Good morning!

The FTSE fell by 1% yesterday and the S&P 500 was down by 0.8% on concerns over Trump's tariff plans.

FTSE futures this morning are slightly lower again, down by 0.1% to 8560.

Tariffs on Mexico and Canada have been delayed by one month, and Trump has said that the UK may be able to avoid tariffs.

However, he also says that tariffs on the EU will "definitely happen". Tariffs of 10% on Chinese goods have already been implemented, and China has immediately retaliated with tariffs of their own on US exports: 15% for US coal and LNG and 10% for crude oil, farm equipment and some autos, starting next week.

I'm hopeful that the UK will not be directly impacted by Trump's tariff plans, and that many of the stocks we cover in this report will be able to avoid major disruption caused by this issue. But it seems inevitable that a trade war between the two largest global economies, and probably involving several other major economies, will have far-reaching effects.

1.15pm: we've reached the cut-off time for today, thank you everyone.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Diageo (LON:DGE) (£53bn) | Interim Results | Volumes -0.2%, op profit -4.9%, leverage 3.1x EBITDA. Dividend held. Tariff/macro headwinds. Removed medium-term guidance. | AMBER/GREEN (Graham) Tariff and general macro uncertainty leaves DGE unable to make useful forecasts for now. I'm a huge fan of this one but I accept that there are plenty of reasons for investors to stay away. |

Vodafone (LON:VOD) (£18bn) | TU | Revenue +5% to €9.8bn in Q3. On track to grow in line with FY guidance, reiterated today. | AMBER (Roland) |

Crest Nicholson Holdings (LON:CRST) (£449m) | Final Results | Results in line with guidance. Rev -6% to £618m, adj PBT -53% to £22.4m. Completions -7%. Interest rates holding back outlook. | |

YouGov (LON:YOU) (£423m) | TU | Modest underlying H1 growth, core biz stabilising. Performance in line with mgt exps. CEO leaves. | |

Mortgage Advice Bureau (Holdings) (LON:MAB1) (£416m) | Business update (CMD) | Possible move to Main Market. Medium term target to double revs with adj PBT margin >15%. | GREEN (Graham) Excellent news that they are considering a move to the Main Market, and aiming to join the prestigious FTSE-250. Ambitious growth targets announced too, which I hope are realistic. |

| Funding Circle Holdings (LON:FCH) (£405m) | Response to press article | They are confident that the purchaser of defaulted loans on their platform will be successful at trial. | AMBER (Graham) I'm cautiously switching to a neutral stance as it's not clear to me how serious this problem might be for FCH's existing loan book. |

Filtronic (LON:FTC) (£218m) | Interim Results | Rev +200% to £25.6m, op profit £6.8m. “Strong start” to H2 supports current exps. | AMBER (Roland) |

Devolver Digital (LON:DEVO) (£107m) | FY TU | Returned to +ve adj EBITDA, in line with exps. Double-digit YoY rev growth to >$100m. $42m cash. | |

Alumasc (LON:ALU) (£104m) | Interim Results | H1 rev +20%. Adj. PBT +19% to £7.5m. Outlook: confident in achieving FY25 expectations. | GREEN (Roland) |

Gaming Realms (LON:GMR) (£104m) | FY TU | Adj. EBITDA +30% to £13m, in line. Early trading in 2025 is encouraging. | GREEN (Graham) Nothing obviously wrong and lots to like at first glance: a growing company with net cash and an undemanding earnings multiple. |

NWF (LON:NWF) (£77m) | Interim Results | Revenue -4% but adj. op profit +25% to £5m. H1 is in line. Expectations are unchanged. | |

Venture Life (LON:VLG) (£44m) | TU | Adj. EBITDA “broadly in line”. Some unexpected de-stocking. “Extremely positive” for 2025. | |

Various Eateries (LON:VARE) (£27m) | Final Results | Rev +9% to £49.5m, adj. EBITDA £0.3m, pre-tax loss £3.4m. Currently trading in line with exps. | |

Staffline (LON:STAF) (£27m) | TU | 2024: ahead of exps. Adj. profit £11.1m, cash £4.4m. 2025 outlook: impacted by macro uncertainty. | |

B90 Holdings (LON:B90) (£12m) | TU | Expects to at least meet exps for 2024, with further growth anticipated in 2025. |

Graham's Section

Gaming Realms (LON:GMR)

Up 4% to 36.85p (£109m) - Pre-Close Trading Update - Graham - GREEN

Gaming Realms plc (AIM: GMR), the developer and licensor of mobile focused gaming content, is pleased to announce its pre-close trading update for the full year to 31 December 2024….

