AI boom: Alphabet (NSQ:GOOGL) has increased the amount it is raising to spend on AI, from $80 billion to nearly $85 billion.

In total, it’s planning to spend up to $190 billion on capex this year, more than double what it spent in 2025. It plans to spend even more in 2027.

Billionaire Ray Dalio, commenting on the AI boom and the rush to sell AI-related shares, was philosophical in an interview yesterday with Bloomberg:

“All great technology changes produce bubbles. The reason they produce bubbles is that nobody can get it exactly right. You have to either spend a ton of money to capture your market share and don’t worry about whether it’s too much or not, or you don’t spend enough money and you lose your market share…”

Noting that “bubbles burst when wealth needs to be converted into money", he said that the indicators for a bubble were currently close to the levels seen in 2000 and also in 1929!

Overnight market movements:

The FTSE is set to open down 0.5% at 10,290

S&P 500 is down 0.4% at 7,530

Brent crude is down 1% at $96.35

Gold is up 0.8% at $4,470

Bitcoin is down 1.6% at $64,000

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

MITIE (LON:MTO) (£2.27bn | SR70) | Revenue +10.5%, or +5.3% organically. Operating profit before Other items up 13% to £264m. Actual operating profit £151.4m (FY25: £161.6m). Share buyback programme for FY27 of £100m. “Entering FY27 with confidence in delivering our FY25-FY27 Strategic Plan and continuing growth and margin expansion…” | ||

Great Portland Estates (LON:GPE) (£1.24bn | SR28) | GPE has secured three further lettings at City Tower, EC2, taking leasing of the recently refurbished space to 69%. | ||

CMC Markets (LON:CMCX) (£1.03bn | SR94) | Net operating income +15%. PBT +20% (£101.3m). Positive start to FY2927. Expects FY2027 net operating income to increase by at least 17% year-on-year to £460m - £480m. | AMBER/GREEN (Mark) The bottom line results look like a miss due to higher than expected costs. However, that is dwarfed by the scale of the upgrade in guidance for FY27. My calculations suggest that this is a 30%+ EPS boost. The impact of this is likely to improve both the Value and Momentum Ranks, keeping this firmly as a SuperStock. Despite this positive trend, I still see some risks around volatility normalising and unexpected cost increases. This company has a long history of large cyclical swings in response to changes in NOI and costs, and I don’t see that changing. Hence, I keep our positive view moderated by the obvious risks of investing in a highly cyclical business. | |

Guardian Metal Resources (LON:GMET) (£511m | SR29) | The Tremor Zone is a newly discovered tungsten-skarn zone at one of the Pilot Mountain Tungsten Project's priority exploration targets. The initial discovery drillhole intersected five distinct zones of tungsten-rich skarn mineralisation. | ||

Halo Minerals (LON:HALO) (£301m | SR7) | IPO completed March 2026, raising £5m. Competent Person’s Report led to an NPV10 of US$154.1 million and an IRR of 50.9% (after tax). Outlook: Focus on optimising the DFS, securing ancillary permits and progressing towards Final Investment Decision. | ||

S4 Capital (LON:SFOR) (£290m | SR96) | Full year LfL net revenue is expected to be within the current consensus range of £632m - £663m, down low single digits year-on-year. Like-for-like operational EBITDA margin targeted to increase by at least 100bps. Plans to recommend total dividends of 2.2p for 2026. | ||

Afentra (LON:AET) (£160m | SR54) | Has raised gross proceeds of $40m via a placing. The new shares represent 19.6% of existing share capital. Retail offer to be carried out separately. | AMBER/GREEN (Mark) I am a little surprised by this placing but it is well supported, at a minimal discount and with a retail offer, so I don’t judge it too harshly. | |

Springfield Properties (LON:SPR) (£112m | SR94) | Expects to report revenue of £245m and adjusted PBT in line with market expectations Net cash £1m, (significantly ahead of market expectations). | GREEN ↑ (Graham)

Springfield's share price has come back quite a long way since the interims, down over 20%. And yet earnings forecasts have been stable. The discount to tangible book is now over 30%. So I think this is worth an upgrade to fully GREEN today. I don’t have total conviction in the EPS forecasts, but I think the balance sheet argument is good enough at this stage. | |

