Good morning! The Agenda is ready now.

1pm: that's a wrap! Thanks everyone.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Lloyds Banking (LON:LLOY) (£38.1bn) | 2024 results | 2025 guidance: ROTE c. 13.5% (2024: 12.3% or 14% before provision charge for motor finance) | |

Anglo American (LON:AAL) (£28.7bn) | FY Results | $3.1bn loss includes $3.8bn impairments. Reduced carrying value of De Beers by $2.9bn. | AMBER (Mark) At 18x earnings and flat forecasts, it is hard to see a positive investment case, even for those bullish on copper. |

Centrica (LON:CNA) (£6.8bn) | Final Results | 2025 outlook unchanged. Path towards £1.6bn run-rate EBITDA by the end of 2028. | |

Mondi (LON:MNDI) (£5.7bn) | Final Results | Rev +1%, adj. EBITDA -13% largely due to lower forestry fair value gain. Order books improving. | |

Ithaca Energy (LON:ITH) (£2.2bn) | FY24 TU | Full year performance at top end of management guidance. Strong Q4 production, cost control. | AMBER/GREEN (Mark) |

Safestore Holdings (LON:SAFE) (£1.3bn) | Q1 TU | LfL revenue +2.9% (constant currencies). LfL occupancy improves to 75.9%. | AMBER/GREEN (Graham) My first impression is that there's an appealing discount here vs. tangible NAV. Additionally, the LTV calculations and related commentary from the company suggest that leverage is not a concern. So I'm tentatively positive on the outlook for shareholders. |

Hays (LON:HAS) (£1.2bn) | HY Report | LfL net fees -13% (perm -19%, Contract -9%). Op profit -56%. Ongoing macro uncertainty. | AMBER (Mark) |

Indivior (LON:INDV) (£1.1bn) | Final Results | FY24 Net Rev +9%, Adj. net income flat at $223m. Ahead of guidance. | |

Home Reit (LON:HOME) (£301m) | TU | £12.2m cash, no debt, Jan25 rent collection £1m | RED (Mark) [No section below] |

AdvancedAdvT (LON:ADVT) (£193m) | TU | Materially above the current market expectations (FY25 Rev. & Adj. EBITDA of £41.0m & £8.4m) | AMBER (Graham) The valuation here doesn't put me off. When you consider the low enterprise value, ADVT's software businesses aren't being priced too expensively. The overall structure is a little odd but it's not supposed to make sense: it's about whether or not you wish to back the founder. |

John Wood (LON:WG.) (£167m) | Contract Extension | 2-yr $120m contract extension with Shell UK | RED (Mark) [No section below] |

Begbies Traynor (LON:BEG) (£150m) | Q3 TU | In line | AMBER (Mark) |

Arbuthnot Banking (LON:ARBB) (£147m) | Pre-close TU | in line with PBT consensus of £34.5m. | AMBER (Mark) [No section below] |

SRT Marine Systems (LON:SRT) (£116m) | Response to press | Allegations of procurement irregularity in the Philippines denied by the company. | AMBER/RED (Graham) The company itself and the CFO have been cleared already. According to the Philippine press, SRT's CEO has been ordered to appear in court. I don't have any view on the merits of the case but I feel much safer taking a moderately negative stance on SRT due to its track record. High risk, high potential reward. |

Zoo Digital (LON:ZOO) (£27m) | TU | FY25 Rev $50.5m, EBITDA $1m Below market expecations. | RED (Mark) |

Graham's Section

AdvancedAdvT (LON:ADVT)

Up 11% to 190.9p (£214m) - Trading Update - Graham - AMBER

AdvancedAdvT Limited (AIM: ADVT, "AdvT", the "Group"), the international software solutions provider for the business, compliance, and resource management, today announces a pre-close trading update for the full year to 28 February 2025.

Not too much info in today's announcement but we are told that adj. EBITDA for FY Feb 2025 will be materially above the current market expectations, these expectations being for revenues of £41m and adj. EBITDA of £8.4m.