It’s a pleasant update from GMR which confirms that FY Dec 2024 was in line with expectations.

Revenues rose 22% to c. £28.5m while adj. EBITDA rose 30% to £13m.

The “Slingo” game (a mix of slots and bingo) seems to go from strength to strength:

This strong performance was driven primarily by content licensing, supported by growth across all major markets. During FY24, Gaming Realms launched its Slingo portfolio with 44 new partners globally and successfully introduced its games in West Virginia, the Company's fifth US iGaming market. Gaming Realms' content is currently active in 20 regulated markets.

Outlook: we learn that early trading in 2025 has been encouraging.

Licensing agreement: the Slingo brand has been licensed for many years by Scientific Games, one of the world’s largest lottery companies (headquartered in Atlanta). The two companies have agreed to work together for another five years, bringing Slingo games to Australia, Canada, Europe, New Zealand and the US.

CEO comment:

We are delighted to announce these strong results for FY24, which underline the continued appeal of our Slingo portfolio and other unique gaming content. Our success in entering new regulated markets, coupled with the addition of multiple new partners, has fuelled significant growth. We look forward to building on this momentum in 2025 as we broaden our market reach and further expand our innovative content portfolio.

Estimates

Many thanks to Canaccord for covering this, despite not being one of GMR’s joint brokers. Canaccord’s Wealth Management business owns c. 4% of the company.

GMR is beating Canaccord’s 2024 revenue forecast (£28.5m actual, vs. £27.1m forecast) and I’m guessing that Canaccord’s 2025 revenue forecast of £30.7m is probably too low now?

The adj. EBITDA forecast for the new year is £15.4m.

If these forecasts turned out to be accurate then the adj. EBITDA margin would improve even further to 50%+, having reached 45.6% in 2024. A reminder that this business is highly profitable.

Graham’s view

I’m happy to leave our existing GREEN stance unchanged here.

Simply put, I cannot find anything obviously wrong here.

The Exec Chairman owns nearly 9% which is a comforting level of alignment with other shareholders.

Growth in recent years has been really impressive with revenues approximately doubling since 2021, as Slingo's popularity spreads internationally and through a wide variety of channels.

The company earns very high quality metrics and EBITDA margins implying high levels of cash conversion (N.B. will want to double check this when we get the full accounts).

The company is expected to already have a healthy cash balance of c. £14m, according to forecasts, and will rise significantly during 2025 if expected profitability is achieved. GMR does not yet pay a dividend.

Given the attractions, the earnings multiple here does not strike me as excessive. Earnings per share for 2025 will hopefully be 3p+, depending on the level of adjustments that are applied and depending on which source you use. The StockReport, for example, shows a 2025 EPS forecast of 3.45p. So the earnings multiple is somewhere between 10x and 12x, depending on how you calculate it.

With no obvious red flags and apparently lots of reasons to like it, I’m keeping this GREEN to reflect my view that it’s a very strong candidate for further research, so that you can make up your own mind.

GMR shares are still trading below their 2021 high. The company only generated revenues of £15m in 2021, and hardly any profits, versus over £30m of revenues forecast for the current year:

Funding Circle Holdings (LON:FCH)

Down 26% to 92.4p (£304m) - Response to press article - Graham - AMBER

There was no early morning RNS from this today but the company was in the news.

The Times has published an article, “Court to rule if firm owned by Elliott hedge fund can pursue debts”, which refers to attempts by a debt purchaser to pursue business owners over personal guarantees. The loans in question originated at Funding Circle.

The article notes the following:

Last year, in an interim ruling, a judge said the two guarantors had a “real prospect of success” in establishing at trial that money they had personally guaranteed was not in fact payable to Azzurro or Funding Circle because of alleged issues with documentation and processes.

The article further notes claims that this debt purchaser may have bought 10,000 loans from Funding circle with a combined face value of c. £500m.

