to do so perpetually.

So if you’re comfortable with that situation, I still think ASHM is worth another look. If or when we see US equity valuations falter, perhaps ASHM can benefit from renewed interest in EM? Especially now that it can offer EM equity exposure.

Legal & General (LON:LGEN)

Up 3% to £2.47 (£14.5bn) - Sale of US Protection; new Strategic Partnership - Graham - AMBER

This is a short RNS considering that there is nearly £2bn at stake.

L&G is selling its US insurance business to the Japanese life insurer, Meiji Yasuda, for an equity value of $2.3bn (£1.8bn).

As part of the deal, Meiji is taking a 20% interest in L&G’s US pension risk transfer business.

Finally, Meiji intends to take a 5% interest in the overall L&G Group.

In the short-term this will allow an additional £1bn buyback for L&G, while still increasing L&G solvency ratios.

In total, L&G “expects to return the equivalent of c. 40% of its market cap to shareholders over 2025-2027 through a combination of dividends and buybacks.”

Trading update: guidance unchanged.

The company reiterates guidance for FY Dec 2024 and its plans out to 2027:

6-9% CAGR in core operating EPS (2024-27)

>20% operating Return on Equity (2025, 2026, 2027);

£5-6bn cumulative Solvency II capital generation over three years (2025-2027).

CEO comment:

"This is a transformative transaction that brings significant strategic and financial benefits to the Group and demonstrates our commitment to deliver on our strategy - sharpening our focus on core businesses, leveraging the synergies between them, and driving sustainable growth to enhance shareholder returns.

This strategic partnership brings together two highly complementary global businesses, with a shared ambition for growth, and will enable us to capitalise on the large market opportunities in US Pension Risk Transfer while driving scale and profitability in global asset management…

Graham’s view

This appears to be a good deal for L&G when we consider the disclosed summary financial information for the US protection business they are selling: operating profits of c. $90m in 2024, with net assets of $850m. In selling this for $2.3bn, they’ll record an accounting gain of over GBP £1bn. Tick, tick, tick - they’ve achieved a very nice valuation based on these numbers.

The growth in their capital base that this will allow will help them on their way to achieving their 3-year targets out to 2027. But they will be lucky if they can find more deals like this in the next two years, so it might be less straightforward to stay on track as we approach 2026 and 2027.

I’m neutral on this stock as it’s too large and complex, and this is just a short review. But I expect that it will probably continue to do its job of paying out vast sums to shareholders, without ever generating very much capital growth.

10-year chart:

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.