Good morning! Welcome to Tuesday's report.

Spreadsheet accompanying this report: link.

The Agenda is complete.

12.45pm: we are out of time for today, see you tomorrow!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Ashtead (LON:AHT) (£18.8bn) | Rev -1% (used equipment sales lower). Adj. EPS -4%. Guidance: rental revenue +0% to +4%. | ||

Legal & General (LON:LGEN) (£14.8bn) | Webcast at 1pm. Also: “we have made a good start to 2025”, core operating EPS growth of 6-9%. | ||

Informa (LON:INF) (£10.5bn) | Five months: underlying revenues +9.3%. Visibility is ahead of last year. Growth guidance reaffirmed. | ||

Morgan Sindall (LON:MGNS) (£1.8bn) | Group PBT is expected to be significantly ahead of previous expectations. | AMBER/GREEN (Roland) I rate this construction group as a best-in-sector operator and believe it could be a wider beneficiary of the recent UK government spending review. But the valuation is now above its normal range and previous forecasts have suggested some risk that earnings growth could slow next year. Perhaps out of an abundance of caution, I’ve moderated our view slightly today. | |

Metro Bank Holdings (LON:MTRO) (£893m) | Press reports of takeover approach (no RNS) | Sky News reported on Saturday that Metro Bank has received takeover interest from private equity firm Pollen Street Capital. | PINK (AMBER/GREEN) (Graham) There’s still no RNS since Sky News reported on this. I guess the lack of an RNS means that any offer received so far has been rejected by the Metro board? We’ve been moderately positive on MTRO while the price has multi-bagged from the depressed levels it reached when its solvency was questionable. It was successfully refinanced and continues to offer cheapness against tangible book value. As such, I see no reason to change my stance today. I'm in good company, with the highly knowledgeable financial investors at Pollen Street now apparently also finding it interesting around these levels. |

| Ocean Wilsons Holdings (LON:OCN) (£522m) | Possible Combination | Proposed all-share combo with OCN’s largest (26%) shareholder. Would remain a listed investment co. OCN shareholders to receive HAN/HANA shares in accordance with the NAVs of each company at the end of June. Separately, OCN also offers to buy back shares for up to £123m, at a discount to NAV. | PINK (GREEN) (Graham) I was AMBER/GREEN on this in the absence of any particular catalyst to close OCN's discount to NAV. While there is still no guarantee that the discount will close further, the tender offer (at a discount to NAV) could help. The proposed merger with HAN/HANA may also help, as it comes with a lower management fee and will create a much larger, simpler entity that will be harder for prospective investors to ignore and to put on a very large discount to NAV. HAN currently trades at a c. 38% discount to NAV. Surely this must tighten up? |

ITM Power (LON:ITM) (£453m) | ITM to deploy “POSEIDON” into two projects aiming to supply local industries with green hydrogen. | ||

Warpaint London (LON:W7L) (£361m) | Confident will meet exps for 2025. H1 sales exp £50-£52m (H1 24: £45.9m). | AMBER/GREEN (Roland) [no section below] | |

RWS Holdings (LON:RWS) (£315m) | Rev -2%, adj. PBT -61% (£18m), loss-making. Outlook in line. Adj. PBT £60-70m if GBPUSD is 1.33. A new divisional structure will launch in October to simplify the business and align RWS’s products and services more closely with current market needs. | AMBER/GREEN (Roland - I hold) Today’s interim results are firmly in line with April’s revised guidance and reiterate full-year expectations. While profits are down sharply, I’m encouraged by strong free cash flow conversion and am cautiously optimistic about the new CEO’s plans. With revenue broadly stable and the stock on a P/E of 6, only a small improvement in profitability might be needed to support a recovery in profits and a re-rating. RWS isn’t without risk, but I remain confident in the business model and think the risk-reward balance could be attractive. A tentative upgrade. | |

| Capita (LON:CPI) (£284m) | Trading Update | Reiterating full year guidance of broadly flat revenue, op margin improvement weighted to H2. | |

B.P. Marsh & Partners (LON:BPM) (£255m) | £1.7m investment in Cameron Specialty HoldCo, a London commercial property underwriter. The investment is a mixture of equity and a loan facility. | GREEN (Graham) [no section below] This is a small investment by BPM’s current standards, but it’s good to see that they continue to put their large cash balance to use within their insurance niche. They had £74m as of January 2025, and already made £20m of new investments, with buybacks and £8m of dividends also planned. I examined BPM’s full year results recently and concluded that the shares are about as attractive as ever at current levels. | |

