Good morning!

The FTSE is set to open unchanged at 10,560 this morning.

The S&P 500 closed at an all-time high yesterday evening, and futures markets expect further small gains when US markets open later today.

Iran: The US and Iran are considering a two-week extension of the current ceasefire, which expires next Wednesday.

Energy prices:

Brent crude is treading water at $95 (it was $70.50 just prior to the war).

UK natural gas futures have dropped back very significantly from their high of about 175p/therm in mid-March, now at 103.5p/therm.

UK GDP: There is a positive economic surprise this morning with UK GDP growing by 0.5% in February, according to figures just released. Expectations had been for growth of just 0.1%. However, 0.5% is still a very sluggish rate of growth - and it’s the rate of growth before the war against Iran kicked off.

Wrapping it up there, will hopefully get a chance to do some backlog sections tomorrow! Cheers. Spreadsheet accompanying this report: link.

Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Tesco (LON:TSCO) (£30bn | SR73) | Sales +4.3% at constant rates. Adjusted operating profit +0.6% at constant rates (to £3,152m). Statutory PBT +8.5% (to £2,403m). “Reflecting the increased uncertainty caused by the conflict in the Middle East… adjusted operating profit of between £3.0bn and £3.3bn for the 2026/27 financial year.” Upgrades medium-term free cash flow guidance to £1.5 - £2bn (from £1.4 - £1.8bn). | ||

Rentokil Initial (LON:RTO) (£12.8bn | SR57) | Organic revenue growth 3.4%. “We have made a good start to the year in a seasonally quieter first quarter…the progress we report today gives us confidence in delivering a full year performance in line with market expectations.” | ||

Schroders (LON:SDR) (£9.33bn | SR78) | Net flows minus £2.5bn. AUM falls from £605.7bn to £599.4bn. | PINK (expected to combine with Nuveen). | |

Intertek (LON:ITRK) (£6.63bn | SR44) | Buys the assets of a solar PV lab from Mitsui Chemicals India. Price not given. The lab “provides comprehensive solar PV testing and certification services to recognised national and global standards, enabling efficient market access for both Indian and international companies.” | ||

Londonmetric Property (LON:LMP) (£4.48bn | SR70) | FY March 2026: c.16% increase in net rental income to over £450 million, 98% occupancy, average lease length 17 years, 4.2% like-for-like income growth. | AMBER/GREEN = Graham [no section below] LMP is considered to be in a takeover situation, as it has recently expressed interest in buying most of the assets of Picton Property Income (LON:PCTN) (market cap c. £400m). If agreed, LMP would probably take Picton’s logistics assets, in exchange for LMP shares. Today’s trading update is encouraging on every count: high occupancy, reasonable like-for-like income growth, and rent reviews delivering a 19% uplift. They highlight a 38% uplift in logistics but I’m not sure how much to read into this - perhaps it’s just a few very old leases that needed to catch up to current commercial reality? Big picture: the company has been making disposals “in line with book value”, and the current share price (197.3p) is only a short distance from net tangible assets per share (last reported at 199.5p). I’m therefore inclined to believe this stock is trading near fair value - but with strong operational metrics, and interesting expansion plans, AMBER/GREEN looks fair to me. | |

Entain (LON:ENT) (£3.57bn | SR21) | Confirms its guidance of 5-7% online NGR growth on a constant currency basis, and remains comfortable with market expectations for FY26 underlying EBITDA. Reiterates confidence in generating at least £500m of annual adjusted cashflow in 2028. | ||

easyJet (LON:EZJ) (£3.00bn | SR48) | H1 “broadly in line” with expectations. Middle East conflict led to c. £25m of incremental fuel costs. “...the booking curve has shortened in recent weeks, resulting in lower than normal forward visibility.” Net cash £434m. | ||

MITIE (LON:MTO) (£2.44bn | SR79) | FY March 2026 revenue up c. 11%, organic growth c. 6%. Adjusted operating profit up c. 12% to at least £260m. “Our strong order book, recent contract wins and bidding pipeline underpin the growing momentum in the business, and we remain confident of delivering our FY27 targets.” | ||

Morgan Sindall (LON:MGNS) (£2.19bn | SR86) | Full year results for 2026 will be significantly ahead of previous expectations. There is increased visibility for the remainder of the year from the Construction and Fit Out divisions. The Construction operating margin is now expected to be at the top end of the medium-term target range (3.0 - 3.5%). | ||

Dunelm (LON:DNLM) (£1.72bn | SR66) | Q3 sales +2.1%, year-to-date sales +3.1%. FY26 PBT is currently expected to be towards the lower end of consensus expectations (range of £210m to £217m, average £213m). | BLACK (still within the range of expectations, but at the lower end)/AMBER/GREEN (Mark) | |

Ashmore (LON:ASHM) (£1.57bn | SR72) | Q3 (to March): net outflows $0.9bn, AUM declines 3% to $50.7bn. “Geopolitical events interrupted some of the macro tailwinds supporting emerging markets, but the reaction across most asset classes has so far been manageable and with limited price dislocations.” | GREEN = (Graham) [no section below] After net inflows of $2.3 billion in H1, this is an unfortunate reversal. Positive momentum “was interrupted by the broadening of the conflict in the Middle East at the end of February.” Fund investor caution is understandable, given the situation in the Middle East, but Ashmore funds primarily invest in Asia and Latin America, so their exposure to spillover effects from the US-Iran conflict should be limited. I’m going to treat this quarter as a bump in the road, and leave our positive stance unchanged here. | |

