Good morning! I'm refreshed after taking a long weekend - thanks to Roland for writing Friday's report. Let's see what we've got today!

Results deadline day: this is the last day on which AIM companies can publish their full-year results for 2024 (if December is their year-end).

Also, for any companies that use March as their year-end, this is the last day on which they can publish their interim results. From the AIM rules:

All such reports (GN: half-yearly reports) must be notified without delay and in any event not later than three months after the end of the relevant period.

So this is the day for stragglers to get their results in, if they don't want to get suspended!

All finished for today, thanks.

Spreadsheet accompanying this report: link.

The Agenda is complete.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

International Workplace (LON:IWG) (£2.1bn) | Transitioning from IFRS to US GAAP accounting, has republished 2022/3/4 accounts. | ||

Chemring (LON:CHG) (£1.51bn) | Landguard makes SDR (radio) systems, consideration up to £20m (2.8x rev). Will be part of Roke. | ||

WH Smith (LON:SMWH) (£1.43bn) | SP -3% | AMBER (Roland) [no section below] Recent softer trading and “a more cautious outlook amongst stakeholders” meant the original sale terms for the High Street business were “no longer deliverable”. Therefore, to complete the sale, WH Smith has taken a significant haircut. I guess we now know why the original deal wasn’t better – even that proved too much of a stretch, perhaps as there are few willing buyers for a business of this type. I can’t help suspecting that buyer Modella (which owns Hobbycraft) has got a good deal here – the high street business generated a trading profit of £15m in H1. However, the disposal means a clean break for WH Smith and will give investors much clearer visibility on its qualities and performance as a travel-only retailer. Megan was neutral earlier in June and I share this view. | |

PRS Reit (LON:PRSR) (£617m) | SP -5% A non-binding proposal from Long Harbor for 115p per share was received and disclosed on 11th June. Talks are continuing. There are no other live offers (all others have been withdrawn). 19 interested parties entered into non-disclosure agreements and were provided access to the company’s data room. | PINK (Graham) [no section below] | |

Serica Energy (LON:SQZ) (£600m) | Restart process underway. Exp reach stable production “during July”. Net prod exp ~25kboepd. | AMBER/GREEN (Roland) [no section below] Today’s news is just about within previous guidance for “a restart around the end of June”, although full production is not expected until sometime during July. The company notes that significant work has been done that should improve reliability and support further production growth. No more maintenance is scheduled for Triton this year. Recent volatility has provided a useful reminder of the link between Serica’s share price and oil and gas prices. I continue to think a low P/E is appropriate, but at current levels I think the stock is likely to offer some value. | |

Polar Capital Holdings (LON:POLR) (£467m) | Y/E AUM -2% to £21.4bn, net flows +£0.1bn. Adj op profit +27% to £57m. Dividend held at 46p. | AMBER/GREEN (Graham) I’m tempted to upgrade this, but on balance I’ll leave it on AMBER/GREEN to reflect the uncertainty around net flows and the high valuation at which this trades versus others in the sector. It’s still one of my favourite fund managers! I wonder how long they can keep paying out 46p in dividends? | |

Porvair (LON:PRV) (£359m) | SP -4% | AMBER/GREEN (Roland) [no section below] | |

B.P. Marsh & Partners (LON:BPM) (£260m) | Acquires further 2% holding from founders at £275m equity value, BPM now has 39%. Also provides an RCF loan of up to £5m. Pantheon has grown into “a leading independent broker in the Lloyd’s and London insurance market”, and is on track to achieve adj. EBITDA of £18m in the current year. | GREEN (Graham) [no section below] As noted earlier this month, BPM has a war chest of funds to deploy and it continues to do so incrementally. A further 2% shareholding at an equity value of £275m presumably means a £2.75m investment. Combine that with the provision of a £5m RCF and BPM is using a decent chunk of its cash pile to back this company. I note that BPM has a 39% shareholding in Pantheon: this is significantly larger than all of its other investments, and it evidently doesn’t mind becoming even more concentrated in this investment. | |

AdvancedAdvT (LON:ADVT) (£225m) | Rev +105% to £43.3m, adj EBITDA ahead of exps at £11.3m. Outlook in line with exps. Proforma organic revenue growth of 17.8% and adjusted EBITDA growth of 90% on the four originally acquired businesses. Post period end there were two further acquisitions for £5m and £7m respectively. Performance explained by “better operational focus, the expansion of multiyear contracts”, and customers embracing digital transformation. | AMBER/GREEN (Graham) [no section below] This slightly odd collection of businesses appears to be doing fine. It raised expectations in February and has today posted very strong gains in profitability. The cash position at year-end is impressive at £88m (February, pre-acquisitions) and should still be high today. As I said last time, the valuation does not appear excessive when you strip out the cash balance. The £20m+ stake in M&C Saatchi (LON:SAA) doesn’t seem consistent with the rest of the portfolio but it’s part of the deal for those who wish to back Vin Murria’s business ventures. I’ll upgrade this to AMBER/GREEN given the momentum that’s evident in these numbers. | |

