Good morning!

There are no big overnight moves to report - the FTSE is set to open unchanged at 10,600.

The US and Iran are likely to have face-to-face negotiations in the next two days, before the current ceasefire expires next Wednesday.

Leaving it there for today, thank you. Spreadsheet accompanying this report: link.

Company News

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Antofagasta (LON:ANTO) (£38bn | SR73) | Copper production down 19.2% to 143kt in Q1 (vs Q4 25). Cash costs up 13.5% to $2.77/lb. Full-year production guidance unchanged for 650,000-700,000 tonnes. Cash cost guidance also unchanged. | ||

Standard Life (LON:SDLF) (£7.2bn | SR69) | Acquisition for £2.0bn, funded through debt, cash and new shares equivalent to 15.3% of the group’s enlarged share capital. Expect total net synergy of £0.8bn and additional £190m adj op profit contribution by 2029. | ||

ROSEBANK INDUSTRIES (LON:ROSE) (£3.7bn | SR13) | Admission to Main Market will take place at 8am on 1 May 26. AIM shares will be cancelled from trading at the same time. | ||

Barratt Redrow (LON:BTRW) (£3.7bn | SR51) | 94% forward sold for FY26 (y/e 30 June). Expect events in the Middle East to have “limited impact on FY26 performance”, but visibility beyond the current year remains “more uncertain”. FY26 completions and adj pre-tax profit are expected to be in line with consensus expectations. | AMBER/GREEN ↑ (Roland) Everything has its price and I think shares in this housebuilder may be starting to look too cheap. While headwinds relating to volumes and costs remain a serious concern, Barratt shares now trade more than 45% below their last-reported book value, while offering a 6% dividend yield. The company also expects to end the year with net cash of more than £550m, providing a further margin of safety. I took a neutral view in February, but I share the StockRanks’ view that this could be a Contrarian opportunity so I am moving my view up by one notch today. | |

Great Portland Estates (LON:GPE) (£1.29bn | SR28) | 28 new leases and renewals in Q4, generating annual rent of c.£24m. On average, new lettings 15.8% ahead of March 2025 ERV. “We start the new financial year with positive momentum”. | ||

Saga (LON:SAGA) (£843m | SR47) | Revenue up 11% to £655m, underlying pre-tax profit up 19% to £44.2m, with strong growth in travel and insurance. Leverage ratio 3.7x (FY25: 4.4x). Outlook: expect further growth in profit and cash generation, with further reduction in leverage. | AMBER ↑ (Roland) My impression is that the quality of this business is improving and that Saga may be generating quite attractive returns on the capital employed within the business. However, I think the valuation is starting to look quite full and the outlook isn’t without risk. I’d also like to see some cleaner accounts, to gain confidence in continuing performance. After four-bagging in 12 months, I suspect the easy gains are in; I would not personally be inclined to buy at this level. | |

Hunting (LON:HTG) (£778m | SR89) | Solid Q1 performance, unchanged full-year EBITDA guidance of $145-155m. Seeing minimal impact in Middle East at this point, with continued order book momentum in S. America and US onshore. | ||

Thor Explorations (LON:THX) (£548m | SR99) | Gold poured down 15% to 20,256oz vs Q4 2025. FY26 production guidance unchanged at 75-85koz of gold, AISC guidance also unchanged at $1,000-$1,200/oz. | ||

Hollywood Bowl (LON:BOWL) (£443m | SR68) | Revenue up 9.5%, with like-for-like growth of 1.9%. 76% of electricity needs are hedged until the end of FY29. Expect to open three new centres in H2. | AMBER/GREEN = (Roland) [no section below] Hollywood Bowl’s share price is pretty much where it was when I last looked at the stock in December, and the outlook doesn’t seem to have changed either. My main niggle would be that like-for-like growth was minimal, with total revenue growth being driven by newly-opened centres from at least 12 months ago. Even so, net cash, a P/E of 12 and a 5% dividend yield seem undemanding. I’m happy to maintain our moderately positive view. | |