Ninety One (LON:N91) (£1.49bn | SR90) | AUM £171.8 billion, up £12 billion from December 2025. Took on £16.5 billion of AUM from Sanlam Investment Management on 1st February. | ||

Hays (LON:HAS) (£499m | SR35) | Group fees down 8% year-on-year. Temp down 6%, Permanent down 12%. Net debt £15m reflects seasonal cash flows, timing of month end payments. “Although near term market conditions are likely to remain challenging , we currently expect FY26 pre-exceptional operating profit will be in line with consensus”. | ||

Beauty Tech (LON:TBTG) (£338m | SR-) | Revenue +39.4%, adjusted PBT +98% (£29.5m). Statutory PBT £15.2m. “Very encouraging start to Q1 FY26… Year-on-year revenue growth expected to continue into FY26, with FY26 revenue in line with current market expectations but due to stronger margins, it is anticipated that profit will be ahead of expectations.” | ||

Central Asia Metals (LON:CAML) (£276m | SR87) | Production guidance for FY2026 reiterated. 2026 exploration in Kazakhstan to include ~2,000 metres at Yuzhnoe and ~2,000 metres at Otyar in the Chingiz-Tarbagatay belt. Results expected in Q3 2026 from Aberdeen Minerals' Phase 3 drilling to test southwestern target zone at Arthrath. | AMBER/GREEN = (Mark) | |

Norcros (LON:NXR) (£260m | SR93) | Group Revenue +10.3% to £393m (+0.7% LFL), U/L PBT +6.9% to £40.4m, in line with market expectations. Net debt excl. Leases £67m (FY25: £36.8m). CFO to leave within the next 12 months. | ||

Sovereign Metals (LON:SVML) (£238m | SR18) | DFS shows: Steady State annual EBITDA US$476M and Free Cash Flow (pre-tax, unlevered) US$452M; Total revenue of US$16.2Bn over 25-year initial mine life, with potential for mine life extensions; Pre-tax NPV8 of US$2.2 billion, NPV/Capex ratio of 3.0x - capital expenditure to first production of US$727 million | ||

Cab Payments Holdings (LON:CABP) (£216m | SR46) | Final price of 110 pence per share in cash. | PINK | |

Avingtrans (LON:AVG) (£191m | SR77) | The Advanced Engineering Systems division has secured orders worth more than £10m for nuclear applications. | AMBER/GREEN = (Graham) [no section below] This contract news provides “further solid support to existing forecast expectations”, according to Cavendish. I’m not entirely sure how this justifies such a positive share price reaction today, but I can see that there’s a strong narrative at work here. Geopolitical instability, combined with surging electricity demand from data centres, creates the conditions where the nuclear sector could be busy, with Avingrants being perfectly positioned to benefit. On top of that, the financial trajectory here is genuinely very positive, with high CAGR in both revenues and profits, both historically and in terms of forward projections. Stockopedia categorises it as a High Flyer, which seems appropriate. We’ve been AMBER/GREEN here; if I was closer to the story I might upgrade it to fully positive, but I’ll cautiously leave our stance unchanged for now. | |

Animalcare (LON:ANCR) (£170m | SR36) | 336 pence in cash for each Animalcare Share, 36% premium to last night’s close. | PINK (Graham) | |

Savannah Resources (LON:SAV) (£136m | SR36) | After raising £14.6m (gross), SAV ended 2025 with “£17.2 million of cash in bank and a further £5.0 million ringfenced in long-term bank deposits”. Loss from continuing operations £4m. Company is pre-revenue. | ||

Mercia Asset Management (LON:MERC) (£122m | SR49) | Now expects its EBITDA for FY26 to be materially ahead of current market expectations. Attracted new funds of £200m, with zero redemptions. Closing cash position c. £26m. | GREEN = (Graham) Excellent news with Mercia’s asset management business continuing to develop promisingly. I treat this as a deep value play but it may need the market to start believing in its operating business before the shares can re-rate. | |

Audioboom (LON:BOOM) (£114m | SR36) | Final Results & Q1 Trading Update & Update on Strategic Review | FY Revenue +10% to $80.4m, PBT +10% to $1.0m. EPS Flat at 5.2c. Q1 Revenue +30% to $22.5m, Q1 Adj. EBITDA +118% to $1.4m. Cash $5.5m. | PINK |

Alumasc (LON:ALU) (£93.9m | SR48) | Overall performance was slightly below expectations, Q3 FY25/26 revenues were 2% ahead of the prior year. Cavendish reduces FY26 Adj. EPS by 24% to 22.2p, and FY27 by 20% to 26.2p. | BLACK (AMBER/RED) ↓ (Mark) | |

