Good morning! The Agenda is complete now.

12.30pm: all done for now, thank you.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

BHP (LON:BHP) (£104.9bn) | Interim Results | HY25 rev -8% to $25.3bn, adj profit -23% to $5.1bn. $2.5bn interim dividend. | |

Anglo American (LON:AAL) (£33.1bn) | Sale of Nickel business | Anglo has agreed to sell its Brazil-based nickel operations for “up to $500m”. | |

Antofagasta (LON:ANTO) (£18.1bn) | Final Results | 2024 rev +5% to $6.6bn, PBT +5% to $2.1bn. 2025 guidance unchanged. | |

Intercontinental Hotels (LON:IHG) (£17.0bn) | Final Results | 2024 rev +6% to $4.9bn, adj op profit +10% to $1.1bn. RevPAR +3.0%. Confident outlook. | |

Plus500 (LON:PLUS) (£2.1bn) | Preliminary Results | Rev +6%, EBITDA +1% ($342m). $110m buyback & $90m in divis. “Extremely well positioned”. | GREEN (Graham) Investors are being asked to trust the strategy of spending big on customer acquisition, with the view that it will pay off in future periods. Additionally, 2025 looks like it could be a quieter financial year, with less trading activity. But the long-term picture is one of tremendous growth and expansion and that continues today most notably in the United States, UAE and Japan. More than 1/3 of the market cap is covered by cash and PLUS continues to buy back its own shares. |

Assura (LON:AGR) (£1.4bn) | Statement re. Possible offer from KKR | The board believes KKR’s offer “materially undervalued the company” and thus rejected it. | AMBER/GREEN (Graham) No change to my view expressed yesterday with the shares offering both a discount to NAV and an attractive yield. Deleveraging could help to boost investor confidence. |

Serica Energy (LON:SQZ) (£562m) | Update on Triton FPSO | Triton production suspended due to Storm Éowyn damage. FY guidance under review. | AMBER/GREEN (Roland - I hold) |

Hollywood Bowl (LON:BOWL) (£470m) | Share Buyback | £10m buyback, “to reduce the share capital of the company”. | AMBER/GREEN (Graham) [no section below] BOWL matches last year’s share buyback, despite very high capex spending which saw net cash fall to £29m as of Sep 2024 (Sep 2023: £52.5m). However, it chose not to propose a special dividend this year, saving about £5m. Interesting that it chose to cancel its special divi rather than its buyback. PER is 12x so it earns a yield of about 8% on buybacks here. |

Foresight Solar Fund (LON:FSFL) (£436m) | Corporate update | Mgt fees reduced, NED board refresh and shareholder discussions re. strategy. | |

Elixirr International (LON:ELIX) (£374m) | TU | FY24 results above market expectations. Revenue >£111m. Momentum continues into 2025. | AMBER/GREEN (Roland) |

Castings (LON:CGS) (£129m) | TU | Profit warning - substantially below expectations. Demand for heavy trucks fell further in Q3. | BLACK (PW) / AMBER/GREEN (Roland - I hold) |

| Sylvania Platinum (LON:SLP) (£120m) | Interim Results | Net profit +132% due to higher prod and PGM basket price. FY prod exp 75-78koz (prev 73-76k) | AMBER (Roland) [no section below] Sylvania has increased its FY production guidance, helped by improved mining grades. Profit growth was as expected and broker Panmure Liberum has left FY25 estimates largely unchanged. SLP remains debt free and at a discount to NAV, but is exposed to cyclical and country risks. Perhaps a recovery in PGM prices and automotive demand can drive a re-rating. |

Transense Technologies (LON:TRT) (£23m) | Interim Results | Trading remains in line (FY June 2025). Trading since period end is strong. Net cash £1.9m in January. | AMBER (Graham) [no section below] Shares down 10%+ despite "in line" trading. Revenue +36% to £2.5m, EBITDA unchanged (<£1m). I noted previously that TRT's sensor technology/measurement businesses were very early-stage, and thus difficult to value. Broker Cavendish says that 70% growth is required in H2 vs H1 to meet full-year forecasts. Those forecasts are unchanged but surely there is a high risk of an official profit warning at some point in H2. They are targeting £15m in sales and £5m of EBIT by 2030, which is when they will stop receiving royalty income under a deal with Bridgestone. Net cash improved to £1.9m in January, but there are plans for £2.5m of capex spending over the next 12-18 months. This business is just so small and early-stage. Very difficult to value and its margin for error seems slim given the size of the cash balance. |