Brickability (LON:BRCK) (£218m) | Director/PDMR Shareholding (Monday RNS) | MD of Distribution Division sold 3m shares and now has 16m. NED sold 1m, now has 2m. | |

Montanaro UK Smaller Companies Investment Trust (LON:MTU) (£134m) | NAVps -11% to 105.9p. Discount reduced to 8.4%. Divi +17.4% to 5.4p. Portfolio turnover 45.6%. | AMBER (Graham) [no section below] This smaller companies trust looks at many of the same companies we do. Its largest holdings are discoverIE, XPS Pensions and Big Yellow. However, the cumulative returns figures as presented in today’s highlights table doesn’t look great: 14% over five years and 30% over 10 years, versus 68% and 60% by their benchmark over the same timeframes. NAV has fallen 7% over the past year. While management do acknowledge some individual stocks that distracted from performance, I don’t see any admission that they themselves made any mistakes. They appear to blame management at one or two companies they invested in, and they also blame “style” underperformance, with growth companies generally underperforming value companies last year. Investment managers should openly acknowledge their mistakes, and so I can’t get above a neutral stance on this despite it trading at a 10%+ discount to NAV. | |

Anexo (LON:ANX) (£80 m) | Deadline for firm offer from DBAY Advisors extended to 5pm on 1 July 2025. | PINK | |

Hercules (LON:HERC) (£37m) | Rev +18%, adj PBT +55% to £1.7m. Cash £9.8m. Outlook: confident in meeting FY exps. | ||

RC Fornax (LON:RCFX) (£29m) | PW: FY25 results to be significantly below exps. Revenue >£4.0m (prev. £11.5m). House broker Cavendish has cut FY25 forecast earnings from 3.2p to a loss of 2.2p per share. Perhaps even more tellingly, the broker has placed its target price and FY26/7 forecasts under review. | BLACK/(RED) (Roland) [no section below] | |

Wynnstay Properties (LON:WSP) (£23m) | Rental income +5.4%, net property income +5.2% to £1.9m. NAV per share +2.8% to 1,168p. | ||

| Altitude (LON:ALT) (£17m) | Board Change and Trading Update | CFO stepped down from board, will leave post FY25 results. FY26 trading in line with exps. | AMBER (Graham) [no section] I noted last year that the company’s expectations for FY March 2025 implied a large H2 weighting, and I wasn’t sure if it was achievable. The company did subsequently announce a revenue and profits warning. With FY26 trading in line, let’s hope that forecasts are now more realistic. I remain to be convinced that this is a company of above average quality, so I’m staying neutral. |

Safestay (LON:SSTY) (£16m) | Confirms that it is considering the sale of some UK freehold assets. No certainty of a deal at this point. | AMBER (Roland) [no section below] | |

Sound Energy (LON:SOU) (£14m) | Completion of regional screening for hydrogen with Getech (LON:GTC). Signed JV with Gaia Energy for 270MW of solar project in Morocco. |

Graham's Section

Ocean Wilsons Holdings (LON:OCN)

Up 5% to £15.60 (£552m) - Possible Combination - Graham - GREEN

It’s fortunate that I studied OCN recently, so its broad features are fresh in my memory.

I described its portfolio as “a highly diversified fund of equity funds”.

The investment manager for the portfolio is Hanseatic Asset Management, which is related to OCN’s largest shareholder, Hansa Capital Partners.

That relationship has led to the following proposal.

.. possible all-share combination of Hansa and Ocean Wilsons, under which Hansa would acquire the entire issued and to be issued share capital of Ocean Wilsons (the "Possible Combination").

It will be a merger of OCN with Hansa Investment (LON:HAN) and Hansa Investment (LON:HAN)A. (“HAN” are the voting shares, while “HANA” are the non-voting “A” shares.)

It’s described as “a compelling long-term opportunity for shareholders by combining two companies with complementary portfolios to create an investment company with total net assets of in excess of £900 million under a simplified group structure (the "Combined Group").”

Shareholders will enjoy “the benefits and synergies of greater scale, including through a reduced blended management fee”.

Hansa and Ocean Wilsons have “complementary investment portfolios which have similar investment objectives”.

