Good morning! I have some backlog comments to start us off today.

1pm: all done for now! Cheers.

Spreadsheet accompanying this report (updated to 10/1/2025)

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Experian (LON:EXPN) (£32bn) | TU | Organic revenue +6% in Q3. FY exps unchanged - in line. | |

Diploma (LON:DPLM) (£5.5bn) | Q1 results | Q1 in line. Organic rev +7%, reported rev (inc. acqs.) +12%. FY guidance unchanged. | |

International Distribution Services (LON:IDS) (£3.5bn) | Q3 TU | On track to return to adj op profit in FY25. | PINK (Under offer) |

Vistry (LON:VTY) (£1.7bn) | FY TU | FY adj PBT to be c.£250m, in line with December’s revised guidance. Completions +7%, net debt £180m. | AMBER/RED (Roland) |

Just (LON:JUST) (£1.5bn) | FY TU | 2024 op profit to be more than 2x 2021 op profit. Just completed £1.8bn DB transaction for G4S. | |

Mitchells & Butlers (LON:MAB) (£1.4bn) | Q1 TU | LFL sales +3.9% during 15 wks to 11 Jan. Total sales +3.8% YTD. £100m of extra costs this year. | |

Hays (LON:HAS) (£1.2bn) | Q2 TU | Q2 fee income -12% LFL, H1 adj profit of c.£25m “towards lower end of the consensus range” | |

Ashmore (LON:ASHM) (£1.1bn) | TU | $0.4bn of net outflows in 3mo to 31 Dec, investment perf -$2.6bn. US uncertainty. Dec AUM $48.8bn. | |

Genus (LON:GNS) (£940m) | HY TU | Strong H1, FY25 adj profit to be at top end of range of market exps. | AMBER (Roland) |

Currys (LON:CURY) (£929m) | TU | Strong peak trading with UK/IRL rev +2% LFL. FY Adj PBT to be £145-£155m, ahead of exps. | AMBER/GREEN (Graham) |

Nichols (LON:NICL) (£462m) | FY TU | FY24 rev and adj PBT in line with exps. Margins improving as inflation eases. | GREEN (Graham) |

Asos (LON:ASC) (£454m) | Changes to dist network | Atlanta site to be mothballed, replaced by smaller site. £10-20m annualised benefit from FY26.. | |

Galliford Try Holdings (LON:GFRD) (£371m) | TU | FY profit to be at upper end of expectations. | |

Fuller Smith & Turner (LON:FSTA) (£320m) | TU | In line. | |

Victorian Plumbing (LON:VIC) (£314m) | Final Results | Confident FY25 profit will be in line with exps. | |

Liontrust Asset Management (LON:LIO) (£259m) | TU | £1.6bn of net outflows in 3mo to 31 Dec. | AMBER/GREEN (Graham) |

Brooks Macdonald (LON:BRK) (£240m) | FUM & Main Market move | Net outflows of £151m in 3mo to 31 Dec. | AMBER/GREEN (Graham) |

Gateley (Holdings) (LON:GTLY) (£174m) | Interim Results | FY results expected to be in line. | |

Frontier Developments (LON:FDEV) (£73m) | Interim Results | In line. “Strong turnaround” in H1 FY25, following return to profitability in H2 FY24. | AMBER (Roland) |

Audioboom (LON:BOOM) (£66m) | TU | Adj EBITDA ahead of expectations. | |

Xaar (LON:XAR) (£51m) | FY TU | In line. Revs lower. Ceramics still bad. “Modest” year adj. PBT. Wide range of outcomes for 2025. | |

Nexteq (LON:NXQ) (£38m) | TU | In line. Economic challenges, destocking, customer delays. 2025 to be broadly in line with 2024. | |

Vianet (LON:VNET) (£31m) | Agreement with global brewer | “Strategic data solutions contract win”: beer monitoring across the UK. Expands footprint by c. 5%. | |

