Good morning! Thanks for all the positive feedback on yesterday's report. Today's Agenda is now complete.

1pm: wrapping up for now, thank you.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Halma (LON:HLMA) (£10.0bn) | TU | Adj. EBIT margin for FY March 2025 now expected above 21% (prev: “around 21%”). | |

IG group (LON:IGG) (£3.2bn) | Q3 TU | Trading rev +15% year-on-year, driven by higher rev/client. Confident of meeting exps. | GREEN (Graham holds) A pleasing update with revenue growth flowing from positive market conditions - there are plenty of reasons for customers to want to trade in this environment. Against that, customer numbers aren't growing much. A new buyback could be announced after the balance sheet is adjusted, leading to further share count reduction. |

Deliveroo (LON:ROO) (£1.82bn) | Preliminary Results | Robust top line, adj. EBITDA at top end of guidance. Outlook: high single digit growth. | |

Osb (LON:OSB) (£1.55bn) | Preliminary Results | Adj. PBT +4%, actual PBT +12% (£418m). £100m buyback. 2025: low single digit loan book growth. | GREEN (Graham) I tend to be positive on cheap lenders in this environment, and can find few reasons not to be positive on OSB at this valuation. It's going to buy back some shares very cheaply using only a fraction of post-tax profits, while also paying a well-covered dividend. |

Savills (LON:SVS) (£1.43bn) | Final Results | Rev +7%, adj.PBT +38% (£130m). 2025: most markets in recovery. Expects refinancing-driven activity. | |

Allianz Technology Trust (LON:ATT) (£1.40bn) | Final Results | NAV +35.6%, behind benchmark. Avoided excessive concentration risk. Discount narrowed to 8.6%. | |

Trainline (LON:TRN) (£1.39bn) | TU | FY Feb 2025: rev +12%. EBITDA margin: marginally ahead of guidance. New £75m buyback. | |

Volution (LON:FAN) (£1.03bn) | HY Results | Rev +4% organic. PBT -11.3% due to non-underlying costs. Outlook: ahead of consensus. | AMBER/GREEN (Graham) [no section below] The SP is up 30% since we looked at it last year. The company has "good momentum" going into H2 with structural growth drivers that include tightening building regs, demand for quality indoor air, and the need to reduce energy costs. With earnings for FY July 2025 trending ahead of consensus (30.4p), I think the current-year PER is likely to be c. 18x. Organic revenue growth is modest at 4%, and I note a large gap between statutory and adjusted earnings, due to acquisition activity. Acquisitions have resulted in net debt of nearly £190m and a higher leverage multiple of 1.5x, and the balance sheet now has deeply negative tangible equity. I think a more cautious stance may be justified, as risk levels have increased. |

Bridgepoint (LON:BPT) (£2.86b) | Final Results | Pro forma underlying income +52% (£404m). PBT £93m. Upgraded fundraising guidance. | |

Glenveagh Properties (LON:GLV) (£676m) | Final Results | Completions +77%, rev +43% (€869m). ROE 14.2%. Outlook: “exceptionally strong”. | |

Alfa Financial Software Holdings (LON:ALFA) (£660m) | Full Year Results | Rev +8%, PBT +15%. Outlook: record level of TCV (total contract value), expects mid-teens growth. | |

C&C (LON:CCR) (£599m) | TU | PW. FY26: expect continued consumer uncertainty. Earnings to be marginally ahead of FY25. | |

Empiric Student Property (LON:ESP) (£556m) | Preliminary Results | EPS +5%. NTA per share 120.7p (share price: 83p). Outlook: like-for-like rental growth 5%. | |

Care REIT (LON:CRT) (£448m) | Annual Results | Contracted annual rent roll +5.3% (£51.4m). Cannot raise more capital to achieve potential. | PINK (108p offer) |

DFS Furniture (LON:DFS) (£303m) | Interim Results | Underlying PBT doubles to £17m. Margin improvements. Expects to outperform consensus exps. | RED (Mark)[No section below] |

