Good morning! The FTSE is due to open unchanged in the low 8400s - it has been stable around this level in the last few trading sessions.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

| Marks and Spencer (LON:MKS) (£7.9bn) | Cyber Incident - Further Update | M&S has suspended all online ordering from its websites as a consequence of the cyber attack first reported on 22/4. | AMBER (Roland) [no section below] The company’s interim results reported that 33% of Clothing & Home orders were made online. Extrapolating the H1 results suggests to me that online orders could perhaps represent c.£150m of annual operating profit – around 15% of the group total. This cyber attack appears to be causing significant disruption, but M&S has not yet provided any real explanation of what’s happened. This leads me to fear that the problem may not yet be fully understood. |

| ITV (LON:ITV) (£3.0bn) | No RNS - press reports re. takeover talks | SP -2% today to 79p. | AMBER/GREEN (Roland - I hold) ITV faces structural challenges at home and tough market conditions more generally. But I continue to believe the content business is undervalued and that the whole group is performing better than the market recognises. The risk, of course, is that I’m wrong – or at least that future headwinds will be worse than I expect. I’m leaving our moderately positive view unchanged today. |

| Deliveroo (LON:ROO) (£2.2bn) | Response to Press Speculation | SP +17% to 171.4p. Friday RNS: possible cash offer at 180p from DoorDash. BoD would be minded to recommend such an offer. Engaging in discussions. | PINK (Graham) I can see why DoorDash are interested to buy at 180p, but I struggle a little to see why the offer would be recommended to shareholders. Some may be keen for the exit ever since the overpriced IPO, but on a forward view I think the prospects for Deliveroo are bright. I'd want more than 180p. |

Plus500 (LON:PLUS) (£2.2bn) | FY25 results to be ahead of exps. Market exps: revenue $719.2m, EBITDA $331.3m. | GREEN (Graham) The market was primed for a strong update so there has been little movement in the Plus500 share price this morning. PLUS continues to make progress on a range of fronts. In terms of customer activity, there is a small reduction in the user base but with a higher ARPU. Overall, it's a nice, reassuring update. Panmure Liberum have made no change to their EPS estimate as they were already near the top of the range. Shares trade at c. 11x earnings before any adjustment for Plus500's very strong balance sheet. | |

Seplat Energy (LON:SEPL) (£1.1bn) | Robust production and cost performance, and firmly on track to deliver FY 2025 guidance. | ||

Yellow Cake (LON:YCA) (£933m) | NAV fell 14.4%. Volatility in spot uranium price. Activity expected to resume once there is tariff clarity. | ||

Elixirr International (LON:ELIX) (£313m) | Rev +30%, adj. PBT +22% (£29.7m). Moving to Main Market. Confident FY25 in line with exps. | AMBER/GREEN (Roland) Strong top-line growth has been aided by acquisitions and organic expansion, including an increase in the number of £1m+ revenue clients. A move to the Main Market could lead to index membership and new shareholder inflows. However, there’s some evidence of pressure on margins and the focus on US growth is arguably slightly less attractive than previously. Dependence on key fee earners is another possible risk. On balance I remain moderately positive at current levels. | |

Marlowe (LON:MRL) (£256m) | Rev & adj. EBITDA in line. Adj. PBT ahead of exps at c. £18.5m. Also: £6.2m bolt-on acquisition. | ||

Metals Exploration (LON:MTL) (£203m) | The mobilisation of the La India project appears to be proceeding to plan. Condor Gold shareholders to benefit per takeover agreement. | AMBER/GREEN (Roland) [no section below] A forward P/E of 5 and net cash position suggest MTL could offer value if gold prices remain high – the recent Q1 update highlighted Q1 free cash flow of $23.5m on revenue of $48.4m. However, as always with small-cap commodity producers, I think it’s important to consider the potential impact falling commodity prices might have on profits and the risk that unforeseen problems could arise in far-off lands. In this case specifically, it’s worth remembering that MTL currently only has one mine in production (Runruno in the Philippines). Metal Exploration’s high StockRank (94) and Super Stock styling are encouraging and highlight positive fundamentals. However, I would personally be very careful about position sizing without carrying out more in-depth research into this business. | |

Aoti (LON:AOTI) (£88m) | Rev +33%, adj. EBITDA $8.1m (2023: $1.7m). Significant uncertainties. Steady start to 2025. | ||

Science in Sport (LON:SIS) (£77m) | Rev down 17%, adj. EBITDA £4.2m (2023: £2m). 2025 has started well. | PINK (recommended cash offer) | |