M Winkworth (LON:WINK) (£25m) | TU | In line. | |

Finseta (LON:FIN) (£25m) | FY TU | Adj. revenue up 26% to £11.3m - no mention of expectations, this seems to be a very slight miss? |

Summaries

GYM (LON:GYM) - up 5% yesterday to 148.6p (£268m) - Pre-close trading update - Graham - AMBER/RED

This low-cost gym operator published a positive update with adj. EBITDA for 2024 coming in “slightly above the top end” of the range, i.e. slightly above £45.5m. Similarly, the FY25 forecast is for adj. EBITDA “at the top end” of the range (£47.2 - 49.7m). However, I’ve run out of patience waiting for GYM to demonstrate economies of scale and publish some real profits. Perhaps it will do that in 2025 as revenue per member and the membership base continues to grow, but I am going to adopt a moderately negative stance to reflect the length of time it has taken the company to do this.

Vistry (LON:VTY) - up 7.8% to 555p (£1.86bn) - Trading Update - Roland - AMBER/RED

The problems with the company’s South Division appear to be under control, but rising debt levels and an increase in unsold stock concern me. I’m unimpressed by the continued focus on share buybacks in these circumstances. I think better choices are available elsewhere in this sector.

Liontrust Asset Management (LON:LIO) - up 1% to 405.2p (£264m) - Trading Update - Graham - AMBER/GREEN

Hefty outflows in Q3 (Oct-Dec) reflecting a terrible month for the UK funds industry in October ahead of the most recent budget. LIO has found some more cost efficiencies as it outsources work to BNY Mellon and CEO John Ions is very pleased with the recent performance of some of LIO’s funds. While I like this sector, LIO would be one of the last fund managers I would add to my portfolio.

Frontier Developments (LON:FDEV) - up 25% to 232p (£92m) - Interim Results - Roland - AMBER

Games developer Frontier’s more focused strategy has delivered an initial win, with its latest release generating 22% of H1 revenue in under four weeks. Management is now confident of a full-year profit and net cash has risen to around 30% of the market cap, providing significant security. FY26 forecasts suggest possible value but remain somewhat speculative. Without industry knowledge, I’m comfortable taking a neutral view.

Genus (LON:GNS) - up 19% to 1,694p (£1.1bn) - Half-year trading update (ahead of expectations) - Roland - AMBER

This genetic improvement specialist has seen strong trading in its pork business and now expects full-year profits to be ahead of expectations. On initial inspection, this business appears to have interesting growth potential, but also faces some risks. I think it’s prudent to maintain our neutral view, but Genus could be worth further research.

Short Sections

MJ GLEESON (LON:GLE)

Up 7% yesterday to 474.5p (£277m) - Trading Update - Graham - GREEN

This low-cost housebuilder and land promoter has seen its shares slide along with the rest of the sector, on fears over interest rates. It was trading at 546p when I looked at it only two months ago, and had traded comfortably above 600p not long before that.

Yesterday saw the publication of an “in line” trading update that was greeted positively by the market. The company’s previous update said that FY June 2025 would be “more weighted to the second half than usual” - a statement that often precedes a profit warning. So it makes sense that a reassuring in-line update would be met with a relief rally, especially after a period of share price weakness

Gleeson has produced a “robust performance” in H1, “despite activity in the market remaining subdued”. At Gleeson Homes, 801 homes were sold, slightly ahead of the prior year. Reservation rates and the forward order book both made positive progress. Meanwhile at Gleeson Land, planning decisions are expected early in H2 which should boost the performance of that division.

Graham’s view: I’m going to upgrade this one to GREEN as it was AMBER/GREEN previously at a higher valuation, e.g. at a 546p share price in November and at a 573p share price in September. Of course it’s fair to say that the outlook has deteriorated since then with far fewer rate cuts now anticipated from the Bank of England in 2025. However that doesn’t mean we won’t get those rate cuts: they may just be delayed. For patient investors, GLE is now trading at a discount to its last-reported balance sheet net assets of nearly £300m, fully tangible.