MS International (LON:MSI) (£220m) | Rev +7.2%, PBT +27.6% to £20.1m. Defence is now main focus, considering disposals. | GREEN (Roland) Today’s results show strong profit growth and operating leverage as increased activity levels improve margins. The company is considering disposing of its non-defence businesses but has not yet received any suitable offers. In the meantime, near-term growth may be held back by slower defence purchasing decisions, but the long-term outlook remains strong. There seems to be a risk that profit growth could slow this year, but my reading of the accounts suggests there’s enough work in progress to support a solid result. I remain positive on MSI as a long-term investment. | |

TT electronics (LON:TTG) (£198m) | SP -5.5% | AMBER (Roland) [no section below] Softness in North America and some deferred US orders seem to be the main concerns here; TT is still reporting strong performance in Europe in Aerospace/Defence. The book to bill ratio suggests the overall order book is flat so far in 2025. This seems broadly consistent with consensus forecasts for a flattish result this year, but isn’t overly encouraging. Mark was neutral on TT when he reviewed the 2024 results and I see no reason to change this view today. | |

Seeing Machines (LON:SEE) (£138m) | Collaboration to give SEE better access to sell Guardian Gen 3 to bus and truck OEMs in Europe. | ||

Victoria (LON:VCP) (£78m) | Replaces existing RCF due Feb 26. New facility is fully available w/out covenants. Refi continuing. | ||

hVIVO (LON:HVO) (£76m) | Positive results for Cidara CD388 field study, for which hVIVO provided services. | ||

Amcomri (LON:AMCO) (£73m) | Contract for UK developer of renewable facilities. Cav upgrade: FY25E EPS 5.4p (prev 5.2p). | ||

Roadside Real Estate (LON:ROAD) (£71m) | Op profit -72% to £1.1m. £48m sale agreement signed. Increasing stake in Meadow Partners JV. | (RH) Interim results to March 2025 being published in late June are a red flag (AIM deadline is 3 months). | |

Eagle Eye Solutions (LON:EYE) (£61m) | Digital promotions and loyalty solutions provider. Consideration €5.5m (5.7x EBITDA). | ||

Frenkel Topping (LON:FEN) (£61m) | Deadline for Harwood Private Equity to make firm offer extended to 5pm 28 July 2025. | ||

Zephyr Energy (LON:ZPHR) (£60m) | Adj EBITDA $10.9m, net loss $19.6m inc $14.5m Williston impairment. Production increased. | (RH) Results to Dec 2024 being published in late June are a red flag. | |

Metals One (LON:MET1) (£36m) | Zero revenue, net loss £1.6m. Material uncertainty due to financing requirements. | (RH) Results to Dec 2024 being published in late June are a red flag. | |

Cirata (LON:CRTA) (£35m) | Win with “top five Canadian bank” for Live Data Migrator product across multiple use cases. | ||

iomart (LON:IOM) (£33m) | New £115m RCF to June 27. No material change to trading since April TU. Results due late July. | ||

Team (LON:TEAM) (£24m) | Rev £5.8m, loss £1.8m. “On track to reach breakeven”. £2.16m cash in bank (March 2025). | (GN) Interim results to March 2025 being published in late June are a red flag (AIM deadline is 3 months). | |

Chariot (LON:CHAR) (£23m) | Loss $22m. Material uncertainty due to need for additional financing in a downside scenario. | (RH) Results to Dec 2024 being published in late June are a red flag. | |

River Global (LON:RVRG) (£16m) | Total loss £1.6m. “A” shares (asset mgmt) loss £2.8m. “B” shares (“Parmenion”) profit £1.2m. | ||

Safestay (LON:SSTY) (£16m) | 12-year lease to operate a 300-bed hostel in Naples. The hostel is set to open in August. | ||

Tiger Royalties and Investments (LON:TIR) (£15m) | Tiger Subnet, acquired May 2025 is emitting tokens at an annualised run rate of $2.56m. | (RH) Results to Dec 2024 being published in late June are a red flag. | |

Power Metal Resources (LON:POW) (£14m) | Rev £200k, £3.1m “other income”. To carry out desired activity levels, it needs to secure further funding. | (RH) Results to Dec 2024 being published in late June are a red flag. | |

