Good morning! A special reminder to watch out for false announcements this morning.

Today's Agenda is complete, we think!

1pm: wrapping it up there, thanks everyone.

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

| Travis Perkins (LON:TPK) (£1.1bn) | Full Year Results | Rev -4.7% to 4,607m, with adj op profit -23% to £152m. Management blame price deflation and lower volumes. Outlook is for adj. operating profit to be “broadly flat” in FY25. This appears to be significantly below previous consensus forecasts. | BLACK (AMBER/RED) (Roland) Weak results were aided by some working capital inflows. However, today’s outlook statement appears to equate to a significant cut to previous expectations for FY25. Management believes macro conditions will have to improve to stimulate a recovery – hard to predict right now. In addition, the company is without a CEO, as September’s appointee has resigned due to ill health. I’m inclined to take a mildly negative view at this point as I’m not convinced the shares are especially cheap relative to today’s guidance. |

Greencore (LON:GNC) (£747m) | TU | Strong Q2 revenue & vol growth, driven by new and existing customers. Good cost control has improved profitability. FY25 adj op profit to be ahead of expectations in the range £112-£115m. | GREEN (PINK) (Roland) [no section below] A short but positive update from Greencore this morning. The sandwich and ready meal producer says that “profit conversion” was better than expected in Q2, supporting an upgrade to full-year guidance. This situation is complicated slightly by GNC’s possible interest in acquiring BAKK (I hold). More broadly, GNC is a low-margin business that I’d not want to pay a high P/E multiple for. But earnings forecasts have trended higher over the last year and the P/E of 11 looks reasonable to me. The shares have Super Stock styling and I agree that a positive view makes sense. |

Serica Energy (LON:SQZ) (£525m) | Full Year Results | Rev -21%, PBT -58% to $160m. Final div 10p. Triton exp complete June, FY prod 33-37kboepd. | AMBER/GREEN (PINK) (Roland - I hold) Today’s results show the expected shortfall in revenue and cash flow as a result of last year’s unscheduled outages. We now learn that the current Triton outage is expected to continue to the end of June. In the meantime, the final dividend has been cut to allow more flexibility for field development and M&A spending. I can see the logic in this, assuming that the threshold for return on investment is not diluted. No updated forecasts are available to me today, but the apparent value on offer here suggests a mildly positive view remains appropriate. |

Renew Holdings (LON:RNWH) (£524m) | H1 TU | H1 trading in line with revised expectations. Rail still slow, but lower capex being partly offset by maintenance demand. Water strong with growth potential, energy and infrastructure stable. FY25 adj op profit exp >2024 result of £70.9m. | AMBER (Roland) [no section below] Investors will be relieved that today’s update is in line with revised expectations, following January’s profit warning. There are still some signs of weakness in rail, but other sectors appear to be performing well. Nuclear expertise remains a differentiator here vs listed peers. While there is perhaps still some risk of a further warning, I think the P/E of 10 looks sensible and could justify a closer look. I’m staying neutral out of respect for the recent warning, but I’d hope that May’s H1 results will validate a more positive view. |

Pantheon Infrastructure (LON:PINT) (£449m) | Full Year Results | NAV per share 118.1p (Dec 23: 106.6p). NAV total return 14.3%. Div 4.2p. Agreed first realisation. | GREEN (Graham) Studying this infrastructure investor for the first time, I like what I see with a 20% discount to NAV and good diversification across sectors, although I would like to see a bigger portfolio with a larger collection of individual investments. Valuations are based on DCF forecasts with PINT's cash flows being index-linked in many cases. I'm going to go out on a limb and suggest that the risk/reward looks promising here. |

Pinewood Technologies (LON:PINE) (£325m) | Full Year Results | Revenue +15.1%, adj PBT unchanged at £8.5m. Total users up 6.3% to 35.2k. Rollout at partner Lithia completed. | AMBER/GREEN (Graham) [no section below] (formerly Pendragon - changed its name after sale of dealerships) There is scope for this to grow substantially with 5 of the top 20 UK dealership groups currently supplied by Pinewood and with another major contract announced in February. In addition, the company is preparing to roll out in North America with a new HQ in Florida. So the upside from growth could potentially be very exciting. For now, the PEG ratio is below 1x (only 0.5x according to the StockReport) with a ValueRank of only 10. It is ranked as a High Flyer and I’m going to upgrade it to AMBER/GREEN as the near to medium-term growth prospects strike me as interesting and may justify the current high valuation. |