Robert Walters (LON:RWA)

Up 2% yesterday to 310p (£224m) - Trading Update - Graham - AMBER/GREEN

The share price rose yesterday despite what was officially a profit warning: investors must have been expecting even worse! This international recruitment group announced that Q4 net fee income was down 14% at constant currencies, or down 17% at actual exchange rates. The year-to-date figures are equally bad, and all four geographic regions are down by double digit percentage rates: Asia Pac, Europe, UK & Rest of World.

The company acknowledged that fee income was “slightly weaker than expected”. As might be expected during a time of general corporate uncertainty, permanent recruitment (down 18%) is underperforming temporary recruitment (down 10%). RWA has cut its own headcount by 5% quarter-on-quarter and by 17% year-on-year. It maintains net cash of £53m, almost a quarter of the market cap.

CEO comment: "As seen throughout the year, 2024 closed with conditions in global hiring markets remaining challenging - marked by muted client and candidate confidence. Fourth quarter fee income was slightly weaker than expected, and in addition further actions were taken on the cost base. As a result, we now expect a broadly breakeven position at the profit before tax level for the full year.

Graham’s view: we’ve been AMBER/GREEN on this one, on the basis that the company has plenty of cash to survive this downturn, and the valuation is very attractive if we do get a recovery in the recruitment sector. The shares are now 10% lower than the last time they were reviewed, in October. I’ll tentatively leave our AMBER/GREEN stance unchanged as little has changed since last time: the company continues to struggle, but the shares continue to offer value to anyone who thinks this sector has the potential to come back to life - my own working assumption is that recruiters will enjoy their previous levels of profitability again. I don’t understand what might have changed (the use of AI?) to prevent corporates from using recruiters to the same extent as they did in the past.

Perhaps I’m clutching at straws, but I find it interesting that the share price rose on the day of a profit warning. Could it be a sign that sentiment here has reached a low?

Currys (LON:CURY)

Up 11% to 91.4p (£1.04bn) - Strong Peak Trading and Improved Profit Outlook - Graham - AMBER/GREEN

I was very nervous about upgrading this to AMBER/GREEN which I did in December on the back of the H1 results. But the company has today published a very confident update for the 10 weeks ended 4 January 2025 (the peak trading period).

Key points: like-for-like revenue in the UK & Ireland up 2% - “robust sales and stable gross margin.” In the Nordics, like-for-like revenue was up 1% - “market share gains in a soft market”.

Outlook: adj. PBT of £145 - 155m for FY April 2025, ahead of consensus expectations which were for adj. PBT of only £140m. As we anticipated, a dividend is coming and the Board intends for it to be 1.3p, to be declared in July with the full-year results.

Graham’s view: I’m never going to be relaxed about taking a positive stance on Currys, a company whose ambition is to achieve an adjusted EBIT margin of just 3%. But I’m going to leave that positive stance unchanged today. One point that stands out to me in particular is that cash interest expense for the current financial year is going to be less than £20m, reflecting the very strong position the company achieved by the end of H1 (October 2024), when it had net cash of £107m.

The improved balance sheet, which includes a falling pension deficit (last seen at £143m on an accounting basis), sets it up well for the year ahead and I’ll probably maintain my positive view here for as long as cash flow remains healthy.

3-year chart:

Nichols (LON:NICL)

Unch. at £12.63 (£462m) - FY24 Trading Update - Graham - GREEN

I’m giving this a mention as it’s a long-standing member of my watchlist. Today’s full-year trading update is in line with expectations, as H2 “continued the positive momentum from the first half”. Full-year revenue inched higher by 0.8% to £172m as the company focused on its “Packaged” business at the expense of the “Out of Home” segment, where it has exited unprofitable contracts.

My investment thesis here rests on the idea that historically high operating margins (they used to be 20%+) might ultimately be restored. There is reassurance on the margin front with the company saying “gross margins have continued to improve as inflationary pressures eased during the year and as the overall product mix improved.” The company’s cash balance remains strong at £54m despite the payment of a special £20m dividend on top of the regular dividends (yield c. 3% at the current share price).

