Good morning! I'm expecting a fairly quiet day for news, according to this week's Week Ahead.

Today's Agenda is complete. The deluge of full-year results has finally ended!

2pm: all done, it's a clean sweep!

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Bakkavor (LON:BAKK) (£1.03bn) | Statement re Possible Offer | Agreement in principle with Greencore (LON:GNC). 85p plus 0.604 GNC shares, ~200p total (last close 177.8p). It’s a 32.5% premium to the undisturbed share price. The previous revised proposal was 85p in cash plus 0.523 shares, which was a 25% premium. | PINK (Graham) [no section below] |

Chemring (LON:CHG) (£1.03bn) | Contract Award | SP +3% MoD multi-year missile defence contract. £251m over six years but "industry partners" will "deliver the significant majority of contract value". | AMBER (Graham) [no section below] This is a nice update that at least quantifies the size of the overall contract and outlines the strategic importance to Chemring (and its Roke subsidiary) of being at the heart of UK missile research and development. I like Chemring but this could have been a much more helpful RNS if they had outlined how much of this contract will convert into their own revenues, and how much of those revenues were already baked into their forecasts . For now I remain neutral as while I do think that prospects are bright, it's highly rated already and performance can be volatile. |

Raspberry PI Holdings (LON:RPI) (£911m) | Final Results | Rev -2%, adj. EBITDA -15%, adj. PBT -57%. “Resilient” (?). Expects demand to build up in 2025. | AMBER/RED (Graham) Very popular products with a thriving community but the valuation of this stock is not currently adding up for me. |

Capital (LON:CAPD) (£122m) | Contract award at Reko Diq | Mining services, $60m Rev. pa once fully operational, through to 2028 with 5-year extension. |

AMBER (Mark- I hold) [No section below] |

Intercede (LON:IGP) (£84m) | New contract orders | US/Mid East orders worth $4.45m. FY25 revenue ahead of exps and enhances the FY26 backlog. | AMBER/RED (Mark) [No section below] |

Topps Tiles (LON:TPT) (£67m) | HY TU | H1 sales +4% to £127.7m, cost environment remains challenging, H2-weighting for profits. CMA agreement in principle on store disposals. | AMBER (Mark) |

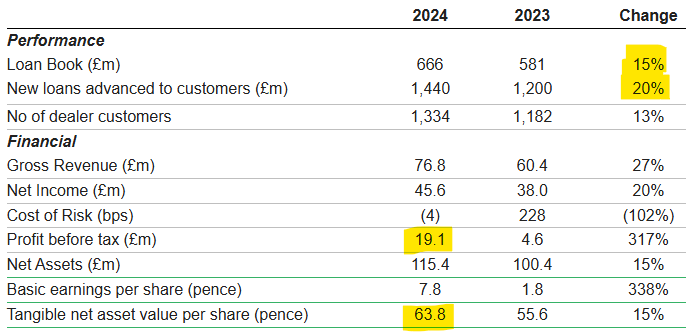

Distribution Finance Capital Holdings (LON:DFCH) (£65m) | Final Results | Loan book +15%, rev +27%, PBT £19m (last year: £4.6m). Outlook: on the way to high-teens ROE. | GREEN (Graham) |

Argentex (LON:AGFX) (£49m) | Final Results | Rev +1% to £50.3m, Operating Loss £0.2m, net cash £18.4m. | AMBER (Mark) [No section below] |

HSS Hire (LON:HSS) | Sale of HSS Ireland | £26.2m received. c.1x sales, 7x EBITDA, 1.8x Net Assets. | AMBER (Mark) |

Gear4music (HOLDINGS) (LON:G4M) (£28m) | TU | PW. Sales +2%. EBITDA expected to be +6% to £10m vs £11.7m consensus. PBT £1.6m vs £2.8m expectations. Progressive cut 2026 EPS by 44%. | BLACK AMBER/RED (Mark) |

Gattaca (LON:GATC) (£26m) | Interim Results | Revenue +3%, net fee income -3%, underlying PBT -15% to £1.0m. Guidance for FY25 underlying PBT remains in line at £3 million. | GREEN (Mark - I hold) |

XLMedia (LON:XLM) (£14m) | Earnout received | Received $7.5m = $3.8m Fixed Consideration + $3.7m million Earnout Consideration. | AMBER/RED (Mark) [No section below] |

| Brighton Pier (LON:PIER) (£6m) | Proposed cancellation | Reasons given: cost and regulatory burden, cheaper refinancing, limited liquidity, etc. Costs expected to reduce by between £250k and £300k p.a. Separately there is a trading update: 2024 is in line but in the first 12 weeks of the new year, sales are down by £0.1m at £4.2m. | Graham [no section below] All stocks worth £10m or less should come with a special health warning that the costs of being publicly traded are likely to be unsustainable for companies of this size. In PIER's case, the annual costs are 5% of their latest market cap. They have been listed since 2013 but financial performance has been very poor in recent years. Net debt was last reported at £7.6m. |

Graham's Section

Distribution Finance Capital Holdings (LON:DFCH)

Down 6% to 35.25p (£64m) - Full Year Results - Graham - GREEN

Distribution Finance Capital Holdings plc, the specialist bank providing working capital solutions to dealers and manufacturers across the UK, today announces its audited results for the year ended 31 December 2024.