Niox (LON:NIOX) (£302m) | Full Year Results | Rev +14%, PBT +90% to £7.8m. Takeover discussions at prelim stage. Outlook confident. | PINK |

CLS Holdings (LON:CLI) (£280m) | Full Year Results | Down 6% to 66.2p | AMBER/GRAHAM (Graham) [no section below] I’m taking a moderately positive view on this as I believe this entire sector is undervalued. However, the enormous discount to NAV at play here is causing me concern that serious issues might be hiding under the bonnet. Of course I may be overthinking it. 99% of rent has been collected and they have made some large disposals including a £101m disposal, at values in line with book. More negatively, loan to value is a little high and is above their target range of 35% to 45%, and the underlying vacancy rate is not very good at 10%. However, bad news should be priced in and barring a catastrophe it ought to be too cheap here. More research needed. |

Big Technologies (LON:BIG) (£215m) | Contract award | Contract to provide electronic monitoring in Northern Ireland for 5 years, value £20m. | (Graham) |

Science (LON:SAG) (£192m) | Increased shareholding in Ricardo | SAG now owns 17.3% of RCDO. Average cost 233p. | AMBER/GREEN (Graham) [no section below] |

Peel Hunt (LON:PEEL) (£96m) | FY Trading Update | Rev +5%. Challenging H2. Smaller LBT than expectations. Encouraging pipeline. | GREEN (Graham) I remain positive on this on the basis that the balance sheet should help to support market cap at this valuation. As ever, it's hard to say when a proper recovery in IPOs/M&A will materialise. |

Corero Network Security (LON:CNS) (£86m) | Full Year Results | Rev +10% ($24.6m). EBITDA +42% ($2.5m). Solid start to 2025. |

Graham's Section

Peel Hunt (LON:PEEL)

Unch. at 79p (£97m) - Year End Trading Update - Graham - GREEN

We have a brief full-year update from this boutique investment bank.

Revenues are up 5% to £90m. This appears to be a miss against expectations.

However, the blow is softened with a smaller loss than expected:

This followed a challenging second half with a number of macro-economic events that weighed on market volumes and corporate activity. During the year we took action to reduce costs, and we expect to deliver a smaller loss before tax than market expectations.

I will say that it would have been helpful if the reduced loss could have been estimated in the RNS.

Strategically, they now act for 52 FTSE-350 clients. Checking last year’s update, I see that they reported acting for 150 clients in total, of which 43 were in the FTSE-350. So they are doing well when it comes to attracting more blue-chip customers.

Outlook:

Against a backdrop of continuing slow market conditions, we have an encouraging pipeline of investment banking transactions across both M&A and IPOs. A number of announced M&A transactions are expected to complete in the first quarter of our new financial year.

Graham’s view

I’m starting to think I made a mistake by leaving both Cavendish (LON:CAV) and Peel Hunt (LON:PEEL) on my watchlist this year. Probably I should have just picked one of them.

That said, I still think there’s a lot to be said for Peel Hunt at this valuation.

The most recent half-year report showed net assets of c. £95m, almost entirely tangible. I’d like to think that should provide some support for the current £97m market cap!

Ongoing losses do eat into net assets but at least that blow will be smaller than expected for FY March 2025.

There have been murmurings in the media about a possible increase in corporate activity this year. For example, this recent article in City AM noted 5 IPOs on AIM so far in 2025 (by mid-March), vs. 11 for the entirety of 2024.

So I do expect 2025 to be better for the likes of Peel Hunt, although at this stage it’s not shaping up to be a bumper year by any means. However, the IPO and M&A markets might not be as deathly quiet as they have been in recent times.

The merger of Cenkos and finnCap, creating Cavendish, made good sense to me and I’d be in favour of more deals of that nature, to reduce the number of firms competing for the same business. Because when the recovery finally materialises, I’d like to think that the financial performance of these investment banks will justify the long wait - and weakened competition might help!

A big event that the City has been waiting for is the $50 billion IPO of Shein. It was originally supposed to happen in H1. That timeline was postponed to H2 as the company got to grips with President Trump’s new trade rules.