Outlook:

Whilst inflationary pressures now appear to be moderating in the UK, the Board remains mindful of continued uncertainty affecting some of the Group's markets and necessary mitigating actions are in place. Underpinned by the strength of its diversified business model and robust financial position, the Group remains confident that Nichols is well positioned to deliver its strategic plans and medium-term financial ambitions that will continue to generate sustainable shareholder returns.

Graham’s view: I’m reassured by the lack of surprises here. It’s important at this stage to refer to NICL’s medium-term ambitions which they set out in November: revenues of over £225m (30%+ higher than 2024), PBT margin expansion to 20%, and PBT of at least £45m. It’s up to you to decide if this is feasible but I think management are credible and I’m happy to maintain my positive stance. Estimates from Singers include adj. PBT of £31.5m in the current year.

The large cash balance takes the sting out of the high earnings multiple this currently trades at:

Brooks Macdonald (LON:BRK)

Up 4.5% to £15.15 (£250m) - Quarterly FUM & Intention to move to Main Market - Graham - AMBER/GREEN

This wealth manager hasn’t made it into this report before, but let’s give today’s update a quick mention. The quarterly update is in line with expectations (please note that the financial year-end is in June, so this is a Q2 update to December).

Funds under management have been stable since June, just shy of £18 billion.

CEO comment:

This is Brooks Macdonald's strongest quarter of gross inflows for 18 months… While outflows remained elevated in the quarter, we are taking actions to improve asset retention as well as driving new business growth. Additionally, we continue to scale and enhance our financial planning expertise, including most recently through the acquisitions of LIFT, Lucas Fettes and CST Wealth Management.

Moving to main market: BRK is leaving AIM. Ordinarily I would consider this to be premature, as a £250m market cap is not big enough to get into the FTSE-250 Index, which is where companies start to really attract the interest of index investors and others looking for blue-chip opportunities. So to me this decision feels like a snub for AIM.

Graham’s view: BRK has been around for a long time and is a respected name in the financial sector. I’ll take a moderately positive stance at this valuation - might be worth investigating further.

Graham's Section

GYM (LON:GYM)

Up 5% yesterday to 148.6p (£268m) - Pre-close trading update - Graham - AMBER/RED

I was excited about this stock once upon a time, but it has sadly failed to produce any real profits since pre-Covid (and those profits weren’t very large, either). Nevertheless, the share price has discovered some momentum over the past year:

As discussed by Paul last year, the company has only really been generating enough cash flow to pay back prior capex investments.

Yesterday’s trading update provided some encouraging data for 2024: like-for-like revenue up 7%, and total revenue up 11%. The membership base and average revenue per member continue to grow, with the 7% increase in average revenue per member beating the inflation rate.

Growth ambitions are less aggressive than they used to be: there were 12 new sites in the year, bringing the total to 245. The plan for 2025 is 14-16 new sites.

Net debt has reduced to £61m (this excludes over £300m of leases).

Outlook:

As a result of the strong delivery of like-for-like growth and new site performance, Group Adjusted EBITDA Less Normalised Rent for FY24 is expected to be slightly above the top end of the current market forecast range of £43.5-45.5m.

Taking into account both higher national insurance contributions and the positive sales momentum in the business currently, GYM suggests that this year’s EBITDA less normalised rent will be “at the top end” of the forecast range £47.2 - 49.7m.

However, as noted by Paul last year and as I always say when it comes to capital-intensive companies, EBITDA is unfortunately a meaningless metric. “Does management think the tooth fairy pays for capital expenditures?”

CEO comment:

There is plenty more still to come as we execute our plan and we look to 2025 with confidence. We are well prepared for our key member recruitment period in the current quarter and beyond, with our strengthening new site pipeline and our flexible, high value, low cost offer making gym membership more accessible for all."