Restore (LON:RST) (£290m) | FY Results & Acquisition | Rev -1%, adj. PBT +14%. Trading since the start of the year has been good. £22m acquisition. | AMBER/GREEN (Mark) [No section below] |

Gulf Marine Services (LON:GMS) (£176m) | Contract | 2 vessels, 3-yr contract extensions in the Middle East at enhanced rates. | GREEN (Mark) |

Cab Payments Holdings (LON:CABP) (£136m) | FY 24 Results | Volumes +7%. £16m adj. PAT, in line. Executing well against 2025 plan, expecting income growth. | AMBER (Mark) [No section below] |

Secure Trust Bank (LON:STB) (£79m) | Final Results | SP up 19% to 500p They have generated an adj. PBT of £39m in 2024. After both taxes and exceptional items, profit for the year is nearly £20m. Profits grew before impairments. Confident in medium-term targets. | AMBER/GREEN (Graham) [no section below] |

Van Elle Holdings (LON:VANL) (£42m) | TU | PW - u/l PBT for 25H2 to be similar H1 due to delays in Canada & UK Building Safety Act | BLACK (AMBER/GREEN) (Mark - I hold) |

essensys (LON:ESYS) (£24m) | Half year Results | Rev -11%, +ve EBITDA, ARR -16%, EPS -3p, Net cash £2.2m (£3.5m) | AMBER/RED (Mark) |

Gem Diamonds (LON:GEMD) (£13m) | FY Results | Rev +9.9% to $154.2m, Att. Profit £2.9m (FY23 $2.1m loss). Net debt $7.3m (FY23 $21.3m). | AMBER/RED (Mark) |

Graham's Section

IG group (LON:IGG)

Up 4% to 966p (£3.4bn) - Third Quarter Revenue Update - Graham - GREEN

At the time of publication, Graham has a long position in IGG.

The punchline from today’s update is that IGG “remains confident of meeting FY25 consensus” when it comes to revenue and adjusted PBT.

The company hopefully includes in the RNS that revenue consensus is £1,027 million and adjusted PBT consensus is £494m.

As for progress in Q3, we learn the following:

Revenue +12% on prior year to £268m, driven by a 15% increase in trading revenue and offset by a 7% reduction in net interest income.

The trading revenue benefited from “stronger trading conditions which increased revenue per client”. Active clients grew by just 2% year-on-year to 328,0900.

Net interest income fell due to lower interest rates and stable client money balances (£3.8 billion as of Feb 2025).

There was some nice growth at US subsidiary tastytrade which saw Q3 trading revenue up 30% year-on-year to $50.9m (reported in GBP as £40.8m).

Freetrade acquisition: we discussed this in January. IG informs us that Freetrade has continued to trade well, and in line with expectations. The takeover is expected to close in April 2025.

Share buyback: there is an ongoing £200m buyback to be completed in FY May 2025. IG are now seeking to adjust their balance sheet - to reduce their “premium account” and “merger reserve” - so that more of their equity will be classified as retained earnings. This would give them more flexibility, and could lead to more capital being returned to shareholders.

Checking the interim balance sheet I see that there was £125m in “share capital and share premium” and £590m in “merger reserve”. So that’s a lot of capital that could potentially be unlocked.

I also note from the interim report that they had “£658m of headroom over the Group minimum regulatory capital requirement”.

So I don’t think it’s a stretch to envisage hundreds of millions of pounds being unlocked for more dividends and buybacks - or it could equally be used for M&A/investment opportunities.

Graham’s view

I’m a broken record here and when it comes to this sector as a whole. I am now consistently GREEN on IGG, PLUS and CMCX. IGG has been in my personal portfolio for years, and was in other portfolios I managed for years prior to that.

Stockopedia’s calculations agree with my assessment, viewing it as a Super Stock. It’s not every day that you see a QualityRank of 100:

Usually with a high QualityRank, there is a catch such as low growth. IG’s growth doesn’t happen in a straight line - it ebbs and flows with trading activity in the financial markets. But the overall trajectory is clear enough.