Gateley (Holdings) (LON:GTLY) (£91.1m | SR50) | FY26 Revenue +7% to c.£193m. u/l Op Profit £21-22m, in line with consensus. “Whilst our Q4 experienced longer than anticipated transactional cycles as a result of the macro backdrop, we enter FY 27 with good activity levels across transactional and contentious workstreams, and we continue to see attractive mandated and pipeline opportunities across the Group's Platforms.” | ||

Jubilee Metals (LON:JLP) (£90.3m | SR28) | Roan annual maintenance shutdown completed during May 2026, with operations successfully resumed at full capacity targeting run-of-mine throughput of 30ktpm. | ||

Ondine Biomedical (LON:OBI) (£81.4m | SR14) | Revenue +29% to $2.6m, Operating Loss $30.0m (2024: $19.4m), Cash $10.6m (FY24: $9.9m) after $24m fundraise in period. Further $9.2m gross raised after period end. | ||

Aurrigo International (LON:AURR) (£66.1m | SR24) | Revenue -10% to £8.0m, Adj. LBITDA £3.0m (FY24: £1.6m LBITDA), Net Cash £11.5m (FY24: £3.1m) after £13.8m net raise in the period. “While it is early, we are seeing initial signs of stabilisation as performance improves and our actions take effect.” | ||

Premier Miton (LON:PMI) | AuM -13% over 6mo to £9.0bn. Adj. PBT -44% to £3.0m. Interim dividend -50% to 1.5p. Reg Cap Surplus £11.4m (30 Sep 2025: £11.4m). “While it is early, we are seeing initial signs of stabilisation as performance improves and our actions take effect.” | ||

Helium One Global (LON:HE1) (£54.9m | SR35) | The Operator has entered an initial 3mo helium offtake agreement with a major US industrial gases purchaser, covering early production output from the Pinon Canyon Plant. Pricing reflects current US spot markets. | ||

Flowtech Fluidpower (LON:FLO) (£41.9m | SR54) | £0.4m for Helipebs, an award-winning British market leader in the manufacture of hydraulic cylinders and hydraulic technology solutions, paid in cash. | AMBER/RED = (Mark) This deal seems just too good to be true. My suspicion is that some liabilities of the acquired company to its former holdco remain, or it is in severe financial distress, but in reality, we have no idea. In my opinion, management owes shareholders an explanation as to why this looks such a good deal. With this deal creating more questions than an initial look suggests and a significant downgrade in EPS less than 6 months ago, I am in no rush to change our broadly negative view. | |

Neo Energy Metals (LON:NEO) (£23.4m | SR23) | South African Minister of Mineral and Petroleum Resources has not yet granted approval for Phase 1 approvals. Deadlines extended by 6mo. | ||

Switch Metals (LON:SWT) (£16.4m | SR20) | Two high priority hard rock drill targets defined at Issia | ||

Portmeirion (LON:PMP) (£13m | SR50) | £17m gross raised at 50p, almost 50% discount to previous close. New shares will represent 70.8% of the enlarged share capital. “ significant confidence in the medium- and long-term prospects for the Company to create substantial value for our shareholders.” | AMBER ↑ (Mark- I hold) | |

Pennant International (LON:PEN) (£11.2m | SR23) | Auxilium Phase 3 delivers enhanced security and a better user experience. | ||

Altona Rare Earths (LON:REE) (£10.1m | SR14) | All assay results now received from the 2025 drilling campaign. Wide significant intercepts have been observed, with up to 30m at 2,677ppm HREO, and HREO/TREO ratios ranging from 21% to 77%, confirming HREE enrichment is widespread across the Fluorite Zone. |

Graham's Section

Springfield Properties (LON:SPR)

Up 4% at 97.3p (£116m) - Trading Update - Graham - GREEN ↑

This Scottish housebuilder issues a full-year update for FY May 2026.

Key points:

Revenue (£245m) and adjusted PBT in line with expectations.

Net cash £1m, significantly ahead of expectations for year-end net bank debt of £10m.

