Good morning and welcome back - today's Agenda is now complete.

Defence stocks

Thanks to Howard Adams in the comments for pointing out the strength of European defence stocks this morning.

A sub-index that’s available on Stockopedia is the FTSE Eurofirst 300 Aerospace & Defense Index. It has performed amazingly well in recent years and is up by nearly 7% this morning alone.

The difficult meeting between President Trump and Ukraine’s Zelenskyy on Friday was followed up with a weekend of diplomacy in London. Britain and France will shortly present a new peace plan to the United States that envisages European peacekeeping troops in the Ukraine.

When it comes to the financial implications of these developments, we have the following snippet from The Times last night:

Macron also said that European countries should raise their defence spending to between 3 and 3.5 per cent of gross domestic product. Earlier in the day, Mark Rutte, the Nato secretary-general, said “more European countries will ramp up defence spending” but did not go into specifics

The UK’s defence budget is heading for 2.5% of GDP by 2027, with an ambition for it to reach 3% in the next parliament.

On Saturday, the government announced a £2.26bn loan to bolster Ukrainian military capability. This loan will be “fully earmarked for military procurement”.

This morning we’ve seen the following movements:

BAE Systems (LON:BA.) up 15%

Qinetiq (LON:QQ.) up 9%

Chemring (LON:CHG) up 4%

Senior (LON:SNR) down 3% (but they have also published annual results)

Well done to those of you who have invested successfully in defence stocks. It’s not a sector where I claim to have any special insight, but it does seem that it will continue to enjoy strong demand for the foreseeable future.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Bunzl (LON:BNZL) (£11.0bn) | Final Results | Outlook: maintaining guidance for robust revenue growth and operating margin in line with 2024. | |

Londonmetric Property (LON:LMP) (£3.8bn) | Adds £13.2m of annual rental income | 122 lettings, regears and rent reviews. Rent reviews giving a 16% uplift on 5-year basis. | |

Senior (LON:SNR) (£678m) | 2024 Annual Results | Outlook: in line with expectations. Committed to sale of Aerostructures business. | |

Hunting (LON:HTG) (£511m) | Sale of associate company | Sale of 23% equity stake in Rival Downhole Tools for $13.1m. Non core. | GREEN [no section below] (Roland) |

Avon Technologies (LON:AVON) (£433m) | Contract win | Team Wendy Ceradyne has received a US Army helmet order (NG-IHPS) worth $17.6m. | AMBER/RED [no section below] (Roland) |

Severfield (LON:SFR) (£141m) | TU | Profit warning. Client decisions deferred. Low business confidence. Cancels buyback. | BLACK (AMBER/RED) (Roland) |

| Zotefoams (LON:ZTF) (£130m) | CFO Retirement | CFO will retire from his role “during 2025”. The search for a successor is underway. He is thanked. | GREEN (Graham) [no section below] This is not an old-age retirement. ZTF’s CFO has been with the company for 9 years and may simply desire a change. Or perhaps the company’s new CEO wants to get the perspective of a new CFO? Either way I don’t find this announcement concerning. It sounds like there will be an orderly transition. ZTF’s leverage multiple of c. 0.9x suggests little risk of financial stress. |

Knights group (LON:KGH) (£117m) | £30m acquisition | Acquisition of IBB Law LLP, a “premium” firm with 140 fee earners. Exp PBT margin c.26%. | AMBER (Roland) |

Ramsdens Holdings (LON:RFX) (£76m) | AGM TU | Has continued to trade well across its key income streams. | GREEN (Graham) [no section below] It would be best if the RNS had explicitly confirmed that trading was in line with expectations. PanLib’s last-published estimates include PBT of £12m and EPS of 27p in the current year (this gives a PER just below 9x). For now I think it’s right to presume that trading “well” means trading “in line”. I’ll leave my positive stance unchanged. In other news the long-standing Chair of the company retires from the Board today, to be succeeded by the current Senior Independent Director. |

