Good morning! The RNS remains quiet for now - it appears that many City workers and company management teams have taken full advantage of the chance to take a break over Christmas. I did think we would have a few more updates than this on January 7th!

11.50pm: we are all done for today, see you tomorrow!

Spreadsheet accompanying this report (updated to 3/1/2025).

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Next (LON:NXT) (£11.9bn) | TU | Full-price sales ahead of exps; pre-tax profit exps increased by £5m to £1,010m. FY EPS +11.4%. | AMBER/GREEN (Graham) |

Serica Energy (LON:SQZ) (£593m) | Production update | FY prod 34,600 boepd, below Q3 guidance. Most issues resolved, output currently 46,400 boepd. | AMBER/GREEN (Roland) |

Corero Network Security (LON:CNS) (£100m) | TU | “Broadly” in line for 2024. Looks like a probable miss for 2024. Confident in 2025 expectations. | AMBER/GREEN (Roland) |

Argo Blockchain (LON:ARB) | Dec Operational Update | Their hosting agreement ended; they are evaluating alternative sites to rehost their machines. | RED (Graham) |

Summaries

Serica Energy (LON:SQZ) - Down 1.7% to 148p (£582m) - Update on production - Roland (I hold) - AMBER/GREEN

Today’s update reveals that Serica’s 2024 production of 34,600 boepd fell below even its 5 December guidance. However, various technical issues now appear to be resolved and reliability is expected to improve in 2025. With current production running at over 46k boepd, I expect strong cash generation and believe the 15% dividend yield remains sustainable.

Next (LON:NXT) - up 3% to £98.32 (£12.2bn) - Trading Statement - Graham (I hold) - AMBER/GREEN

Full price sales in the pre-Christmas period were up 5.7%, vs. prior guidance of 3.5%. This slightly increases the full-year PBT estimate for FY January 2025 to £1,010m. Looking ahead, the company anticipates 3.5% growth in full-price sales for January 2026, and a similarly modest increase in PBT. Next remains impressively robust to my eyes and it will need to rely on this robustness if its pessimism re: the UK economy is well-grounded.

Corero Network Security (LON:CNS) - Down 2.5% to 19p (£98m) - Trading Update - Roland - AMBER

Today’s full-year trading update reveals Corero has missed 2024 revenue and EBITDA expectations slightly, but trading performance has remained positive and the growth outlook for 2025 is unchanged. I think there could be an interesting story here, but the low profitability and full valuation mean I’m neutral for now

Short Sections

Argo Blockchain (LON:ARB) - down 7.4% to 4.9p (£35m) - December operational update - Graham - RED

This crypto miner issues its normal monthly update. Revenues are up to $3.9m thanks to the rising bitcoin price, but there is a sting in the tail:

As previously announced, the Company's hosting agreement with Galaxy ended on December 28, 2024. The 23,619 S19J Pros at the Galaxy site will be refurbished so they can be used in an air cooled facility. The Company is currently evaluating alternative sites to rehost the machines.

Galaxy is the company that rode in and saved Argo back in 2022, buying its Texas mining facility for $65m and also lending it $35m. That loan has since been repaid but now Argo is without a facility, as Galaxy are not interested in keeping Argo as a tenant.

I could hazard a guess as to why Galaxy might have have made this decision. Interim results for Argo to June 2024 showed that it had a negative balance sheet value of minus $20m, and to add insult to injury it was loss-making at the operating level. The cash balance was only $4m; it has since raised £6.5m in fresh equity (July) to help it finish repaying the Galaxy loan, and then another £4.2m (December). Shareholders have suffered dilution of c. 20% so far this year.

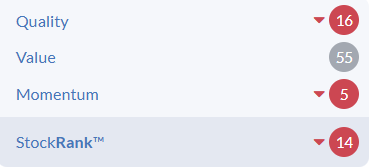

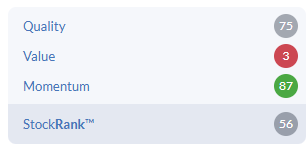

I’ve never been a fan of this stock and it remains an automatic RED for me after today’s update. At least the class action lawsuit by some of Argo’s US-based investors has been dismissed. With the company’s crypto mining machines now in need of being relocated or sold, they are exploring new ventures in high-performance computing. I’m afraid I don’t view this as a serious investment opportunity, and the StockRanks are on my side:

Graham's Section

Next (LON:NXT)

Up 3% to £98.32 (£12.2bn) - Trading Statement - Graham (I hold) - AMBER/GREEN

It’s pleasant news for NXT shareholders such as myself, as we get yet another ahead of expectations trading update.