Rank (LON:RNK) (£422m | SR52) | Like-for-like net gaming revenue up 6% to £625.2m for the year to date. No material impact from energy costs expected in FY26 or FY27. Now expect FY26 adj op profit to be at least £68m (consensus £65.1-£68.2m). | GREEN ↑ (Graham) | |

Tatton Asset Management (LON:TAM) (£396m | SR55) | AUM +11% to £24.2bn, with underlying net inflows of £2.8bn and market performance of £2.5bn, excluding the previously reported cancellation of the £3.3bn Perspective mandate. Expect FY26 results to be “towards the upper end of market expectations”. | ||

Anglo Asian Mining (LON:AAZ) (£297m | SR48) | Copper production of 3,711t, gold production of 6,062oz. Total gold sales of 4,100oz at $4,728/oz, with copper concentrate sales of 18,553t valued at $45.6m. | ||

Ferrexpo (LON:FXPO) (£269m | SR61) | Production activities largely suspended in Q1 due to power shortages. Total Q1 production -45% to 593kt vs Q4 2025. The company continues to monitor its cash position and is actively exploring and progressing a number of potential funding options, which could include an equity capital raise. Funding issues and the ongoing VAT dispute “could give rise to material negative consequences for the Group”. | ||

Brooks Macdonald (LON:BRK) (£229m | SR47) | Total FUMA down £0.2bn to £19.9bn, with net inflows of £58m and £301m of adverse market and investment movements. FY26 expectations are unchanged. | ||

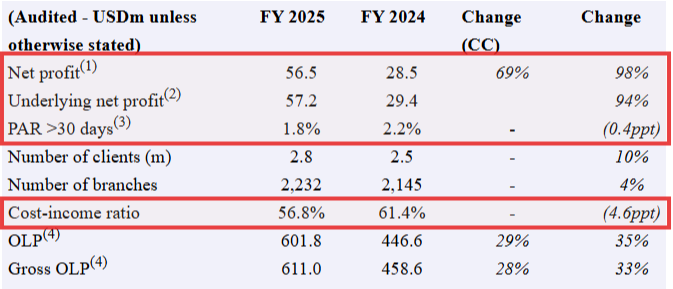

ASA International (LON:ASAI) (£214m | SR71) | Gross Outstanding Loan Portfolio up 33%. Net profit almost doubled to $56.5m. Underlying net profit +94% to $57.2m. Portfolio at risk improved to 1.8% (2024: 2.2%). “...overall, the Board believes the fundamentals of the business are strong with the Group being more resilient than was the case previously. The Group delivered growing levels of profitability in January and February of this year and demand for loans from clients is expected to remain resilient.” | GREEN = (Graham - I hold)

It’s hard to imagine that the full-year results could have been any better than this. But as I’ve repeatedly emphasised, this is not a low-risk blue-chip stock. ASA lends to its customers in local currencies, and the value of these currencies can be unstable, to say the least. A period of dollar strength would make ASA’s results look less impressive. | |

Made Tech (LON:MTEC) (£61m | SR82) | Awarded a new three year Strategic IT and Security Delivery Partner contract with the Government Digital Service. Total contract value £19 million, expected to contribute to FY27 and beyond. “The expected uptick in bookings during the second half supports current expectations for FY26 and enhances revenue visibility for FY27.” | (Graham) - this doesn’t change forecasts. | |

Robert Walters (LON:RWA) (£61m | SR45) | SP +4% First quarter trading in-line with the Board's expectations. Q1 Group net fees down 3%, or down 2% at constant currencies. Guidance for 2026 Group net fees remains unchanged. PanLib forecasts unchanged: FY26 and FY27 are both expected to be loss-making at the net income level, but operating profit should turn positive next year. The forecast EBIT loss this year is £8.7m, then an EBIT profit of £0.5m in FY27, and EBIT profit of £10.2m in FY28. | AMBER/RED = (Graham) [no section below] We were AMBER/RED on this last time and the market cap has shrunk further since then (from £85m). Today’s update has been well-received, as Q1’s year-on-year decline in net fees slows down to only 2% (e.g. H2 last year saw net fees down 14% year-on-year). Europe remains the major source of weakness, with net fees down 16%. I discussed the issues in the recruitment sector yesterday in relation to Pagegroup (LON:PAGE). Both large and small recruiters have been suffering, especially in Europe. It could be argued that most of the bad news is already priced in here at a market cap of just ~£60m, but I wouldn’t be in any rush to get involved here. Even if net fees are now bottoming out, the company is not profitable at this level of activity. | |