Inspiration Healthcare (LON:IHC) (£12.1m) | Trading Update | FY rev £38.3m, return to +ve EBITDA. Results below exps due to delay, but improved momentum. |

Graham's Section

Assura (LON:AGR)

Unch. at 42.4p (£1.4bn) - Statement re Possible Offer from KKR - Graham - AMBER/GREEN

We have independent confirmation from Assura that they rejected the 48p cash proposal from KKR.

The Board confirms that it considered the Proposal carefully with its advisers and concluded that it materially undervalued the Company and its prospects and therefore rejected it unanimously. No further proposal from KKR has been received.

Graham’s view: many thanks to Ken Mitchell in the comments who pointed out that it’s not unusual for REITs to accept takeover offers below their net asset value.

Tritax Eurobox (EBOX) was an example: the Canadian investment company Brookfield bought EBOX in late 2024 at a 12% discount to its March 2024 NAV.

Each case is different, however, and the Board of Assura clearly thinks that their company is worth its last-published NAV or more - the offer from KKR is 48p, while Assura’s last-published NAV is 49.4p.

Some general factors that come to mind:

Date of measurement: the last-published NAV might be out of date. The Directors might have a sense of what the next-published NAV is going to be, e.g. if there have been acquisitions, disposals, or changed valuations.

Quality of portfolio: different industries (healthcare, retail, residential, etc.) and their changing outlooks over time might justify a premium or a discount to NAV, depending on the outlook for demand and for rent collection.

Investor sentiment: if a REIT’s shares have been trading at a large discount for a long time, and/or if most shareholders are happy to move on, then accepting a discounted takeover might be a lot more palatable.

Personally I’d always want to ensure that buyers paid full price for any REIT that I was involved with - especially when it comes to the most financially sophisticated buyers, such as KKR.

I do accept that there are circumstances when a discounted offer will be accepted. A REIT can be worth more or less than its NAV, and if it's worth less than NAV, then it might make sense to accept a discounted offer. But as things stand, Assura does not appear to be one of these cases.

Plus500 (LON:PLUS)

Down 5% to £27.14 (£2.01bn / $2.53bn) - Preliminary Results - Graham - GREEN

Plus500, a global multi-asset fintech group operating proprietary technology-based trading platforms, announces today its preliminary unaudited results for the year ended 31 December 2024.

The headlines for these results were already disclosed in a year-end trading update last month: revenue up 6% to $768m, and EBITDA up 1% to $342m.

The cash balance at the end of 2024 was $890m, slightly lower than where it finished 2023.

As we discussed in January, the question investors need to decide is whether they trust the strategy to spend big on customer acquisition.

As the CEO says in his first paragraph today:

We leveraged our proprietary marketing technology to significantly increase our customer acquisition by 30% year-on-year and by 46% in Q4 2024 versus Q3. Our commitment to continued strategic investment has established the foundations for growth in future years.

Customer churn at PLUS remains my main concern, as it has done for some time, despite my overall positive view on the shares.

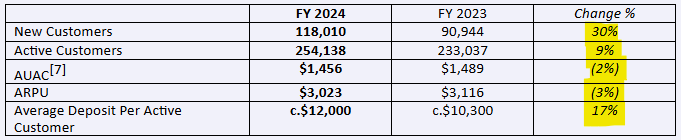

The table below shows that the number of new customers recruited during FY 2024 (118k) was much higher than the number of new customers recruited during FY 2023 (91k). But the number of active customers increased by only 21k.

If my sums add up correctly, it seems to me that nearly 100k customers must have become inactive in 2024, in order for the above table to make sense. That’s about 43% of the active customers in 2023 who became inactive in 2024.

With the average life of a customer being so short, PLUS has to constantly pump its marketing machine in order to keep new ones coming in the front door.

It has consistently demonstrated an ability to do this, so I’m not changing my positive stance. I’m just highlighting an important feature of the company.