Checking my notes from February (we were AMBER/GREEN), the expectations at the time included a very large H2 weighting, with 56% of full-year revenues and 65% of full-year EBIT expected in the second half. So it’s nice to see that these forecasts were hit. They are even slightly ahead of the revenue forecast I quoted then.

As for the cash position, I personally wouldn’t read too much into this, as I expect that it’s a volatile figure from month to month. Even so, beating expectations by £11m is not a bad thing, and they’ve made enormous progress on this front: net debt was £93m in November 2023, and £40m at the interims.

SSEN Transmission: we’ve touched on this last time; Springfield has agreed to build and rent 300 homes to SSEN Transmission employees in the North of Scotland. My understanding is that these homes will later be sold.

The outlook for housing in the North of Scotland and in Scotland generally are good:

The Board remains very excited about Springfield's prospects in the North of Scotland. Forecasts for expected housing demand in the region are substantial, which the Group is well-placed to meet thanks to its strong land bank and established position as a housebuilder of scale in the area. The Group is receiving increasing interest from major infrastructure providers who are looking for solutions to their worker accommodation requirements…

Alongside this, the fundamentals of the housing market in Scotland remain strong. There is a critical undersupply of housing across all tenures and the newly formed Scottish Government has reinforced housing as a priority with £4.9bn of investment for affordable housing and £10,000 interest-free shared equity loans to First Time Buyers over the Parliamentary term.

CEO comment: he is “delighted” to have eliminated net bank debt and concludes:

"Our underlying business remains strong, with the achievement of year-on-year growth in private and affordable housing. We also continue to hold significant landholdings in areas of high demand. Accordingly, we continue to believe Springfield is well positioned for the future and we look forward to reporting on our progress."

Estimates

Many thanks to Equity Development for covering this. They have left FY27 and FY28 forecasts unchanged:

FY May 2027: revenue £220.7m, adj. PBT £13.4m

FY May 2028: revenue £206m, adj. PBT £19m

So revenue is expected to decline year-on-year, while adj. PBT continues to rise.

Graham’s view

I think the strongest argument for this share remains centred on the balance sheet. It’s not that I don’t think the earnings numbers are realistic; it’s more that they are far less certain than numbers in hand. Springfield reported tangible net assets of £167m at the interims.

The share price has come back quite a long way since then, down over 20%:

And yet earnings forecasts have been stable:

The discount to tangible book is now over 30%.

In StockRank terms, Springfield is a Super Stock that looks increasingly contrarian (i.e. weak Momentum):

Putting it all together, I think this is worth an upgrade to fully GREEN today.

I don’t have total conviction in the EPS forecasts, but I think the balance sheet argument is good enough at this stage.

Mark's Section

Portmeirion (LON:PMP)

Down 37% at 57p (£13m) - Placing - Mark (I hold) - AMBER ↑

(At the time of writing, Mark has a long position in PMP.)

When I last looked at this company, I viewed it as AMBER/RED, saying:

Perhaps most worryingly net debt is up, they say this is due to order timing (presumably customers trying to beat tariffs) but it reveals that the seasonal peak in debt will typically be after the 30 June balance sheet date here. This has required a revised RCF and that has come at the cost of higher interest, making short-term profitability a further challenge.

However, I recently bought a small position. My thesis was that it would be embarrassing for the Government to announce a package of support measures for the UK ceramics industry and then have one of the most iconic names go bust. However, I was very clear that insolvency was one of the possible outcomes, hence my position size was very small.

So while today/last night’s announcement is better than insolvency, the scale of the raise needed to rebuild the balance sheet means that the company (or probably more likely, their banks) were not willing to wait around for the details of any government support:

…it has conditionally raised gross proceeds of £17.0 million (before fees and expenses) by way of a placing of 34,000,000 ordinary shares… at a price of 50 pence…

It is clear that with a company with a market cap of £13m raising £17m (up from an initial planned £15m) would be a huge dilution. On top of this we have a £2m open offer for existing shareholders (another reason why it was worth risking a small position), making it a £19m raise.

Net debt at 31 Dec was £17.5m and we can normally expect the seasonal peak in debt to be a few £m higher. Fees on a raise of this size are typically around 5% of the amount raised, meaning the net amount is closer to £18m (assuming the open offer is fully subscribed). So we can perhaps still expect a few £m net debt after this raise.