This remarkable management team continues to under-promise and over-deliver. It’s amazing how the simple act of keeping expectations low, and then consistently beating them, even by small amounts, can generate such goodwill among shareholders like me.

The headlines:

Full-price sales in the six weeks to 28 December are up 5.7% year-on-year, after adjusting for the timing of Christmas this year compared to last year.

The full-year PBT forecast for FY Jan 2025 increases by £5m to £1,010m.

This PBT estimate is 10% higher year-on-year, with pre-tax EPS up 11.4%. That controversial topic of buybacks is relevant here: NXT’s share count continues to gradually decline, which helps to put upward pressure on earnings per share.

The share count is expected to reduce by nearly 3% this year. As the stock currently trades at a moderate PER of about 14x, I don’t think they need to be any more aggressive than this when it comes to buying back their shares.

Trading performance

For the financial year to 28th December, we have the familiar pattern of UK online sales growing (+5.2%) faster than UK retail sales (minus 1.1%). Overall UK growth is modest at 2.5%.

Overseas sales unexpectedly accelerated in the pre-Christmas period (31.4%) and now have a growth rate of nearly 24% year-to-date.

Cash flow and net debt plans

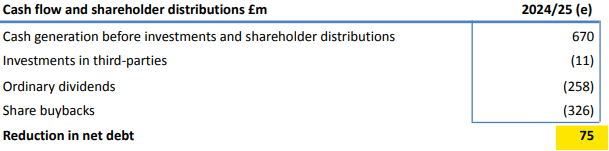

The company’s planned use of its £670m of surplus cash generated this year is clearly explained. There’s a nice mix of dividends and buybacks to keep fans of both happy, plus a small reduction in net debt from £700m to £625m.

There is £250m bond maturing in August 2025, so Next wants to have some extra cash available:

Next’s intention has been to repay this bond using its own resources. However, “subject to market conditions, we may choose to issue a new bond in 2025 which would allow us to distribute more surplus cash to shareholders.” So there could be a nice boost to the dividend, or more buybacks, if the company thinks it can borrow cheaply again in August.

With full-year PBT significantly higher than net debt, I do think that Next can afford to use more leverage, but I’m relaxed about whatever option it chooses as August approaches.

Guidance for FY January 2026

Not much growth is baked into these forecasts:

Full-price sales growth 3.5%

PBT up 3.6%

Pre-tax earnings per share up 6.7% after the effect of share buybacks.

Next say they are being cautious on the UK, where they expect only 1.4% sales growth, due to employer tax increases, i.e. higher National Insurance. These tax increases will “filter through into the economy”, impacting prices and employment.

Internationally they are only forecasting 14% sales growth, vs. 24% in the current year. They say that the current year saw a step change in overseas marketing expenditure, and they don’t think they can profitably increase marketing spend at the same rate in the current year.

£67m increase in wage costs: this figure is estimated from “normal” inflation of 2%, plus the change in the national living wage, plus higher NICs, plus the cost of wage inflation at NXT’s suppliers. The change in the national insurance threshold alone creates a 6.5% increase in the cost of hiring a part-time low-wage employee.

How the company will mitigate this: firstly, by increasing prices by 1% (but NXT’s prices will still rise by less than 2%). Secondly, by operational cost savings, primarily new mechanisation at warehouses. It seems that about half of the increased wage costs can be offset in these ways.

Graham’s view

In my view, NXT remains the absolute gold standard when it comes to UK company reporting. The clarity, transparency and (I hope) honesty are second to none.

As for the company’s actual trading performance, I have no complaints. Of course growth could always be stronger, but this is a mature business and moderate growth comes with the territory.

It does trade at a higher PER than its industry peers:

However, even at this PER, its buyback activity (paid for out of ongoing cash generation) helps to juice its EPS growth in a noticeable way.

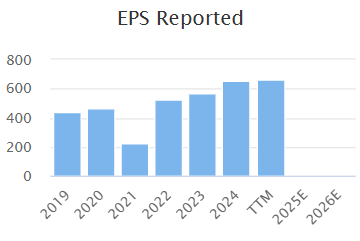

Stockopedia reports net profit growing at a CAGR of 6% since 2019, while reported EPS has grown at a CAGR of 8.3%:

See my update in October when I gave a big-picture summary of Next’s attractions.