Pulsar (LON:PULS) (£50m) | New contract with very large marketing/ad client. Total annual spend +150% to $2.2m. | ||

Frenkel Topping (LON:FEN) (£44m) | Rev +14%, PBT +31% to £4.2m. FUM +17% to £1,560m. Strong Q1, outlook in line with exps. | ||

MTI Wireless Edge (LON:MWE) (£43m) | $0.8m defence win for test range shelter. Delivered before end 2025. Forecasts unchanged. | ||

Cyanconnode Holdings (LON:CYAN) (£36m) | SP down 22% | BLACK (RED) (Graham) [no section below] | |

Orosur Mining (LON:OMI) (£34m) | $2.36m cash post placing. Colombia acq complete, seeing some “exceptional” drilling results. | ||

Christie (LON:CTG) (£23m) | Rev +15%, adj op profit £2.0m (2023: £0.3m). Net cash £4.9m. Strong pipeline, confident outlook. | ||

Smarttech247 (LON:S247) (£8.1m) | Rev +21.4%, ARR now €9.4m. LBT reduced to €(383k). New contract wins, positive outlook. | ||

Feedback (LON:FDBK) (£7.7m) | PW. NHS contracts delayed.FY25 rev now exp £0.9m (prev: £1.6m). Increased loss. £6.6m cash. | BLACK | |

Ingenta (LON:ING) (£7.4m) | Rev -5.6%, ARR +2.3% to £8.9m. Adj EBITDA -18% to £1.8m. 4.1p divi. FY25 trading in line w/ exps. |

Graham's Section

Plus500 (LON:PLUS)

Unch. at £30.46 (£2.21bn) - Q1 2025 trading update - Graham - GREEN

Plus500, a global multi-asset fintech group operating proprietary technology-based trading platforms, announces today the following trading update for the three months ended 31 March 2025.

The outlook section here states that PLUS has made “an excellent start to the year, driven by recent macroeconomic and financial market conditions among other factors”.

As a result, FY Dec 2025 is anticipated to be ahead of market expectations.

So why are Plus shares flat today (and initially fell on this announcement)?

There’s a clue in the chart:

Since the beginning of April, spread bet and CFD shares have been very strong, e.g.Plus and IGG (in which I have a long position) both gained over 10%. This happened of course while most stocks and indexes were falling.

Volatility is great news for trading platforms, and the VIX volatility index spiked to levels not seen since Covid. So naturally, the market has been expecting good news from the likes of Plus.

Some of the highlights from today’s release. These numbers relate to Q1 (to the end of March), before the recent spike in volatility.

Q1 revenue +13% to $205.8m against Q4 2024, but down 5% against Q1 2024.

Customer income (the most reliable income - spreads, overnight charges and commissions) +3% to $176.3m against Q4 2024.

EBITDA margin of 46%, better than the average seen in 2024.

Despite the positives, the year-on-year drop-off in revenue and EBITDA against Q1 2024 may be of some slight concern, even though there was sequential growth against Q4 2024:

As for customer numbers, I see that there has been a sharp slowdown in the number of new customers recruited (down 26% vs. Q4 2024).

A key feature of this business (and not a good one) is that users are constantly dropping out. I presume that most customers leave when they aren’t willing to lose another deposit. So unless customer recruitment is very active, the user base is always inclined to start shrinking.

When I discussed the company in February, I noted that they had been spending very big on customer acquisition.They recruited 118,000 new customers in 2024 with 36,000 recruited in Q4 alone.

In Q1 2025, however, they have only recruited 27,000.

This meant that their active user base declined, both year-on-year and against the previous quarter.

The blow of slightly fewer customers is softened by an 18% increase in average revenue per user in Q1 (vs. Q4 2024). Plus has tried to target higher value customers and this seems to be working with ARPU up and a doubling in the average deposit per active customer from $6,000 to well over $12,000.

India: Plus recently acquired an Indian broker for $20m - a “key strategic milestone”.

US futures business: this is a major source of growth currently and is classified by Plus as part of their “non-OTC” business. Non-OTC has grown to 12% of their total revenue (10% in 2024).

Cash balances: $885m as of 31st March.

Estimates: Panmure Liberum have nudged up their revenue estimate for the year by 4% but they leave their EBITDA estimate unchanged at $343m, “given we are already at the top end of the consensus range”.