Bulge bracket banks will be handling Shein’s business, rather than the likes of Peel Hunt, but hopefully this IPO will indeed happen and will help to promote renewed interest in the London market.

Pantheon Infrastructure (LON:PINT)

Unch. at 95.6p (£448m) - Full Year Results - Graham - GREEN

As mentioned recently, I’ve added a new holding to my portfolio - Pantheon International (LON:PIN). This is a private equity investment trust in the FTSE-250, managed by Pantheon Ventures.

PINT is a related entity, also managed within the Pantheon family. But it’s much newer, only launching in 2021.

The description on the website:

Pantheon Infrastructure Plc aims to provide exposure to a global, diversified portfolio of high-quality, infrastructure assets. We will seek to build a portfolio of co-investments in infrastructure assets with strong defensive characteristics, typically benefitting from contracted cash flows, inflation protection and conservative leverage profiles.

The Company is targeting an annual NAV total return of 8-10% and a dividend yield of 4% once fully invested.

Key points from today’s full-year results:

Dec 2024 NAV £553m, equivalent to 118.1p per share.

NAV total return 14.3% for the year (previous year: 10.4%).

Total dividends 4.2p (previous year: 4p).

Sectors in which they are invested: digital (wireless towers, data centres, fibre optic networks), power & utilities (gas, electricity, district heating), renewables & energy efficiency, transport & logistics (ports, rail, road, airports).

So it’s a very broad exposure to all types of infrastructure, despite not yet being a very large trust in terms of AUM. The investment manager says “we do not carry material exposure to any single sector specific risk”.

Chairman comment:

We are pleased to report a strong year for the Company. This performance, during a period of market challenges, reflects the resilience of our portfolio, which remains diversified and well positioned, providing shareholders with unrivalled exposure to assets with proven upside potential, in sectors benefiting from notable tailwinds, meaningful yield, and resilient downside protection.

Graham’s view

While I’m impressed by the returns at PINT, I do think there are some cautionary observations to be made.

Firstly, despite the claim that the company doesn’t take on sector specific risk, the portfolio is not all that well diversified yet. There were 13 investments at the year-end with the largest of them (excluding American electricity company Calpine, which has been sold) being worth close to 10% of their aggregate value.

Secondly, as with all private investments, there is necessarily some trust involved when it comes to the calculation of their value. Valuations for each asset are provided by their individual sponsors:

These valuations are typically calculated on a discounted cash flow (DCF) basis, which are subject to a variety of underlying assumptions that are specific to the sector and characteristics of each Portfolio Company. The degree to which these long-term assumptions change or are adjusted has the potential to impact the Company’s NAV.

The good news is that discounted cash flow valuations should be much more objective than valuations based on earnings multiples.

This chart was published today:

So for example - if you assume a 0.5% increase in interest rates, this takes nearly 2p off of NAV.

In conclusion, I'm leaning towards the view that PINT is potentially a very pleasant investment opportunity with hopefully not too much risk and reasonable prospects of earning an annual return of 8-10%. Even if it can’t quite hit that target every year, it should still beat inflation by a comfortable margin. I note that the cash flows at many of PINT’s investments are index-linked, i.e. having built-in inflation protection.

At a 20% discount to its official NAV I like what I’m seeing. And Pantheon - the broader private equity group, not just PINT - has really impressed me. So I’m giving this a GREEN.

Roland's Section

Serica Energy (LON:SQZ)

Up 4% to 141p (£559m) - Full Year Results - Roland - AMBER/GREEN (PINK)

(At the time of publication, Roland has a long position in SQZ.)

Serica Energy plc (AIM: SQZ), a British independent upstream oil and gas company with operations in the UK North Sea, today announces its audited financial results for the year ended 31 December 2024.

Today’s results from North Sea oil and gas producer Serica were always likely to be a little downbeat, given the impact of the Triton FPSO outages and last year’s lower gas prices.

CEO Chris Cox wastes no time in reminding investors how much better things could be if the Triton FPSO (which is not operated by Serica) was working properly:

The highly positive results of the drilling campaign at Triton are not yet being reflected in our production and cashflow due to ongoing issues at the Triton FPSO. Our frustration is exacerbated by the fact that the Triton area alone could be delivering up to 30,000 boepd net to Serica with the addition of the wells already drilled.