It’s a market leader with a trusted and broadly recognised brand, and yet it trades at a modest earnings multiple:

The cherry on top is that the share count has been reducing as excess cash flow has been directed to buybacks.

I’m still quite sceptical of the $1 billion tastytrade acquisition in 2021, which resulted in the creation of 61 million new shares.

However, buybacks in the last three years have taken the share count back below where it was prior to the acquisition, and the share count looks set to fall further still. Meanwhile, tastytrade has been growing well.

IG is currently 13% of my personal portfolio.

In the interest of balance, some risks faced by the company include:

Competition from aggressive rivals (when it comes to their marketing) such as CFD broker Plus500 (LON:PLUS).

A fresh round of regulatory intervention is always a possibility.

Quieter market conditions will produce a revenue decline, especially if there has been no substantial growth in customer numbers.

The expansion into a variety of new product categories brings potential risks.

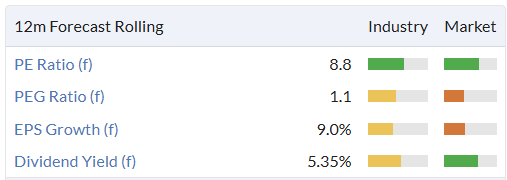

Osb (LON:OSB)

Up 2% to 429p (£1.59bn) - Preliminary Results - Graham - GREEN

OSB GROUP PLC (OSBG or the Group), the specialist lending and retail savings group, announces today its results for the year ended 31 December 2024.

OSB is “focused on carefully selected sub-segments of the mortgage market such as Buy to Let, Residential, complex commercial and semi-commercial, development finance, bridging and asset finance”.

They are “predominantly funded by retail deposits sourced through our Kent Reliance and Charter Savings Bank franchises”.

Some highlights from today’s results:

Underlying PBT +4% to £442m

Statutory PBT +12% to £418m

Most KPIs and key numbers have moved negatively, for example:

The loan book fell slightly due to a securitisation in December.

The net interest margin also reduced slightly due to lower mortgage spreads over the Sterling interest rate benchmark.

And the company's cost to income ratio rose due to “continued investment in the transformation programme, redundancy costs and the new Bank of England levy”.

More positively, the loan loss ratios (a measure of the impairment charge as a percentage of total loans) fell dramatically, due to higher house price expectations.

CET1 ratio: this key measure of safety has increased slightly to 16.1%, which I think is slightly higher than the banking sector as a whole.

Share buyback: there will be a new £100m buyback over the next twelve months. I can’t argue against this given the CET1 ratio. It’s only a fraction of statutory PBT and it will lead to share purchases at a very cheap earnings multiple:

CEO comment notes that 2024 was the second year of a five-year transformation programme.

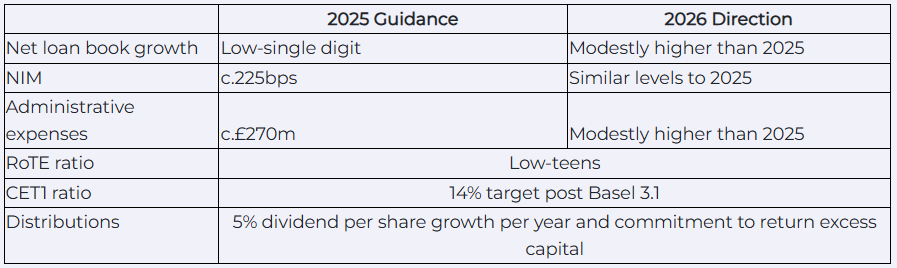

Outlook

I appreciate the clear guidance. There is little growth baked into forecasts but I guess at a PER of less than 6x this is to be expected!

The company also provides a list of medium-term aspirations for 2027-2029 which I recommend checking out. The main point for me is that the company is targeting RoTE (return on tangible equity) of mid-teens, rather than the low-teens expected in 2025-2026.

Graham’s view

I don’t study this one frequently but based on a review this morning I see little to dislike.

The results for this year are pretty clean, without excessive adjustments.

The balance sheet has shareholders’ funds (i.e. net assets) of £2.2 billion, almost fully tangible. It’s no surprise in this environment that the market cap would offer a substantial discount to that figure.

