Good morning!

It's another positive set of announcements with lots of updates but possibly no profit warnings, with everything either in line or ahead of expectations. This happened several times last week, too. [EDIT: we also have another takeover offer!]

Could it be that economic worries, for the time being at least, have been fully priced into consensus forecasts for most companies?

I doubt this will last come April and the planned tax increases, but let's enjoy it while it lasts!

With the markets we cover arguably offering both a) historically cheap valuations, and b) forecasts that almost all companies are now able to meet or beat, surely the outlook for overall performance can't be bad!

11.30am: wrapping it up there for now, thank you.

Spreadsheet accompanying this report (updated to 17/1/2025)

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Johnson Matthey (LON:JMAT) (£2.3bn) | Strategy update | Maintaining focus on PGM, scaling back hydrogen tech, committee to consider capital allocation. | |

WH Smith (LON:SMWH) (£1.5bn) | Response to press speculation | Confirms w/end press reports that the company is exploring options to sell its High Street business. | AMBER/GREEN (Graham) A positive announcement as this is primarily a travel business now. |

Dr Martens (LON:DOCS) (£704m) | Q3 TU | Q3 trading was as expected and FY25 outlook is unchanged. Q3 revenue +3% at constant FX. | AMBER/RED (Graham) Upgrading this as a recovery now seems more achievable although debt and inventories may remain challenging. |

Volex (LON:VLX) (£521m) | TU | 9M revenue up 21.8% to $789m, inc 9.6% org growth. FY profit exps remain in line with forecasts. | GREEN (Roland) |

Pensionbee (LON:PBEE) (£373m) | AUM update | AUA has reached “over £6 billion” representing >265k customers. | |

Costain (LON:COST) (£231m) | TU | FY24 in line (adj. op profit £41.9 - 43.4m, net cash £160m. “Forward work” rises by £1.5bn to £5.4bn. | GREEN (Graham) Very impressive growth in the forward work position. If they execute this at expected margins then shareholders should do well. |

Stelrad (LON:SRAD) (£180m) | TU | 2024 revenue -6% to £290m, but adj op profit marginally ahead of exps at c.£31.5m. | AMBER/GREEN (Roland) |

Genel Energy (LON:GENL) (£175m) | Trading & Operations update | FY24 free cash flow of $19m and net cash $131m. FY25 cash gen expected to cover org costs. | |

Concurrent Technologies (LON:CNC) (£152m) | £3.4m contract award | “Significant order” for VME-based 6u boards from existing European customer, delivered 2025-27. | |

Good Energy (LON:GOOD) (£73m) | Recommended cash takeover at 490p | Cash offer at 24% premium to Friday’s close. Buyer is energy transition tech group Esyasoft. | PINK (Roland) |

Synectics (LON:SNX) (£57m) | $2.2m contract award | Synergy upgrade and expansion at a major gaming resort in SE Asia, delivery in current financial year. | |

PCI- PAL (LON:PCIP) (£51m) | TU | H1 revenue up 26% (up 13% normalised) and in line. ARR up 21% year-on-year to £16.8m. | |

Renalytix (LON:RENX) (£37m) | TU | On track to deliver expectations for FY26 and FY26, which assume average 20% quarterly growth. | |

Lendinvest (LON:LINV) (£33m) | FUM update | FUM crosses over $5bn, after a series of major funding uplifts. | |

Brave Bison (LON:BBSN) (£28m) | TU | FY24 adj. PBT £3.9m ahead of exps (£3.7m). Board “remains comfortable” with FY25 forecasts. | |

Fadel Partners (LON:FADL) (£13m) | FY24 TU& FY25 outlook | FY24 rev/LBITDA in line? Net cash $2.4m ahead of exps. O/look: big improvement in LBITDA. |

Graham's Section

WH Smith (LON:SMWH)

£11.48 (pre-market) (£1.49bn) - Response to press speculation - Graham - AMBER/GREEN

A brief acknowledgement from WH Smith:

WH Smith PLC ("WHSmith", or the "Group") notes the recent press speculation regarding its High Street business.