Graham’s view: I was genuinely excited about this one pre-Covid, but I’m now resigned to the view that competition in the gym sector is too fierce, and the capital-intensive nature of the service it provides (as with cinemas, restaurants, etc.) makes it a fundamentally difficult sector for investors to approach. GYM has had enough time since Covid to demonstrate economies of scale, and it hasn’t done it yet.

That being the case, I’d only want to pay a bargain price for shares in this. And the £320m+ enterprise value here does not strike me as offering all that much of a bargain.

If adj. EBITDA comes in near £50m this year, it’s trading at an EV/EBITDA multiple of about 6.5x. There is hardly any tangible balance sheet support.

I’m going to nudge this lower to AMBER/RED on concerns that it hasn’t built a sustainably profitable business and that sooner or later, it will run into trouble.

Liontrust Asset Management (LON:LIO)

Up 1% to 405.2p (£264m) - Trading Update - Graham - AMBER/GREEN

More outflows at this fund manager: another £1.6 billion left the building in the final calendar quarter of 2024, Oct-Dec, which is the company’s Q3 period.

Assets under management fell 5.3% in Q3 alone, and are down 11.5% year-on-year (from £27.8bn in Dec 2023 to £24.6bn in Dec 2024).

If we look back to H1, net flows were minus £2.1 billion over six months. We’ve now had a £1.6 billion outflow in Q3 alone.

Rival fund manager Polar Capital Holdings (LON:POLR) recently observed that October 2024 was the third worst month on record for the UK funds industry, and Liontrust reiterates that today. Half of LIO’s Q3 outflows (£0.8 billion) were in October alone.

CEO John Ions seems pleased with recent fund performance but I remain sceptical on that front - see for yourself in today’s “key fund performance” table. Many of LIO’s funds are still in the 3rd and 4th quartiles for performance over 3 and 5 years. I do agree with Mr. Ions when he says:

There are reasons to believe we are entering a more positive period for active investors. There is currently an extreme concentration of the mega caps in the US market, which is at its highest level for a century. Any broadening of returns from equity markets, greater focus on valuations and lower index returns going forward will present opportunities for price discovery among active investors.

Graham’s view

There is no major change to my view here. I still think this is a great time to buy fund manager shares, but LIO is not my first pick in this sector. See here for my laundry list of problems with it.

LIO's shares are down by another 10% since I covered it last, and that is before it cuts its dividend. I said last time that its planned dividends were affordable only on a one-off basis, and the market surely agrees with me now.

It’s a great pity that it didn’t retain more cash for buybacks: it is currently carrying out a tiny £5m buyback, but had it preserved cash, it could have bought back a huge chunk of shares instead. That’s on management:

I will give credit to LIO for outsourcing work to BNY Mellon and finding other cost-saving measures, to save up to £6m annually.

But my overall view of LIO’s strategy remains negative: it has too many funds and I don’t trust that they won’t try for another strange acquisition as they did with GAM. I think this company needs a fresh start under new management.

Roland's Section

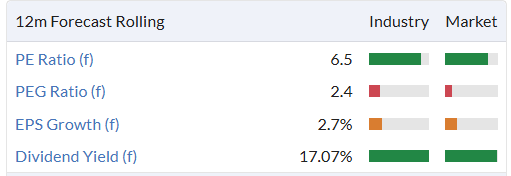

Vistry (LON:VTY)

Up 7.8% to 555p (£1.86bn) - Trading Update - Roland - AMBER/RED

This FTSE 250 housebuilder blotted its copybook with a Christmas Eve profit warning that made it three in a row since September.

Fortunately today’s update appears to be in line with the revised expectations laid out at the end of December.

Group adjusted profit before tax is expected to be c. £250m (FY23: £419.1m), in-line with the revised company guidance announced in December.

This profit figure would be a 40% decline on last year and is also an adjusted figure. We’ll have to wait for the company’s full-year results on 26 March for the full details of the adjustments, but here are some of the key numbers from today’s update.