hVIVO (LON:HVO) (£60m | SR51) | Revenue of £46.8m (2024: £62.7m). Adjusted EBITDA of £1.4m (2024: £16.4m). In active discussions with ILiAD Biotechnologies regarding a human challenge trial. High single-digit revenue growth expected in 2026, weighted to H2. | ||

EnSilica (LON:ENSI) (£59m | SR56) | ENSI’s shares have been approved to trade on the OTCQX Best Market. Will commence cross-trading later today under the ticker symbol "ENSIF”. | ||

Iofina (LON:IOF) (£57m | SR81) | Produced 178.9 metric tonnes of crystalline iodine from its eight IOsorb® plants in Oklahoma, up 44%. Making good progress with the development of its new, larger IOsorb® plant with Western Midstream Partners in the Permian Basin. | ||

Digital 9 Infrastructure (LON:DGI9) (£54m | SR n/a) | Results for the year ended 31 Dec 25 & First Compulsory Redemption and Timetable | “Tangible progress delivering the managed wind-down”. NAV at year-end was 9.3p. Post year end received an early cash settlement for an earn-out for £10m. | |

Poolbeg Pharma (LON:POLB) (£31m | SR31) | UK Medicines and Healthcare products Regulatory Agency has granted Clinical Trial Authorisation for the POLB 001 TOPICAL trial. The trial remains on track to deliver interim data this summer. | ||

Windar Photonics (LON:WPHO) (£27m | SR10) | “Strongest ever first quarter in terms of new test order activity.” Expects FY26 revenue of at least €7.8m (up 22%), adjusted EBITDA of at least €0.5m. Share subscription agreement for up to £20m over three years. Deal includes warrants. | ||

M Winkworth (LON:WINK) (£22m | SR85) | Revenue flat (£10.74m). PBT down 11% to £2.1m. Cash £3.9m. “After a steady start to the year, early 2026 trading across our network has been resilient, with sales applicant registrations and agreed sales broadly in line with recent years.” | ||

Metals One (LON:MET1) (£21m | SR5) | Update on the proposed acquisition in South Africa by Lions Bay Resources (LBR). MET1 owns 30% of LBR. LBR has submitted revised offers to the Business Rescue Practitioner. | ||

Frontier IP (LON:FIPP) (£13m | SR11) | The European Commission has approved €211 million in Italian State Aid for CamGraPhIC, a subsidiary of FIPP’s portfolio company 2D Photonics. |

Graham's Section

ASA International (LON:ASAI)

Up 6% at 226p (£225m / $305m) - FY2025 Results - Graham - GREEN =

(At the time of writing, Graham has a long position in ASAI.)

ASA International Group plc (LSE: ASAI), one of the world's largest international microfinance institutions, is pleased to announce its audited results for the twelve month period ended 31 December 2025.

This is a recent holding for me, and one that I’m still quite excited about. It’s primarily a value play for me:

That said, the growth it’s achieving is not to be sniffed at, either.

In 2025:

Loan portfolio +33% to $611m

Underlying net profit +94% ($57.2m)

Actual net profit +98% ($56.5m)

A small gap between underlying net profit and actual net profit is always a green flag for me, and that’s the case here.

Arrears: ASAI lends to millions of micro businesses (primarily female entrepreneurs), charging high rates of interest, but arrears are remarkably low. And despite the growth achieved over the past year, portfolio quality has apparently improved.

Portfolio at risk >30 (payments outstanding for more than 30 days) has fallen to only 1.8%. A year ago, this was 2.2%.

Here are the KPIs in table format. I’ve highlighted the big three financial KPIs at the top. Also the key profitability metric for financials, the cost-income ratio, which fell considerably in 2025 (the lower the better).