At this sort of valuation, I would personally be happy with a RoTE of over 10%, let alone in the low-teens or mid-teens. So I don’t think the company even needs to hit its targets to justify the current share price.

I’ll stick my neck out and give this a GREEN.

Out of £28 billion in liabilities, nearly £24bn in is the form of retail depositors. Perhaps that is one niggle worth mentioning - a very large reliance on deposit funding.

And from a macro point of view, any major problems in the buy-to-let sector will be felt at OSB.

Mark's Section

There seems to be an increasing focus on pensions recently, with Norcros (LON:NXR) announcing the outcome to their 2024 triennial review this morning:

The 1 April 2024 valuation has now been agreed, subject to completion of the formal documentation, with the prior actuarial deficit from April 2021 of £36.0m being updated to an actuarial deficit of £11.7m on a technical provision basis, representing a funding level of 96%.

This is good news, but it is worth noting that this doesn’t have any impact on the short-term contributions:

The schedule of cash contributions to June 2027 of £3.8m per annum (indexed by CPI) that was agreed in the 2021 valuation, will continue.

The reduction is after June 2027 and will be paid into escrow. This is because once cash contributions are made into a scheme, it is almost impossible to get a surplus, should it arise, back out. Whether these more positive conditions continue really depends on interest rates. If these fall, then deficits may rise again, which is why many companies are keen to get a buyout, where possible. A buyout also removes the need for the company to pay the scheme administration fees, which can be significant and last as long as the scheme does. Here, Norcros say:

Cash contributions post June 2027 are expected to be less than c.£1m per annum and will only be paid to the extent that asset performance or any escrow funds do not cover ongoing scheme administration fees.

Investors need to be careful when analysing companies with deficits. These often don’t appear on the balance sheet due to more favourable assumptions under IFRS accounting standards. It is the more cautious triennial valuation that determines the cash contributions, and investors need to look at the cash flow statement to understand the real situation for shareholders (for whom that cash goes permanently out of their pockets and into the pension scheme).

Many companies like to exclude pension administration charges from the adjusted results, despite these being cash costs borne by the company and ongoing in nature. For example, Reach (LON:RCH) in the last annual results adjusted out £5.5m of admin and past-service costs:

Reach have also had what appears to be an ongoing dispute with their pension trustee. With the last set of FY results, they announced that:

After a number of years, the 2019 and 2022 Pension Triennial valuations are concluded. There is an agreed pathway to fully funding the schemes and from 2028 pension commitments are expected to reduce by c.£40m(1)

However, cash contributions to the scheme before 2028 actually went up, and there will be a further assessment before 2028. This week, The Times, reports that

The Pensions Regulator (TPR) revealed that it had to resort to threats of enforcement action, which includes fines and criminal prosecution powers, to force Reach plc, which now owns the Mirror, to lift its payments to the scheme to help fill the shortfall in its funding position.

This is what the Pension Regulator said:

Through negotiation, we were able to help facilitate the trustee and company to reach a mutually acceptable solution without the formal use of our powers. The final agreement included making significant improvements in the deficit recovery schedule with the financial support of the wider group, and improving an existing dividend sharing agreement whereby amounts above a certain percentage increase in dividend distributions will result in a sum matching the excess dividend increase being made to the scheme.

Our intervention, through working with Reach Plc and the trustee, resulted in the scheme receiving an additional £5.1 million per annum from the company, backdated to the start of 2023, which will be paid every year until the end of January 2028. The scheme is expected to be fully funded on its prudent technical provisions basis by January 2028.

Although they didn’t have to use their legal powers, the regulator has real teeth and has forced Reach to pay an extra £25.5m into the pension fund that the company appeared reluctant to do. Investors should be very wary of any delays in agreeing on triennial recovery payments. Such delays are likely to prove bad news for shareholder returns.