So the case going to trial may in effect serve as a test case for 10,000 Funding Circle loans, and perhaps many other Funding Circle loans.

If small business owners learned that the personal guarantees associated with their Funding Circle loans were to some degree not enforceable, it’s not hard to imagine that this could have serious consequences on the Funding Circle loan book.

The Times quotes Funding Circle’s CEO: “We’re really confident in our position.”

And they quote Funding Circle’s chief legal officer: “It is not disputed that the loans were validly entered into and that there is money owed under the personal guarantees. We are confident that Azzurro will be successful at trial.”

Graham’s view

I’m not a legal expert but I find it hard to imagine that guarantors will be able to avoid the liability altogether, although the Times article seems to suggest that this is possible.

I would say it’s far more likely that if there is a problem, it is to do with the attempted transfer of the loan from Funding Circle to the debt purchaser, Azzurro. And if the transfer isn’t possible or has failed for now, due to problems with documentation, it implies that Funding Circle might be left with the job of attempting to enforce their debts until this is sorted out.

What does all of this mean for the shares? Unfortunately, it creates two bear arguments against FCH.

Firstly, there are now claims in the media that FCH has been “totally unprofessional” in terms of how it handles loans and guarantees. So there is an argument that FCH is simply not very good at its core business, and that they needlessly created this situation.

Secondly, there are the immediate - and potentially long-term - financial consequences of loans getting stuck in the justice system. I’m referring not just to the test cases going to trial but any other of Azzurro’s loans that require legal input, and any other FCH loans that may end up in the same boat.

This situation is inherently uncertain and I’m downgrading our stance on this all the way from GREEN to AMBER, as I can’t properly assess FCH shares at this time.

As of July 2024, immediately following the sale of its US business, FCH had balance sheet net assets of £237m. Therefore the stock is still trading at a premium to book value, even after today’s fall.

It has been a rough ride for long-term shareholders:

Edit to add: the company has released an RNS which states:

No question has been raised as to the general enforceability of loans and personal guarantees on the Funding Circle platform. It is not disputed that the loans were validly entered into and that there is money owed under the personal guarantees.

The case is going to full trial and we are confident that Azzurro will be successful.

I think this is consistent with what I said above: it is probably not a question of whether or not the money is owed, but more to do with the question of who the money is owed to.

Mortgage Advice Bureau (Holdings) (LON:MAB1)

Up 4% to 748p (£433m) - Business Update - Graham - GREEN

We already covered a trading update from MAB1 very recently - see here. The company has beaten estimates for 2024, delivering adj. PBT of over £30m.

Today we have a “business update” rather than a trading update, that relates to the strategy for the next few years.

Those who are interested in learning more can look into the company’s “Capital Markets Day” at the LSE, which will also be available on webcast.

New medium-term growth targets:

Double revenues (2024: £266m)

Adj. PBT margin >15% (2024: I calculate 11.5%)

Cash conversion >100%

Double the company’s market share of new mortgage lending

Dividend policy: the company has had a policy of paying out at least 75% of profits to shareholders.

In order to attack the growth targets shown above, that dividend policy is being scrapped in favour of a progressive policy with no specific percentage target.

In other words, MAB1’s dividends might not grow as quickly as profits do in future, as more funds are likely to be kept inside the business for growth.

The dividend for FY Dec 2025 (to be paid in 2025 and 2026) is likely to be set at just 50% of profits.

However, there will be an annual review which may result in share buybacks or special dividends, if there is surplus capital over and above what the business needs.

Move to the Main Market? MAB1 are considering a move away from AIM and onto the Main Market, “with the ambition of meeting the criteria for inclusion in the FTSE 250 index”.

Graham’s view

This update is undiluted good news. As I’ve said before, I think that AIM stocks that can get into the FTSE 250 should do so, as it’s a prestigious index that’s worth being a part of. The companies in that list today with the smallest market caps include the likes of SThree (LON:STEM) , Jupiter Fund Management (LON:JUP) and Crest Nicholson Holdings (LON:CRST). MAB1’s current market cap should be big enough to get onto the bottom tier of this index, if they decide that this is what they want.