Graham’s view

My previous comments (Feb and Jan) cover much of the same ground. I tend to always have one or two concerns when it comes to Plus500 - and the main thing I worry about these days is customer churn. But the big picture from my perspective is that the company remains extremely well capitalised (at least on paper!), highly profitable, shareholder-oriented with a mix of buybacks and dividends, and is constantly growing and expanding its capabilities, including through acquisitions.

The StockRank remains terrific:

I’ve long abandoned my misgivings about this one, when it comes to giving it a GREEN colour. Perhaps I still don’t 100% trust its risk management policies. I still feel uneasy about its policy to book its customers' trades and then to profit directly from their losses - another $15m in “customer trading performance” in Q1.

However, I can’t deny that Plus is extraordinarily successful at both growing its market share and at generating cash. I’m positive on this entire sector and I’m invested in it through IG Group (IGG). So I don’t see how I can be anything but positive on Plus.

Even after recent gains, valuation still appears reasonable. Remember that the PE Ratio is calculated without making any adjustment for the company’s enormous cash pile, at least some of which is surely surplus to requirements..

Deliveroo (LON:ROO)

Up 17% to 171.9p (£2.57bn) - Response to Press Speculation Graham - PINK

This announcement came out at 6.10pm on Friday: response to press speculation.

I’m glad that I wasn’t too negative on the company recently, giving it an AMBER/GREEN two weeks ago after noting that nearly £6n of air had been removed from its £7.6bn 2021 IPO valuation.

Net cash was £668m, covering a decent chunk of the market cap.

Doordash have noticed this:

Following recent press speculation, the Board of Deliveroo confirms that on 5 April 2025 it received an indicative proposal from DoorDash, Inc. ("DoorDash") regarding a possible cash offer for the entire issued and to be issued ordinary share capital of Deliveroo at a price of 180 pence per Deliveroo share (the "Possible Offer").

Having carefully considered the Possible Offer with its advisers, the Board of Deliveroo has indicated to DoorDash that, should a firm offer be made on the financial terms set out above, it would be minded to recommend such an offer to Deliveroo shareholders, subject to the agreement of the other terms of the offer.

It’s interesting that it took so long for this news to come out. While I don’t think that every takeover offer that a company receives should be disclosed immediately, I do think that credible offers that a Board is seriously considering should be disclosed as soon as they reasonably can. This one clearly fits into that category!

Graham’s view

This takeover makes good sense to me strategically, from DoorDash's perspective.

Firstly, DoorDash has leading market share in the United States, with 67% market share in food delivery, and is highly ambitious internationally.

In the UK, however, DoorDash is very far behind - Just Eat has 45% market share, while Deliveroo and UberEats both have 27%. So it makes sense that DoorDash would want to accelerate their progress by buying up on one of these three.

Just Eat was already acquired by the Dutch company takeaway.com (StockReport) while UberEats is of course owned by Uber Technologies (NYQ:UBER). So Deliveroo will be the simplest to acquire of the main three UK players.

Secondly, on valuation. DoorDash itself trades at a Price to Sales multiple of 7x, and a PER of 71x. This is the DoorDash StockRank:

Deliveroo, meanwhile, as of last night, was at a Price to Sales multiple of only 1x and a PER of 24x. This is before taking into account its enormous cash pile.

Now I wish I had acted on my suspicion that it offered good value at that level!

With DoorDash trading at such lofty heights, and internationally ambitious, I think I can see why it might have identified Deliveroo as a target.

Actually, if I was a Deliveroo shareholder, I would probably demand a higher sale price than 180p.

This is a company that came to the market four years ago at 390p.

Everyone agrees now that valuation at that time was silly. But the company has made progress since then: revenues have grown over 20%, the company looks to be turning the corner into meaningful profitability, and its share count is lower now thanks to hundreds of millions of pounds spent on share buybacks.

If I was a Deliveroo shareholder, I would be concerned that I had taken all the risk of holding it through some tough years and then DoorDash was taking away most of the upside just as it was on the cusp of producing some excellent financial results.

This isn’t a normal business - it’s a platform-type business with high market share and a well-known brand. It deserves a premium rating. Is DoorDash really offering that at 180p? I doubt it. It’s only about 10x the EBITDA forecast for next year. I’d vote no to this. But Deliveroo shareholders will decide!

Roland's Section

Elixirr International (LON:ELIX)

Up 4.8% to 681p (£328m) - Final Results - Roland - AMBER/GREEN

Elixirr International plc (AIM:ELIX), an established, global award-winning challenger consultancy, is pleased to announce its final results for the year ended 31 December 2024.