Quartix Technologies (LON:QTX) (£76m) | Final Results | SP +10%. | AMBER/GREEN (Graham) [no section below] 2024's full-year dividend (4.5p) is much higher than the forecast at broker Cavendish and given the strong start to 2025, this year's numbers are upgraded. The revenue forecast is increased by 2% (to £36m) and the adj. EBITDA forecast is increased by 8% (to £7.3m). 2024's accounts are pleasantly free of adjustments and hopefully this will be true again in 2025. The PER is c. 16x currently. On fundamentals, I am still a little concerned about price erosion as an ongoing feature of the telematics sector. QTX has managed to implement price increases across the board but revenue from existing customers still isn't growing with NRR (net revenue retention) below 100%. So I don't know if this truly offers a growth opportunity for the long-term. On balance, I will upgrade our stance on this slightly to AMBER/GREEN. Attractive features include the positive outlook for the current year, oversight by the founder and largest shareholder Andy Walters, and clean accounts for 2024. |

HSS Hire (LON:HSS) (£43m) | FY TU | Adj EBITDA of £48.5m for 12 mo. to 30 Dec. Costs +3% YoY. No guidance for new y/e of 31 March. | |

Petrofac (LON:PFC) (£35m) | Update on restructuring timeline | Court hearing on 28 Feb, adjourned until 20/21 Mar. Sanction hearing finish mid-Apr. | |

Argo Blockchain (LON:ARB) (£23m) | Term Sheet for up to $40m Financing | Interest rate 8%. Convertible. Lender also to get warrants and 3 board seats. | |

Bigblu Broadband (LON:BBB) (£17m) | Proposed return of £6.1m to shareholders | Received £14.9m from a disposal. Proposes a tender offer at 40p (vs. latest share price: 28p). |

Roland's Section

Severfield (LON:SFR)

Down 42% to 28p (£82m) - Trading Update - Roland - BLACK (AMBER/RED)

As such, underlying profit before tax for FY26 is now expected to be below our revised expectations for FY25.

Structural steel group Severfield has issued another profit warning this morning. This is the second in four months, following November’s downgrade which Megan covered here.

Today’s update relates to the year ending 29 March 2025 and the following (FY26) financial year. The company’s commentary suggests to me that a weak year lies ahead:

Since [our November update], market conditions have shown no signs of improvement, with pricing remaining at tighter levels for longer than expected in a competitive market and project opportunities continuing to be either cancelled or delayed.

The order book has fallen from £410m on 1 Nov 24 to £403m on 1 Feb 25.

Orders for delivery in the next 12 months have fallen from £307m to £281m over the same period.

Cost savings are underway and the share buyback programme has been cancelled but these measures will not generate enough savings to cover factory overheads in Q4, prompting today’s profit warning.

Severfield’s management now expects to report an FY25 underlying pre-tax profit of £18m to £20m.

Estimates: house broker Panmure Liberum has helpfully translated today’s update into revised earnings estimates - many thanks.

Unfortunately, the news isn’t good:

FY25E EPS down 34% to 4.5p

FY26E EPS down 64% to 2.9p

FY27E EPS down 42% to 4.9p

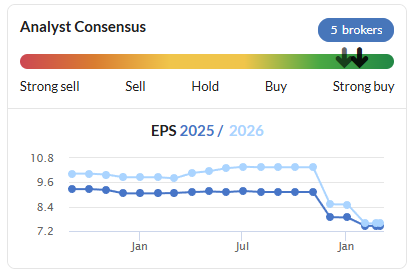

These changes come just three months after September’s profit warning, when Panmure cut its FY25 and FY26 forecasts by 26% and 25% respectively. Stockopedia’s consensus trend chart shows the impact of cuts from the five analysts covering Severfield:

Outlook: the company’s outlook statement reinforces my view that the business has very limited visibility on when a recovery might begin:

client decision-making continues to be deferred and projects are not being awarded or progressing within normal timescales

Management comment on the “lower level of business confidence in the UK economy as a whole” and warn that Severfield does not currently have any “large ‘anchor’ projects” in its order book.

There’s also some uncertainty about the eventual cost of the bridge remedial works programme the company is engaged in. The company took a £20m provision for this in H1, but my impression is that insurance will cover a substantial proportion of the costs being incurred.

The company says we should see some improvement from FY26 onwards:

Looking further ahead, we have already secured some attractive large projects for FY27, and we are also seeing future large opportunities in sectors such as data centres, manufacturing (industrial) and commercial offices, including the emergence of several planned large developments in London.