The reasons: “good growth in both new customers and the renewal of substantial contracts on improved terms”, plus “laser focus on operational efficiencies”.

Comment by Vin Murria:

"Our strong performance reflects the operational changes implemented in the first half of the year and the positive impact of key customer contract wins. These factors provide a solid foundation for continued growth. We remain focused delivering long-term value for our shareholders and continue to pursue further M&A targets."

Estimates: Singers have updated their FY25 revenue forecast to £42.5m and their EBITDA forecast to £9.6m.

Looking ahead to FY Feb 2026, the financial year that starts in less than two weeks, the forecasts have been raised there, too. The revenue estimate is now £45m (prev: £43.2m) and the EBITDA estimate is now £10.1m (prev: £8.8m). Singers says that ADVT has “continued to benefit from the ongoing migration of its customers to the cloud and sustained demand for its digital software and solutions.”

Graham’s view

I did some back-of-the-envelope calculations in September and suggested that ADVT was generating annualised revenues of >£42m and adj. EBITDA of <£9m, thanks to an acquisition it made in July 2024.

FY25 is going to be ahead of that calculation even though the acquisition (Celaton) didn’t start contributing until nearly half-way through the financial year. Impressive!

Celaton provides “intelligent document processing”, consistent with the theme across ADVT’s businesses that they provide productivity-enhancing software.

Checking the interim results to August 2024, I see that ADVT’s cash remained very high at £83m. There was also the near-10% stake in M&C Saatchi (current value: £22m).

Subtracting their value from ADVT’s market cap, we are left with an enterprise value of only £109m.

For that you get a set of software businesses which are forecast to earn EBITDA of £10.1m in the financial year about to start.

And the company did generate what I would call “real profits” (not just positive EBITDA) in H1. Even if you are very strict and don’t allow them to adjust out the amortisation charge, the adjusted operating profit was still £2.5m for H1.

There are some great imponderables at play here, the main one being the ultimate destination of that £83m.

I’m tempted to upgrade my neutral stance but I don’t think I will, for now. As I’ve said before, this stock is really about whether or not you wish to hang on to Vin Murria’s coattails. It is her vehicle: she is the largest individual shareholder and the Chair.

Objectively speaking, I don’t think it makes a lot of sense for a PLC to own an extraordinarily large cash balance, 10% of M&C Saatchi (LON:SAA), and five software businesses. But that’s not the point of the thing: it’s about whether or not you believe in the long-term vision of Vin Murria OBE.

SRT Marine Systems (LON:SRT)

Up 5% to 48.8p (£122m) - Response to reports in Philippines press - Graham - AMBER/RED

This relates to the Integrated Marine Environment Operating Systems (IMEMS) fisheries project in the Philippines.

The relevant press report is thought to be this article in the Daily Tribune, a national broadsheet.

CEO of SRT Marine, Simon Tucker, is named in the article in which they state that he, along with others, “will stand trial on graft charges related to an allegedly anomalous P2 billion vessel monitoring system project in 2018”.

2 billion Philippine pesos are today worth £27m.

The article continues:

The case stems from allegations that the three conspired to award a P2.09 billion contract to SRT-UK, despite the company’s prior disqualification from a French-funded bidding process. The original project, backed by a P1.6 billion French government loan, required bidders to be French or in a joint venture with a French firm.

SRT-France, a subsidiary of SRT-UK, was disqualified by the French Ministry of Finance due to British ownership and lack of operational facilities in France.

And then perhaps most worryingly:

Tucker has yet to surrender to authorities. Judge Alagar ordered Tucker to appear in court and post bail before the 26 February proceedings.

SRT’s response (emphasis added by me):

As noted via an announcement on 24 April 2024, SRT clarifies that the IMEMS contract was won following an open and competitive international tender, which has been successfully implemented and is operational. The Ombudsman has previously confirmed that both SRT and Richard Hurd were cleared of any allegations. The Ombudsman had recommended further investigation into Simon Tucker and other individuals outside of SRT, and we are pleased to see this now moving forward through the Philippine legal process towards a clear resolution. The Board remains fully supportive of Simon who continues with the process to clear his name.