WHSmith confirms that it is exploring potential strategic options for this profitable and cash generative part of the Group, including a possible sale.

Over the past decade, WHSmith has become a focused global travel retailer. The Group's Travel business has over 1,200 stores across 32 countries, and three-quarters of the Group's revenue and 85% of its trading profit comes from the Travel business.

Sky News had the scoop, revealing on Saturday that the company was in secret (not for long!) talks to sell its entire high street business. According to Sky, SMWH “has been in negotiations with a number of prospective buyers for several weeks”.

Graham’s view: I’ve always had a fairly positive impression of SMWH and I think that the disposal of its High Street business could only improve its quality. I expect that most investors would share this view, as High Street competition is considered to be intense while airport competition is much less so.

Checking the most recent annual results, I see that most of SMWH’s official “debt” is the the form of leases; debt excluding leases is a more modest £370m, which looks manageable against adj. PBT of £166m.

In any case, a sale of the High Street business could be expected to wipe out that debt.

I’ll take an AMBER/GREEN stance on this as I see today’s announcement as positive news from a stock I’ve always liked. Valuation is not outrageous:

Costain (LON:COST)

Up 6% to 90.9p (£244m) - Trading Update with Strong Forward Work Position - Graham - GREEN

A nice full-year update from this contractor:

Trading for FY 24 has been positive with Group adjusted operating profit expected to be in line with market expectations and net cash at the end of the year in line with market consensus.

Consensus figures: adj. operating profit £41.9 - 43.3m, net cash £160m.

The stand-out figure provided is the £1.5bn year-on-year increase in the company’s “high-quality forward work position”, to £5.4bn.

This is not exactly the same thing as the order book. The definition:

Forward work is the total of order book and preferred bidder book which includes revenue from contracts which are partially or fully unsatisfied and probable revenue from Water and other frameworks included at allocated volume.

Including the “preferred bidder book” within this metric means including projects there is an increased risk of delay and possibly some uncertainty over the final price, as my understanding is that negotiations may not have been fully concluded. But these are projects where Costain has been selected and should get the job.

Having said that, £1.5bn is still a huge year-on-year increase. Annual revenues are only around £1.3bn, so more than an entire year’s worth of revenues have been added on.

Graham’s view

As we’ve said before, contractor businesses are problematic for investors due to the small and vulnerable profit margins they generate.

Costain today says that it has “increasing confidence in its ability to deliver further growth in operating profits and margins”, as it works towards its >5% operating margin target.

It is expected to generate a run-rate margin of 3.5% in FY24 and then a run-rate margin of 4.5% in FY25.

The most recent balance sheet was strong (net assets £230m, although this includes £48m of intangibles and a £55m pension surplus). It has been carrying out a £10m share buyback due to a strong cash position.

All things considered, I’m inclined to leave our GREEN stance unchanged. The shares are cheaply priced if you think the company is likely to make further progress on margins.

I also note a StockRank of 97.

Let me just emphasise that I don’t view any stock in this sector as offering much in terms of quality. But if I did have to invest in this sector I’d make sure I picked something that offered a strong balance sheet, a management team who placed great emphasis on improving and maintaining their profit margins, and a cheap earnings multiple.

COST offers all of these, so I’ll stay GREEN. Let’s hope that they stay disciplined as they execute the projects in their much-enlarged “forward work” position.

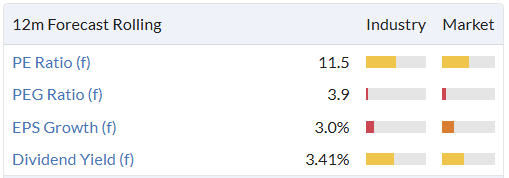

Dr Martens (LON:DOCS)

Down 3% to 70.4p (£679m) - Graham - Q3 FY25 Trading Statement - AMBER/RED

It’s an in line update from Dr. Martens that leaves the FY March 2025 guidance unchanged.