Premier Miton (LON:PMI) (£72.3m | SR73) | Q2 AuM -6% to £8.99bn, Outflows of £443m (4.6% of AuM), -£124m market performance (-1.3%). Further cost-savings implemented, saving £2.5m annualised from September. Cash £24.6m (30 Sep 25: £31.3m) Cavendish reduces FY26 Adj. EPS by 24% to 3.4p, and DPS by 33% to 4.0p. | BLACK (AMBER/RED) ↓ (Mark) | |

IG Design (LON:IGR) (£53.1m | SR61) | Appointment of Gerald Kuehr as Chief Executive Officer Designate. Starts on 1st July. Previously a company advisor. | ||

Creo Medical (LON:CREO) (£48.5m | SR60) | Entered into an agreement to sell its manufacturing operations to Creo's current management for an undisclosed amount. Expected to reduce the Company's annual operating costs by over £1m. | ||

Blencowe Resources (LON:BRES) (£43m | SR13) | An additional 36 assay results were received and compiled from the Stage 7 programme, including 31.5 meters @ 8.19% TGC from surface. | ||

@KR1 (£26.1m | SR23) | Following the recent launch of the BTW token, KR1 plc holds a total of 100m BTW, acquired through the Company's US$300k investment in Bitway's pre-seed funding round. Now worth $1.7m. Lockup 12-24months. | ||

@GSCU (£23.3m | SR4) | Rock chip sampling programmes at the Monolith Target show assay grades range up to 1.5% Cu and 95.8 g/t Ag. Channel sampling up to 0.53% Cu and 47.5 g/t Ag. | ||

@EAAS (£21.7m | SR40) | Q1 Revenue £11.0m, Adj. EBITDA £0.7m, Order Book £10.7m. Revenue recognition policy change reduces FY25 revenue by £4.0m, and increases FY26 by the same amount. | ||

@ORR (£16.1m | SR22) | Recent selective rock-chip sampling at Ndom has returned gold grades of up to 17.00g/t Au | ||

@GDR (£15.3m | SR10) | Implementation of its CYP2C19 ID kit at Bristol NHS Trust Southmead Hospital's Hyperacute and Acute Stroke Units is expected to commence shortly. | ||

@88E (£14m | SR15) | Acquisition and interpretation of the Schrader Bluff 3D (SB3D) seismic dataset. | ||

@QHE (£13.7m | SR26) | Extended production test program progressing well, with operations advancing in line with plan | ||

@ZIN (£10.3m | SR34) | Revenue +28% to £41.5m (16% organic), Adj. EBITDA +27% to £1.9m, Adj. PBT +33% to £0.4m. Net Cash £0m (FY24: £2.8m). |

* Market caps at previous trading day’s close

Graham’s Section:

Mercia Asset Management (LON:MERC)

Up 5% at 29.75p (£126m) - Year end trading summary and notice of FY results - Graham - GREEN =

Mercia Asset Management… the proactive, regionally focused private asset manager with over £2.0billion of assets under management… is pleased to provide a trading summary for the financial year ended 31 March 2026.

Good news: after a strong H2, the company “now expects its EBITDA for FY26 to be materially ahead of current market expectations.”

The explanation is not particularly detailed, but they note >£200m of “proposed increases to existing fund mandates, plus successful VCT and EIS fund raises”. So some of that £200m will already be included within AUM, while some should hopefully be coming on board soon.

There were “no redemptions during FY26” - it helps when funds are structured as VCT or EIS, rather than open-ended funds. It continues to hold a large portfolio of direct investments (this was valued at £131.1m at the interim results, higher than the current market cap). That portfolio “continues to make good overall commercial progress, despite the current elevated challenging market backdrop”.

Buybacks: a £3m buyback was completed, and a new £3m buyback has begun. This might not sound like much but with a market cap of £126m, it’s a meaningful reduction in the share count.

Cash position: c. £26m, zero debt.

CEO comment: Dr. Mark Payton says that the inflows are “continuing testament to our clear strategy of focusing on growing our profitable private asset management capabilities”. And with that strong cash position, “Mercia has entered the new financial year in a very strong financial position”.

Estimates: My thanks once again to the team at Equity Development for covering this one. Analyst Paul Bryant’s previous estimate was for FY March 2026 EBITDA of £7.2m, converting to PBT of £4.8m and EPS of 0.8p. Those estimates should now be beaten - certainly the EBITDA forecast.

Graham’s view

Obviously I’m going to be a little smug about this, as this is a stock I’ve been very positive on (although sadly I haven’t yet found a space for it in my personal portfolio). I stubbornly left it on my annual watchlist for the year.

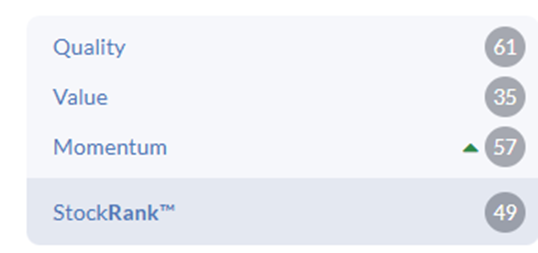

Eagle-eyed readers may note that the ValueRank is only 35:

This is a case where the stock does look expensive against earnings, but the balance sheet supports it. For example, even if EPS came in ahead of prior expectations at about 0.9p, the P/E multiple would still be 33x. So that’s expensive. But then you’re also getting a direct portfolio worth more than the market cap, and a big chunk of cash. So in my mind, this is a value play.