Roland’s view

As a relatively capital-intensive business with quite high fixed costs, one risk worth considering is that Severfield could become financially stressed.

Today’s update confirms year end net debt (exc. leases) is expected to be between £45m and £50m at the end of March, in line with expectations. The company says this provides “cash headroom of £25m - £30m”.

Panmure’s figures today suggest net debt will improve slightly over the next couple of years, although this is predicated on cuts to the dividend in FY26 and FY27, to maintain 2x earnings cover.

This level of debt isn’t without risk, but it does look manageable to me relative to revised profit forecasts for the next couple of years.

Today’s share price drop leaves the shares trading at nine times revised FY26 estimates and just five times FY27 numbers. The shares could be cheap if and when order intake improves. However, prospective investors need to offset this against the risk of further bad news, which I think is possible.

Megan went RED on Severfield in November. Today’s 40% share price drop has vindicated that caution. However, I don’t yet see any existential risks to this business and I believe some value may be emerging at current levels.

On this basis, I’m going to move tentatively to AMBER/RED today.

Knights group (LON:KGH)

Up 2.5% to 139p (£120m) - Acquisition of IBB Law LLP - Roland - AMBER

Legal services group and serial acquirer Knights has announced that it will pay up to £30m to acquire the business of IBB Law LLP:

IBB brings a team of 140 fee earners delivering premium legal services to both business and private clients, significantly increasing Knights' scale in the South East, an attractive market with a significant concentration of corporates and private wealth.

This is a fairly sizable acquisition for Knights, which has a market cap of £120m. The company says it will be funded out of existing bank facilities – i.e. using debt.

IBB has 29 equity partners who will receive £30m, with an initial cash payment of £21m and deferred cash consideration of £9m paid over three years. So the partners will receive an average of c.£1m each.

The economics of the deal seem interesting and highlight the potential appeal of Knight’s roll-up business model:

In FY24 IBB reported £23m and a “corporatised PBT margin of 6%”

Knight’s management expects to transform this to a PBT margin of c.26%, “following full integration and realisation of synergies”

This implies a possible pro forma purchase multiple of 5x PBT, which doesn’t seem expensive.

Roland’s view

Knights seems to be executing well and is continuing to generate both top line and bottom line growth:

However, I am not all that enthusiastic about professional service partnerships being rolled up into corporate vehicles. This is partly for philosophical reasons and partly because of the risk that key fee earners may take their client relationships elsewhere.

A comment in today’s RNS highlights this risk (my bold):

Prudently assuming 20% revenue churn post-acquisition and excluding the non-core Crime business

Knights reported net debt (exc. leases) of £50m at the end of October 24. Assuming this figure has remained stable, then today’s deal suggests net debt will be £71m after the initial payment for IBB.

The company recently extended its credit facility from £70m to £100m and I estimate that net debt/EBITDA leverage should remain under 2x following this deal.

But on more conservative measures of leverage, relative to net profit or free cash flow, Knights looks more highly geared to me. I don’t see any pressing concerns at the moment, but this is an area I’d watch.

Similarly, I think it’s worth remembering the large divide between the company’s reported and adjusted profits. In January’s half-year results a pre-tax profit of £9.0m was transformed into an underlying PBT of £14.6m.

Even the cash flow statement includes “non-underlying operating costs”.

These adjusting items are generally related to acquisitions and seem perfectly legitimate to me. But they tend to recur in Knights’ accounts and I would tend to view them as routine operating costs.

For this reason, I prefer to value Knights shares on reported earnings, rather than adjusted earnings. On this basis, my sums suggest Knights trades on a trailing 12-month P/E of 10.

Roland’s view

CEO David Beech has a 22% shareholding, suggesting his interests remain well aligned with those of shareholders.

Knights shares look reasonably valued to me at the moment and I can see the potential for further gains.

However, as I’ve commented above, I don’t think the shares are as cheap as adjusted broker earnings forecasts might seem to suggest and I can see some risks in this business model.

Another concern is that I’d like to see more evidence of organic growth. Knights’ H1 results showed organic revenue flat, with top line growth driven by acquisitions alone.

It’s possible that I’m being a little too cautious. But with no update on trading or full-year guidance today, I’m going to maintain my neutral view from November. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.