Good morning - I hope you're feeling refreshed after the long weekend!

The Agenda is complete.

12pm: wrapping it up there. It was a rather strange collection of announcements, as might be expected on the first day back after a Bank Holiday. We should get a more normal set of updates tomorrow! Cheers.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Bodycote (LON:BOY) (£940m) | SP +4% For the recent 4-month period, “core” revenues are down 5% organically. Total revenues down 6%. “Supply chains improving in Civil Aerospace; conditions remain weak in Automotive and Industrial markets.” Full year outlook in line with an H2 profit weighting. No material direct exposure to tariffs. Net debt £90m. | AMBER (Graham) [no section below] This issued a profit warning last month, prompting me to downgrade my stance to neutral. Today’s update reassures that the outlook has not deteriorated any further, with the share price reaction suggesting investor relief. The company’s ongoing “Optimise” programme targets savings and benefits of £12-14m p.a., and the company is exploring the potential to expand this. At a modest earnings multiple (and a neutral StockRank) I remain comfortable with my neutral stance. This is a reputable company with a strong heritage but in the short-term I would be a little cautious around the potential for another profit warning - especially given the expected H2 weighting for adjusted profits. | |

Elementis (LON:ELM) (£770m) | Enterprise value of sale $121m, net cash proceeds c. $55m. $50m buyback. Outlook unchanged. Disposal is expected to improve adj op margin by +2.4%. | AMBER (Roland) [no section below] The Talc business has been sold after a difficult year for a multiple of 15x 2024 operating profit. The new CEO will now try to improve the performance of the remainder of the business. This could be an interesting turnaround, but revenue has only risen by an average of 1% per year over the last decade and profitability has been variable. Further research would be needed for me to form a view on this situation, although perhaps Elementis will benefit from a wider chemical sector recovery. For now, I will give the new and highly-experienced CEO the benefit of the doubt and upgrade our view to neutral. | |

Enquest (LON:ENQ) (£212m) | Production efficiency >90%. Q1 production 42k boepd. Net debt $405m. 2025 guidance unchanged. | AMBER (Roland) [no section below] Like most peers in this sector, this independent O&G producer looks superficially cheap and offers a potentially tempting dividend yield. Deleveraging has reduced equity risk and the acquisition of Harbour Energy’s Vietnam assets may be a logical addition to Enquest’s existing SE Asia assets. | |

M&C Saatchi (LON:SAA) (£204m) | Agrees to buy a sports agency in Dubai and Abu Dhabi. Price not given. Funded by cash on the balance sheet (net cash was £18m as of December 2024). | AMBER (Graham) [no section below] When no price is given for an acquisition, we know that the cost must not be material - otherwise the company would be obliged to tell us what it is! The small size of the deal is backed up by its description as a “bolt-on” and the low staff count: its 40 employees join the M+C Saatchi Group family of over 2,400. Megan was neutral on this stock last month and I’m inclined to agree with her; in general, advertising, marketing and PR companies shouldn’t trade at rich earnings multiples and with modest like-for-like growth in 2024 I don’t see why this one should trade much more highly than it does already. PER is 8x on the StockReport and the StockRank style is Neutral. | |

4Basebio (LON:4BB) (£174m) | Revenues £933k (2023: £506k). LBT £12.7m (2023: £8.4m). “Transformational year of growth.” | AMBER/RED (Graham) [no section below] Given the £174m market cap, this is effectively pre-revenue with turnover of less than £1m in 2024. I note in passing that these are results for FY December 2024: companies reporting last year's results in late May are leaving shareholders in the dark for far too long, in my view. As for the results themselves, a key number is the cash balance (£34m following an equity raise in November) which should give the company a runway of a few years, based on historic and forecast losses. On that basis I can leave this at AMBER/RED rather than straight RED. | |

SRT Marine Systems (LON:SRT) (£147m) | SP +4% €167m Indonesia project has commenced. Implementation for 2 years, then 8 years of services. The half-year report to Dec 2024 showed H1 revenues improving to £26.2m and a PBT of £2.1m, after their Kuwait project commenced delivery. £320m of systems were said to be under contract. Estimates: still not estimates. Cavendish expects to reinstate forecasts late June/early July. | AMBER (Graham) [no section below] I was AMBER/RED on this in February on the back of allegations of irregularity (denied by the company) in the Philippines. I had previously been neutral, waiting to see if long-promised revenues from major contracts would at last materialise. Today’s update confirms that the Indonesia contract is now live and I’m happy to go back to neutral, bearing in mind that the half-year report in March showed revenues accelerating and the company moving into profitability. If only the company hadn’t promised success so many times before, I would be more inclined to trust the bull thesis today! It will be fascinating to see how how quickly the company can turn £320m of contracted systems revenue into profits and cash. | |

Inspired (LON:INSE) (£113m) | PE makes a possible cash offer of 81p per share, minus final dividend (if not withdrawn). | PINK (Graham) | |