Dividend: the full-year dividend has doubled to USD 0.143. The payout ratio remains 25%.

CEO comment: he describes 2025 as “an outstanding year for ASA International with the delivery of both strong operational growth and significantly increased levels of profitability.”

New product: in partnership with a Ugandan company, ASA is now offering credit life insurance along with its loan products, and will be expanding this across all of its African markets.

Outlook:

The Board continues to closely monitor the impact of the ongoing conflict in the Middle East and any potential impact on economic activity, inflation, local currencies and growth in ASA International's operating countries.

Notwithstanding these external factors, overall, the Board believes the fundamentals of the business are strong with the Group being more resilient than was the case previously. The Group delivered growing levels of profitability in January and February of this year and demand for loans from clients is expected to remain resilient…

Competition: kudos to the company for summarising its view on the competitive landscape:

The competitive landscape remains broadly unchanged with the strongest competition being faced in The Philippines, Nigeria, Tanzania, and Uganda. In most other markets, competition from traditional microfinance institutions is less intense. Competition from pure digital lenders has not had a meaningful impact thus far given the product offering and client engagement model is very different.

Graham’s view

It’s hard to imagine that the full-year results could have been any better than this.

But as I’ve repeatedly emphasised, this is not a low-risk blue-chip stock.

The geographic footprint is:

· East Africa - Tanzania, Kenya, Uganda, Rwanda and Zambia

· West Africa - Ghana, Nigeria, and Sierra Leone

· South East Asia - The Philippines and Myanmar

· South Asia - Pakistan, India and Sri Lanka

ASA lends to its customers in local currencies, and the value of these currencies can be unstable, to say the least.

2025 saw dollar weakness and as ASA reports in dollars, that's a significant tailwind to performance. A period of dollar strength would make ASA’s results look less impressive.

The use of many different currencies also leads to complexity when trying to understand results. For example, consider this snippet:

South East Asia continued to demonstrate underlying resilience in 2025. Reported financial performance and operational data, however, was impacted by a change in how Myanmar's results are translated into USD, following the updated IFRS IAS 21 accounting standard relating to lack of exchangeability. Market rates are now used as opposed to the central bank rate utilised in 2024.

In short, the use of a different interest rate has led to a completely different result when measuring the size of ASA’s business in Myanmar. A reminder that there are often surprises contained within the financial statements of a business like this!

The balance sheet now has equity of $161.8m, up from $96.5m a year ago, thanks both to the excellent profit performance and to favourable currency movements.

The market cap is twice the company’s balance sheet value, so this isn’t a deep value play in the sense of having balance sheet support - it’s all about earnings.

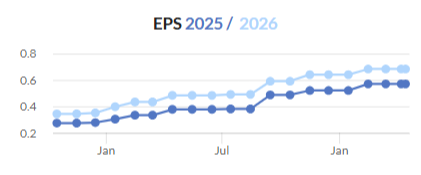

And earnings forecasts have been going in one direction only:

I’d never want this to be a pillar of my portfolio, due to the inherent risks in microfinance and in emerging market investments. But it’s currently just 2% of my portfolio now, and I do wish it was a little more.

Rank (LON:RNK)

Up 12% at 101.6p (£476m) - Q3 2025/26 Trading Update - Graham - GREEN ↑

It’s a positive update from this casino and bingo hall operator.

Year-to-date NGR (net gaming revenue) is up 6%, with all sectors roughly equal year-to-date

Grosvenor +6%

Digital +6%

Mecca (bingo) +5%

Enricha (Spain) +7%

Grosvenor venues, the largest division, has received a nice boost from additional gaming machines. These were enabled by recent legislation:

Grosvenor venues LFL NGR grew 5% in the period. Whilst it is likely that the Middle East conflict will create ongoing uncertainty around international travel, we expect to see continued revenue growth in Q4. At a product level, gaming machines were the fastest growing vertical, +10%, with significant room for further improvement as we optimise the performance of the additional machines.