Richard Hurd is SRT's CFO.

It’s good news that the company itself has already been cleared. But Simon Tucker has been CEO since 2008 - I trust that the Board has a succession plan, if a replacement for him was needed at short notice for any reason?

Graham’s view

Long-time readers will know that I’ve never believed in this company. There have been so many false starts and promises that it was about to succeed financially, but it never happened.

Recently, the promises of imminent success became larger than they had ever been.

The last outlook statement said that “the coming years will be transformational” (the Chair’s words). There were said to be £320m of system projects in the order book, to be implemented over the next two years. Another small ($15m) contract has been signed since then.

Historic annual revenues at SRT peaked at £30m (2023) and have been as low as £8m (2022). So the size of the order book now is huge, relative to past revenues.

Accordingly, I switched to neutral (e.g. see my comments in December) as I waited to discover if these huge projects would be delivered soon and if they would, as promised, transform the company’s fortunes.

But it was noteworthy that broker Cavendish did not publish any financial forecasts - not for FY June 2025 or any other year. Perhaps that’s just because the timing of revenue recognition is too difficult to predict, but it’s unusual.

Anyway, after today’s update, I think I’m going to trust my instincts and put AMBER/RED back on this stock again.

This could be overly pessimistic. The case in the Philippines might come to nothing, the company might be about to generate £300m+ of revenues, and the £1.2bn “validated pipeline” might convert well into revenues, too.

Maybe. But an important point of the colour system is to highlight risk and I deem SRT to be extremely risky.

More reliable than profit growth has been the growth in its share count:

Let me emphasise that I don’t have a strong view on the legal situation in the Philippines. It’s just another risk that gets added into an overall picture that I already believed to be highly uncertain and unpredictable, from a company with many historic promises of success.

Safestore Holdings (LON:SAFE)

Up 2% to 597p (£1.3bn) - 1st Quarter Trading Update - Graham - AMBER/GREEN

It has been many years since we checked in on this self-storage REIT.

Sentiment doesn't look great:

Revenues have grown at a long-term CAGR of 8% according to the StockReport, although there was no growth in 2024 and expected total growth (not like-for-like) in FY October 2025 is modest at 6%.

Some headlines from today’s Q1 update:

Like-for-like revenue +2.9% at constant exchange rates.

Total revenue +3.5% at constant exchange rates.

Like-for-like occupancy 75.9% (Q1 last year: 74.5%).

Like-for-like average store rate £29.88, down 0.6% year-on-year.

It’s all very stable, even unexciting. But I suppose many REIT investors are trying to avoid fireworks.

CEO comment refers to the “improving trajectory” in UK occupancy, with “strong domestic demand”.

There has been >30% growth in revenues from “Expansion markets” (Spain, Netherlands, Belgium) but they are starting from a low base. I think they account for less than 10% of total revenues.

We continue to make progress in opening our pipeline of stores in line with the programme we disclosed in January with six new stores and an extension opening in the quarter, adding over 300,000 sq ft of MLA [maximum lettable area] to the portfolio. Our future development pipeline includes a further seven stores projected to open this year, with a total 8% increase in MLA projected for the year.

I guess the 8% increase in lettable area help should support the total forecast revenue growth.

Graham’s view

I’ll tentatively go AMBER/GREEN on this due to EPRA (real estate) net tangible assets per share of 1,091p as of year-end, October 2024.

Net debt was very significant at £900m. However, the LTV ratio was only 25%, and “the Board considers the current level of gearing is appropriate for the business” (according to the results published in January).

I also take comfort from the debt repayment schedule, with light maturities until FY 2029:

So this is another REIT where I’d be interested - possibly cheap against its existing estate and possibly not too risky in terms of leverage. More research is needed.