Headlines (everything is measured at constant FX rates except where mentioned otherwise):

Q3 revenue +3% to £267m (or down 3% at actual FX rates)

Wholesale revenue up 9%, but direct-to-consumer revenue only up 1%

Within direct-to-consumer, e-commerce grew 2% while retail revenue fell 1%.

Direct-to-consumer revenue grew very well in APAC (+17%). Americas was up 4% while Europe/Middle East/Africa fell by 5%, “impacted by the deep promotional nature of several markets, especially in December”.

Dr. Martens are currently running an end of season sale. Paul previously (e.g. here) flagged the company’s very high inventories as a problem; the company today says they are ON Semiconductor (NSQ:ON) track to meet our inventory reduction target for FY25@

Here’s a summary table. Q1 and Q2 were very poor year-on-year, but Q3 has greatly helped the year-to-date performance:

Estimates: this stock is covered by 7 brokers although none of them are currently posting research for this company on Research Tree.

Dr. Martens was supposed to be a much more influential stock, having originally achieved a valuation of £3.7bn at its IPO price (370p) and quickly racing higher to over 500p, before reversing.

It has now become one of the best examples of a 2021 IPO flop.

Consensus forecasts suggest revenue for this year (FY March 2025) of £818m and net profit of £28.8m.

Graham’s view: I’m happy to upgrade this to AMBER/RED on the basis that the company reduced its inventory by £69m (year-on-year) according to the interim results, published in November. Inventory fell from £314m (Sep 2023) to £245m (Sep 2024). With another season finished and an end-of-season sale, I’m expecting more progress on this front by the full-year results.

Net debt is also a concern with the company publishing a leverage multiple of 2.3x at the end of H1. The company did not provide an update on that in today’s announcement, but we can presume there is no change in the outlook there.

Overall, it’s not a pretty picture but the company did enjoy a period of bumper profits immediately before and after its IPO. To reflect the possibility that it achieves some form of recovery, I think I have to upgrade it today, although personally I would not yet be tempted to buy in.

Roland's Section

Good Energy (LON:GOOD)

395p (pre-market) (£73m) - Recommended Cash Acquisition - Roland - PINK (takeover)

This fast-growing energy supply and services group first disclosed takeover interest on 28 October 2024. Today we have the outcome – Good Energy has received a 490p per share cash offer from energy transition technology specialist Esyasoft Holding Limited.

This offer values the business at £99.4m and is being recommended by the board. It represents a 66% premium to the closing price on 25 October 2024 and a 24% premium to Friday’s close. I think it’s likely to proceed unless a competing buyer emerges.

The valuation represents a multiple of 18x 2024 forecast earnings and 11x 2025 forecast earnings.

The high multiple of 2024 earnings reflects its current dependence on profits from low-margin energy supply.

Good Energy is in the process of switching its strategy to focus on high-margin energy services, using an acquisitive approach. Services generated an operating loss of £2.2m in H1 2024, but the profit contribution from services is expected to outweigh energy supply in 2026.

Depending on your point of view, Esyasoft is paying a high price for the legacy business or a low price for the faster-growing but currently less profitable services business.

On balance, I think today’s offer looks reasonable, given the risks of the group’s acquisitive growth strategy and its current dependency on a slow-growing energy supply business.

While some shareholders may be disappointed, I think it’s worth remembering that this offer provides a guaranteed profit and removes the risk of disappointment if the services transition doesn’t go smoothly.

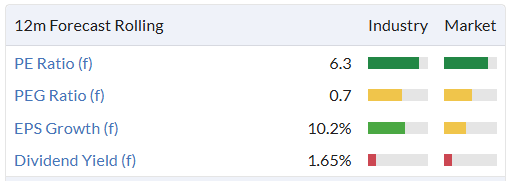

Volex (LON:VLX)

Up 0.5% 284p (£524m) - Trading Update - Roland - GREEN

Today’s trading update from this AIM-listed cabling specialist (“integrated manufacturer of critical power and data transmission products”) covers the 39 weeks ended 29 December 2024.