And the outlook:

The Group expects to deliver further year-on-year revenue growth in Q4 and full year LFL underlying operating profits are expected to be at least £68m. This takes account of energy cost volatility which, based on current market prices and reflecting the Group's hedging policy, is not expected to have a material impact on profitability in 2025/26 or 2026/27.

As a primarily physical, land-based business, Rank is highly vulnerable to energy, labour and other fixed costs. So the news that energy costs aren’t going to hit the company for the next few years is very reassuring. Of course the hedges will run out some day!

Estimates: Shore Capital were previously estimating like-for-like underlying operating profit this year of c. £65m, vs. new guidance of £68m. They have raised their FY June 2026 EPS estimate today by 5% to 9.6p. FY June 2027 is also seen at 9.6p.

That puts the shares on a P/E multiple today of 10.6x.

CEO comment:

"Having implemented the actions required to mitigate much of the impact of higher RGD in our UK digital business, and with clear plans in place to drive sustainable revenue growth, the Group is well placed to deliver the medium-term objective of generating at least £100m operating profit."

Rank’s Digital business is vulnerable to RGD, but the mitigation efforts must be working out very well so far, given today’s guidance.

Graham’s view

I’ve been AMBER/GREEN on this one (see here) and I am tempted to upgrade it further today.

Net cash was last seen at £39m, giving it some flexibility to deal with whatever challenges it might face next - whether that is energy costs, legislative change, etc. Or it might find new opportunities to invest for growth and hit that £100m operating profit target.

It’s a little risky but I’ve been pretty positive on this one for a while, and it seems to be building up some real business momentum. I’ll therefore go fully positive on it today, as I see value at this level:

Roland's Section

Saga (LON:SAGA)

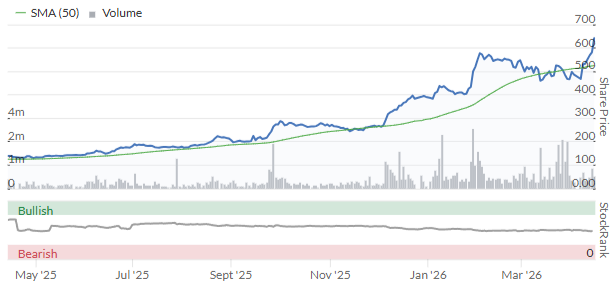

Up 11% at 645p (£935m) - Preliminary results for the year ended 31 Jan 2026 - Roland - AMBER ↑

This over-50s travel and insurance group has attracted a lot of investor interest over the last year as its turnaround has gathered pace. Various well-known fund managers have discussed the stock publicly, including Alyx Wood at November’s Mello.

Saga’s share price has doubled since Mello and has four-bagged since our last (negative) view in April 2025:

Quite a lot seems to have changed over the last year. I reckon today’s full-year results offer a good opportunity for us to refresh our view and bring our coverage up to date.

FY26 results highlights

Saga completed the sale of its insurance underwriting unit to Ageas last year. This has left the group with two divisions: Travel and Insurance Broking.

Today’s headline financial figures focus on Saga’s continuing operations:

Underlying revenue up 11% to £654.6m;

Underlying pre-tax profit up 19% to £44.2m;

Net finance costs up 61% to £43.1m;

Underlying earnings per share up 69% to 30.6p;

Net debt down by 16% to £499.5m (FY25: £592.8m);

Net debt/EBITDA leverage: 3.7x (FY25: 4.4x).

Including discontinued operations adds a further 10.5p per share to earnings, giving total underlying earnings of 41.1p per share.

I’m pretty sure this is the correct metric to use as a comparison with broker Singer Capital’s March 2026 FY26 forecast of 41.6p per share – so I would conclude these results are in line with latest forecasts.

There are quite a lot of moving parts in today’s results, but I think the key elements to look for are evidence of strong trading, cash flow/debt reduction and profitability. I’ll try and address each of these in turn before considering valuation.

Trading - Travel

Travel trading performance appears to have been strong last year, with both revenue and margin growth in all three sub-segments. Forward bookings also look fairly healthy to me and the company stresses that its exposure to the Middle East is minimal – evidently this is not a popular destination for Saga customers.