This consultancy group has been one of the more successful AIM market flotations of recent years:

Sadly for AIM fund managers, today’s results include news that Elixirr is planning a move to the Main Market in 2025:

This move is an important step in Elixirr's evolution, and one that should set Elixirr up perfectly for the future as we continue to grow towards our stated ambition of becoming a consulting unicorn, with a market capitalisation exceeding $1 billion.

Stocko’s algorithms view this stock as a High Flyer, so I’m interested to see how the business has performed over the last year:

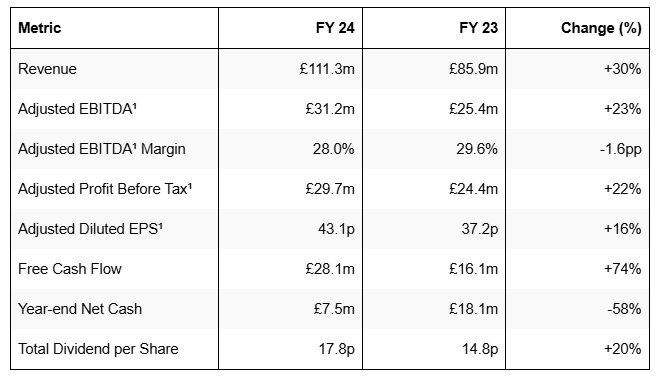

2024 results summary: I covered Elixirr’s 2024 trading update in February, when the company upgraded its guidance for the year (slightly). Today’s results are in line with February’s revised guidance for revenue of at least £111m and adjusted EBITDA of around £31m:

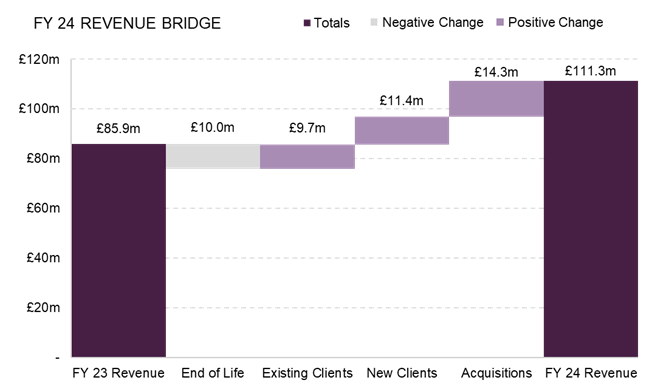

Elixirr is an acquisitive business and completed the purchase of Hypothesis Group for $45m in October 2024 and Insigniam earlier in 2024. The Hypothesis purchase was a fairly material deal for a company of this size so it’s helpful to see the company provide a revenue bridge separating out last year’s growth into its component parts:

My sums suggest that organic revenue growth was around 13% last year, still a respectable performance.

Looking further down the accounts, the acquisition of Hypothesis appears to have had a slightly dilutive effect on profitability.

Administrative expenses rose by 28% to £11m, while the group’s adjusted EBITDA margin fell from 30% to 28%:

This is in the middle of our guidance range of 27-29% and includes the dilutive impact of Hypothesis when compared to FY 23 Group Adjusted EBITDA margin.

As usual, investors must choose whether they want to accept adjustments relating to depreciation, amortisation, share-based payments and M&A costs:

Adjusted pre-tax profit: +22% to £29.7m

Reported pre-tax profit: +3.6% to £22.9m

Using the more conservative statutory figures, my sums show that Elixirr generated an 2024 operating margin of 21.3% and a return on equity of 12.4%. These are a little below the trailing 12-month figures for the group, highlighting the impact on H2 profitability of the Hypothesis acquisition:

Turning to the cash flow statement, I estimate Elixirr generated free cash flow of £18.4m excluding acquisitions last year. This represents 105% conversion from the group’s total reported income of £17.5m, giving me confidence in using the group’s statutory profits for my analysis.

Trading commentary: the company says its existing partners were stretched in 2024, with revenue per partner rising by 6% to £4.1m. This was said to be driven by growth in existing accounts and “targeted expansion across higher-margin service lines”.

New partners were added with “deep expertise” in areas including financial services, cybersecurity and technology.

The acquisition of Hypothesis (“a US-based insights and strategy firm”) is expected to accelerate Elixirr’s US expansion and enhance the group’s capabilities in research, brand strategy and data science.