Does the company face significant risks? Of course. I am extremely selective when it comes to retailers, and there are probably only a handful that I would even consider buying. This is a low-quality sector where economic winds often decide the face of mediocre businesses.

I think that Next is different: that it has a management team who are uniquely logical and sensible.

One of the major concerns facing the sector right now is of course employment costs and taxes, but Next has an in-built cushion in the form of a chunky operating margin (19% according to the StockReport). It doesn’t need to panic about profits evaporating overnight.

As for my current stance, I’m inclined to leave my AMBER/GREEN unchanged here. I was AMBER/GREEN in October at a share price of £102. At a share price of £98 and in the wake of another upgrade to earnings expectations, there is little reason to change my view.

The outlook for 2025 is indeed very cautious but that is probably appropriate in the circumstances and in any case Next are known for their caution, so there is really no surprise on that front.

Roland's Section

Serica Energy (LON:SQZ)

Down 1.7% to 148p (£582m) - Update on production - Roland (I hold) - AMBER/GREEN

The title of today’s RNS sounded slightly ominous to me – and so it proved. After warning of further issues with the Triton FPSO in December, the company today admits it did not meet even December’s reduced production guidance.

Serica now confirms full-year 2024 production of 34,600 boepd, slightly below 5 Dec guidance of 35,000 to 36,000 boepd. This quarterly table provides a useful breakdown, showing that overall production did not recover as previously hoped in Q4:

The issues: the Q4 shortfall is primarily blamed on the Triton restart being “at the longer end of expectations”.

Production shut down on 5 December and gas exports did not resume until 29 December, when the export gas compressor was restarted “following extensive root cause analysis and remedial work”.

Unfortunately, Serica’s owned and operated Bruce field also experienced a period of unscheduled downtime during December. This was said to relate “primarily” to a subsea intervention to improve production reliability on the neighbouring Rhum field.

I assume the impact of this downtime is reflected in the lower Q4 production from the Bruce Hub versus Q3. The big drop off in Q3 reflected scheduled annual maintenance.

2025 production: it may be that these issues are now in the past. Overall production net to Serica was running at 46,400 boepd on 5 Jan.

This figure is expected to increase as the phased restart of Triton completes and the newly-completed Gannet GE05 well is brought online.

Other drilling is also underway that could contribute to H1 2025 production, while Triton reliability is expected to improve when the FPSO resumes operations with two compressors later in Q1.

Roland’s view

In his comments on 5 December (when the latest Triton problems were announced), Mark documented the decline in Serica’s 2024 production guidance during H2 2024:

H1 actual - 43,700 boepd

2nd Oct FY guidance - towards the bottom of the 41,000 to 46,000 boepd range

29th Oct FY guidance - expected to be slightly below this previous guidance (41,000 boepd)

Today's FY guidance - 35,000-36,0000

It’s not a pretty picture and it may be worth remembering that Serica’s assets are fairly mature. I can’t be sure, but I wonder if they may be more prone to reliability issues than more recent developments, especially as operators are likely to manage capex tightly to reflect limited production lifespans.

However, Serica is a respected operator with a good reputation. Today’s update suggests to me that recent issues are now largely resolved.

This view is supported by updated broker commentary from Auctus Advisors forecasting total production of c.41k in 2025 – many thanks.

The investment case for Serica – and the reason I hold the shares – is based on the company’s strong cash generation. In its H1 2024 presentation, the company said it expected to generate surplus cash equal to its then market cap (c.£500m) between now and 2028.

This should underpin the stock’s current 15% dividend yield, which continues to look safe to me.

The rising gas price trend should also be positive for Serica, whose production is roughly 60% gas, 40% liquids:

I remain happy to continue holding and believe the shares offer value at current levels. However, I may turn more cautious if 2025 turns out to be as problematic as 2024. For now, I’m maintaining our previous view of AMBER/GREEN.

Corero Network Security (LON:CNS)

Down 2.5% to 19p (£98m) - Trading Update - Roland - AMBER

Trading across FY 2024 is expected, subject to audit, to be broadly in line with market expectations.

Corero Network Security provides security software (SmartWall) to protect against denial of service attacks.

The shares have doubled over the last year. While today’s update appears to be a slight miss against expectations, the muted market reaction suggests to me investors remain comfortable with the outlook.

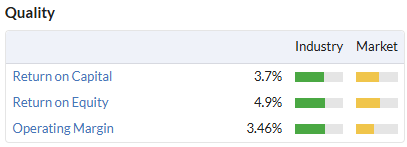

Interestingly, the sloping line at the bottom of the chart above shows us that Corero’s StockRank has improved and become much more respectable over the last year. The shares now boast a high quality-momentum score, typical of High Flyers in the Stockopedia style rating.