CAP-XX (LON:CPX) (£12m) | Extends global availability of CAP-XX’s prismatic, cylindrical and hybrid supercapacitors. | ||

Angus Energy (LON:ANGS) (£12m) | Net revenue £11.3m from oil and gas production. Profit of £0.756m. Material uncertainty. | (GN) Interim results to March 2025 being published in late June are a red flag (AIM deadline is 3 months). | |

OptiBiotix Health (LON:OPTI) (£12m) | Rev +35% (£870k). Op loss £2.3m. “Strong cash position” of £739k. Very strong start to 2025. | (GN) Results to Dec 2024 being published in late June are a red flag. | |

Westminster (LON:WSG) (£10m) | Broadcast System to East African Parliament. Security screening system to worldwide broadcaster. | ||

Celadon Pharmaceuticals (LON:CEL) (£8m) | £1m debt raised at 10%. £20m convertible offered if CEL goes private. Shares to be suspended due to late results. | ||

Oxford Biodynamics (LON:OBD) (£7m) | Revenue £587k, op loss £5.9m. Cash £4.3m (March 2025). Material uncertainty. | (GN) Interim results to March 2025 being published in late June are a red flag (AIM deadline is 3 months). |

Graham's Section

Polar Capital Holdings (LON:POLR)

Up 3% to 473.9p (£481m) - Graham - AMBER/GREEN

In a very difficult year for fund managers, these results stand out:

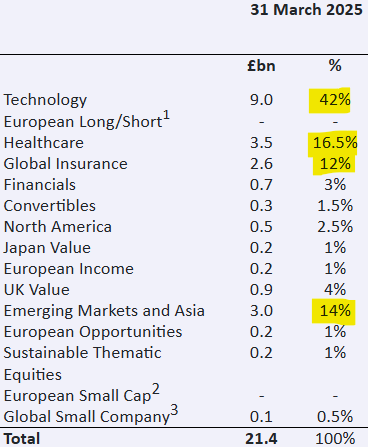

Closing AUM down only 2% to £21.4bn, while average AUM during the year rose 17% to £22.9bn.

Core operating profit +27% to ££56.7m. This is ahead of forecast at Equity Development (£53.9m), due to higher revenue margin and lower operating costs.

Including a £13.6m impairment charge, actual PBT falls 6% to £51.6m, behind forecasts due to the impairment.

Total dividend for the year unchanged at 46p. This is covered by adjusted EPS (53.5p) although not covered by actual EPS 36.6p.

CEO change: we learn today that Polar’s eight-year CEO is stepping down soon. Impressively, the company already has a CEO Designate: their Global Head of Distribution, who has been with the company for 20+ years. He will become CEO in September.

Talking about this set of results, the current CEO says:

"Polar Capital delivered a resilient outcome for the financial year despite industry headwinds for active equity managers. Our AuM ended at £21.4bn on 31 March 2025, just 2% lower than the £21.9bn a year prior. This decline was primarily due to negative market movements in the final quarter, as net flows over the year were broadly flat. Total AuM as at 20 June 2025 were £22.6bn with net outflows of £0.6bn from open ended funds and segregated mandates in the period 1 April to 20 June 2025.

“Broadly flat” net flows during such woeful conditions is a fantastic result, in my book.

Looking at the bigger picture, Polar’s strategy is called “growth with diversification” - which does make me a little nervous, as I think it’s important for fund managers to have a niche, and diversification can dilute this. Polar’s reputation in specific sectors - technology and healthcare come to mind - has served it well.

Here is the AUM split by strategy at year end, where I’ve highlighted everything over 10%:

Over the past year, Insurance and Emerging Markets and Asia have both grown, with particularly strong growth from EM and Asia.

In technology, I note that there were nearly £600m of net outflows from the Polar Capital Global Technology Fund, offset by £173m of net inflows into their AI Fund (of course!).

Geography of investors: important to note that Polar is not just serving UK investors. It has big ambitions in the US although this isn’t showing up in the AUM statistics yet. UK investors provide 63% of AUM with the main other contributors being Europe (23%) and Asia (7%).

Performance: three and five-year fund performance can’t be faulted:

At 31 May 2025, 84% of our UCITS fund AuM was in the top two quartiles versus Lipper peer groups over three years with 82% and 100% in the top two quartiles over five years and since inception respectively.