As for the medium-term strategy, the only question in my mind is whether it might possibly be unrealistic to double revenues and to double market share in a medium-term timeframe. Will acquisitions be needed to do this?

Doubling revenues doesn’t seem out of the question, particularly if market conditions are favourable.

But doubling market share means growing faster than everyone else, even in a rising market - MAB1 does have a track record of outperformance, but it sounds like they are planning to push themselves very hard indeed over the next few years.

This stock has been a regular fixture on my annual watchlist and I’m excited to see what they might achieve next.

Diageo (LON:DGE)

Down 1% to £23.48 (£52bn) - Interim Results - Graham - AMBER/GREEN

(Disclosure: at the time of writing, I have an indirect interest in DGE shares.)

These interim results have attracted negative media coverage and I can understand why, as the company takes the unusual step of removing its medium-term guidance.

Before getting into that, here are the headlines in terms of sales.

Reported sales down 0.6% due to unfavourable foreign exchange.

Organic sales up 1%

Volumes down 0.2%

And profits:

Reported operating profit down 5% to $3.15bn. Driven by foreign exchange and a reduction in operating margin.

Organic operating profit down 1.2%. On an organic basis, margin has fallen due to “continued investment primarily in overheads”. The curse of an extremely mature business!

Adjusted EPS falls nearly 10% to 97.7 US cents (equivalent to 78.7p at latest exchange rates).

So there is nothing much to write home about in terms of sales, volumes or profits.

Leverage multiple is 3.1x, which is at the very high end of what I consider to be acceptable, but DGE is the type of business that should be able to operate at this level.

The interim dividend is unchanged at 40.5 cents (32.6p)

Medium-term guidance. Here is the really bad news:

Medium-term guidance has been removed due to the current macroeconomic and geopolitical uncertainty in many of our key markets impacting the pace of recovery. We remain confident of favourable industry fundamentals and our ability to outperform. Instead in the interim, we will provide more regular near term guidance.

Medium-term guidance had been for sales growth of 5 - 7%.

CEO Debra Crew has this to say within her comments (emphasis added):

Diageo has anticipated and planned for a number of potential scenarios regarding tariffs in recent months. The confirmation at the weekend of the implementation of tariffs in the US, whilst anticipated, could very well impact this building momentum. It also adds further complexity in our ability to provide updated forward guidance given this is a new and dynamic situation.

DGE’s CFO is quoted in media reports as saying that planned tariffs would reduce operating profits by c. $200m in the current financial year (FY June 2025), before any mitigation measures. For context, total operating profit last year was $6.0 billion.

The tariffs would hit tequila and whisky that are imported to the US from Mexico and Canada.

Graham’s view

I’m going to be a little bit contrarian and express an AMBER/GREEN stance on this one, as I view it as one of the highest-quality large companies listed in the UK.

Some may reasonably take the view that it’s still too expensive, especially considering the enormous debt pile:

For me, the quality of the brands in the DGE portfolio is beyond question. But of course it is a very mature business and reduced alcohol consumption may ultimately see drinks companies rated in the same way that tobacco companies are rated - as legacy companies. That is possible.

As for the tariffs, I’m wondering if Trump is using China as an example and if the threats against Canada, Mexico, the UK and Europe might be little more than negotiation tactics. I presume there are a wide range of concessions he is looking for and would be willing to accept, over the next month, in exchange for the continuation of a light tariff regime. Negotiation is what he's all about, isn't it? So I think there must be a very wide range of possible outcomes in terms of the tariffs, if any, that might ultimately be applied against America’s allies.

And besides, making tequila and whisky expensive is hardly going to do anything for his popularity (not that he needs to worry about the next election!).

Bottom line: withdrawing guidance is a reasonable move by DGE, given the importance of the US market to them and the uncertainty hanging over the trade rules that may soon govern this market.Roland's Section

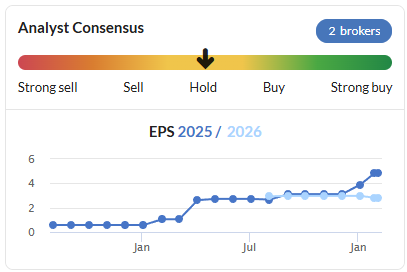

Filtronic (LON:FTC)

Down 3.4% to 96p (£210m) - Interim Results - Roland - AMBER

Filtronic plc (AIM: FTC), the designer and manufacturer of products and sub-systems for the aerospace, defence, telecoms infrastructure, space and critical communications markets, announces its half year results for the six months ended 30 November 2024 ("H1 2025").