Importantly, the proposal “has the support of the long-term, strategic shareholders of both Hansa and Ocean Wilsons”.

Terms of proposal: OCN shareholders would receive one HAN share for every two HANA shares they receive, in line with the currently existing ratio of HAN to HANA shares. The number of shares they receive will be calculated based on the net asset value of each company as at June 30th 2025.

The combined group will continue to use Hansa’s existing listing.

The fee charged by Hansa to manage the portfolio will be will be “0.8% of Hansa's NAV up to £500 million and 0.7% thereafter, as compared to the existing management fee of 1.0% currently payable by each of Hansa and Ocean Wilsons…and eliminates the additional performance fee that forms part of Ocean Wilsons' existing management fee arrangements.”

Graham’s view

I’m seeing very little to dislike here.

With any investment product - including investment companies - simplicity is better than complexity.

OCN took a major step towards simplification by selling its stake in Wilson Sons.

That sale - worth about £447m based on exchange rates I calculated recently - resulted in an implied net asset value per OCN share of $27.20 (£21.06).

It also resulted in a huge uplift in OCN’s cash balance, and the company announces today that it is returning up to £123m to shareholders via a tender offer.

OCN’s major shareholders have pledged not to tender any shares, so it’s only the smaller shareholders - owning 40% of the company - who may tender.

However, there is a good reason the larger shareholders aren’t getting involved: the tender offer is taking place within a price range of 1543p - 1736p.

This is a premium to recent prices at which the stock has traded, but is still significantly below NAV:

So personally, if I liked their investment strategy and owned shares in OCN, I’d be reluctant to tender many shares.

Looking forward, it seems to me that the combination of HAN/HANA and OCN should help to grow HAN’s prominence in the investment company landscape.

It will be a much simpler proposition from now on, simply owning a portfolio of funds. Prospective HAN investors won’t have to try to understand the large shareholding in OCN.

OCN investors are already benefiting from the simplicity of no longer owning the Brazilian shipping company Wilson Sons. The combination with HAN/HANA, if it goes ahead, will also see them benefiting from lower management fees and larger scale.

And I do expect the proposal to go ahead.

I'm going to upgrade my stance on OCN to GREEN as the value of its NAV will be reflected in the number of HAN/HANA shares that its shareholders receive. Its NAV is already £21.06, according to the last quarterly update, and could be boosted further by the tender offer purchasing shares below NAV. Against a share price of £15.60, this looks quite attractive to me.

I note that HAN's own discount to NAV is currently very wide at 38%. But surely this must tighten up if this merger goes ahead?

Roland's Section

Morgan Sindall (LON:MGNS)

Up 15% to 4,430p (£2.1bn) - Trading Update and Outlook for 2025 - Roland - AMBER/GREEN

Today we have another upgrade from this well-run and founder-led construction group, which I tend to view as the best listed business in this sector in the UK.

The main headline is short but sweet:

Group PBT is now expected to be significantly ahead of previous expectations.

This is the latest in a string of upgrades over the last 18 months that have increased 2025 EPS estimates by 14% (prior to today):

Management says that two of the group’s divisions have been outperforming, driving today’s upgrade:

Fit Out: strong trading earlier this year has continued, providing good visibility for the remainder of the year. Profits expected to significantly exceed previous expectations.

Construction: operating margin is now expected to be in the middle of the target range (3.0%-3.5%), with revenue above previous expectations. As a result, profits are expected to exceed expectations.

The group’s other divisions are all said to be trading in line with expectations, hence today’s upgrade.

Outlook & Estimates: The extent of today’s upgrade isn’t clear, but use of the word “significantly” suggests to me it could be in the region of 10%.

Unfortunately I don’t have access to broker forecasts for Morgan Sindall, so we’ll have to wait for upgrades to filter through to Stockopedia’s consensus estimates.

Roland’s view

I’ve been singing the praises of this business for several years, but have sadly failed to follow my own advice. Shareholders who have stayed invested through some volatile periods have enjoyed a multibagger:

On the assumption that today’s update is equivalent to a c.10% increase in FY25 earnings per share, then I estimate Morgan Sindall could be trading on a forward P/E of 13-14 after today’s news.

This isn’t cheap for what remains a low-margin business, but Morgan Sindall is extremely well run (in my view) and has avoided the contract pitfalls and other financial disasters that seem to periodically befall its rivals.