Note that Saga owns both ocean and river cruise ships, but its holiday business is capital-light – the company doesn’t own hotels or similar.

Ocean Cruise: revenue up 12% to £265.6m, underlying pre-tax profit up 38% to £67.3m (25% margin).

Load factor for 26/27 bookings is currently 79%, unchanged from last year. The average per diem value of forward bookings rose by 13% to £447. Fuel prices are 100% hedged for FY27 and 75% hedged for FY28, although the company remains exposed to the risk of fuel shortages.

River Cruise: revenue up 8% to £53.4m, underlying pre-tax profit up 48% to £5.9m (11% margin).

Load factor for 26/27 bookings is currently 73%, improved from 68% at the same time last year. The average per diem value of forward bookings rose by 3% to £372 last year. Fuel hedging is as per my comments above.

Holiday: revenue up 10% to £185.1m, underlying pre-tax profit up 31% to £14.0m (8% margin).

Marketing expenses rose by 17% to £12.7m last year as the company invested to drive growth. However, this was partially offset by a £0.4m reduction in other operating expenses at an improved investment return of £1.5m, supporting improved overall profitability.

Revenue from bookings for FY27 departures rose by 4% to £165.9m as of 12 April 2026, while passenger numbers were flat at 51.6k (13 April 2026: 51.5k).

Trading - Insurance

The economics of this business have changed significantly with the sale of the underwriting unit. Going forward, Saga will increasingly just earn a commission on each sale, without carrying any underwriting risk. This reduces the capital requirements of the insurance business. I would expect that it will also smooth out profitability, albeit ultimate returns might be lower.

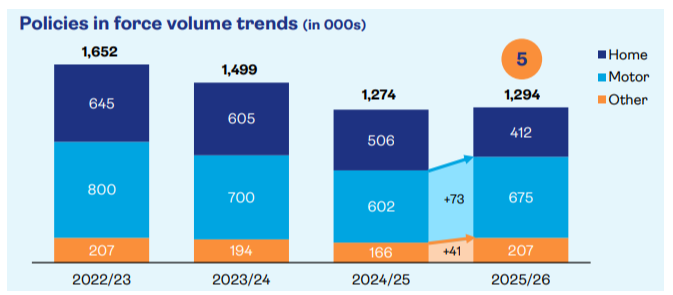

Happily, Saga’s rejuvenated insurance sales efforts appear to have borne fruit last year. The number of in-force policies rose last year following several years of decline:

The outlier in the chart above is Home insurance, where the number of in-force policies fell again. However, the profitability of both home and Other insurance sales was much stronger than the ultra-competitive Motor business.

My reading of this is that Saga’s wealthy and older customer base are still willing to shop around when it comes to car insurance. The company’s preferred metric of gross profit after marketing expenses highlights the variation in profitability across product lines:

Motor: £29.3m (10% of gross written premium)

Home: £29.3m (22% of GWP)

Other: £37.9m (27% of GWP)

Overall insurance underlying pre-tax profit rose by 15% to £16.5m, on a continuing basis.

Cash flow & debt reduction

Saga’s debt burden debt situation has attracted some very mixed views in the investor community. The main divide appears to be over how much of a concern the cruise ship debt should be, given that it’s backed by tangible assets that could presumably be sold if needed.

I can see this argument, but you will probably not be surprised to learn that I’m not inclined to ignore debt that’s secured on depreciating assets with limited liquidity.

The fact that Saga’s cash interest and financing costs rose by 55% to £67.1m last year supports my view that the group’s balance sheet deserves my attention.

Saga reported a leverage ratio of 4.4x EBITDA at the end of January 2025. This ratio fell to 3.7x last year, thanks to higher profits and a £93m reduction in net debt to £499.5m.

3.7x EBITDA is still much higher than I’d like to see and it seems founder family member and chairman Sir Roger De Haan agrees – the company’s target is to reduce leverage to under 2.0x by 2030.