Mark and I have both covered Serica quite regularly in recent months, so I’ll try to focus on what’s new in today’s results.

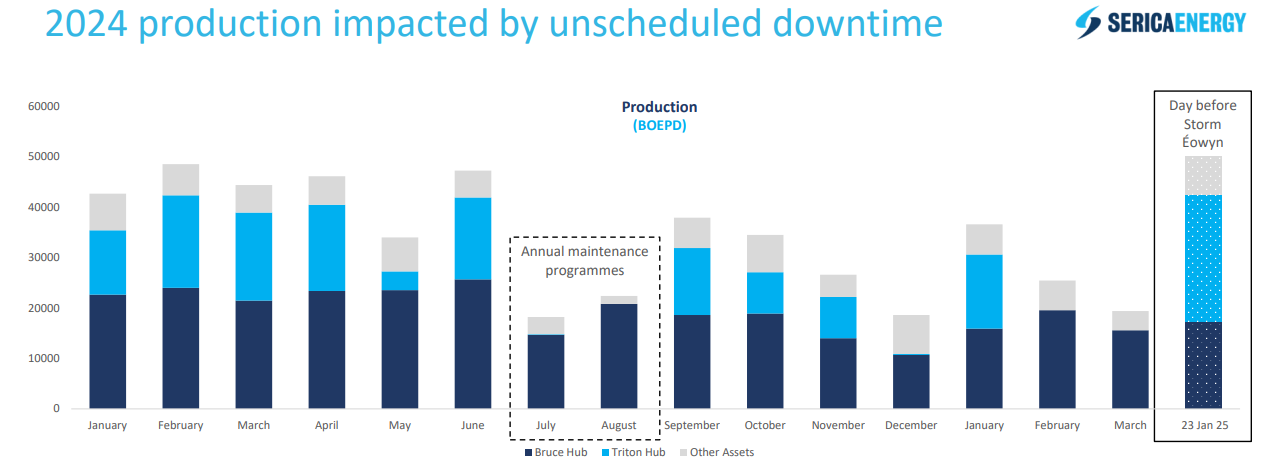

2024 financial summary: last year’s financial performance was adversely affected by the combination of various unscheduled outages, mainly at Triton, and lower gas prices. For a quarter of the year, Triton produced nothing at all:

Here are some of the key numbers from today’s results:

Revenue down 20.7% to $727m

Operating costs up 20.8% to $330m

Capital expenditure up 168% to $260m

Pre-tax profit down 57.9% to $160m

Cash tax paid: $153m (2023: $348m)

Free cash flow: $(1m) (2023: $16m)

Adjusted net debt: $(83m) (2023: adj net cash of $99m)

These numbers do deserve some explanation. Free cash flow would obviously have been significantly stronger without last year’s Triton outages.

In addition, Serica ended up overpaying tax last year and expects to receive a $71m cash tax rebate in 2025 that will aid cash generation. Overall cash tax payments are expected to be “significantly reduced” in 2025.

In terms of production, here are the key numbers:

Production down 13.7% to 34,600 boepd

Average realised Brent oil price: $75/bbl (2023: $67/bbl)

Average realised gas price: 76p/therm (2023: 94p/therm)

One key attraction for many shareholders here, including me, is the generous dividend on offer. Today’s results offer mixed news on that front.

Dividend & shareholder returns: the total spent on dividends and buybacks last year was broadly unchanged, at $114m. But Serica has cut its final dividend today to provide more flexibility to allocate capital to M&A, development programmes or buybacks, as suitable opportunities arise.

Final dividend: 10p (2023: 14p)

Total dividend: 19p (2023: 24p)

Assuming a 19p payout for 2025, the shares offer a potential 13.5% yield at current levels. I’m only guessing, but I would not be surprised to see this further reduced by increased buybacks. With the shares trading below book value, this could offer value for shareholders.