We’ve covered Filtronic several times in recent months as it’s upgraded expectations for 2024/25. This has mainly been driven by a large contract with Elon Musk’s company SpaceX.

Today’s half-year results confirm that current expectations should be underpinned by a strong start to H2, but do not include any further upgrades. Let’s take a look.

H1 summary: I think it’s fair to say the SpaceX work has been transformational for Filtronic this year. These numbers cover the six months to 30 November 2024:

Revenue +200% to £25.6m

Operating profit of £6.8m (H1 24: (£0.4m)

Earnings of 3.08p per share (H1 24: (0.24p))

Cash generated from operating activities up 16.7% to £2.1m

Net cash exc leases: £5.1m (H1 24: £5.2m)

Filtronic’s half-year results show a healthy 26.5% operating margin against a reported loss for the same period last year.

This was achieved despite a 62% increase in the company’s overhead cost base during the period, reflecting a 16% increase in headcount and expanded manufacturing facilities. Two new production lines were installed during the half year.

Cash performance: the cash flow statement gives us a feel for some of the moving parts behind the scenes here.

£6.6m working capital outflow, due to rise in inventories and receivables

£1.6m spent on plant, equipment & intangible assets (software?)

£0.5m of capitalised development costs

The working capital movements explain why operating cash flow of £2.1m was so much lower than operating profit of £6.8m. However, I’d expect these to reverse over time if the pace of growth slows.

Overall, Filtronic operated at free cash flow breakeven for the half year, with net cash unchanged. I think that’s probably a creditable result in this situation.

Update on key markets: SpaceX has been the big story for Filtronics this year and the company seems hopeful of further growth:

Our strategic partnership with the market leader, SpaceX, continues to strengthen and grow. The success of the relationship has enabled us to deliver at high volume and high quality, working closely with our business and supply chain partners. This achievement has enabled both parties to consider further collaboration following the remarkable success of the Starlink constellation.

Low Earth Orbit satellites remain Filtronic’s key market and the company believes there will be further opportunities elsewhere in this sector.

However, all the company’s main live programmes with other customers appear to be due for completion in the next 12 months or so:

European Space Agency: a “prestigious programme” completes “over the next year”, material revenues to be recognised in FY26

QinetiQ: an active defence programme “will substantially complete in FY2025”

BAE Maritime Systems: defence programme will complete “within FY2026”

The UK’s Strategic Defence Review “pushed back the planned timing of a number of prospective opportunities”

My feeling is that there are opportunities in both space and defence, but some lack of visibility at the moment.

Outlook: the company reminds us that the “positive cadence of order intake” has resulted in material upgrades over the last two months.

Our order book is healthy and underpins the recent upgrades, whilst the opportunity pipeline continues to build serving us well as we move towards the next financial year.

However, there are no further upgrades today and nor is there any new guidance for FY25, according to Chairman Jonathan Neale:

we look forward to being able to communicate more about the next financial year as things develop during H2

An updated note from house broker Cavendish leaves forecasts unchanged today, highlighting the current lack of visibility on FY26 earnings:

FY25 adjusted EPS: 4.8p

FY26 adjusted EPS: 3.0p

Roland’s view

I can’t fault Filtronic for seizing the opportunity with SpaceX. My concern is that it looks to me like there’s some risk of earnings falling substantially below current levels next year.

From what I understand of the SpaceX agreement (I haven’t studied it in detail), there could be a lull in demand for Filtronic’s products next year, before a second phase of ordering begins in 2026 onwards.

From a long-term perspective, I can see that it might be worth accepting some volatility in earnings to continue benefiting from the company’s long-term growth.

On the other hand, the level of customer concentration here would concern me. In addition to the financial risk, I wonder if it might make Filtronic less attractive to other potential partners, who might feel they were always in second place for resources.

Filtronic doesn’t seem to split out the SpaceX revenue in today’s results, but the company does say that £23.5m (92%) of H1 revenue was to US customers. I don’t know how many other US customers Filtronic has.