The Group's underlying operating profit expectations for the full year remain unchanged and are in line with market forecasts.

Trading summary: Volex says that revenue for the financial year to date rose by 21.8% to $789.4m. Within this, 9.6% was organic growth while 13.1% was contributed by acquisitions. Foreign exchange had “a small adverse impact”.

The company separates its business into five customer segments:

Electric Vehicles: demand is driving “significant organic growth”

Consumer Electricals: “continued to perform strongly”

Medical: softened slightly, normalising from a strong comparative last year

Complex Industrial Technology: improved relative to first half

Off-Highway: growth rates normalised with some markets showing “subdued demand”

The breadth of Volex’s customer base is in part a reflection of its regular acquisition activity, which has driven more than half its revenue growth over the last nine months.

Operating profit margins are said to be “within our target range” of 9%-10%.

Net debt at the end of the quarter was $151m excluding lease liabilities, representing 1.3x EBITDA, unchanged from H1.

Growth investments have continued, adding capacity in countries including India and Indonesia during the year. The company also reports recent increased demand from a major data centre customer in North America.

Outlook: the company says its confident customer demand will sustain “high single-digit organic growth for the full year” while maintaining margins in their target range.

Volex expects to report underlying operating profit in line with current market expectations. These are helpfully included in the footnotes to today' s release – the averages provided are:

Revenue: $1,031.4m

Underlying operating profit: $96.7m

These estimates price the shares on a forward P/E of 11 and would represent growth of 13.0% and 7.8% respectively versus FY24 results. This suggests slightly lower margins versus last year’s figure of 9.8%.

Roland’s view

Executive Chairman (and 25% shareholder) Nat Rothschild appears to be continuing to deliver attractive growth at reasonable margins.

This business is relatively capital intensive, so quality metrics are only modestly above average:

For this reason I wouldn’t personally want to pay a high multiple. However, Volex operates in a number of attractive long-term growth segments and seems to be performing well.

The current valuation looks very reasonable to me. I’m happy to maintain our GREEN view.

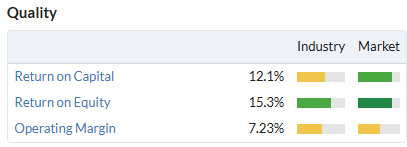

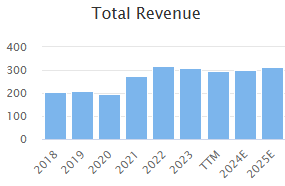

Stelrad (LON:SRAD)

Unch. at 142p (£181m) - Trading Update - Roland - AMBER/GREEN

the Board expects to deliver an adjusted operating profit of c.£31.5m, marginally ahead of expectations

Stelrad is a leading manufacturer of central heating radiators in the UK, Europe and Turkey. This business was one of the class of 2021 IPOs, but unlike many flotations from that year has subsequently proved to be a decent business.

Today’s full-year update appears to be slightly ahead of expectations and contains some points I think are worth highlighting.

Trading update: Stelrad says revenue fell by 9% to c.£290m last year as “ongoing high interest rates and inflation” held back activity in both new build and RMI markets (repair, maintenance and improvement).

As a result, full-year revenue fell by 6% to c. £290m. Although H2 volumes benefited from some new business wins, overall volumes remained below 2023 levels. Indeed, revenue peaked in 2022:

However, while volumes were down, profitability rose sharply. Stelrad says it achieved an 11% increase in contribution (profit) per radiator during the year. This was achieved through “proactive margin and cost management” but also due to “the price benefit of further increases in average radiator size”.

Impressively, in my view, Stelrad says this is the seventh consecutive annual increase in contribution per radiator.

It’s because of this that the company expects to report an adjusted operating profit of c.£31.5m (2023: £29.3m) at an operating margin of 10.8% (2023: 9.5%).