Graham adds: there was an interesting announcement from the government in January which expressed an intention to unlock the surplus funds in defined benefit pension schemes. In particular, pension trustees could agree to share a portion of their surplus with sponsoring employers, to enable the employer to reinvest in their core business. The employer will have no access to the surplus without the consent of the trustees, but it seems increasingly likely that an element of the surplus funds at some schemes could make their way back to them. The ownership of pension surpluses is a complex legal topic! Perhaps it will be adjusted back slightly in favour of the employer.

Van Elle Holdings (LON:VANL)

Down 18% to 31.5p - Trading Update - Mark (I hold) - BLACK AMBER/GREEN

It is a profits warning from this ground engineering contractor:

…the Board now expects underlying profit before tax for the second half of FY25 to be similar to the first half.

Their broker Zeus reveals what this means:

Zeus forecast revenue for FY25 is reduced by 6.1% to £137.3m and underlying PBT is reduced by 32.6% to £4.0m, implying an even 50:50 split between H1 and H2 2025 PBT.

The blame is put on two areas. Firstly, delays caused by Building Safety Act approvals in their Rock & alluvium subsiduary. Although they say that overall UK operations are only slightly below expectations. So it seems the bulk of the issues appear to be with delays in Canada:

Van Elle Canada Inc. has experienced further delays as a strategic supply partner to the major infrastructure upgrade programme for the Toronto rail network. As a consequence of these delays, the division's trading performance will now be weaker than initially anticipated. Van Elle has developed a solid track record locally in Canada and has secured several key frameworks throughout FY24 and FY25 which have created several attractive medium-term opportunities. With the near-term uncertainty around the timing of key investment programmes, the Board is reviewing its strategic options with respect to its operations in Canada.

The move into Canada is sounding increasingly like a mistake. It has incurred significant start-up costs and appears to have not yet delivered meaningful profitability. They now appear to be considering selling or exiting the business, which would be embarrassing.

The downgrades Zeus makes for future years are far less severe:

Due to the current challenging market conditions, we reduce FY26 revenue by 5% to £153.3m and underlying PBT by 7.5% to £7.0m. FY27 PBT is also reduced by 4.0% to £9.2m. FY27 estimates still show Van Elle hitting its medium-term financial objectives of 5-10% revenue growth, 6-7% underlying EBIT margin and 15-20% ROCE.

This puts them on an FY27 P/E of around 5 following today’s fall, which makes them cheap if you believe the forecasts. However, after this warning, it will take some time to build confidence that management have a handle on things. Perhaps the biggest embarrassment is that the much larger geotechnical groundworker, Keller, have been continuously upgrading forecasts during this period:

This difference in performance is why Keller trade on a P/TBV of 2 compared to around 0.6 for Van Elle. The company is taking steps to improve the productivity of its assets, but this appears to be taking the form of selling off under-utilised equipment rather than improving utilisation:

In light of the trading pressures the Group is facing, there is an acute focus on careful working capital management and aligning its cost base to drive operating efficiencies. Additionally, the Group has disposed of certain non-core assets in support of a robust balance sheet and its objective of improving ROCE.

Given the recent performance, shareholders (of which I am one) may prefer that they sell the whole business to someone who can better use the assets. The shouts for this from the more activist shareholders on the register may be getting louder today.

Mark’s View

Paul, Graham, Roland and I have all rated this GREEN over the last year. However, Roland rightly expressed concerns over the H2-weighting implied by the H1 results. Despite the low forward rating and discount to TBV, it feels like this profits warning should downgrade this to AMBER/GREEN. It may well prove to be a blip caused by understandable delays, but the gap between trading here and the likes of Keller opens the possibility that the issues are more serious.

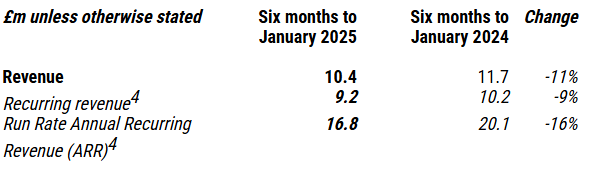

essensys (LON:ESYS)

Down 2% to 36p - HY Results - Mark - AMBER/RED

The main headline at this flexible workplace technology provider is that they have returned to positive EBITDA. However, the other metrics are going the wrong way:

The reason given is the previously flagged downsizing of a large strategic customer. The company would prefer we ignore this in comparisons, but I don’t see why this should be treated any differently. Like many companies, their revenue appears to be recurring, until it isn’t.