The organic growth I mentioned earlier appears to have been aided by an increase in larger customers. This seems very positive to me:

The Group increased its number of "gold clients" (where revenue exceeds £1 million in one year) from 19 in FY 23 to 27 in FY 24, demonstrating the effectiveness of the Elixirr Partners in deepening existing client relationships.

Outlook: the company says that 2025 has started well, with the first quarter delivering record revenue for the group. April 2025 is also expected to be a record revenue month.

Management say that performance for the full year is expected to be in line with expectations:

Elixirr remains confident in delivering FY 25 trading results in line with management expectations, supported by revenue contracted to date and anticipated client demand.

We are not told what these expectations are. The company says that “in line with market norms”, it is not providing direct guidance on revenue or EBITDA ahead of its Main Market listing.

However, broker Cavendish appears to have left its 2025 forecasts in place and unchanged today, suggesting revenue of £139.2m and adjusted earnings of 48.4p per share. These figures would represent an increase of 25% and 12.3% respectively from 2024.

Roland’s view

Cavendish estimates suggest Elixirr’s top-line growth will remain healthy in 2025. But the revenue growth rate of 25% is double the forecast earnings growth rate, suggesting that we could see further pressure on profit margins this year.

I remain impressed by Elixirr’s growth and can see the logic for a move to the Main Market. The stock’s current valuation of 16x FY24 earnings seems fair, if not cheap, and I can see the scope for further growth.

The continued leadership of founder Stephen Newton is also a positive for me, given his 23.7% shareholding and strong track record to date.

At the same time, I’m always slightly wary about companies with aggressive, acquisition-led growth plans. I also tend to be cautious about service groups where key fee-earning staff are the business.

Elixirr’s plans to continue expanding in the US may also be a reason for caution, given the uncertain outlook in that market.

On balance, I don’t think I can justify a fully positive stance. But I’m comfortable maintaining our previous AMBER/GREEN view following today’s results.

ITV (LON:ITV)

Down 2.3% to 79p (£3.0bn) - Press reports - Roland - AMBER/GREEN

(At the time of publication, Roland owns shares in ITV.)

The UK’s largest commercial broadcaster is a perennial takeover target, due to the perceived undervaluation of its ITV Studios content production business. Over the weekend, the Financial Times reported (£) that French rival Banijay – which makes programmes including Peaky Blinders, Masterchef and Big Brother – is in early talks with ITV.

Options being considered are said to include an offer for the ITV Studios business or a full takeover of ITV, in partnership with other investors.

According to the FT’s source, ITV’s discussions with Banijay are still at an early stage, with no certainty they will progress to a possible offer.

ITV has reportedly previously held early talks with investment group RedBird IMI (owner of All3Media) and has also considered acquiring All3Media itself, before reportedly deciding that its shareholders would not accept the resulting financial strain.

Roland’s view: my personal portfolio has a small ‘legacy’ position in ITV which I continue holding because I too believe the content business is undervalued.

The Studios business generated an adjusted operating profit of £300m last year. In my view, it’s plausible to suggest that this alone justifies ITV’s £3bn market cap, with the still-profitable broadcast business (FY24 EBITA: £250m) valued at zero.

(I discussed ITV’s business model in more depth in a Stock Pitch in January.)

While ITV’s legacy broadcast business is under pressure from declining ad revenue and changing viewing habits, it remains profitable and cash generative. My perception is that the company is making good progress migrating its UK viewers to digital services.

ITV remains by far the UK’s largest commercial broadcaster, with around 14m monthly active streaming viewers and a 32% share of UK commercial broadcast viewing.

On balance, I believe the UK market is large enough to retain space for dedicated UK television services (as opposed to global/US streamers).

For now, I’m not getting too excited about this new bid interest. It’s hardly the first time ITV has been the subject of such stories.

Markets are taking a cool view too, with the stock down slightly at the time of writing – albeit up 7% so far this year:

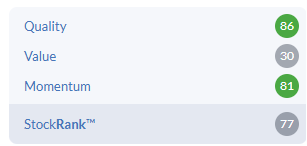

The StockRanks remain highly positive, styling this business as a Super Stock – potentially highlighting an investment case regardless of any takeover activity:

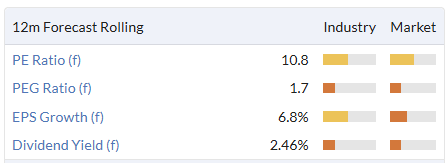

The current valuation certainly doesn’t seem demanding to me:

I remain happy (if slightly frustrated) to continue holding.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.