Despite the rapid churning of many customers, PLUS notes that 67% of its OTC (over-the-counter) revenue is generated by customers who have been trading with the Group for more than three years.

This percentage has increased over time and it is undoubtedly a positive. Note that trading platforms are like casinos in the sense that a small number of high rollers tend to generate the large majority of revenues. So my interpretation of the 67% number is that PLUS’ high rollers are becoming more mature customers of the company. Which is not a bad thing.

The table also shows small declines in both user acquisition cost and in average revenue per user - I guess it makes sense that these might rise and fall together, reflecting industry trends.

Finally, the 17% increase in the size of the average deposit shows that PLUS is, on average, finding larger customers than it did previously. Another positive sign.

Outlook: they are “confident about the Group’s future prospects and strategic direction…”

Profits and shareholder returns

EPS rose 13% to $3.57 despite net income being virtually unchanged. The share count continues to fall, thanks to the company’s propensity to buy back its shares, boosting EPS.

On that point, today the company has announced a new $110m buyback, to begin when the existing $110m buyback completes. There will also be $90m of dividend payments.

Estimates: thanks to Panmure for covering PLUS. Their forecasts for FY25 are unchanged with a revenue forecast of $704m (below consensus $727m) and EBITDA of $343m (above consensus $336m). Lighter revenues are based on an expectation of calmer markets, but the “very lean, flexible cost base” should allow EBITDA to remain firm.

Graham’s view

The market is a little disappointed this morning, which I guess might have something to do with the dawning realisation and acceptance that 2025 could be a relatively quiet year for PLUS in terms of growth.

However, nothing has really changed. The company continues to expand both geographically and in terms of its licenses. It's increasingly active in the US with a thriving futures business and a B2B business for introducing brokers. It has a new licence in the UAE and a new localised trading platform in Japan.

Quantitatively, it’s almost impossible to argue against:

So I have no alternative but to maintain my positive stance. This trades on a PER of less than 10x and that’s before allowing for the cash balance which covers more than a third of the market cap. As the share count continues to reduce, and the company continues along its path of long-term growth, I can only assume that the path of least resistance is higher.

Roland's Section

Serica Energy (LON:SQZ)

Down 11% to 127p (£501m) - Update on Triton FPSO - Roland (I hold) - AMBER/GREEN

At the time of publication, Roland has a long position in SQZ.

We have more bad news from North Sea oil and gas producer Serica today, relating to the ageing Triton FPSO (Floating Production Storage & Offloading) vessel.

Serica Energy plc (AIM: SQZ) announces that, as a result of issues resulting from Storm Éowyn, production from the Triton FPSO has been suspended.

Safety critical fault: the company says that sea spray during Storm Éowyn triggered Triton’s fire and gas detection system, causing an automatic shutdown.

After an initially successful restart, storm damage was noticed to one of the cargo tanks. While preparing to repair the tank, operator Dana Petroleum discovered a further, safety-critical issue:

While preparing to conduct the necessary repairs, Dana Petroleum ('Dana') identified an integrity issue with a coupling in the inert gas line required for purging the tanks prior to carrying out the repairs. Triton has remained offline subsequently pending identification of the root cause of the issue and the best means of resolving it.

Triton is operated by Dana Petroleum but Serica says it is supporting Dana, including with the secondment of a member of staff. The implication of this would seem to be that the problem is not straightforward to fix (or that Serica has limited confidence in Dana’s technical team).

Expected restart date: Serica currently expects production to resume “in mid-to-late March”. Summer maintenance plans – currently scheduled for 40 days – are also under review. My reading of this is that this maintenance period may need to be extended.

Impact on FY production: Serica’s 2025 production guidance has been placed under review and will be restarted or revised when the timeline for repair of Triton is clarified.

When compared to previous guidance, the numbers provided by the company today and the extent of the shutdown suggest to me that a downgrade to guidance is likely, if not inevitable:

7 Jan 25: production net to Serica running at 46,400 boepd

21 Jan 25: FY25 production guidance for “around 40,000 boepd”, reflecting planned maintenance

18 Feb 25: January 2025: averaged 37,000 boepd, February 2025: “averaging 27kboepd to date”

I’m not able to model the timing and impact of new production expected to come onstream this year. But my rough estimates suggest that production could be much closer to last year’s level of 34.6kboepd than previously expected.