The problem with value plays is figuring out how long it's going to take for that value to trickle down to shareholders. In this case, we have a growing asset management business, a commitment to sell the portfolio of direct investments over time, and a declining share count from buybacks.

In my view, that’s a nice mix of catalysts and so this is a case where I think that the fundamental value has a good chance of finding its way into shareholders’ hands, over time. Of course I could be wrong about that. And the share price still doesn’t agree with me:

Animalcare (LON:ANCR)

Up 34% at 331p (£229m) - Recommended Acquisition - Graham - PINK

Congratulations to holders of this one: we have a recommended offer at 336p. That’s a 36% premium to yesterday’s close.

Harwood Capital are major shareholders here, with 18% of the company, so a takeover event is perhaps not the biggest surprise.

ANCR shares have traded higher than 336p before, but not for a few years:

The buyer: Charterhouse Capital, a London-based mid-market private equity firm with AUM of c. €7 billion. The flow of private equity takeovers has slowed down in 2026, which makes sense as the market is no longer as obviously cheap as it was over the last couple of years. To illustrate this, here’s the FTSE SmallCap Index - it’s more representative of companies that can be taken over by private equity than something like the FTSE 100.

Still, there are pockets of value, with AIM-listed Animalcare evidently being perceived as such. The rationale is typical: being a private company will mean that the company can make more long-term investments, away from the scrutiny of short-sighted stock market investors.

Charterhouse believes Animalcare is better able to achieve its long-term growth potential as a private company rather than a public company. Charterhouse is well positioned to support Animalcare's next phase of growth by partnering with the high-quality management team, providing the strategic flexibility required to accelerate R&D investments for the long-term, make the required operational investments and pursue transformative M&A.

The Animalcare Board agrees, saying that the company needs to embark on an “intensive investment cycle”, with “high-risk early-stage discovery and clinical development, with durations of up to 7-8 years” that “is better suited to a private company capital structure with a longer-term investment horizon”.

They do have a point: if results were spotty for the next eight years, due to risky and expensive R&D, then fund managers and market commentators such as myself are likely to be critical of performance.

Irrevocable undertakings: the largest shareholder Marc Coucke and Harwood Capital both support the proposal, so 41.7% of shareholders have already promised to vote in favour. This makes it highly likely to go through, which explains why the shares are already trading at 331p.

Alternative offer: if shareholders don’t want to fully cash out, there is an option to continue holding shares in the newly restructured business. But I imagine that nearly everyone will fully cash out.

Graham’s view

The management team at Animalcare were kind enough to speak with me at their interim results last year.

I’ve been moderately positive on the shares, but didn’t know how to value their R&D spend. There is always a tension between investing for future growth and running a business for cash today. Animalcare clearly wants to prioritise the former. That requires patient and understanding shareholders. But most stock market investors (including yours truly), and fund managers such as Harwood, are not operating on a 7-8-year timeframe. There is patience, and then there is patience.

Personally, I’m happy to sit on a stock and be wrong for a year or two. And if it performs well, I’m happy to leave a high-conviction stock in my portfolio permanently. But I don’t really want to make bets where the outcome is uncertain for 7-8 years. I think most share investors would feel the same way. Therefore, based on what Animalcare have said about their R&D plans, which could create volatile financial results, I think it’s reasonable for them to accept a PE takeover.

As for the offer they’ve recommended: a 36% premium is not exorbitant but it is at the sort of level that I think most investors would find reasonable. So well done to Animalcare and its investors - you now have the nice problem of reinvesting your winnings.

Mark's Section:

Alumasc (LON:ALU)

Down 10% at 234p - Q3 Trading Update - Mark - BLACK/AMBER/RED ↓

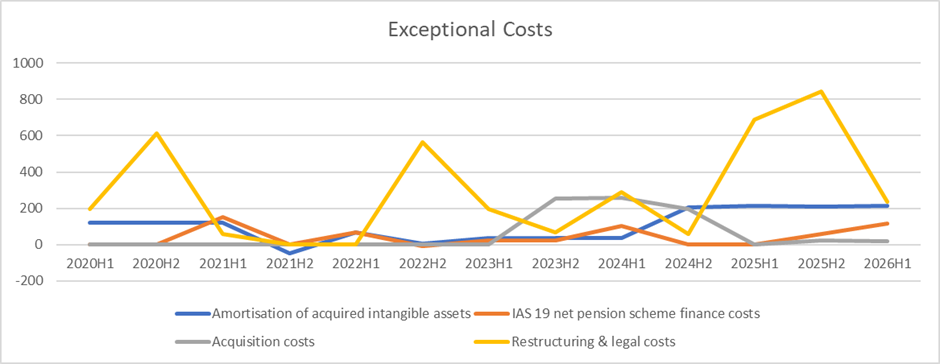

My first thought when seeing this profit warning was that things must be bad if Alumasc can't adjust their way out of this one! I've been critical in the past of the scale of the adjustments made, and how some of these appear to be less exceptional than one would presume:

The trading update itself doesn't read too badly:

The strong momentum in order intake seen towards the end of H1 FY25/26 continued into Q3, albeit overall performance was slightly below expectations, due to the impact of events in the Middle East from the end of February 2026. Overall, Q3 FY25/26 revenues were 2% ahead of the prior year, with an average monthly run-rate 8% ahead of H1 FY25/26. The order book at the end of March 2026 was 28% higher than March 2025, and 8% higher than December 2025.