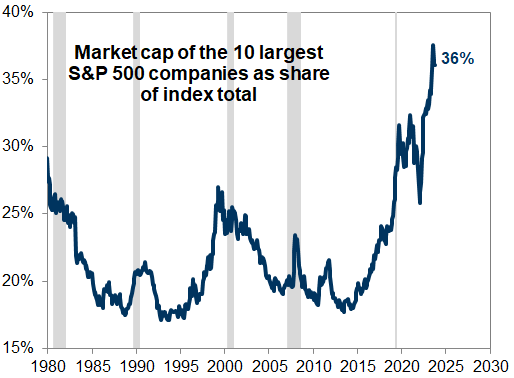

I see that the Technology Fund has underperformed during the year. Polar says that this is due to “two related structural factors, namely equity benchmark concentration, and the underperformance of smaller companies versus broad markets”.

As Polar points out, this is something that affects active managers in general.

Over the last several years, it has been possible to do well by buying Magnificent 7 stocks, or the automated indexes which hold them.

This is a very rough environment for active managers, who are unlikely to have overweight positions in stocks which are already very large components of their benchmark index. Their own fund concentration rules may prevent them from doing so!

A quick google search throws up this chart created by Goldman Sachs:

If or when the largest companies start underperforming, active managers should hopefully start to see their relative performance improve. If it doesn’t, they’ll have little excuse!

Outlook:

Although global economic and political uncertainty continues to weigh on financial markets, we believe that growing return dispersion and a renewed allocator focus on alpha generation will create a more favourable environment for active management. Polar Capital is well positioned to benefit from this shift, underpinned by our differentiated strategies, global distribution capabilities, and scalable operational platform.

“Growing return dispersion and a renewed allocator focus on alpha generation” are references to the factors mentioned above. In other words, attractive returns will be generated from stocks beyond just the mega-caps, and investors will again be interested to try to “beat the market”, i.e. to generate some alpha.

Graham’s view

As this is a watchlist stock for me, I’m glad to see that its share price has recovered strongly, like many others, since the 350p low it reached during the tariff sell-off.

It remains considerably more expensive than other fund manager stocks, but I continue to think that this is justified by its strong reputation and superior performance - definitely in terms of net flows but also I think in terms of overall fund performance.

Buying £1 of POLR stock gets £47 of AUM based on the latest figures. The corresponding figure for other managers is £90+.

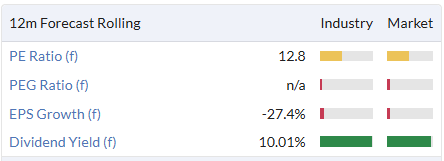

In P/E multiple terms, it’s expensive but not that expensive:

The high dividend yield is helping to support a strong ValueRank. The overall ValueRank is 91.

I was AMBER/GREEN on this last time due to a large EPS cut on lower AUM forecasts.

Equity Development have today increased their guidance for FY26 (e.g. they now forecast basic EPS of 38p, previously 33.8p), thanks to recent inflows. But they have also lowered guidance for the following years, as it balances out.

I’m tempted to upgrade this, but on balance I’ll leave it on AMBER/GREEN to reflect the uncertainty around net flows and the high valuation at which this trades versus others in the sector. It’s still one of my favourite fund managers! I wonder how long they can keep paying out 46p in dividends?

Roland's Section

MS International (LON:MSI)

Down 13% to 1,180p (£187m) - Final Results - Roland - GREEN

I am delighted to report that we have, once again, made excellent progress across all Group companies.

Today’s results from this owner-managed mini conglomerate showcase record profits for the year ended 30 April 2025, but have received a poor reception from the market.

To recap briefly, this unusual group owns a defence business that makes various kinds of military weapons. In addition, it also has separate operations producing fork lift arms, petrol station superstructures and corporate branding signage (mainly for UK petrol stations).

The issue seems to be that MSI’s defence business, which accounts for 70% of sales, is seeing increasingly long revenue recognition cycles. This could impact results for the current year, but management say they remain “very optimistic about the next two full financial years”.

I’ll return to this shortly, but in short I don’t see too much to worry about in today’s results. Let’s take a look.

FY25 results summary

Today’s headline numbers are refreshingly free of adjustments and show strong profit growth for the year to 30 April 2025:

Revenue up 7.2% to £117.5m

Operating profit up 26.9% to £18.7m

Pre-tax profit up 27.6% to £20.1m

Diluted earnings up 28.9% to 87.0p

I’ve included both operating profit and pre-tax profit above to highlight how MSI’s full-year result was boosted by £1.3m of interest income on the group’s £23.8m net cash position. We’re seeing this more and more at net cash companies – it’s a nice contrast to the growing interest costs incurred by some other firms.

Last year’s increased profit seems to have been driven by operating leverage. Staffing costs were broadly unchanged, allowing most of the increase in gross profit to drop straight down to operating profit.