Estimates: how much financial impact will any production shortfall have on current forecasts? This is not easy to model as it’s dependent on commodity prices through the year. But gas prices have been strong so far this year:

This has included strong production from the Bruce Hub into a robust gas market, with February NBP prices averaging 134p/therm, as well as solid contributions from our other assets.

Auctus Advisors have published a note on Research Tree this morning - many thanks. They suggest that the financial impact of an extra Triton outage is not as great as it might have been, as gas prices have been above their modelled level so far this year.

Auctus estimates that the dividend might still be supportable, assuming gas prices remain favourable.

Triton FPSO life extension: Serica also uses today’s update to inform us that the company has recently received a draft of a third-party study into the work required to extend the life of the Triton FPSO. This is necessary as production through the FPSO is expected to continue potentially to 2040.

The report has confirmed that, subject to the continuation of the programme of maintenance and upgrades, the FPSO has the potential to continue producing well into the next decade.

Internet research suggests that construction started on Triton in 1997, with production starting in 2000. So by 2040, it will have spent more than 40 years floating in the North Sea. I suspect maintenance requirements may remain fairly high.

Roland’s view

Serica CEO Chris Cox sounds a little frustrated by today’s news. I think his comments are worth reproducing in full:

"Given that the Triton FPSO was recovering strongly from the operational issues of 2024, with material production from new wells, the impact of Storm Éowyn is deeply frustrating. Safety is of course always the number one priority, and we fully support the operator's actions in ensuring that this supersedes other considerations.

Recent drilling results illustrate the significant value of proven hydrocarbons in the Triton area. We will continue working with the operator and discussing with them at the highest level all options to secure a lasting improvement in the operating performance of the FPSO."

Serica has featured several times in the report recently. Both Mark and I have covered the stock, taking an AMBER/GREEN view due to the apparent value on offer and high expected free cash flow.

However, I’ve also mentioned my growing concerns about the age of Serica’s assets and the risk they may be more prone to reliability issues.

Today’s update makes me think I may have underestimated this risk, especially in relation to the Triton hub, which is not operated by Serica.

I’m tempted to downgrade to AMBER today, but I’m going to maintain my view at AMBER/GREEN as I think Serica does remain both cheap and cash generative.

Castings (LON:CGS)

Down 14% to 246p (£110m) - Trading Statement - Roland (I hold) - BLACK (AMBER/GREEN)

At the time of publication, Roland has a long position in CGS.

Castings’ RNS style is clean and concise. Unfortunately this clear style of communication has been used by this morning to report a significant profit warning:

it is the board's expectation that the company's result will be substantially below market expectations in the current year.

Around 75% of Castings’ revenue comes from supplying parts to European heavy truck manufacturers. The company has previously reported a slowdown in demand after a busy period, but says that volumes dropped further than expected during the company’s third quarter (Oct-Dec 24).

As a result, the underlying profitability of the foundry and machining businesses has fallen below expectations.

The slowdown in demand was such that Castings has actually had to pay penalties to its electricity supplier for not using enough of its contracted supply.

However, it’s not all bad news. Demand appears to be starting to recover:

Our major customers have recently reported increasing sales orders which are expected to positively impact Castings sales volumes early in the next financial year.

Estimates: with thanks to both Zeus and Canaccord Genuity we have updated estimates this morning. The company’s comments on FY26 initially suggested to me that existing forecasts for the next financial year might be unchanged, but both brokers have trimmed their estimates.

Zeus has cut its FY25 earnings estimate by 45% to 9.4p per share. FY26 forecasts have been cut by 20.2% to 17.2p per share.

Canaccord has a slightly more positive stance, cutting FY25E by 40% to 10.3p per share and FY26E by 17% to 17.3p per share.

Both brokers expect the ordinary dividend to be held at c.18.4p this year, supported by an expected year-end net cash position of £10m+. After this morning’s fall, that gives Castings a possible 7.3% dividend yield.

Roland’s view

Graham covered Castings’ interim results (and a previous profit warning) in November, taking a neutral view.