Adjusted revenue +9% to £4.4bn;

Adjusted PBT down 40% to £250m

Year-end net debt: £180m (FY23: £88.8m)

Average month-end net debt £535m (FY23: £459m)

Note how much higher average month-end net debt was than the year-end figure – I believe more companies should report average net debt through the year, as the year-end figure is not always representative of year-long debt usage.

This financial performance was driven by higher volumes:

2024 completions rose by 7% to c.17,200;

Average selling price stable at £275k (FY23: £276k);

Sales rate up 11% at 1.07 sales per site per week (FY23: 0.96);

Forward sales of £4.4bn (Dec 23: £4.5bn).

Interestingly, peer Persimmon also reported a 7% increase in completions yesterday. These companies target slightly different parts of the market, but this does seem to suggest that conditions improved slightly for housebuilders last year, supporting higher volumes without price cuts.

Increase in unsold stock: Vistry’s profit slump despite higher revenues is a painful reminder that its business has not been performing as shareholders might have hoped. The company says there are three main reasons for this:

Delay to a number of partner agreements (for developments) now expected to complete in FY25

Vistry has withdrawn from some planned land transactions with other developers where it no longer feels the commercial terms are attractive

Some delays to open market completions

Today’s update also flags up a further problem which may help explain why adjusted profit performance is so weak – rising levels of unsold stock:

Working capital levels were higher than expected at the year end reflecting a slower open market sales rate than forecast and a resulting build up in stock. The Group is targeting a significant reduction in stock and work in progress levels in FY25 and will adjust build rates in line with changes in market conditions.

We’ll have to wait for the 2024 balance sheet for a more accurate idea of the numbers involved. However, this situation is a potential concern for me, especially as Vistry appears to be using a fair amount of debt through the year to fund its operations.

South Division issues: Vistry’s original September profit warning was blamed on cost control issues in its South Division. Today’s update leaves previous estimates of the impact on adjusted pre-tax profit unchanged at £105m in FY24, £50m in FY25 and £10m beyond FY25.

A new management structure and cost control enhancements are now said to be in place in the South and more broadly across the group.

Outlook: In FY25, the company expects “low single digit build cost inflation” and is confident of making year-on-year progress in profit and cash generation

Consensus forecasts suggest adjusted earnings could climb 28% to 72.3p per share in 2025, putting Vistry on a possible FY25 P/E of 7.1.

Roland’s view

Today’s update does not seem to flag up any serious new issues. I’m not surprised to see the shares rising slightly.

Personally, I have some concerns. The build-up of unsold stock is a potential worry. I’m also not convinced by the company’s continued focus on share buybacks, given the average month-end net debt of over £500m.

A total of £130m of buybacks have been announced so far with respect to 2024. These buybacks are still underway, but I think it’s plausible to argue they are responsible for much of the c.£91m increase in year-end net debt.

Buying back shares at a discount to book value is theoretically advantageous for remaining shareholders, as it should increase book value per share (assuming book value remains stable).

However, Vistry’s net interest costs were £28m in H1, or £56m annualised. These are real cash costs. Rising debt levels erode the company’s equity value and add risk for shareholders.

In my view, shareholders would be better served by Vistry becoming less reliant on borrowed cash before buying back its own shares.

At 555p, the stock continues to trade more than 10% below its last-reported tangible book value of 642p.

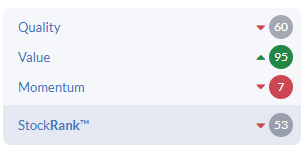

Stockopedia’s algorithms suggest Vistry could be a contrarian stock, with a high ValueRank and moderate QualityRank.

However, given the mediocre profitability and inconsistent performance of this business in recent years, I don't find Vistry very attractive. In my view, there are better choices elsewhere in this sector.

Vistry’s share price looks up with events to me, at least until we see evidence the problems highlighted in today’s update are receding. AMBER/RED.