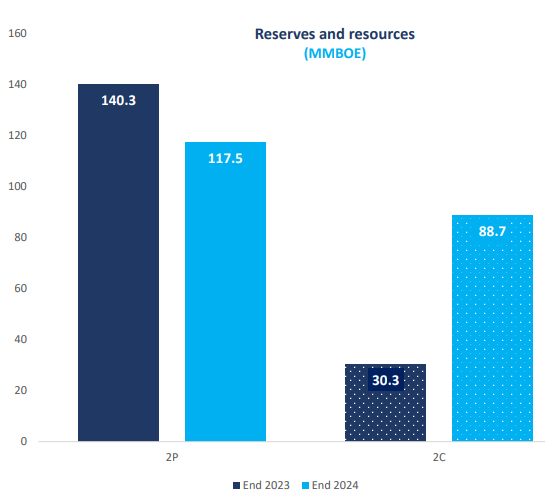

More broadly, my feeling is that the dividend cut has also been driven by a shift in the shape of Serica’s resource portfolio. Last year saw a fall in reserves (assets available for commercial production), but a large increase in contingent resources (discovered assets that require further development).

The company hasn’t been replacing its reserves fast enough to offset production. To put a number to this, last year’s production of 34.6kboepd is equivalent to around 12.6mmboe per year.

So with production at 34.6k, reserves remaining fell from 11.1 years to 9.3 years in 2024. Of course, without the Triton outages, the decline in reserves would have been greater:

I think the company is also keen to do more acquisitions in the region in order to strengthen its position as a consolidator and gain further tax and scale benefits.

Over time, spending more now could lengthen the producing lifespan of the group’s portfolio. Of course, future spending may not deliver the attractive returns of past spending – this is where we have to trust management not to squander cash on empire building (rather than simply returning it to shareholders and winding down the business).

Triton FPSO: repair work on Triton is now expected to complete “at the end of June”, meaning that it will have been offline for around five months. The only silver lining here is that the previously scheduled summer maintenance will also be carried out during the repair period, so no further outages will be scheduled for the remainder of the year.

As a result, Serica expects a significant H2 weighting to production (and potentially to profits):

With maintenance work at the Triton FPSO set to complete in June, and no summer shutdown to then follow, portfolio production in H2 is forecast to be materially ahead of the full-year 2025 guidance range

2025 guidance: Serica’s 2025 production outlook has been a tail of woe. Today we have another downgrade due to the extended Triton FPSO outage:

Following operational issues at Triton in Q1, production guidance for 2025 has been amended to 33,000-37,000 boepd

For context, here’s the history of 2025 guidance:

7 Jan 25: production net to Serica running at 46,400 boepd

21 Jan 25: FY25 production guidance for “around 40,000 boepd”, reflecting planned maintenance

18 Feb 25: January 2025: averaged 37,000 boepd, February 2025: “averaging 27kboepd to date”

In fairness, the Triton issues are out of Serica’s control. And the group’s portfolio does have the latent capacity to produce at a far higher level (my emphasis):

With all assets producing, our portfolio is capable of delivering over 50,000 boepd. Issues at Triton during the first quarter which, albeit different, compound on the challenges of Q4 2024, mean that we have been a long way from our production potential in the first quarter, and our production guidance for 2025 has today been set at a revised range of 33,000 to 37,000 boepd. Given the potential flow rates, a period of stable production will help us to strive for the top end of this range.

Outlook: unfortunately I don’t have access to any updated broker notes for Serica today, so I can’t see how estimates have changed as a result of today’s updated production guidance.

Forecasts from Auctus Advisors in February suggested Serica could generate $187m of free cash flow in 2025 – equivalent to around 37p per share. That’s equivalent to a P/FCF of 4.

Whether this is still achievable will depend on oil and gas prices and the extent of the production recovery in H2. But even a reduction would leave SQZ shares looking very cheap relative to cash flow.

Roland’s view

Today’s share price reaction suggests investors are slightly more positive about today’s results than I am.

Serica shares certainly still look attractively valued to me at current levels, with a potential double-digit dividend yield and low single-digit P/E.

In addition, there’s still the prospect of an all-share merger or takeover with Enquest. I would expect this to deliver reasonable value to Serica shareholders, given that commodity group Mercuria is the company’s largest shareholder (24.7%).

On balance I’m going to maintain our AMBER/GREEN view due to the apparent value on offer here. But I would caveat this with heightened uncertainty about the outlook for 2025.