Mark's Section

Zoo Digital (LON:ZOO)

Down 33% to 18.5p - Trading Update - Mark - RED

This update sounds ok:

The Board currently expects full year FY25 revenues will be at least $50.5 million, which is up 24% on the prior year. The full year revenues will result in a return to EBITDA profit of at least $1.0 million, compared to a loss of $13.6 million last year.

Until we get to this line:

As a result, FY25 revenues and EBITDA1 are expected to be below market expectations

Helpfully, they give those expectations:

For the purpose of this announcement, the Group believes market consensus for FY25 to be revenue of $55m, and adjusted EBITDA of $2.75m.

So that is a material downgrade in EBITDA. It annoys me when companies say “EBITDA profit”. While they may be trying to distinguish between positive and negative EBITDA, at the end of the day, EBITDA is not profit, unless you have a company with no assets, no cash and doesn’t pay tax!

I can’t see any updated research coverage, so I’m going to have to do my own legwork on this one. The HY results released in November had:

· Adjusted EBITDA1 returned to profit, as previously guided, of $1.6 million (H1 FY24: EBITDA loss of $7.1 million)

· Operating loss of $2.5 million (H1 FY24: loss of $10.9 million)

So that means that H2 actually delivered a $0.6m LossBITDA. There is $4.1m of D&A in H1, so we should expect an operating loss of about $4.7m for H2. To be fair, their capex in H1 was a lot lower than D&A at around $1.2m. However, there was around $200k in interest costs. So unless they have cut capex further, we will see about $2m of cash outflow in H2. This tallies roughly with the guidance today:

The Company has also been closely managing its cash position and it expects the balance at the end of FY25 will exceed c.$1 million, and has invoice discounting facilities of $3m and £2m, which are expected to be largely unutilised.

They had $4.3m cash at the half-year. The difference may be that payables looked elevated at the end of H1 and may have normalised. The invoice discount facilities provide some breathing room, but not that much, given the current level of cash burn.

The company are guiding FY26 to be better:

The Company is seeing a marked increase in customer discussions around new projects to a level greater than at any time over the past two years. Currently, an enlarged proportion of customer assignments relate to them both licensing in third party content and licensing out catalogues, rather than the processing of new original programming. The Board envisages that this will be an ongoing trend, with the additional volumes of original content starting to recover later in FY26.

Although not in dubbing:

Based on current visibility, ZOO expects that dubbing revenues for FY26 will be lower than in FY25. However, with a lower cost base and higher margin revenue mix the overall profitability of the business is expected to improve significantly year on year.

And there is the usual cost-cutting exercise that we are seeing so much of at the moment with UK companies. However, they seem to have been far too slow to cut these when they suffered from the writers and actors strike. The company has only survived until now because the strikes ended when they did and that they raised £12.5m from the market in mid-2023 in order to acquire a Japanese company. They were unable to complete this; hence were able to use the cash to fund their losses. Now they say that:

The ongoing restructuring of the cost base to reduce the unit cost of production provides a strong platform to return to cash breakeven.

Note that “providing a strong platform” is different to actually being cash flow positive! Given all this, I can’t put much weight on FY26 being materially better than FY25, for earnings or cash flow.

Mark’s view

While they say it is often better to be lucky than good, this is not a maxim I want my investments to be run by. This company have been lucky to survive this long. Although they are guiding a better FY26, given the recent history, there must be considerable uncertainty about this. Their luck may be about to run out. RED

Begbies Traynor (LON:BEG)

Up 2% to 96p - Trading Update - Mark - AMBER

It is a short, in-line statement from this professional services group:

Financial performance across both divisions has been consistent with the board's expectations in the quarter. With a strong pipeline and continuing elevated activity levels, our expectations for the full year remain unchanged. This would extend our strong financial track record of growth.