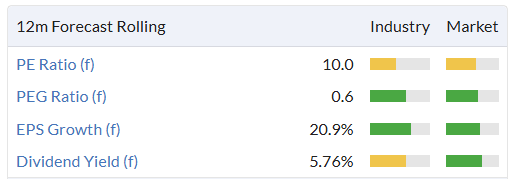

Frontier Developments (LON:FDEV)

Up 25% to 232p (£92m) - Interim Results - Roland - AMBER

Shares in this game developer have shot up today after Frontier delivered H1 FY25 results in line with expectations, maintaining the return to profitability reported for H2 FY24.

Today’s results cover the six months to 30 November 2024, so exclude strong trading over the festive period, when Frontier saw its third-highest ever festive sales:

After the end of the Period, strong sales across the portfolio in the Steam winter sale and other price promotion events delivered Frontier's third-highest festive sales performance, surpassed only by the stay-at-home boosted years of 2020 and 2021.

The Board remains confident of delivering FY25 revenue and profitability in line with expectations following the strong performance achieved in the first seven months.

Financial summary: today’s H1 numbers show the company’s profit margins are still a long way from the 20%+ enjoyed during the pandemic boom:

Revenue: £47.3m (HY24: £47.7m)

Operating profit: £4.5m (HY24: £(33.3m))

Operating margin: 9.5%

However, the accounts do flag up a return to positive cash generation, with net cash of £27.2m at the end of November (HY24: £17.1m) and £30.5m on 31 December 2024. A further increase seems possible for January, as management notes that the 31 Dec figure was “before receipt of December revenue”.

Trading commentary: game developers are in the hit business and one or two big hits (or flops) can make a big difference to annual results. This is illustrated here.

Frontier says that Planet Coaster 2 achieved the #1 chart position on Steam when it was released in early November. It subsequently contributed 22% of half-year revenue in less than four weeks of sales - that’s £10.4m of sales within the half year.

The company says total sales of Planet Coaster 2 reached 400,000 base game units within two months of release.

This is the first of three creative management simulation (CMS) games confirmed through the company’s strategic reset in 23/24, when it decided to concentrate on this traditional area of strength. The next planned release is a new Jurassic World title due in FY26.

Outside of CMS games, the Elite Dangerous space simulation game generated a substantial increase in revenue through new story elements and content. This game celebrated its 10th anniversary in December.

Outlook: company commentary seems to imply that there’s no change to expectations after today’s results:

The Board remains confident of delivering FY25 revenue and profitability in line with expectations following the strong performance achieved in the first seven months.

However, with thanks to Panmure Liberum, we can see that this broker’s expectations have changed slightly.

Panmure has tweaked its FY25 revenue forecast down to £85.9m (previously £88.3m) but is now forecasting improved profitability, with adjusted earnings of 1.9p per share (previously -1.4p per share).

Earnings are now expected to recover to a much healthier 19.2p per share in FY26.

These estimates price Frontier on a FY25e P/E of 122, falling to a FY26e P/E of 12.1 – potentially cheap, but presumably quite speculative at this stage.

Roland’s view

Frontier Developments has been through a torrid time in recent years, suffering a slump in sales and a period of losses following some strategic missteps.

One saving grace for the business (and its shareholders) has been the company’s strong net cash position. This has allowed Frontier to maintain development of new games and evolve its strategy without financial problems.

Revenue and profit growth look likely to remain lumpy and perhaps a little uncertain, given that the next big release is not due until sometime in the next financial year (June 25 onwards).

However, I think today’s update indicates the potential for this company to regain its mojo and deliver more attractive levels of profitability once more.

While I think the overall outlook remains quite speculative here, Frontier’s net cash balance now accounts for around one-third of its market cap and is sufficient to cover around six month’s operating costs. This should provide significant security for the business and its equity holders.

Given the company’s historic pedigree and the early success of its new strategy, I’m going to take a neutral view here. AMBER

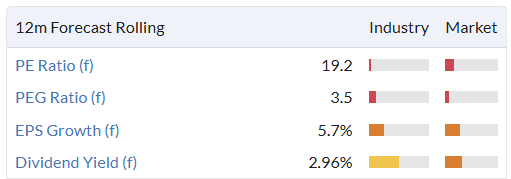

Genus (LON:GNS)

Up 19% to 1,694p (£1.1bn) - Half-year trading update (ahead of expectations) - Roland - AMBER

This animal genetics company is the top mover in the FTSE 250, up nearly 20% following an upgrade to full-year profit guidance.