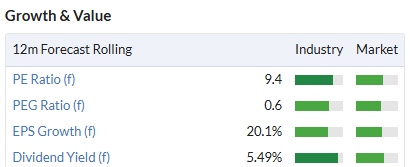

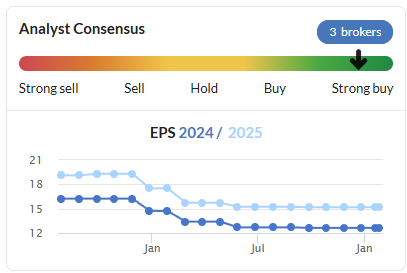

Outlook: no broker forecasts are available on Research Tree for Stelrad but consensus forecasts on Stockopedia prior to today suggested 2024 earnings of 12.6p per share. I suspect the impact of today’s upgrade will be relatively small, so I’d estimate an updated figure of c.13p, pricing the shares on 11x 2024 earnings.

There’s also a useful 5.4% dividend yield:

Looking ahead to 2025, Stelrad is expected to deliver further earnings growth, with consensus estimates suggesting earnings could rise by 20% to 15.2p per share.

In today’s statement, Stelrad says it expects “continued softness in market conditions” but is starting to see a recovery in volumes in some core European markets. I get the feeling European markets are a little ahead of the UK in terms of demand – the company cites:

strong embedded replacement demand across Europe, product premiumisation upside and long-term regulatory tailwinds for decarbonised energy efficient heating systems continue to underpin the Group's confidence in the future

We’ll have to see if any updated broker forecasts filter through to Stockopedia over the coming days. My impression from today’s update is that current 2025 expectations are largely unchanged.

Roland’s view

Stelrad appears to be benefiting from two factors, premiumisation and decarbonisation – heat pumps require larger radiators than fossil fuel systems. In the UK at least, I think there’s also the potential for a cyclical recovery at some point.

I am not sure how far Stelrad can go with premiumisation, but I expect the decarbonisation trend to remain a structural driver for the fitment of larger radiators for many years. I know if I was buying radiators today, I would consider the spec likely to be needed for a heat pump, even though I’ve no immediate plans to replace my boiler.

Stelrad shares have lost their IPO froth and now look quite reasonably valued to me, given continuing progress:

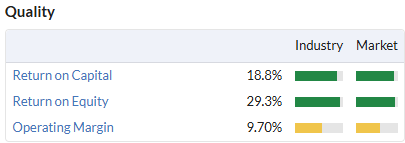

The company’s quality metrics are also above average:

However, there are a couple of points that I think are worth watching.

As Paul has commented previously, debt levels are relatively high. The interim results showed net bank debt of £64m with cash interest paid of £3.8m, or perhaps c.£7.6m annualised. That would be roughly a quarter of FY24 adjusted operating profit.

Today’s update reports year-end leverage of 1.4x EBITDA. This sounds reasonable and is comfortably within covenants, but I think it understates the level of indebtedness here, given that interest payments are deducted from EBITDA.

I prefer to compare net debt to net profit to get an idea of how quickly a company might repay its debt. The interim net debt figure of £64m represents 4x 2024 forecast net profit of £16.2m. This is at the upper end of my comfort zone.

Much as I like receiving big dividends, Stelrad’s dividend payout of c.60% of earnings also looks a little generous to me. I think it would be sensible to reduce the payout and use some additional cash to repay debt.

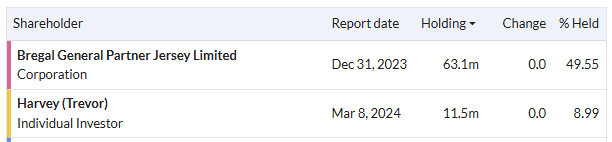

However, I’d speculate that one possible reason for the company’s dividend policy is CEO Trevor Harvey’s 9% shareholding. I estimate he is receiving over £880k per year in dividends!

Similarly, the company’s former private equity owner is receiving around £5m.

On a related note, these two shareholders effectively control the company – there’s not much liquidity:

Despite these comments, I’m positive about Stelrad and am hopeful of seeing volumes and revenue stabilise this year. The StockRanks are also positive:

On balance, I think the shares are probably decent value at current levels. AMBER/GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.