This is what the Chair has to say about the prospects going forward:

We have an experienced senior leadership team in place led by CEO Michael Scheepers, an exciting growth plan for 2027 and beyond, a substantially strengthened financial position and a portfolio of exceptional homeware brands. This gives the Board significant confidence in the medium- and long-term prospects for the Company to create substantial value for our shareholders.

Valuation:

One of the attractions here was the asset backing, with significant inventories on the balance sheet at cost. The company doesn’t reveal their gross margin (presumably to avoid giving customers a target to aim for) so if those inventories are not obsolete, there is considerable value. Part of the failure of previous management has been being unable to reduce those inventories in the face of a downturn in demand and they took an inventory provision in the FY results.

NTAV was £36.1m excluding a probably inaccessible pension surplus, and this will be increased by the net amount of cash raised, say £18m to give a NTAV of around £54m.

There are an additional 38m shares in issue (assuming full take up of the open offer) and there was 14m prior to the raise giving 52m shares in issue. At 60p to buy the proforma market cap is £31.2m, meaning the company still trades at 0.58xTBV. Not quite as good as the 0.33x TBV pre-raise but still showing some potential value.

NTAV is meaningless unless those assets can be made productive. Current forecasts have been suspended so we can’t rely on the figures in the StockReport. However, looking at longer term history, this is a business that can deliver £5-6m PAT in the good years:

This would put the company on a P/E of 5-6, if the current Board’s “significant confidence in the medium- and long-term prospects” is not misplaced.

Mark’s view

This placing rebuilds the balance sheet, and while it comes at the cost of huge dilution, a large discount to TBV remains. The recovery may still take some time, and it would be naive to assume that they will immediately return to prior highs of profitability. However, it remains a strong brand with a long heritage and has received considerable support from new and existing shareholders in the placing. Given that the risk of short-term insolvency has been removed, and there is a potential upside if the new management can return the business to more normal profitability, I think we can risk taking a more neutral view today. AMBER

Flowtech Fluidpower (LON:FLO)

Up 8.5% at 56p (£41.9m) - Acquisition of Helipebs Controls Ltd - Mark - AMBER/RED =

This seems an exceptional deal. This is what they are getting:

Helipebs is an award-winning British market leader in the manufacture of hydraulic cylinders and hydraulic technology solutions, serving some of the world's most technically demanding industries, including energy, aerospace & defence, nuclear and industrial manufacturing….Alongside its UK-based manufacturing capabilities, Helipebs has significant engineering expertise in delivering high-quality engineered solutions to customers globally across sectors including oil & gas, sub-sea, marine, research, green energy, and defence.

And this is what they are paying:

The £0.4m consideration for the Acquisition has been financed from the Group's own cash resources. It is expected that this cost will be fully recouped from customer receipts before the end of FY26. The Acquisition is likely to lead to a bargain purchase gain for the Group, which will be reported as an exceptional item in the current financial period.

Even better:

In the remaining six months of FY26 Flowtech expects the Acquisition to contribute turnover of c.£1.5m and modest positive EBITDA to the Group. For FY27 the Acquisition is expected to deliver turnover of c.£4m and EBITDA of c.£0.5m.

Even if the numbers are relatively small at around 3% of Flowtech’s revenue, paying 0.1x Sales and less than 1xEBITDA just seems too low to me and there must be more going on.

While it is hard to be certain, a quick look at HELIPEBS CONTROLS LIMITED on companies house, shows that at 31 March 2025 they owed group undertakings £2.7m:

Presumably, this is HELIPEBS (HOLDINGS) LIMITED. And while we don’t have up to date accounts, it is clear that Flowtech are buying the subsidiary and not the (former) parent HoldCo and hence they may have agreed to take on some of these liabilities.

If the current financial position is similar, they are still acquiring £700k of inventories and up to £1m of net working capital. However, this just looks like too good a deal for there not to be a further element to it. No one sells a 150 year old high-tech manufacturing business with a great management team for less than 1xEBITDA and 0.1x Sales unless it is in severe financial distress, or the acquirer agrees to take on certain liabilities. In my opinion, management owes shareholders a further explanation on this, either to have given the consideration on a debt-free, cash-free basis, or explain why the seller was willing to virtually give this away.