The EBITDA improvement comes from cost-cutting:

Operating expenses decreased to £5.3m, a reduction of £2.2m (29%) compared to the prior year. This reduction was driven by the Group reorganisation, which began at the end of H1 23 and completed in H1 24 and reflects the strong emphasis on cost management and operational simplification in the business.

However, it is worth noting that EBITDA is not a useful measure of performance for a company that capitalises intangibles:

The Group continues to invest in product development in the UK. Where such work is expected to result in future revenue, costs incurred that meet the definition of software development in accordance with IAS38, Intangible Assets, are capitalised in the statement of financial position. During the half year, the Group capitalised £1.1m in respect of software development (H1 24: £1.1m), as it continued to invest in its products.

Capitalisation is running behind amortisation, which helps cash flow, but at a time when a company is cutting costs, it may represent them putting a brake on development to conserve cash. The balance sheet doesn’t look too bad for this sort of company, although there is no real tangible asset backing. Cash burn during the half was around £1m. They claim their cash is enough to see them through to cash flow breakeven:

Cash at the half year end was £2.2m (H1 24: £3.5m). Cash outflows in H1 25 amounted to £0.9m, compared to £4.4m in H1 24. This was supported by tax credits in respect of R&D activities received in H1 25 of £0.9m. Management expect cash burn to reduce further in H2 25, as we optimise our Cloud costs. The Group continues to maintain sufficient cash reserves to fund its working capital requirements and its return to cash generating operations. Excluding leases, the Group has no debt and has an existing undrawn £2m loan facility committed until 31 July 2025.

But this would seem to assume further cost-cutting. It may be that the management changes also announced today could lead to a change of strategic direction and improved trading:

Chief Executive Officer succession

· As announced separately today and as part of a planned succession, Mark Furness has decided to retire as Chief Executive Officer, after founding essensys in 2006 and leading the business since launch

· Mark will remain on the Board of the Company and will move to a new role as a non-executive director of essensys with effect from 1 May 2025

· James Lowery, Chief Operating Officer, will take over as Chief Executive Officer on 1 May 2025

However, given this is an internal appointment, it seems that muddling along will most likely be the future course.

Mark’s view

It seems as though the company finds itself between a rock and a hard place. They have been unable to grow revenue, which is forecast to be at similar levels to 2019 in the future:

Cost cutting has stemmed the cash burn but perhaps at the expense of being able to invest in sales or product development. This means that flat revenue and continued small accounting losses appears to be the most likely future for the business. As such a £24m market cap seems very hard to justify. AMBER/RED.

Gulf Marine Services (LON:GMS)

Up 6% to 17.5p - Contract - Mark - GREEN

A short update from this marine vessel operator to say that two of its vessels have had 3-yr contract extensions. The most important part is that these were “secured at enhanced rates”. However, it would have been nice to get more details on how enhanced these were.

The issue is that the company is highly cash-generative at the moment because they have a high depreciation charge but are not investing capital into growing their fleet. With a Return on Assets of only around 6%, we are still at the point of the cycle where investing in new ships looks uneconomic based on current rates. So, the strategy of running the existing fleet and using the cash to pay down debt looks the right one. However, at some point, management will need to make a decision - are they going to invest again into growing the fleet, or are they just going to run the existing fleet until the ships eventually become uneconomic to operate? These are relatively long-life assets, so you feel that shareholders would probably prefer the latter, especially if the cash generation ends up as dividends instead of debt reduction. However, management teams don’t tend to like running declining businesses, and the temptation must be to re-invest that capital into growing the fleet at some point in the future. Shipping is a highly cyclical industry, and management teams have a tendency to invest at exactly the wrong point in the cycle, which is how Gulf Marine Services originally ended up with a large new fleet of ships funded by debt just as rates collapsed.