Avacta (LON:AVCT) AVCT (£106m) | Results due 29 May 25 are delayed to 4 June 2025 due to audit delays. No impact on cash. | RED (Graham) [no section below] I wish this company every possible success with its mission to eliminate cancer. Quantitatively speaking, the stock is a RED - the StockRank is only 3, but the sea of red on the income statement (including the financial forecasts), along with the rising share count would lead me to a similar conclusion. Today we get a red flag to go along with all the red on the income statement: the company's audit isn't finished yet, and so it is unable to publish its results by May 29th as originally planned. Instead, it looks to publish them on June 4th. These are results for FY December 2024 - so they are already very late! | |

Software Circle (LON:SFT) (£109m) | £427k recovered in full. Incident isolated to a single unit. No evidence of breach of systems. | ||

MOH Nippon (LON:MOH) (£78m) | Expect FY25 loss of JPY1,151m. No H2 revenue due to project delays halting crowdfunding. | ||

MTI Wireless Edge (LON:MWE) (£38m) | Rev +7%, net profit +9% to $1.02m. EPS +12%, net cash $8.05m. Confident FY outlook. | AMBER/GREEN (Roland) This AIM technology group has a solid track record and benefits from exposure to several structural growth markets. However, growth is steady rather than rapid and I believe there are some additional risks for UK investors. On balance, I think a moderately positive view is appropriate. | |

Prospex Energy (LON:PXEN) (£20m) | FY loss of £46.8k, NAV +19.5% to £24.6m. Net cash £1.2m, no debt. Now has 3 producing gas assets. | ||

OPG Power Ventures (LON:OPG) (£20m) | FY25 generation flat at 2.3bn units. Revenue & EBITDA are expected to be in line with expectations. Cavendish forecasts (published in Dec 24): FY25E revenue £161m (FY24: £156m); FY25E adj PBT £5.1m (FY24: £8.0m). | AMBER (Roland) [no section below] OPG looks perennially cheap and trades at a near-90% discount to book value. But this may be justified by the sub-3% returns on equity. Shareholders have suffered a massive destruction of value over the last decade from this owner of Indian power stations. Forecasts are unchanged today, but suggest flat revenues and a lower pre-tax profit than last year. The algorithms style this as a contrarian stock and I can see this argument. But I think there’s also a risk that OPG is a value trap; I’d view this as a special situation requiring very careful research before taking a strong view. I can’t get higher than neutral. | |

Conygar Investment Co (LON:CIC) (£17m) | NAV +4.4% to £63.8m (107.5pps). H1 profit of £2.7m. A loan due Mar 25 has been extended to Dec 25. | ||

React (LON:REAT) (£17m) | H1 rev +14%, adj EBITDA +12% to £1.4m. Loss of 1.18pps. FY25 now to be below expectations. | AMBER/RED (Roland) [no section below] Today’s half-year results look poor to me. Last year’s debt-funded acquisition of drainage contractor Aquaflow has pushed the business to an H1 loss and the company now warns of sluggish order conversion, warning on full-year profits. React has a patchy record of profitability. While its collection of operating subsidiaries may include some attractive businesses, management empire building has delivered very little for shareholders – the share count has tripled since 2019, but the share price has fallen. I don’t see any reason to invest at this time. | |

Goldplat (LON:GDP) (£11m) | Ghana and SA achieved a combined Q3 PBT of £769k, including £90k of FX gains. |

Graham's Section

Inspired (LON:INSE)

Up 10% to 77.75p (£124m) - Potential Offer - Graham - PINK

This is a business advisor, helping companies to buy and optimise how they use energy.

It’s not one that we’ve covered very often. I see that I was RED on it back in Sep 2023, blaming its “balance sheet, debt, acquisition strategy and the presentation of its barely profitable results”.

The share price at the time was 85p; I’m relieved to see that today’s takeover offer is below that level!

Its two largest shareholders control most of its shares:

One of these - Regent - made a bid for the entire company last month at 68.5p, which was roundly rejected by the company and by the other major shareholder, Gresham.

Today the company announces that it has found a private equity buyer who is willing to make a possible cash offer of 81p.

They also say that the takeover would be structured so that it could go ahead without needing Regent to accept it.

The potential buyer is an American mid-market PE firm, HGGC.

Graham’s view - my assumption is that this deal will go through, perhaps unless Regent is willing to make a better offer.

Checking the recent full-year results for 2024, I see that the company is carrying significant debts (£59m) vs. its profitability (adj. PBT £12m).

In a situation like this, a takeover offer is often warmly received by small shareholders, so long as it is not viewed as being overly opportunistic. The new potential offer is 18% higher than Regent’s. As I’ve historically not been enamoured of this share, I would take the money and run.