The key attractions for me are the company’s market leadership in its niche and strong balance sheet. Offsetting this are the cyclical risks (as we’re seeing) and the capital intensity of this business, which limits profitability.

Arguably, growth potential in the company’s core truck market is also limited, although management is trying to expand into areas such as renewables to access new growth opportunities.

Both brokers seem confident that Castings’ will maintain its longstanding net cash position and be able to sustain the ordinary dividend, which hasn’t been cut for more than 30 years:

Based on the last-reported book value of 294p per share, Casting shares may now be trading below book value. Although historic return on equity has only averaged just over 8% in recent years, I think the opportunity to invest below NAV and gain a 7%+ dividend yield suggests the stock may now offer attractive value.

I also wonder if today’s profit warning will be the last of this cycle. Stockopedia’s consensus trend chart suggests this is the third material downgrade in the last year:

As a value proposition, this won’t appeal to everyone.

However, given the continued strength of Castings’ balance sheet and the seemingly improving outlook, I think a more positive stance makes sense.

As a shareholder, I’m more inclined to buy more than sell following today’s announcement. AMBER/GREEN.

Elixirr International (LON:ELIX)

Up 6% to 819p (£395m) - Trading Update - Roland - AMBER/GREEN

The Board of Elixirr International plc (AIM: ELIX) ("Elixirr", the "Company") the established, global, award-winning, challenger consultancy, is pleased to provide an update on trading.

I’ve not looked at this consultancy business before and we haven’t covered it here since 2023, so I thought it might be useful to put a marker in our coverage ahead of April’s full-year results.

Today’s update from Elixirr is ahead of expectations, albeit only slightly:

Subject to audit, FY 24 results are expected to be above market expectations with:

The company is now guiding for revenue “greater than £111m”, versus a guidance range of £108-£111m. This represents an increase of 29% on the 2023 figure of £85.9m.

Adjusted EBITDA is expected to be “approximately £31 million”, versus a previous estimate from broker Cavendish of £30.4m. EBITDA margins are in line with expectations at 28% (guidance “27-29%”).

The company expects to end the year with net cash of £7.5m, having fully repaid debt drawn to fund the initial cash consideration of $28.9m for the acquisition of Hypothesis Group in October 2024. From what I can see, up to $7.6m in further consideration will be due in FY25 and FY26.

Trading commentary: Elixirr has not provided any detail on 2024 trading in today’s results, except to comment that the year ended “strongly”.

2025 trading to date is said to have been strong, with “record revenue for January”.

Estimates: broker Cavendish has increased its FY24 adjusted EPS estimate from 40.8p to 41.4p (an increase of 1.5%.

There’s no change to FY25 estimates at this point, but these have previously been upgraded to increase the rate of expected growth versus 2024:

Roland’s view

Elixirr floated on AIM in July 2020 and has four bagged since then. The stock has hit a new record high this morning:

As I commented yesterday in relation to FRP, professional services businesses such as this can be vulnerable to external conditions and the risk that key people will leave.

I’m always slightly sceptical about companies with misspelt names, but Elixirr certainly has lived up to its name so far.

Profitability and cash generation have been consistently strong since listing, supporting excellent quality metrics.

Revenue has grown at a compound average rate of 38% since 2018, while operating profit has grown at a CAGR of 30.9% over the same period.

Cavendish describes Elixirr as a possible ‘rule of 40’ stock in today’s note. This appears to be a term for (mainly) software companies targeting a combination of annual revenue growth and EBITDA margin in excess of 40% each year (Bain & Co have a useful introduction to this topic here).

I can certainly see the logic of this kind of metric - if a company has sufficient underlying quality, slowing revenue growth should be offset by higher margins, supporting continued high returns.

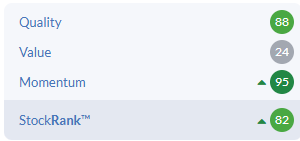

Stockopedia classes this stock as a High Flyer with strong quality and momentum. The StockRanks reflect this:

After today’s gains, I estimate Elixirr is trading on a FY24E P/E of 20, falling to a forecast P/E of 17 for FY25.

A certain amount of growth is baked into the valuation here. But if momentum can be maintained, I think Elixirr shares could have further upside on a medium-term view. AMBER/GREEN.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.