If my suspicions are correct about there also being some former HoldCo liabilities remaining after acquisition, this turns an exceptional deal into a largely unknown deal. If Helipebs Controls Ltd still owes Helipebs (holdings) Limited £2.7m then the consideration is more like £3.1m or 6.2x EV/EBITDA.

We do know that Flowtech are paying less than Book Value as this will be a bargain purchase gain, and the acquired business had -£400k of equity at 31 March 2025, so perhaps I am completely wrong about still owing the HoldCo. But they could still owe say £1.8m to the HoldCo, and be buying £500k of TBV for £400k with a £100k bargain purchase gain.

Net off £400k cash and in this example, they would be paying a 3.6x multiple, which seems reasonable but not as amazing a deal. The reality is it could be any figure, and if they really are getting this for £0.4m on a cash-free, debt-free basis because it is in severe financial distress, why are they bigging up the management that ran it so close to insolvency?! It just raises more questions than answers.

The market liked this announcement this morning with the share price rising 8.5%. This may just be that shareholders appreciate the activity. However, I can’t help feeling that part of the rise is due to the view that the company has got an amazing deal, and the jury is still out, in my opinion. If it turns out that Flowtech has not paid just £0.4m on a cash-free, debt-free basis, this speaks to management credibility, as I start to wonder what other details are they omitting from statements?

Mark’s view

It’s been a while since we reviewed this company. Just over a year ago, Graham downgraded it to AMBER/RED as the wait for a recovery seemed interminable. Since then the share price has largely gone nowhere, although there has been a modest bounce in the last month:

In January this year, there was a placing, partly to make an acquisition and partly to rebuild the balance sheet. Combined with a warning, this led to a significant downgrade in EPS:

This means they don’t look particularly cheap, especially on an enterprise basis. As such, I’d want them to be exceeding expectations in their next trading update, scheduled for late July, before being willing to upgrade our view. We may even have to wait until half year results are released in September before we get the full story on this acquisition and can take a further judgment on management credibility.

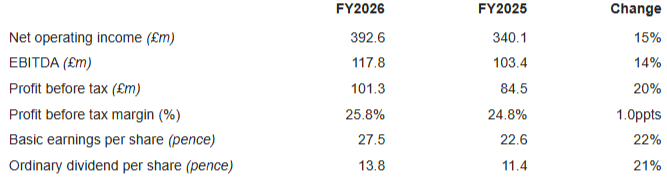

CMC Markets (LON:CMCX)

Up 16% at 428p (£1.03bn) - Preliminary Results - Mark - AMBER/GREEN =

When I wrote a StockPitch article on CMC markets in March this year, I concluded that:

The FY26 setup looks compelling. Record client cash, dynamic hedging, and 24/7 trading mean CMC can capture volatility-related upside better than ever. The macro backdrop - geopolitics, policy uncertainty, AI swings - all suggest that elevated volatility will persist for some time. A largely fixed cost base means that any increase in net operating income will drop straight to the bottom line and drive significant upside beyond current guidance.

The share price at the time was 323p, so it is pleasing to see the market react positively to today’s results, taking the stock up almost 30% since I wrote the article.

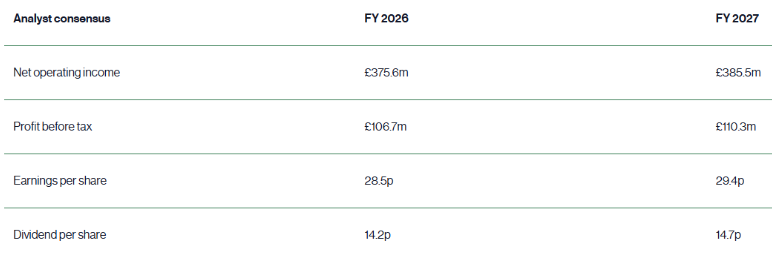

These look strong, with a significant increase in net operating income. We can’t access the broker coverage here. However, the rest of the numbers look like a miss to me. Here is the company’s own consensus from their website:

They don’t appear to have updated this since April, which means it may be somewhat stale. However, the StockReport has 28.1p EPS and 14.7p EPS in for FY26, and these results are slightly behind these.