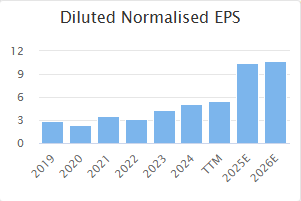

While that “strong financial track record of growth” may be good at the top line:

It is far more patchy and linear at the EPS level:

At least partly because that growth has been dilutive to the share count:

Things are looking better for this year with EPS forecast to jump by over 100%:

However, it is worth noting that the broker trend has been against them, and now FY26 is forecast to be barely above FY25:

The rating is modest based on these forecasts, so the confirmation of in line is good news:

However, this should be a boom time for insolvency practitioners, so the risk is that these are peak earnings. Equity Development have a note out this morning that includes forecasts out to FY27, but again, these are largely flat in real terms without any further acquisitions, underlining that this company trades at around the right price based on current forecasts.

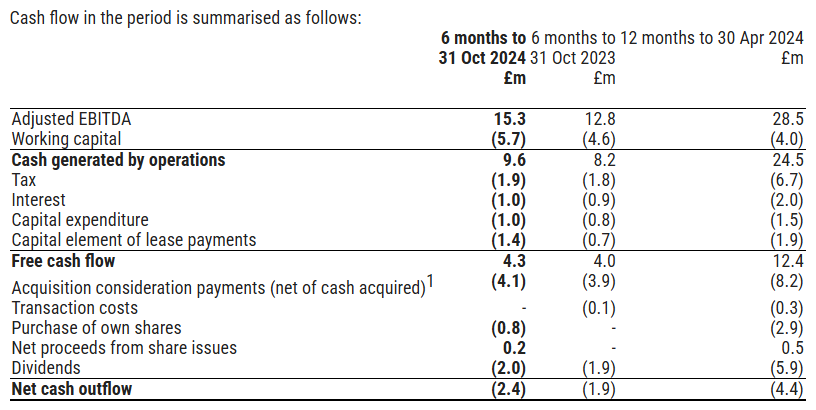

Free cash flow after acquisitions in recent periods has been close to zero:

This means that the dividends and buyback in recent years have been funded by increasing debt:

The overall gearing is low, so this isn’t an immediate concern, but sooner or later, they may need to choose between acquisition-led growth and shareholder payouts.

Mark’s view

The shares are modestly rated on forward earnings, but I can see why the market isn’t willing to rate them higher. Acquisition-led growth over the years has come at the cost of shareholder dilution and increased debt. Plus, there is the risk that the current UK economic conditions are peak season for an insolvency practitioner. So, I remain neutral here. AMBER

Anglo American (LON:AAL)

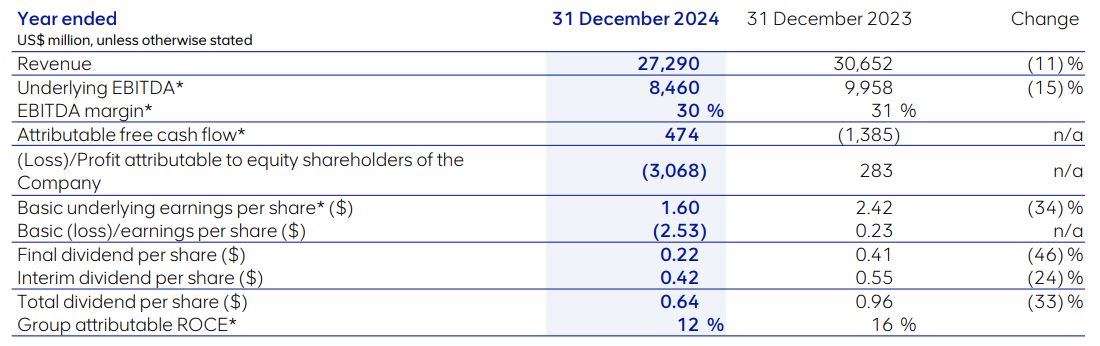

Up 3% to 2447p - Final Results - Mark - AMBER

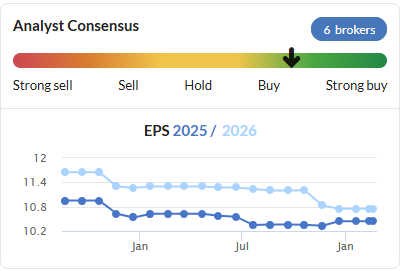

When I looked at this a couple of weeks ago, following its Q4 production report, I struggled to get excited by its 18x forward earnings. Nor did the brokers who slightly reduced forecasts again:

At 160c vs 164c consensus this appears to be another slight miss:

Although, it can be hard to tell with such large caps as it depends how often brokers have updated their notes. A single “stale” forecast can throw these off.