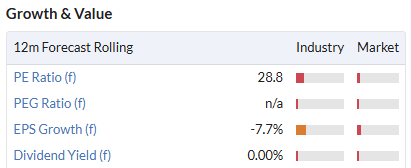

So where are we today? Filtronic is poised to deliver record results this year, but the current order book does not yet support a repeat performance in FY26. Current forecasts suggest earnings could fall by nearly 40% next year.

As a result, the shares are starting to look quite expensive on a rolling 12-month view:

Given the current lack of visibility and the apparent customer concentration risks, I’m going to maintain my neutral view here. AMBER.

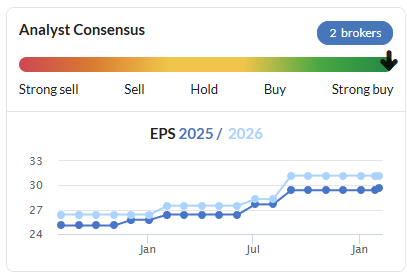

Alumasc (LON:ALU)

Up 4.1% to 299p (£108m) - Half-Year Results - Roland - GREEN

This sustainable building products and solutions group is reporting its half-year results for the six months to 31 December 2024.

We are pleased to report a record first half, driven by both organic and inorganic growth. Group revenue grew by 20% compared to the prior period, which is a particularly impressive result given the challenging market environment.

Alumasc has been an impressive trade over the last couple of years. The shares have been buoyed by strong trading, but also by the imminent prospect of the company’s pension deficit being eradicated.

H1 results summary: Alumasc saw half-year revenue rise by 20% to £57.4m, while pre-tax profit rose by 16% to £6.5m.

These numbers lift Alumasc’s trailing 12-month reported operating margin to 23.9% and its TTM ROCE to 24.0%. Both are very respectable figures, in my view, that seem likely to support continued value creation for shareholders.

Net debt was reduced to an insignificant £4.6m at the end of December, reflecting free cash flow of £5.4m for the period. That represents 110% cash conversion from H1 net profit, an excellent performance.

Cash generation could also receive a further boost if the pension deficit is eradicated. Alumasc contributed £600k to its pension scheme in H1 but says that the scheme is now “approaching self sufficiency”.

The group achieved growth in all of its divisions during the half year:

Water Management: revenue up 34% to £29.6m (15.8% op margin)

Building Envelope: revenue up 8% to £20.2m (12.5% op margin)

Housebuilding Products: revenue up 6% to £7.5m (25.0% op margin)

The company says that its largest business, Water Management, benefited from accelerated deliveries to a Hong Kong airport project during the period.

Water Management revenue was also boosted by a £5.7m contribution from ARP Group, which was acquired in December 2023. It’s nice to see this disclosed clearly.

Stripping the ARP revenue out tells me that Water Management’s organic revenue rose by 8.6% to £23.9m during the half year – consistent with the growth seen in the other two divisions.

Outlook: Alumasc believes it is well positioned “to continue to outperform the UK general construction market” while investing selectively to drive overseas growth.

Guidance for the full year remains unchanged:

The Board continues to remain confident both in the Group achieving its expectations for the year to June 2025, and in the significant opportunities available over the medium and longer term.

With thanks to broker Cavendish, I can also see that its FY25 and FY26 EPS forecasts are unchanged today at 29.4p and 31.4p respectively. That’s broadly in line with the estimates on the StockReport, which have been upgraded several times over the last year:

Roland’s view

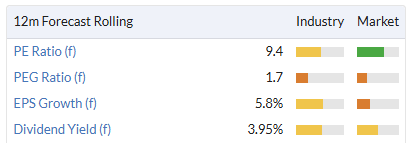

Alumasc’s forward valuation doesn’t look too demanding to me, given the company’s strong profitability and balance sheet:

It’s also worth noting that strong cash conversion means the shares also offer a free cash flow yield in excess of 9% – an attractive measure, in my view.