The Board now expects Group FY25 adjusted profit before tax to be at the top-end of the range of market expectations in actual currency.

Genus is not exactly a household name, although many of us may have been exposed to its products. It uses “genomic selection” (genetic engineering?) to supply “semen, embryos and breeding animals with superior genetics to those animals currently in farms”

The company’s technology is currently applied to dairy and beef under the trademark ‘ABS’ and pork production under ‘PIC’.

Today’s update is brief. Performance during the half-year to 31 December 2024 was strong and the Board now expects to report adjusted pre-tax profit of at least £35m.

With thanks to broker Panmure Liberum, I can see that previous expectations for H1 were under £30m. So this upgrade represents a 17%+ increase.

ABS: the beef and dairy division is said to have performed in line with expectations with profit growth driven by “Value Acceleration Programme” initiatives. This sounds like a cost-cutting programme to me.

PIC: the pork business has traded ahead of expectations thanks to “greater volume” in both the Americas and Asia.

Growth opportunity? Genus appears to have a new offering known as the “PRRS Resistant Pig” programme that’s currently working its way through US regulatory approval. It looks like there could be some political exposure here, depending on the approach taken by the incoming US administration.

If approved, the expectation appears to be that this could be an important new source of growth for the business.

Outlook: management now expects profit for the full year to 30 June 2025 to be at the top end of market expectations. These are helpfully specified as £63.0m to £67.4m.

Panmure Liberum’s analysts have updated their FY25 full-year earnings estimates by 7.6% to 78.8p per share. That puts Genus on a forward P/E of 21 after today’s share price rise.

Roland’s view

This comment is only a quick review on today’s news from Genus. Anyone interested in investing would want to dig deeper to understand the company’s current offerings, market size and the PRRS programme.

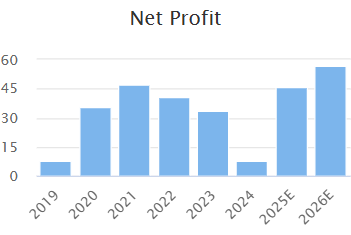

From a financial perspective, a couple of things strike me. Profits have been much higher in the past, but Genus appears to have suffered some kind of setback last year. I think this is partly cyclical, but I’m not sure if other factors are involved:

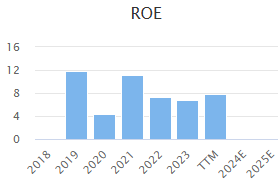

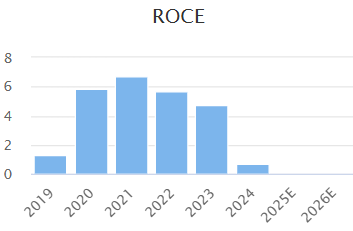

Profitability seems poor for such a highly-rated business. Even during the peak pandemic period, operating margins remained under 10% and return on capital employed was less than 8%:

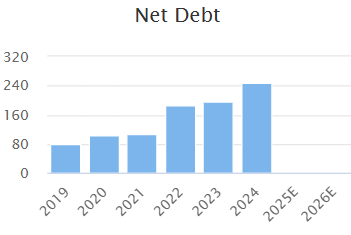

Net debt also looks a little high to me, at £248.7m as of 30 June 2024. This figure has more than doubled since 2021. It might be interesting to understand why. There are some leases in this mix, but most of it seems to be bank debt:

On balance, I’m going to take a neutral view here. Trading and profits appear to have some positive momentum and as Ed discussed recently, earnings upgrades can sometimes signify the start of a longer period of outperformance.

On the other hand, the balance sheet looks rather average to me and this business appears to face a mix of cyclical, political and regulatory risks. AMBER.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.