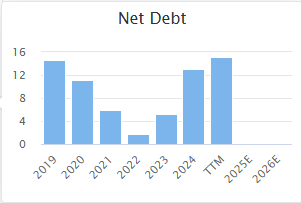

The $3.1b accounting loss is also unimpressive, even if it is largely caused by write-downs in the carrying value of De Beers. Underlying earnings are down, though. Net debt is flat at $10.6b, and the dividend is halved in line with the established dividend policy to pay out 40% of underlying earnings.

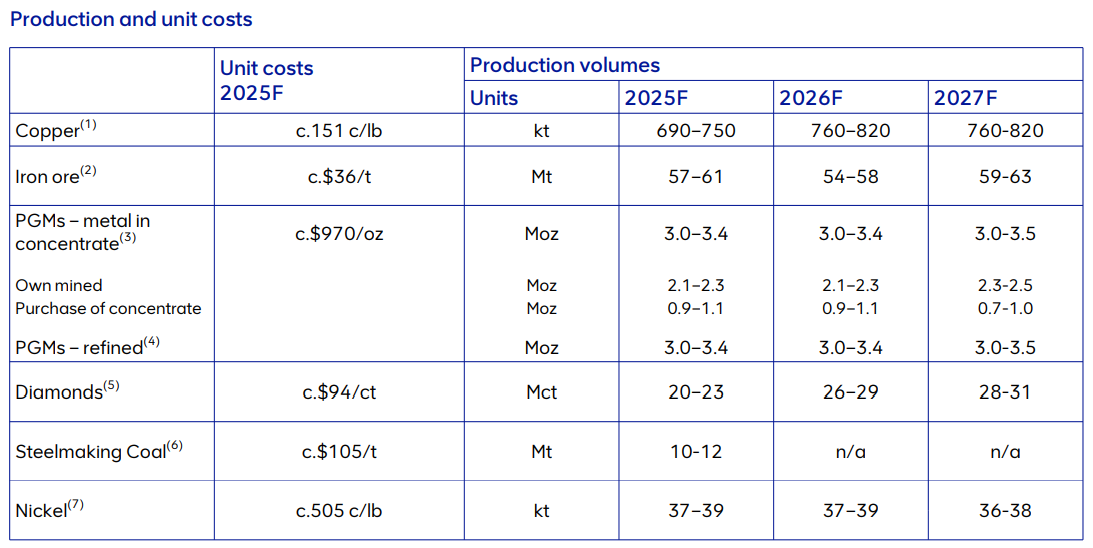

Despite all of this, the market seems to have liked these results, bidding the shares up 2%, on top of a 6% rise in response to the Q4 production report. Presumably, the market is looking forward to FY26, where copper production is forecast to grow:

Plus, they may be noting the recent strength in copper prices in 2025:

Despite these being known, brokers forecasts are for flat EPS in 2026, suggesting that the growth in production and prices may be being offset by higher costs.

Mark’s view

I don’t know enough about this miner to say that it is overvalued. However, at 18x earnings and flat forecasts, it is hard to see a positive investment case on the given numbers. For those who are bullish on copper, there would appear to be many cleaner and cheaper ways to get exposure than owning Anglo American. AMBER

Ithaca Energy (LON:ITH)

Up 10% to 144p - Trading Update - Mark - AMBER/GREEN

The past couple of years hasn’t been a good time to be a North Sea oiler, as the share price chart of ITH since listing at the end of 2022 attests:

However, the shares bottomed towards the end of 2024 and are up around 50% since then, including around 10% today. The good news is that:

Strong 2024 production of 80.2 kboe/d1 at the top end of market guidance range

Which combined with costs coming in below guidance, will surely mean exceeding expectations at the PBT level. Things are complicated by a material acquisition of assets from ENI, which was completed in October, giving a further significant uplift in production.