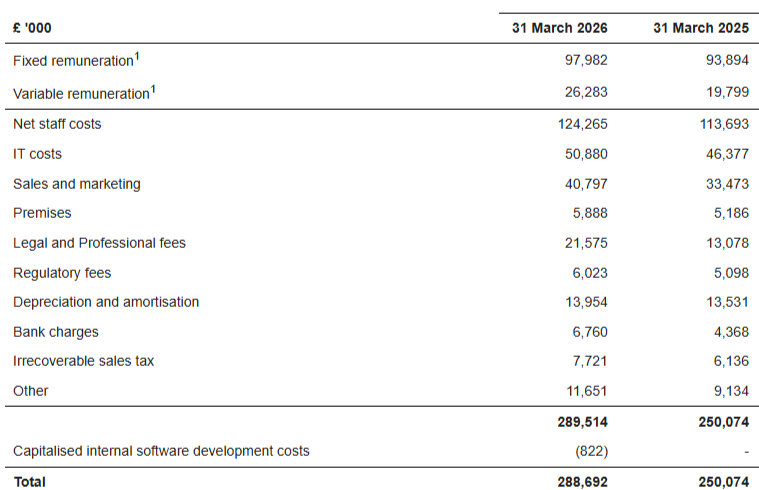

The difference will be due to higher costs, with almost every category seeing some kind of rise:

Outlook:

The market is forward looking, though, and the rise today appears to be due to a big upgrade in forward guidance:

· The Group has made a positive start to FY2027, with net operating income supported by continued momentum across institutional and B2B partnerships, an increasingly diversified product offering and sustained client activity.

· As a result, the Group expects FY2027 net operating income to increase by at least 17% year-on-year to between £460 million and £480 million, with operating costs (excluding variable remuneration) of approximately £280 million.

Net operating income guidance is 15% ahead of the current consensus on the StockReport. If we guessed that variable remuneration came in at around £30m then this would imply £310m total operating costs and £160m operating profit at the mid-point. Interest income is counted with NOI, so with finance costs of around £3m, I would estimate £157m PBT, and £116m PAT on normalised UK tax rates. This is 36% ahead of the consensus on the StockReport. You can see why the market has liked this update today.

Valuation:

If we take my £116m PAT estimate this works out to be around 42p of EPS, meaning that the company is on a relatively modest 10x forward earnings. They would normally pay out half that as dividends for a 5% forward yield. On top of this cash and cash equivalents has increased to around £276m, of which £76m is blocked, meaning that there is up to £200m of unencumbered cash on top of this. In reality, financial firms won’t run the business anywhere close the their regulatory capital limits. However, even if we assume half of this is available for distribution, this makes the P/E look even better.

Caution:

There are some reasons to remain cautious:

The current guidance will presumably be based on continued volatility and risk appetite amongst investors. This tends to be cyclical, and at some point will moderate.

The word salad continues with phrases like Web3 and Defi featuring heavily in their narrative.

IT spend may accelerate. They continue with their “SuperApp” development and the company has a slightly chequered past of delivering large IT projects. A few years ago the company increased costs significantly to develop a non-leveraged trading platform, which as far as I can tell, never delivered any usable product, at least in the UK.

News stories suggest that the company has signed a £30m deal with Everton to be their shirt sponsor, and may do a similar deal with Fullham. It is not clear how long such deals will be for and therefore the yearly cost. However, it seems that marketing spend is due to increase overall going forward.

Overall, given the above, and that they appear to have missed FY26 numbers due to higher than expected costs, I would take the guidance for declining operating costs in FY27 with a pinch of salt.