This was reflected in MSI’s operating margin, which increased from 13.5% to 15.9% last year. That’s very nice to see, as is the increase in return on capital employed to 26.3% (FY24: 22.9%).

Divisional trading

Looking across the group’s operating segments presents more of a mixed picture:

Defence: operating profit up 36% to £17.7m;

Forgings (fork arms): operating profit down 50% to £573k

Petrol Station Superstructures: operating profit down 52% to £974k

Corporate Branding: operating loss reduced to £565k (FY24 loss of £1.4m)

Defence: management commentary highlights the strong progress in this business. Last year saw record export sales, driven by Naval weapons systems for the United States and the first deliveries of Naval weapons to the German Navy.

Forgings: fork arm sales were depressed in H1 due to overstocking by some manufacturers. Performance improved in H2. The company believes its US manufacturing operation is likely to become a stronger competitive advantage given the risk of tariffs and has the potential to expand into new markets.

Petrol Station Superstructures: this business is described as “the UK and East European market leader”. Trading is said to be strong in the UK:

I am pleased to report that we have reinforced our dominant market position by completing several substantial, complex new fuel and convenience hubs, including provision for electric vehicles, on major UK roads.

However, demand is said to be weaker in Eastern Europe due “inevitably” to the Ukraine war.

Corporate Branding: the UK business (also concentrated on petrol stations) performed well, but this was apparently cancelled out by continued losses in the Netherlands, where a more diverse range of customers are served. This unit has been restructured and is expected to return to profit this year.

Strategic review

Perhaps unsurprisingly, MS International has decided that defence should be the group’s main focus, going forward:

Given the growth of our Defence and Security division, and its medium and long term prospects, we have decided that this should become the Group's primary focus.

The MD of the defence unit has now joined the group’s board.

Chairman Michael Bell says MSI has tested the market’s interest in some of the group’s other operating units, with a view to possible disposals. Considerable interest was received, but the offers were “not at the levels” that would provide an attractive proposition for MSI shareholders.

We are not in a rush to sell these successful businesses as they continue to have considerable potential and make a significant contribution to the Group. I expect to be able to give shareholders more clarity later this year as and when relevant news is available.

Outlook: a weaker year?

MS International doesn’t appear to commission any broker forecasts and no consensus figures are available that I can find.

Shareholders have to make do with somewhat vague outlook commentary from Mr Bell. I think it’s this that has spooked the market today, perhaps along with a round of profit taking after an exceptional run up.

Here’s what the company has to say about the outlook for the year ahead for the core defence business, which I believe is where the issue may lie.

Defence: MSI has recently received a request for purchase from the US Navy for another year’s procurement of the company’s 30mm naval gun.

However, while the medium-term outlook for defence spending is positive, the company expects “government reviews and subsequent delayed decisions” to affect this year’s results.

One reason for this is that even when an order is received and MSI’s factories start work, revenue may not be recognised until certain delivery milestones are reached – potentially in the next financial period.

This kind of lumpiness is not uncommon in defence and other industrial businesses. Unfortunately MSI doesn’t publish the size of its order book, but it does hint at some shrinkage over the last year:

The Group order book at the April year end was marginally lower than the record figure reported last year. This is purely owing to delays in the placing of substantial defence equipment orders as both military requirements and governments have changed.

Delayed orders are of course not guaranteed. I note that inventories have fallen from £37.5m at HY25 to £30.7m at the end of the year. This is a reverse of the pattern seen last year (HY24: £16.9m, FY24: £25.3m), suggesting that order intake may have slowed.

Even so, the year-end inventory position is still higher than it was a year ago. Using an unchanged 34% gross margin suggests this inventory could convert into £46m of gross profit over the year, 15% ahead of the FY25 result of £40.0m.

Roland’s view

Today isn’t the first time that MSI has warned of the risk that long revenue recognition cycles for defence contracts could lead to lumpy revenue. Graham also commented on this issue in December.

For an investor who accepts the narrative of increasing defence spending, then I don’t see this issue as a concern.

Indeed, I’d argue that perhaps some of today’s fall is simply due to profit taking after a very strong run. MSI’s share price is still up eightfold in five years:

Today’s results leave the stock trading on a trailing P/E of 13 with a dividend yield of 2.0%. Adjusting for net cash reduces the P/E of around 11.5x.

In the absence of forecasts, investors are slightly in the dark about the year ahead. But this is a illiquid stock with a broad spread. I’d only really consider holding it as a longer-term investment. And from that perspective, I don’t see too much to worry about. I’m going to leave our positive view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.