Quality metrics other than margin are excellent, as is cash generation (financial management is very tight):

More broadly, my impression is that Morgan Sindall’s various divisions may be well positioned to benefit from increased government spending following the recent review. Examples might include affordable housing, healthcare and education.

In March I was GREEN on Morgan Sindall and Graham maintained this view at the start of May. However, the shares have become more expensive since then and are now trading a little above their normal range:

While I have confidence in the company’s ability to deliver on its promises, Morgan Sindall’s valuation metrics are starting to look less appealing to me than previously.

It may also be worth remembering that prior to today, analysts were forecasting a fairly flat outlook for earnings in FY26. I don’t know if this is still valid, but I think it’s worth considering.

While I continue to regard this company highly, I’m going to trim our view to AMBER/GREEN today on valuation grounds.

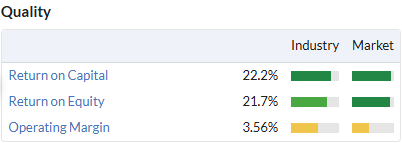

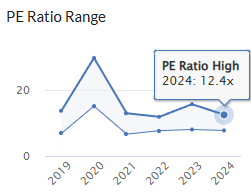

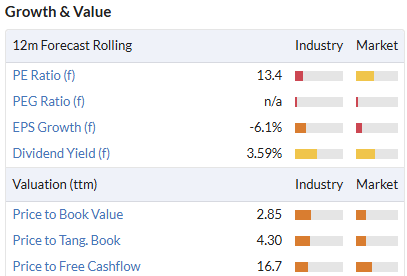

RWS Holdings (LON:RWS)

Up 6% to 90p (£333m) - Half-Year Report - Roland - AMBER/GREEN

At the time of publication, Roland has a long position in RWS.

The headline numbers in today’s interim results from translation specialist RWS look dire, but we already knew that would be the case following April’s profit warning. Today’s numbers are in line with April’s guidance.

The big question now is what happens next. Can new CEO Ben Faes stabilise performance, control rampant IT spending and return the business to growth in a market that’s being disrupted by AI?

The first key takeaway from today’s results is that things have not worsened since April. Guidance for the full year (y/e 30 Sept) is unchanged (my emphasis)

The Group continues to expect to deliver adjusted PBT in the range of £60m-70m for FY25, as previously guided, based on an H2 GBP / USD FX rate of 1.33

Let’s take a closer look at today’s numbers and the company’s revised strategy.

H1 results - key points: revenue for the half year fell by 2% to £344m, while adjusted pre-tax profit dropped 61% to £18.0m.

On a reported basis, RWS made a pre-tax loss of £12.7m for the period. This was due to various adjusting items including amortisation of acquired intangibles, acquisition-related costs, share-based payments and restructuring costs.

I would normally be inclined to include most of these costs in my measure of profitability. However, in the interests of balance I think it’s worth noting that free cash flow for the half year was £17.6m, excluding acquisitions and disposals. This is almost identical to adjusted pre-tax profit for H1.

I think this FCF performance supports the view that RWS is still highly cash generative. On an annualised basis, I estimate RWS could have a free cash flow yield comfortably in excess of 10%.

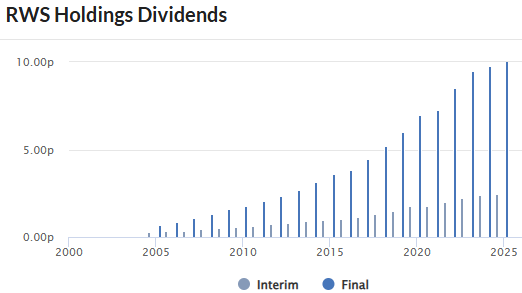

A £14.1m increase in net debt to £27m reflects the payment of the £36.9m final dividend during H1 – this wasn’t fully covered by last year’s free cash flow.

Dividend: the interim dividend was held at 2.45p, suggesting that (for now), RWS is protecting its enviable track record:

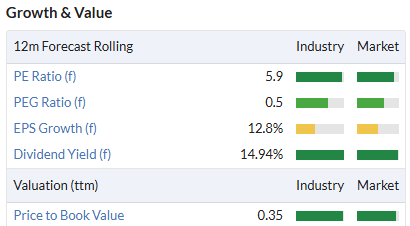

If the final dividend is held unchanged this year, the stock currently yields a tempting 14%!