Roland's Section

MTI Wireless Edge (LON:MWE)

Up 6.6% to 46p (£39m) - Q1 Results - Roland - AMBER/GREEN

MTI Wireless Edge Ltd (AIM: MWE), the technology group focused on comprehensive communication and radio frequency solutions across multiple sectors, is pleased to announce its financial results for the three-month period ended 31 March 2025.

Today’s first-quarter results from this Israeli technology group look fairly positive to me:

Revenue up 7% to $12m

Operating profit up 6% to $1.25m (10.4% margin)

Earnings per share +12% to 1.18 US cents

Net cash of $8.05m (31 Dec 24: $5.96m)

MTI’s operations are structured in three divisions, providing exposure to three industrial sectors that all appear to be benefiting from structural growth at the moment:

Defence;

5G mobile telecoms;

Water management.

Here’s what the company has to say about trading in each of its divisions.

Antennas: this business is described as a “one-stop shop for off-the-shelf flat and parabolic antennas”. It also produces custom designs.

Performance was strong in Q1:

Revenue up 22% to $4.04m

Segmental profit up 205% to $342k (8.5% margin)

These antennas are used for 5G mobile backhaul and for military use. 5G is seen as a big long-term growth opportunity in this business and MTI has a factory in India to target its large domestic market.

However, my impression is that the recent growth has been driven by increased military deliveries (mainly to the Israeli government), not the hoped-for surge in volume orders from 5G operators. Unfortunately we aren’t given a sales split between these two markets to provide extra clarity.

Water Control & Management: this business provides wireless systems under the Mottech brand for agriculture and municipal purposes (e.g. irrigation and fountains respectively). These solutions help users to save water and improve crop yields.

Sales rose in Q1, but profits fell due to a weighting to lower-margin projects. The company says the existing project pipeline should deliver improved profitability over the remainder of the year:

Revenue up 11% to $4.21m

Segmental profit down 23% to $446k (10.6% margin)

Distribution & Professional Consulting Services: this distribution business sells RF and microwave components to the defence sector and other industrial customers in Israel. Some products are later exported, so it’s hard to be sure how much revenue is derived from Israeli end users.

Q1 performance was weak as the PSK subsidiary (acquired in 2022) continued to drag on results:

Revenue down 7% to $4.02m

Segmental profit down 9% to $284k (7.1% margin)

PSK makes communication systems for defence and government clients and has required some additional support since its acquisition. But in another recent update, MTI indicated that the outlook could be improving:

[…] the Board believes that PSK has now resolved the issues it encountered in 2024 and has begun 2025 with a very healthy order backlog and a long pipeline of opportunities driven by Governments seeking to increase their investment in defence.

This view is reiterated in today’s Q1 results:

Overall backlog and pipeline of opportunities in both the traditional representation business and PSK is very strong which bodes well for the remainder of 2025.

Outlook & Estimates: CEO Moni Borovitz (whose family controls c.33% of the stock) sounds confident about prospects for the remainder of the year:

Overall MTI is in a good position, Q2 is progressing well with three material contracts wins announced so far and as a Board we are confident about the outlook for the year.

This view appears to translate into an outlook that’s in line with expectations.

With thanks to house broker Shore Capital, I can see that full-year forecasts are unchanged today, suggesting FY25 earnings of 5.1 cents per share.

Roland’s view

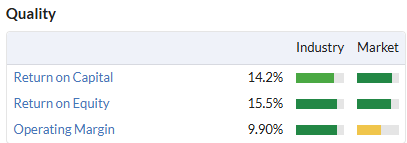

MTI has been a steady performer on AIM for many years:

Quality metrics are also very respectable:

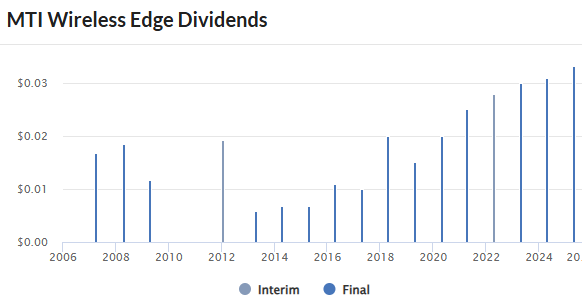

… and the dividend has proved very reliable, backed by a strong balance sheet and (perhaps) strong support due to family ownership:

On the face of it, the stock’s forecast P/E of 12 and 5.5% dividend yield don’t look demanding. However, recent years’ growth has only been in single digits. I would also argue that the company’s foreign ownership, family control, and heavy single-country exposure may justify a modest valuation discount.

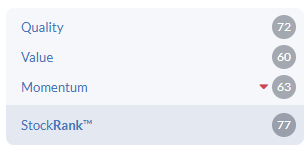

Stockopedia’s algorithms view MTI as a Super Stock, but the StockRanks have been falling recently and are starting to look less compelling to me.

On balance, I’m going to leave my previous AMBER/GREEN view unchanged today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.