However, the net result is:

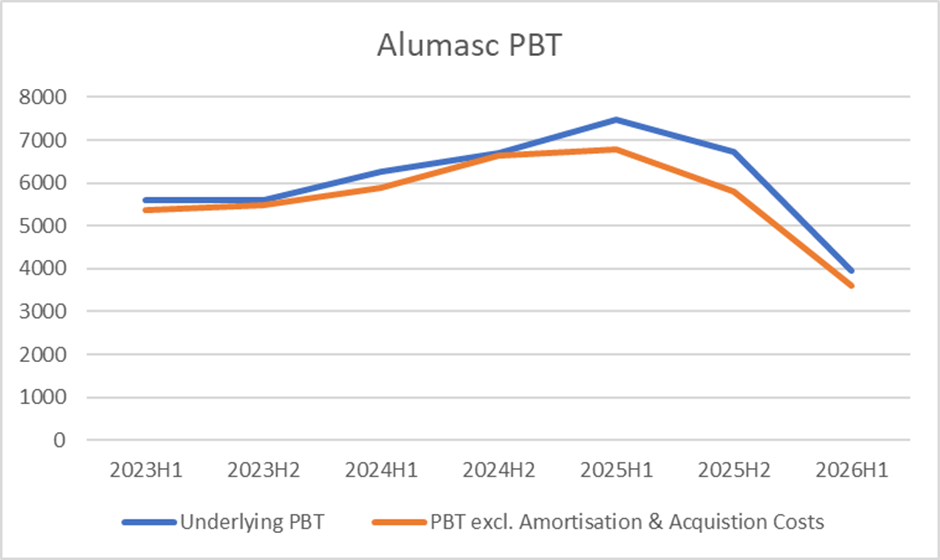

Against this market backdrop, the Board is adopting a more cautious view of the Group's outlook for the remainder of the 2026 calendar year, and now expects FY25/26 underlying profit before tax to be approximately £11m. The Group continues to have a strong balance sheet, with the year end net bank debt leverage ratio expected to be approximately 0.4x, allowing it to capitalise on opportunities as they emerge.

Forecasts:

We need their broker, Cavendish, to update us on what this means for the financial figures:

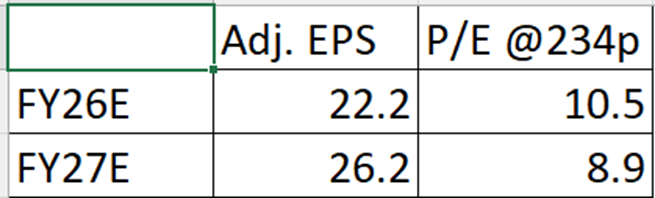

FY26E Changes: Revenue -3.9%, EPS -24% to 22.2p, Net Debt £4.3m (from £0.3m Net Cash)

FY27E Changes: Revenue -3.8%, EPS -20% to 26.2p, Net Cash £3.2m (from £5.1m Net Cash)

While the company suggests this is a minor blip and that the cost savings to be implemented will deliver benefits, this is still a sizable profit warning impacting all future forecast years.

The signs were there?

A weak Q1 update in October last year prompted Graham reduce our view to AMBER, and the share price fell from around £3.50 to £2.50:

FY26 estimates were reduced at this time, but FY27 only trimmed very slightly:

Interim results released in February seem to have assuaged market concerns, as the company said they were trading in line. However, Roland's comments suggested that caution was required given the H2 Weighting. As did my own analysis of the trends here:

This does make me wonder if the outgoing CEO timed his exit well, although he doesn't appear to have sold any of his 3% holding.

Valuation:

The share price has only dropped by around 10% this morning, making the initial price action look like an under-reaction compared to the 24% reduction in EPS forecasts. Especially, as this is more than a one-off warning and now impacts FY27 net cash/debt figures as well. The FY27 EPS forecast is back to FY24 levels, when the share price was some 20% lower than today.

Calculating updated figures, the rating isn't crazy:

However, it is not obviously cheap compared to peers or the typical historical multiple that Alumasc trades on. Plus, with more cost savings on the way, we can look forward to yet another period of heavy adjustments, which will be excluded from these underlying figures.

Dividend forecasts are only slightly cut, meaning the dividend yield is over 4%. However, this isn't exceptional in current small cap markets.

Mark's view

This is now the second profits warning, and despite the company putting on a brave face, it is impacting FY27 forecasts as well. The response, which is further cost-cutting, is surely the right thing, but it means that my critique that their excluded restructuring costs are anything but exceptional bears even greater weight. Even on the heavily adjusted figures, the share price is not obviously cheap compared to peers or their recent history.

With a Stock Rank that is likely to face a further lurch downwards once the algorithms process the impact of the updated forecasts, I feel we need to take a more negative view of AMBER/RED.