If growth remains strong, this suggests to me the shares could potentially continue to perform well:

Let’s take a closer look at today’s update.

FY24 trading: operationally, 2024 seems to have been a decent year for Corero.

In line with industry trends, the company aims to sell its software on a subscription basis as well as through upfront licence sales. The subscription service is described as “DDoS Protection as-a-Service (DDPaas)”.

Reflecting this model, annualised recurring revenue (ARR) rose by 16% to $19.5m last year, while order intake increased 13% to $28.2m.

Corero’s interim results showed ARR up 12% to $17.2m and order intake up 10% to $14.2m, so H1 performance appears to have been maintained during the second half of the year.

Profit miss: as Mark commented before Christmas, use of the world “broadly” generally indicates results below expectations. That seems to be the case here.

Corero’s full-year revenue rose by 10% to $24.6m, slightly below Stockopedia’s consensus forecast of $25.6m. Updated notes from Canaccord Genuity and Zeus Capital today both confirm this slight miss.

In terms of profit, adjusted EBITDA is expected to be between $2.2m and $2.5m (FY23: $1.8m), versus broker forecasts of $2.6m to $2.7m.

I’m not a fan of adjusted EBITDA as it excludes too many costs for my liking. This is reflected in sharply downgraded earnings forecasts from broker Zeus today - many thanks.

Zeus has used the low end of Corero’s EBITDA guidance to update its forecasts. As a result, the broker believes Corero will only achieve a breakeven result at the bottom line this year:

FY24 EPS (previous): 0.1 cents

FY24 EPS (latest): 0.0 cents

Margins remain low: I’m surprised Corero is providing such a wide EBITDA guidance range, given that 2024 has now ended. I wonder if there are some accounting questions to iron out.

Regardless, these numbers highlight the continuing poor profitability of this business. Using the midpoint of today’s EBITDA range gives me an FY24 EBITDA margin of just 9.5%.

That doesn’t seem all that exciting to me – ID security group Intercede (LON:IGP) is of a similar size, for example, and reported a 21% EBITDA margin in its last set of accounts.

I understand Corero has been scaling up its sales team and I would hope to see evidence that operating leverage will improve margins with further growth. At present, profitability remains uncomfortably low, for me:

2025 outlook: the company sounds confident about the year ahead:

Management is encouraged by the FY 2024 exit rate of ARR and new Orders and remains confident that 2025 market expectations will be achieved.

The group’s $5.3m year-end cash position is also expected to improve early in Q1, as $4.8m of cash for orders invoiced in Q4 is expected imminently.

Forecasts for 2025 have been left unchanged today, with Zeus estimating earnings of 0.4 cents per share, slightly ahead of Stockopedia’s consensus figure of 0.3 cents per share.

This leaves Corero shares trading on a hefty forward P/E of between 60 and 80, depending on which estimate you choose.

Roland’s view

I don’t have any insight into the quality or scalability of Corero’s product. I’m not sure who the end users are – smaller companies or large enterprises? What’s the realistic addressable market? Who are the competitors?

It would be very interesting to hear from any industry insiders (or investors) who are more familiar with this sector in the comments.

From a financial perspective, Corero seems to be making progress at building a growing base of recurring revenue. I’m also encouraged by the 97% customer retention rate. This seems to suggest the product is both sticky and reasonably useful.

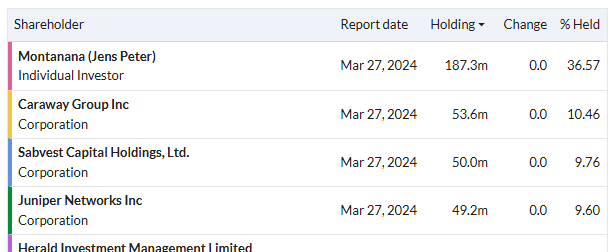

Looking at the shareholder register, I don’t recognise many of the names, but the presence of network equipment provider Juniper Networks (NYQ:JNPR) seems positive. I understand Juniper resells Corero’s SmartWall product to its customers, potentially providing access to a sizeable market.

On balance, I’m going to take a neutral view here. Corero’s net cash position and growing scale suggest to me it should be able to self-fund continued growth.

On the other hand, profitability is lower than I’d like to see for a £100m company, and I think the valuation already prices in significant further growth. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.