Travis Perkins (LON:TPK)

Down 7% to 511p (£1.1bn) - Full Year Results - Roland - AMBER/RED

Travis Perkins plc, the UK’s largest distributor of building materials, announces its full year results for the year to 31 December 2024

Last week, we had downbeat results from Kingfisher, which owns B&Q and Screwfix. Today we have further evidence from builders’ merchanting group Travis Perkins that conditions in this sector remain tough.

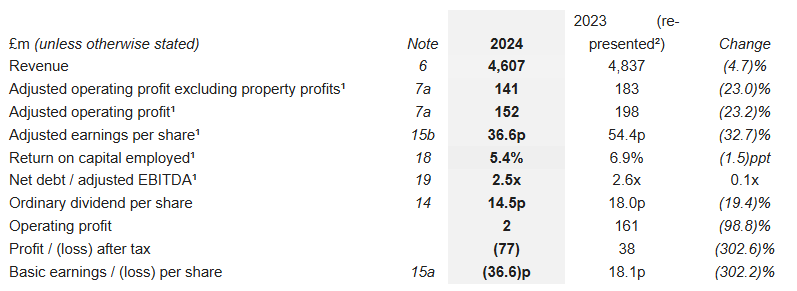

2024 results summary: all the numbers are moving in the wrong direction here, as Travis Perkins reports a nasty combination of falling volumes and price deflation. That’s hard for a low-margin, volume-driven business to combat:

At an adjusted level, operating margins fell from 4.1% to 3.3% last year.

But to give credit to Travis Perkins, today’s results do also highlight a couple of (relatively) positive points.

Operating costs fell by 5.2% to £1,051m last year, presumably due to cost savings and the impact of lower volumes (e.g. lower delivery costs);

The group was also still able to generate free cash flow of £125m, giving a matching £123m reduction in net debt. This was achieved through careful management of working capital (£64m inventory reduction) and capital expenditure. But in a market like this, it’s a sensible (if one-off) win.

Net debt: at a statutory level, the business looks quite highly geared.

Net debt of 845m (including leases) was 2.5x EBITDA at the end of 2024, although net debt falls to £191m (0.6x EBITDA) if leases are excluded.

Statutory leverage still appears to be well below the covenant level of 4x EBITDA, but this is clearly an area management is focusing on.

Checking the balance sheet shows net lease liabilities of £109m, which suggests some sites may not be operating profitably at the moment, relative to their lease costs. This deficit could reverse in an upturn but is a possible source of cash leakage over the coming years as things stand.

CEO departure: unfortunately, former CEO Pete Redfern resigned on 10 March 2025 due to ill health. Redfern only took up the role in September 2024, so the business could also be suffering from a lack of consistent leadership.

The CEO role is being covered by chair Geoff Drabble while a search is underway for a new CEO. Drabble only joined TPK as chair in October, but was CEO of FTSE 100 equipment hire group Ashstead from 2006-2019. So he has an impressive pedigree in this sector.

Outlook: Kingfisher’s strongest performing business is Screwfix and the situation is similar here, with TPK’s Toolstation chain outperforming the core merchanting business:

The Group has experienced a mixed start to 2025. Trading conditions have continued to be challenging in our Merchanting businesses with pricing now stabilised but volumes in modest decline. By contrast, Toolstation has started the year more positively and continues to deliver good growth.

The company says it’s seeing some pockets of improvement, but management note that further cuts to interest rates and improved consumer confidence are needed to stimulate “a meaningful increase in demand”.

Guidance for the year ahead is for FY25 adjusted operating profit to be broadly in line with FY24, excluding any profits from property disposals.

This appears to be below previous City expectations, based on previous consensus forecasts on Stocko for a strong recovery in earnings this year:

Roland’s view

Profits were heavily adjusted last year, due to impairment charges and other factors. Adjusted operating profit of £151.8m translated into statutory operating profit of just £2.3m.

Likewise, the strong free cash flow showing seems to have been due to a large reduction in inventory that I suspect is a one-time gain.

All of this makes it hard for me to guess what the likely cash performance of the business will be this year.

However, using today’s adjusted earnings of 36.6p as a guide translates to a possible FY25E P/E of around 14, after today’s share price drop.

This doesn’t immediately strike me as good value, unless you have a strong conviction that market conditions will soon start to improve.

I’m not sure I’m that confident, so I’m going to take a mildly negative view today, to reflect today’s weak results and outlook.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.