Good progress was made last year, although this was aided by some of the cash received from the sale of the underwriting business. Prior to today, broker forecasts were for net debt to fall by c.£50m per year in both FY27 and FY28.

Based on my reading of today’s cash flow statement, this looks realistic to me and perhaps even a little too conservative (i.e. debt might reduce faster). I should caveat this by saying that the accounting for the sale of the underwriting business is quite complex and a clearer picture should emerge over the course of this year.

Profitability

I’m happy to assume that Saga’s debt position and repayment plans are sustainable and realistic, based on steady-state operations (i.e. no major disruption to travel or insurance sales).

Given this, I want to know if the business is likely to generate attractive returns for shareholders from these operations – how profitable is it?

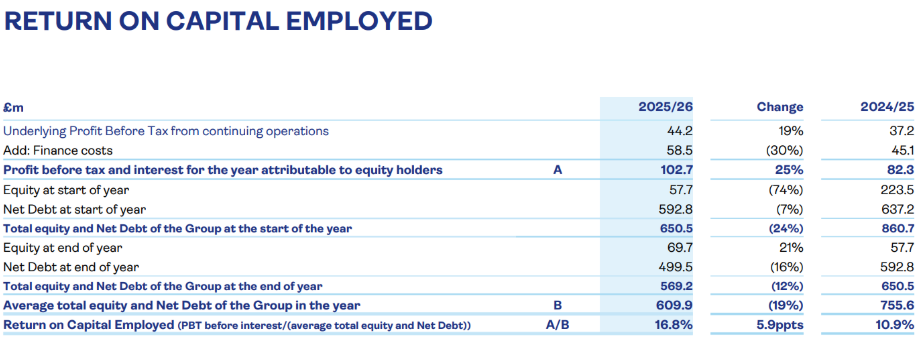

It pains me to write this, but I am (mostly) happy to accept today’s underlying pre-tax profit from continuing operations of £44.2m as a reasonable proxy for continuing pre-tax profit from the business.

While this year’s statutory profits have been hit by large restructuring charges and various other issues, I think these should largely cease from FY27.

By adding back finance costs from continuing operations of £58.5m, I get a pro forma pre-tax profit estimate of £102.7m. Applying this to the company’s balance sheet gives me an estimated return on capital employed of 15%

Saga offers this view today, suggesting a very similar return on capital employed of 16.8%:

My tentative conclusion is that Saga’s business (and its expensive floating assets) are probably generating quite decent returns.

This gives me additional confidence the company should be able to continue reducing its debt levels.

Outlook & Valuation

My review of Saga’s results hasn’t unearthed any obvious problems. The final question is whether the shares are still attractively valued, having four-bagged in 12 months.

The company’s outlook statement is positive but non-specific:

Following the performance delivered in 2025/26 and the strong forward bookings in Travel, we look ahead to 2026/27 with confidence and expect to deliver continued growth in both profit and cash generation. Underlying Profit Before Tax is expected to take a further step forward [...]

Saga expects underlying pre-tax profit from the Travel business to rise this year, but profits from insurance are only expected to be “at least in line with 2025/26”.

I don’t have access to any updated forecasts today, but I can see forecasts from 13 March 2026 on Research Tree, with thanks to Singer Capital:

FY26 actual adj EPS comparative: 30.6p (continuing operations)

FY27E adj EPS: 36.5p (+19% vs FY26)

FY28E adj EPS: 43.5p (+19% vs FY27E)

This suggests a pleasing run of double-digit percentage growth over the next couple of years, paired with falling leverage.

However, I think it’s fair to say some of this is already priced in.

Saga shares are up by c.10% today as I write, at 640p. This gives me a FY27E P/E of 17, falling to a P/E of 15 in FY28.

I’m not sure I see much value at this level, especially given the continued dependence on deleveraging.

Roland’s view

Prior to today, the StockRanks viewed the shares as a Momentum Trap, raising the possibility that the valuation had run ahead of events.

The poor statutory figures reported today (including many adjusting items) may mean the StockRank remains subdued.

My personal view on this initial review of Saga is that the quality of the business is improving but the valuation is very much up with events.