Mark’s view

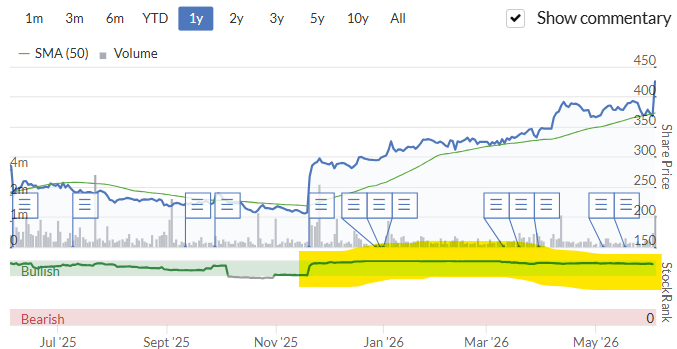

We’ve written extensively on the company on Stockopedia over the last year. However, it was last reviewed on the DSMR in November last year when I upgraded our view to AMBER/GREEN. Since then it has remained a Super Stock and has rewarded investors who have hung on for the ride:

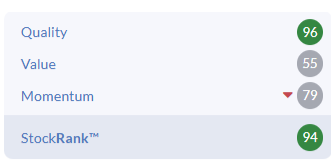

While it remained highly-ranked overall, the lower Value Rank and declining Momentum Rank were perhaps flashing some warning signs:

However, I expect today’s large upgrade and associated share price reaction to rejuvenate these Ranks, and confirm that we should remain positive about the prospects here. Given the scale of the upgrade, it is tempting to go fully GREEN here. However, it remains at the riskier end of investments since any reduction in volatility, or if we saw recent speculative behaviour regarding space and AI stocks abating, we would likely see NOI moderate. Combined with the possibility of increasing costs, this would mean the current positive operation gearing would go into reverse. The company has a history of facing many of these cycles in its past:

So while I don’t see signs of that moderation in the short term, I feel that our rating should still reflect that cyclical risk that will always be present. AMBER/GREEN.

Afentra (LON:AET)

Down 1% at 70p - Equity Fundraising & Retail Offer - Mark - AMBER/GREEN

I am a little surprised by this placing. When I was asked to write up a StockPitch on one of the African oil producers, I chose Afrenta, as it appears to be the pick of the bunch; cheap on current production, and with material development potential. When I wrote the article, I pointed out that they had recently refinanced their debt, saying:

Favourable refinancing: In May 2026, Afentra secured a new US$125m pre-payment facility with commodities trader Gunvor, replacing its existing Reserve-Based Lending and working capital facilities. The new facility extends the maturity profile to 2030 and pays interest at SOFR+6% (improved from SOFR+8%). It also carries a 12-month repayment grace period, giving the company the financial flexibility to fund its drilling campaign.

This is clearly a well-supported raise, with shares representing roughly 20% of the enlarged share capital issued at 67p, just a 5% discount to last night’s close. With $40m gross raised from institutions there is also a £2m retail offer which seems a reasonable compromise, to allow individual investors to avoid excessive dilution. This level is still some 50% above where they started the year.

The reason for the placing is given in the announcement yesterday evening, which is “to accelerate these growth activities and enhance strategic flexibility.” These are how they summarise those activities:

Afentra has a much larger opportunity set within its portfolio that can be accelerated to deliver growth and value accretion for its shareholders, including follow up drilling activity and workovers on Block 3/05, drilling, near-field developments and exploration on Blocks 3/05A and 3/24, and short-cycle production and significant exploration on the Company's material onshore Kwanza basin acreage;

I’m surprised that they have the ability to accelerate what already looks like a fairly tight drilling schedule, so I do wonder if they have their sights on acquiring some further assets and need the flexibility to move quickly.

Mark’s view

We’ve not reviewed this on the DSMR before. When I wrote my Stock pitch article I came away with a broadly positive view of the company. If the oil price remains around current levels, the company should be highly cash generative, and they have some great opportunities to double their WI production over the next few years. However, there are quite a few risks, from operating in Africa to the impact on the company should oil prices fall. Perhaps I should have been a little less surprised that they chose to re-inforce their balance sheet ahead of some material drilling campaigns.

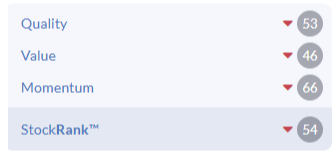

Adding to the concerns, the StockRanks look middling in all respects and have been getting weaker:

However, I think it is worth bearing in mind that if the company gets anywhere close to FY26 forecasts, all of these ranks will be materially higher. Hence, I will go for AMBER/GREEN overall, at least on a relative sector view.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.