Premier Miton (LON:PMI)

Down 7% at 41p - Q2 AuM update - Mark - BLACK/AMBER/RED ↓

I thought I was experiencing Deja Vu this morning while summarising the news, as trading updates from both Alumasc and Premier Miton saw Cavendish downgrade their current year EPS forecasts by 24%, by pure coincidence!

When I looked at Premier Miton following their Q1 AUM update in January, I concluded:

…when it comes to Premier Miton specifically, this AUM update worries me. They have seen big outflows in the last quarter and delivered mediocre investment performance. The risk that they miss current EPS forecasts and need to cut back their dividend payout looks to have increased today.

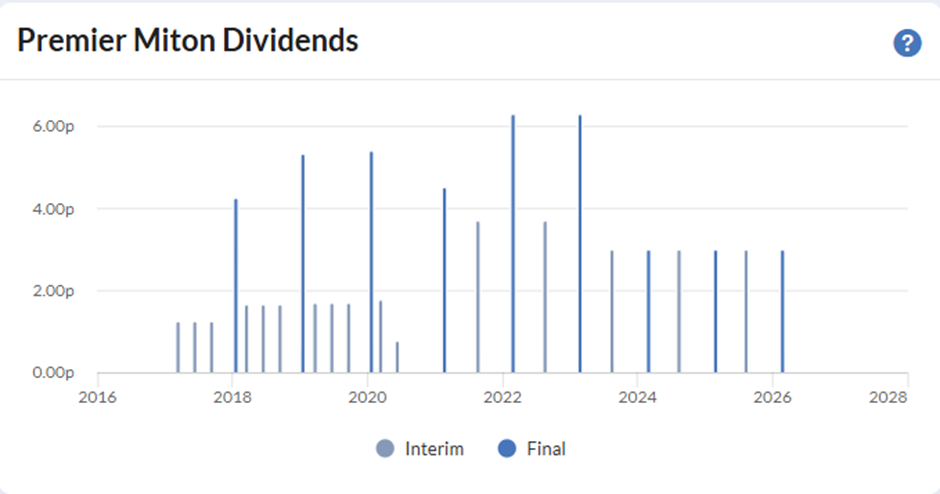

This was perhaps prescient, as today, the surprise for me is not the EPS downgrade but the dividend forecast cut. A 3p dividend paid biannually had become the norm since 2023 and, until today, was forecast to remain at that level going forward.

Forecasts:

Here is what has changed today:

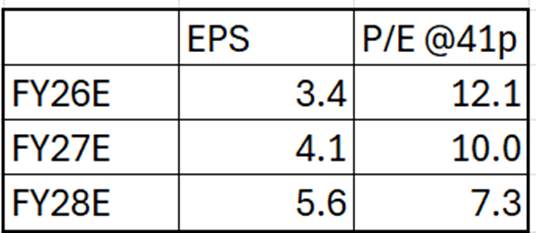

FY26E Changes: Avg. AuM -4%, EPS -24% to 3.4p, DPS -33% to 4.0p

FY27E Changes: Avg. AuM -5%, EPS -17% to 4.1p, DPS -33% to 4.0p

FY28E Changes: Avg. AuM -3%, EPS -9% to 5.6p, DPS -33% to 4.0p

However, from the share price chart and the lack of share price reaction today, this was perhaps viewed as inevitable by shareholders:

Balance Sheet:

Perhaps one reason for the forecast cut in dividend is that net cash continues to decline:

Closing cash position as at 31 March 2026 of £24.6 million

Helpfully, the company reveals its regulatory capital requirements when it publishes results. This was £13.1m at year-end, so assuming a similar level now, we have a roughly £11.5m surplus. This is enough to keep paying the uncovered dividend for FY26, but they won't want the buffer eroded too far.

Sector Comparison:

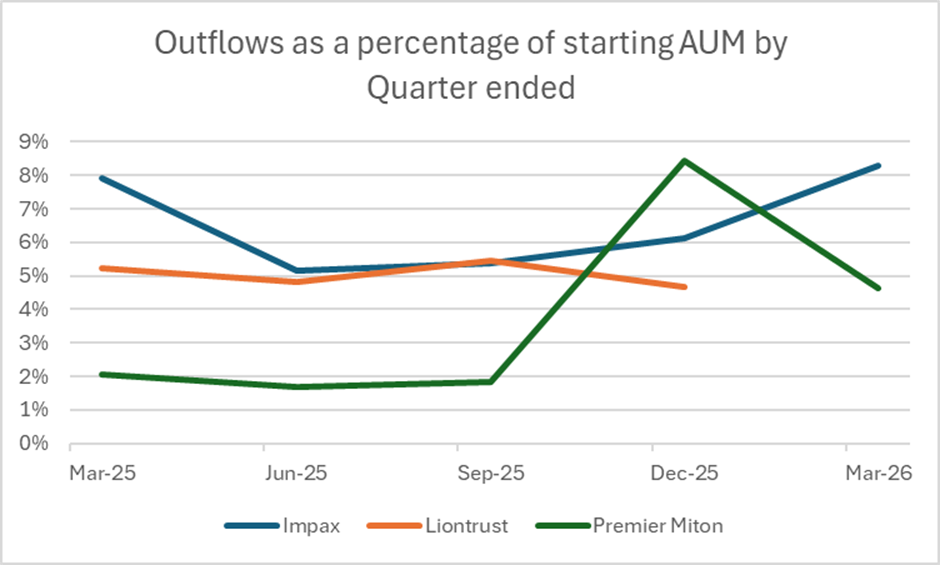

Impax reported its quarterly AuM recently, and this caused a 25% fall in the share price. In that case, Cavendish cut the outer forecast years more severely, taking 31% out of FY27, for example. This may explain the comparative lack of reaction here, although looking at the AuM, I don't see a huge variation in performance. (Liontrust are yet to report AuM for this quarter.)