Risks remain too, both at a macro level and due to the continued demands of generating sufficient cash to reduce leverage to a more sustainable level.

Graham was RED on Saga one year ago when he reviewed the company’s last set of annual results.

I am going to move our view up by two notches to AMBER today. I don’t see any serious fundamental issues, but I think the shares are starting to look quite expensive.

Barratt Redrow (LON:BTRW)

Up 2% at 264p (£3.68bn) - Third Quarter Trading Update - Roland - AMBER/GREEN ↑

Barratt Redrow’s financial year ends on 30 June. Today’s update suggests the company has good visibility on meeting its targets for the year, with 94% of homes now forward sold for the period (FY25: 96%).

The company also reminds us that it has a better-than-average record of building houses that create satisfied customers:

Retained five-star homebuilder status for the 17th consecutive year - an unparalleled industry record.

Although home completions lagged behind the same period last year, management says this reflects the end of the Stamp Duty holiday last year. Increased construction work is currently in progress and the company has left previous guidance for 17,200 to 17,800 home completions this year unchanged today.

There’s also a slight increase in the net private reservation rate. This rose to 0.64 in Q3, up from 0.62 in the prior-year period. This metric measures reservations per active sales outlet per week.

This modest increase in activity has helped to drive an increase in the order book, with total forward sales up by 11% to 11,395 homes. That’s equivalent to an order value of £3,539m (30 March 25: £3,139m).

Within this total, the private home order book is 2.5% higher, at 5,643 homes, mirroring the rise in private reservation rates.

While I see any increase in private sales as positive, this figure only represents half the total forward order book. I think this highlights Barratt’s growing dependence on lower–margin affordable housing and JV sales, continuing a trend highlighted in the half-year results.

Rising net cash & slowing land purchases

Barratt expects to end the year with net cash of between £550m and £650m, £150m ahead of previous guidance of £400 to £500m. Management says this relates to the timing of building safety remediation payments and reduced land investment.

The company had already planned to slow its land purchase rate this year, but we learn today that further cutbacks have been made:

Now, with a less certain backdrop, given recent geopolitical events and their likely impact on mortgage rates and build cost inflation, we are being even more selective.

In this context, we now anticipate total land approvals for the financial year will be between 7,000 and 9,000 plots, below our previous guidance range of between 10,000 and 12,000 plots and land spend of between £700m and £800m, from our previous guidance range of between £800m and £900m.

It’s not unusual to see housebuilders accumulate cash during a slowdown as sales run ahead of inventory replacement rates. Of course, this process will need to be reversed at some point.

Outlook

[...] we are reiterating our unchanged guidance for FY26 total home completions of between 17,200 and 17,800 (including c.600 JV) homes and we are on track to deliver adjusted profit before tax in line with consensus expectations.

Consensus forecasts for adjusted pre-tax profit are given as £568m, within a range of £534m to £586m.

Roland’s view

I’ve looked at a number of housebuilders recently and my view has been that a number of stocks in the sector look like they should be offering value, with discounts to book value and solid balance sheets.

The caveat is that it’s not clear to me where the catalyst will come from that’s needed to resolve the tension between costs, planning holdups and pricing power. Housebuilders’ margins are under pressure and the situation doesn’t seem to be improving.

Barratt doesn’t comment on profit today except to reiterate guidance for adjusted profits to be in line with expectations.

This leaves the shares trading at a very modest multiple of earnings, with a well-covered dividend and a near-50% discount to book value:

My feeling is that the stock is probably offering some value at this level, for investors sufficiently patient to wait for a recovery. The StockRanks share this view with Contrarian styling, but the ultra-low MomentumRank is perhaps a warning that the outlook remains uncertain and that patience is likely to be needed:

Barratt shares have de-rated massively over the last five years and are now trading at levels first seen more than 10 years ago:

On a medium-term view, I think this decline may have gone too far. While the outlook may be weak, I think the company’s balance sheet and discount to NAV should provide a margin of safety, with the potential for a re-rating over time. To reflect this view, I am upgrading my previous neutral view to AMBER/GREEN today.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.