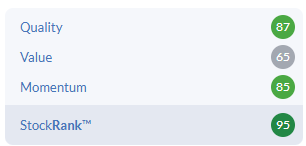

The StockRanks are also very strong and I imagine they will remain so when today’s interim numbers are digested by Stocko’s algorithms:

Alumasc’s double-digit profit margins and high ROCE suggest to me that the company’s products do have pricing power and perhaps some level of competitive advantage.

While this probably isn’t a business where I’d want to pay a high multiple of earnings, I’ve been impressed with progress at this business in recent years. I’m happy to maintain our previous GREEN view after today’s numbers.

Vodafone (LON:VOD)

Down 5.9% to 65.9p (£16.7bn) - Q3 FY25 Trading Update - Roland - AMBER

This third-quarter update from the FTSE 100 telecoms giant looked relatively positive to me at 7am, However, markets have taken a more cautious view due to ongoing challenges in Germany, Vodafone’s largest market.

Vodafone’s headline figures showed a return to top line growth during the three months to 31 December 2024:

Group total revenue: Increased by 5.0% to €9.8 billion in Q3 with good organic service revenue growth partially offset by adverse foreign exchange movements.

The company’s measure of organic service revenue grew in all its main markets except Germany:

Germany: -6.4%

UK: +3.3%

Other Europe & Turkey: +2.6% and 53.1% respectively (reflecting hyperinflation)

Africa: +11.6%

Business: +4.3%

The company also reiterated its full-year guidance for the year ending 31 March 2025:

On track to deliver Group Adjusted EBITDA of c.€11 billion and Group Adjusted free cash flow of at least €2.4 billion.

This compares to adjusted free cash flow of €2.6bn in FY24, but I think it should continue to underpin the current dividend, giving a prospective yield over 6%.

Disposals/M&A: the sale of Vodafone Italy also completed in December 2024 for €8bn, while Vodafone UK achieved regulatory approval for its planned merger with Three. This is expected to support higher utilisation and improved returns on capital in the future – a big weakness in this sector.

Germany: Vodafone also offers cable television in Germany, but changes to the law last year have had a big impact on this market. My understanding is that TV was frequently bundled by apartment landlords into rental packages, leaving tenants with no option. This is no longer permitted and tenants have free choice – meaning some have left Vodafone and many have had to be re-recruited.

This process is now nearing an end and Vodafone says it’s retained 49% of affected customers, or 4.1m households, against a target of 50%. I see this as a one-off headwind that should ease over time.

Vodafone’s other businesses in Germany saw mixed performance, with broadband customers -7k but mobile customers +23k. However, pricing remains under pressure in mobile and broadband, with both businesses seeing small falls in underlying revenue per user during the period.

Outlook: Vodafone’s FY25 guidance is unchanged today and the company expects to complete the merger with Three UK in “the next few months”.

The €8bn proceeds from the Vodafone Italy sale have been used to reduce debt and the board is targeting a further €2bn in share buybacks when the current buyback programme is completed.

Broker forecasts suggest earnings of 7.9 Euro cents per share this year, with a dividend of 5.3 cents. This prices the stock on a forecast P/E of 10 with a yield of c.6.5%.

Roland’s view

The bear arguments on Vodafone are well-known and largely justified. It’s generated returns on capital below its cost of capital for many years, has too much debt, and has destroyed a lot of shareholder value.

However, CEO Margherita Della Valle has done everything she has promised so far since taking charge in 2023. The changes have been substantial – Vodafone has sold its operations in Spain and Italy and secured agreement to merge with Three in the UK, reducing the number of incumbent networks from four to three.

This merger is expected to improve returns on capital – a critical challenge for the company and the wider sectors.

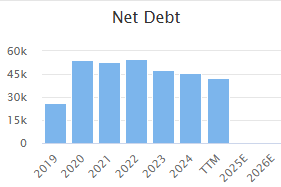

The group’s net debt has already fallen by c. 20% from its peak of €55bn, according to Stockopedia.

Germany remains a challenge, but Della Valle has made it clear this is now her main priority.

In the meantime, I think the group’s business in Africa – where it is one of the largest mobile operators and has an important mobile banking service – remains an attractive long-term growth opportunity.

Despite my cautious optimism, I think it would be naive to think that Vodafone couldn’t continue to disappoint as it has in the past.

On balance, I’m going to start our coverage with a neutral view. I think this is a fair reflection of the current situation. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.