Premier Miton's outflows are lower this quarter at around 5% of AuM, but still elevated compared to FY25, where they escaped relatively unscathed:

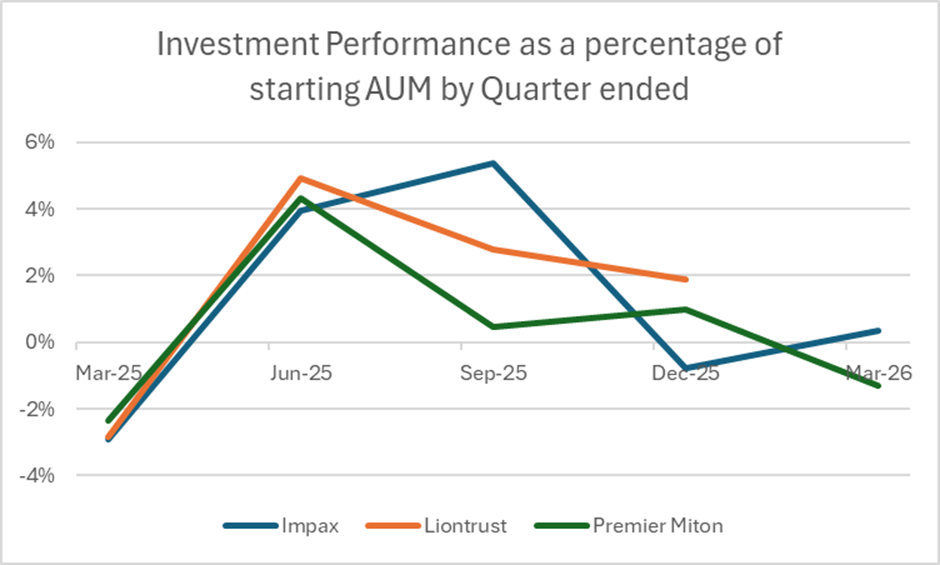

Plus, their investment performance continues its poor trend, and dips into negative territory:

Overall, I don't see a great case for optimism here, at least in the short term.

Valuation:

Here's what the updated earnings multiples look like:

This isn't obviously cheap until you get out to FY28, and at this stage it's really just guesswork.

However, a 4p/share dividend represents an almost 10% yield, despite today's cut in guidance. This is uncovered in FY26 and barely covered in FY27. However,

The surplus cash above regulatory capital levels represents around 15% of the current market cap and makes these figures look better, but in reality, I don't see a huge amount of surplus cash beyond that needed to support the uncovered dividend.

Impax and Liontrust both now look cheaper on many metrics (although there's a risk that Liontrust warns when their quarterly AuM figures are released soon).

Mark's view

While the market may not have been surprised by the cuts to forecasts in response to these quarterly AuM, the company now appears to be trading at a premium to listed peers. I am sympathetic to the idea that the whole sector is cyclical and will look undervalued once any upswing in AuM gains traction. However, with Premier Miton no longer looking cheap compared to peers, and little cause for optimism in today's figures, I think we should take a slightly more negative view of AMBER/RED.

Dunelm (LON:DNLM)

Down 5% at 80p - Third quarter trading update - Mark - AMBER/GREEN =

Q3 sales are growing, but only just, and at 2.1% YoY, this is below the 3.6% growth rate of H1. They manage a 30bps improvement in Gross Margin, but, overall, this isn’t enough to avoid a mild warning:

FY26 PBT currently expected to be towards the lower end of consensus expectations

The blame is put on the current low consumer confidence levels due to geopolitical events.

Helpfully, they quantify the expectations:

Company compiled consensus average of analysts expectations for FY26 PBT is £213m, with a range of £210m to £217m

This is a surprisingly tight range, so in reality, coming in at the bottom of the range is at most a 1.4% reduction. As such, the current 5% drop in the share price appears to be a potential overreaction. And it perhaps looks a little harsh for us to mark it as BLACK today. Especially as it comes on the back of a weak year for the share price so far:

However, it is worth noting that, as a well-covered, larger UK company, forecast changes tend to be incremental here and can occur outside reporting periods. The overall trend here is not particularly encouraging:

This will drop a bit more today as the consensus shifts.

There is a risk that this business has gone ex-growth, and hence the current rating represents fair value for a mature business:

High returns on capital are great, and the asset-light model allows high free cash flow generation. However, it is only worth paying up for a high-quality company if it can deploy additional capital to grow rapidly. FY26 isn’t going to be one of those years.

However, I buy the excuse that a lot of this weakness is due to consumer uncertainty and the knock-on impact from low housing market transactions, rather than something fundamentally wrong with the business.