Divisional performance: three of the group’s four divisions reported revenue growth on an organic constant currency (OCC) basis. This continues the improvement seen during the second half of last year:

Language Services: revenue of £158.4m (OCC +4%), adj op profit -58% to £6.4m (4.0% margin)

The company says the fall in profit was driven by increased competition on price. This is said to be primarily in the non-West Cost technology part of the division. My reading of this is that RWS’s Silicon Valley AI customers are paying good rates for the company’s AI training expertise, but pricing on localisation services are under pressure elsewhere. This is what I might expect, given growth in availability of lower-cost AI-driven translation tools.

I wonder if there’s a risk that RWS will eventually make itself redundant, however, by providing AI training services to big tech customers.

Regulated Industries: revenue of £65.6m (OCC -7%), ad op profit -64% to £2.7m (4.2% margin)

This division is continuing to suffer from reduced activity in finance and legal, plus “a larger decline” in our linguistic validation business in H1. Oddly, the latter is said to be due to management changes last year – it looks to me like something has gone wrong, but this situation is now said to have been addressed.

H2 is expected to be stronger, in particular in life sciences.

Language & Content Technology: revenue £71.2m (OCC +6%), adj op profit -33% to £8.5m (12% margin)

This division supplies the technology products used by clients for their own translation. Flagship translation products are Language Weaver (Machine Translation) and Trados. Other key products for broader content management are Tridion, Contenta and Propylon.

It also includes the in-house Evolve AI translation tool, which now offers 27 language pairs and is continually improved through input from human editing.

Language Weaver and Propylon were the main drivers of revenue growth. Like many software companies, this business is shifting to a subscription fee model and the company says such payments now account for 43% of total licence revenue, from 39% last year.

IP Services: revenue £49.1m (OCC +1%), adj op profit -10% to £10.5m (21% margin)

This division is the original RWS business and is a world leader in patent translation and related services. The appeal of this specialised, expert business is reflected in its margins, which stayed over 20% even in a difficult year.

Performance in the APAC region is said to have been particularly strong, thanks to a significant new win with “a major Chinese online retailer”.

Restructuring/New Strategy: these four divisions reflect the group’s historic core business and later acquisitions. New CEO Ben Faes has decided that a restructuring is needed to reflect the rapid pace of change in technology and to align RWS’s offering with the broader global content market.

From 1 October, RWS will reorganise its operations into three units:

Generate: content technology and TrainAI businesses

Transform: localization businesses, including language technologies as well as services

Protect: IP Services business

Outlook: as mentioned already, guidance for the full year is unchanged. RWS expects to deliver modest OCC revenue growth during the second half of the year, leading to a full-year adjusted pre-tax profit of £60-70m, based on a USD/GBP rate of 1.33.

I don’t have access to broker forecasts for RWS, but I don’t expect too much to change given the firmly in line nature of today’s results.

Mr Faes plans to provide new medium-term targets and more detail on his strategy with the company’s full-year results in December.

Roland’s view

There are signs that RWS’s customers are continuing to value its services. Client retention levels were 94% in H1, with a record Net Promoter Score (NPS) of +51 for the 12 months to 31 March 2025. New work was secured “across all divisions and in a wide range of end markets”.

Some of the slump in profits during H1 is said to be due to changes needed to accommodate new clients and perhaps address some previous mis-steps. I think that margins in the Language Services businesses may reset permanently below historic peaks, but increased volume potential may help to offset this.

Remarkably (and slightly depressingly, in my view), RWS claims that more content has been created in the last 18 months than the previous 30 years. For large organisations, managing this and ensuring customers can engage with this content will be a key commercial requirement – this is where I believe RWS has a competitive opportunity.

The risk, as always, is that I’ve completely underestimated the scale of technological change and that having shared and commoditised much of its expertise, RWS may end up making itself redundant (or unable to maintain the necessary pace of expenditure).

The very cheap valuation certainly suggests many investors remain sceptical:

However, the recent share price recovery seems to support Mark’s view that the April sell-off may have been overdone:

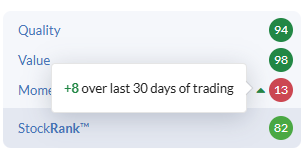

I am broadly reassured by today’s results. I note the stock’s MomentumRank has also started to creep up recently:

Noting the stock’s Contrarian styling and high QV ranks, I am going to stick my neck out and tentatively upgrade our view here to AMBER/GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.