Q4 production of 116.0 kboe/d1 and opex per boe of approximately $14/boe delivering estimated Q4 EBITDAX of $642 million

This growth isn’t reflected in earnings per share forecast, though:

This is because the ENI transaction was a share-based one:

Following Admission of the New Ordinary Shares, the total number of shares in issue in the Company will be 1,653,732,455, of which 50.7% will be held by DKL Energy Limited, an indirect wholly owned subsidiary of Delek Group Limited and 38.7% by Eni UK Limited, an indirect wholly owned subsidiary of Eni S.p.A.

This makes the market cap around £2.4b or $3b, and the forward P/E look quite high at around 10 compared to the sector. Serica, for example, is on half this near-term rating. Their cash flow is clearly good as their commitment to paying a large dividend demonstrates:

The Group remains committed to delivering attractive returns to its shareholders, reaffirming total dividend target of $500 million for 2024 and 2025

Given the dilution and today’s price change, the dividend yield is not quite as good as the StockReport suggests, but at 16.7%, this is not to be ignored.

Mark’s view

A full valuation would require a detailed look at the various assets, reserves and production profiles. Something that is beyond me, not being an oil sector specialist. I cannot see any PI-friendly research notes either. However, this is clearly an ambitious company backed by some big oilers. The 16.7% dividend yield would clearly be attractive to income investors wanting to diversify from the more accident-probe Serica. So for that, I’ll give it in an AMBER/GREEN

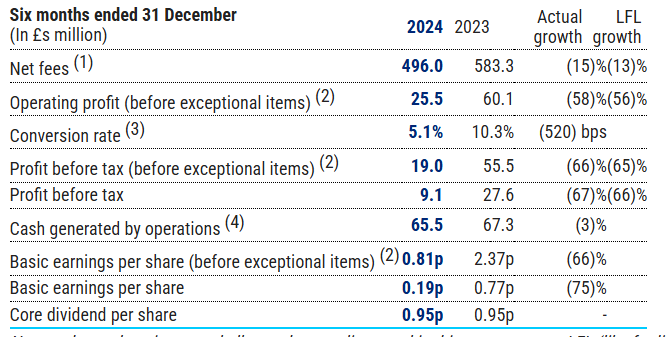

Hays (LON:HAS)

Flat at 73p - Half-Year Report - Mark - AMBER

These are poor results, with Net Fee Income down 15% and operating profit (even excluding rather large adjustments) down 58%:

However, this appears to be in line with expectations, as the share price reaction has been negligible. However, this still leaves them with an H2 weighting to hit the 2.34p EPS consensus in the StockReport. When the consensus trend looks like this, there is perhaps a bit of relief that things weren’t worse:

The rest of the story is familiar to anyone who has read the reports of similar recruiters. Cost-cutting, positive operating cash flow as working capital unwinds due to reduced trading, and dividends maintained. There is also the expectation of a medium-term recovery, although current conditions remain challenging. All that makes sense. However, this doesn’t mark Hays out as any different to the other struggling, larger listed recruitment companies.

This means that investors taking the long-term view will probably do well from the cyclical rebound in the sector when it does arrive. Calling the bottom (or not) in such things is a fool’s game. However, I can’t help feeling that the time to buy would be when there are at least some tentative signs of a rebound in trading or at least when the Momentum Rank is higher than 17:

Mark’s view

Hays is suffering in the same way as all the other larger recruiters at the moment. This means that it will benefit from the same recovery when it eventually arrives. If it returns to historical EPS highs, then it will look cheap. However, I see nothing that suggests that this will be soon or that Hays will be a particularly strong beneficiary compared to any other similar company. The second half weighting for EPS revealed in today’s results adds to the short-term risks. AMBER

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.