Mark’s view

Roland looked into the details of the business model and longer-term growth prospects when he reviewed the company’s interim results in February and rated the company AMBER/GREEN. I don’t consider a very slight downgrade in PBT guidance to change that view. However, I can see why some investors may want to wait for signs that the company can return to historical revenue growth rates, or have a higher Momentum Rank, before jumping in:

Central Asia Metals (LON:CAML)

Up 1% at 156p - Q1 2026 Operations Update - Mark – AMBER/GREEN

It's not been a fun year so far for Central Asian Metals shareholders. The initial optimism of being a commodity play appears to have been snuffed out by an update that took 5 years off the Life of Mine at Sasa, their lead/zinc mine in Macedonia:

The FY results were not particularly well greeted by shareholders:

However, brokers havebeen upgrading prospects based on better copper pricing:

It feels like investors at this point would have preferred them not to have expanded into lead and zinc and just kept their copper mine in Kazakhstan.

However, they are certainly cheap if they hit those forecasts:

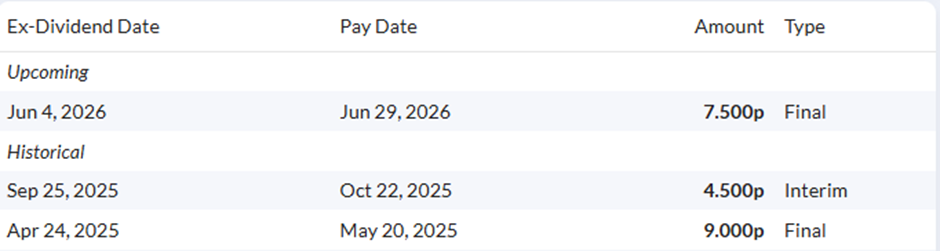

I'm not sure how much faith I'd place in that yield forecast, given that the recently declared final dividend was at a reduced level:

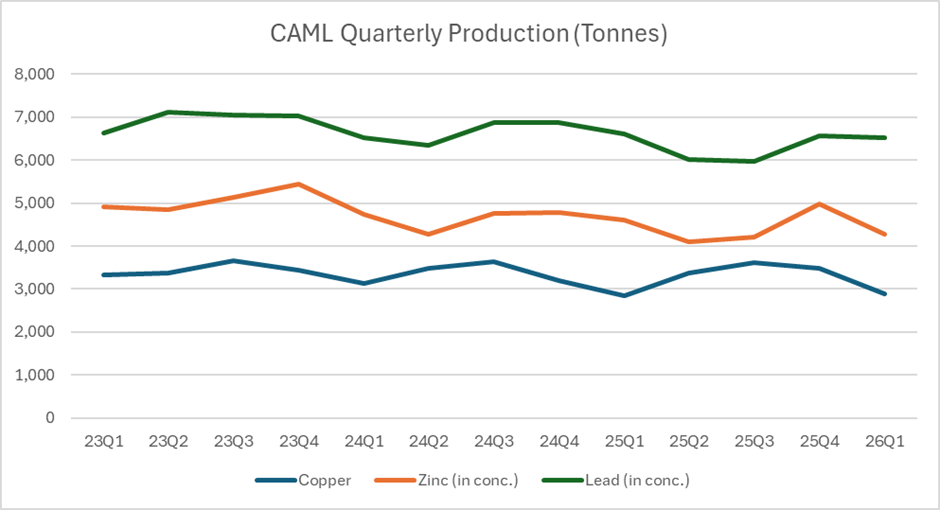

In today's update, they confirm they are trading in line with production guidance:

Production guidance for FY2026 reiterated:

o Copper of 12,000 to 13,000 tonnes

o Zinc-in-concentrate of 18,000 to 20,000 tonnes

o Lead-in-concentrate of 26,000 to 28,000 tonnes

However, the quarterly figures come in slightly below the run-rate required to hit these:

- Kounrad copper production of 2,880 tonnes

- Sasa zinc-in-concentrate production of 4,282 tonnes

- Sasa lead-in-concentrate production of 6,529 tonnes

Looking at the historical production, there does seem to be some seasonality in copper production due to weather effects (which were said to be unusually low), but not in Lead and Zinc:

This suggests these targets may be a challenge. It also sounds like costs are going up here, too:

During Q1 2026 we signed a new collective bargaining agreement with the trades unions at Sasa, providing certainty with respect to labour rates through to Q1 2028. The negotiations also included productivity measures designed to ensure the workforce shares more directly in the success of the operation.

Mark's view

It seems that things are going well for their copper production at Kounrad, and that for investors who want exposure to this base metal, this could be a good play.

However, their foray into Lead and Zinc appears to have detracted from the exposure many investors would have wanted. Sasa seems to have faced challenges with Life of Mine and costs recently, and the production targets for the Full year look a little challenging based on Q1 production. So, despite a good record of dividend payments, I think there's a risk that management's priorities don't align with shareholders'.

Despite these concerns, this is far from the worst offender in this sector, and the current multiples buy quite a bit of leeway on valuation, especially for those bullish on copper prices. So overall, with production guidance in line so far, I keep our broadly positive view of AMBER/GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.