Mark’s view

Roland rated this GREEN following their recent re-financing, and with enhanced (although unquantified) rates agreed today, I see little reason to change that rating. The low P/E and discount to TBV mean that there is potential value here as rates continue to strengthen. However, what stops me from owning the shares is the uncertainty over whether rates will ever get back to levels that make the assets productive enough to justify a premium to TBV and, if they do, whether management will suddenly discover a desire to add to the fleet rather than pay down debt and make returns to shareholders.

Gem Diamonds (LON:GEMD)

Flat at 9.6p - FY Results - Mark - AMBER/RED

It seems a modest recovery here with weaker production offset by higher value per carat received:

· Carats recovered of 105 012 (109 656 carats in 2023)

· Waste tonnes mined of 5.4 million tonnes (8.8 million tonnes in 2023)

· Ore treated of 5.0 million tonnes (5.0 million tonnes in 2023)

· Average value of US$1 390 per carat achieved (US$1 334 in 2023)

· The highest dollar per carat achieved for a white rough diamond during the year was US$41 007 per carat

This has always been a business highly dependent on a few large, high-value diamonds, which makes results quite variable. However, this year, this has produced profits and a reduction in debt:

· Revenue of US$154.2 million (US$140.3 million in 2023)

· Underlying EBITDA of US$29.7 million (US$15.2 million in 2023)

· Profit for the year of US$8.1 million (US$1.6 million in 2023)

· Attributable profit of US$2.9 million (loss of US$2.1 million in 2023)

· Earnings per share of 2.1 US cents (loss per share of 1.5 US cents in 2023)

· Net debt of US$7.3 million as at 31 December 2024 (2023: net debt of US$21.3 million)

The difference between profit and attributable profit is because, as well as a royalty expense, the government of Lesotho holds a minority interest:

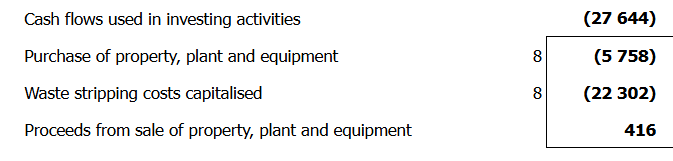

The other complexity is that they capitilise and amortise their waste-stripping:

In this case, the debt reduction is almost entirely due to reduced waste stripping. This may be due to the decision to use steeper slopes, and may be a permanent shift. However, it may also indicate the company is taking short-term actions at the expense of long-term ones.

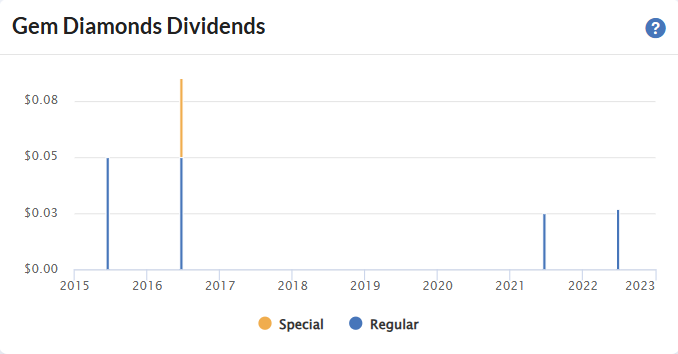

The fundamental problem with this business, is that it has been unable to make consistent returns to shareholders:

This doesn’t appear to be about to change in the short term either:

The Board is not proposing a dividend based on the 2024 financial results due to the volatility in the current macro-economic outlook, the expected impact thereof on the diamond market, the Group's available cash resources, and the medium-term business outlook with the implementation of Letšeng's updated mine plan, which will result in higher-value Satellite Pipe ore only being accessible from the end of 2029.

Mark’s view

The few dividends it has been able to pay in the good years don’t make up for the bad. In the meantime, it is running a large mining operation almost entirely for the benefit of other stakeholders. That may well be the right thing to do, but it doesn’t make it a business I want to be an equity holder in, especially as mining assets tend to have limited operational lives. AMBER/RED.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.