I’m looking forward to speaking with company management at DFCH for the first time, later this morning.

I previously covered DFCH’s trading update here. The company’s main product is inventory finance (short-term loans for an average of 145 days), although it is also branching out into new products.

Key sectors include motorhomes and caravans, marine, motorcycles and automotive.

I’ve highlighted some of the figures that stand out to me in these full-year results:

Firstly we have good top-line growth, with a 15% increase in the loan book and a 20% increase in new loans to customers.

PBT has quadrupled to £19m although this does include a £4.7m write back of a provision made in 2023 (relating to the collapse of a caravan park).

It’s probably far more realistic to take that £4.7m write back and apply it to 2023, instead.

So that would make 2024 adjusted PBT £14.4m, and 2023 adjusted PBT £9.3m. The company previously guided that 2024 adjusted PBTwould be not less than £14m.

The loss on the caravan park is a stark reminder that even one major default can be very costly for a lender of this size.

The market is keenly aware of this and indeed the current level of risk aversion puts DFCH on a discount to its tangible book value of nearly 45% (share price 35.25p vs. tangible net asset value per share 63.8p).

The current position re: arrears sounds fine:

Strong credit risk performance with continued low number of arrears cases: 33 dealers (2023: 30), with arrears one day past due and in legal recovery, representing less than 3% of the Group's entire dealer customer base

I note that the cost of risk (adjusted for the loss mentioned above) was 0.75% in 2024, down from 1.36% in 2023.

Given that DFCH is earning a net interest margin of 7.9%, it must be charging quite high APRs to its borrowers.

CEO comment:

2024 was another year of significant progress for the Group, marking our third consecutive year of profit growth since our authorisation in 2020. This year, we have continued to scale the bank in our core inventory finance lending space, whilst also making investments in new products and services, bringing to life our ambitions to become a multi-product lender. I am incredibly proud of the team and the products we are bringing to life for our customers. We have an exciting journey ahead of us."

The Chair is no less enthusiastic, with this particular comment from the Chair’s statement standing out to me:

Our singular focus on reaching profitability quickly after authorisation has paid off. We have a strong financial base and accretive capital position that allows us to grow at meaningful levels year-on-year. We are now in a virtuous circle of scale, generating increasing levels of annualised earnings, which in turn creates capital unlocking further scale in our lending capacity.

As a small bank scales up, it should become more profitable, e.g. with a lower cost-income ratio (as operating expenses are spread out over more revenues) and a higher return on equity (as its balance sheet equity is used more efficiently to churn out profits).

DFCH did not make progress in 2024 in terms of its cost-income ratio, which increased slightly to 59%, but says that it expects this ratio to fall to less than 50% by 2028.

Adjusted return on equity did increase, from 6.7% to 9.8%.

Bespoke lending: this has grown from £18m in 2023 to £75m in 2024, and includes a range of tailored products for particular customers. I’m not sure how shareholders can assess the risks taken by DFCH here.

Asset finance: they are entering the hire purchase and leasing business for consumer borrowers. With so many legal issues currently facing the sector, at least they enter it without the distraction of unknown liabilities for any prior business they’ve done. Their entry point is in the motorhomes and caravans sector, where they already have a strong industry footprint.

Deposits are a major source of funds with £650m at the end of the year from depositors.

Outlook:

We are at an exciting point in the Group's strategic journey. 2025 will see us truly become a multi-product lender, with significant opportunity to grow our lending and further scale the bank. With scale comes increasing returns and, being on the cusp of double digit returns in 2024 already, we believe we are well on our way to achieve the high-teens ROE we have talked about for some time.

Graham’s view

I’m happy to upgrade this to GREEN as I’m not seeing what the catch is. I’m generally positive on cheap lenders in this market and DFCH falls into this category:

The algorithms classify it as a “Turnaround” having both Value and Momentum, but lacking in Quality.

However, I think Quality is likely to improve as the company grows, which will complete the third leg of the stool.

Please note that the shares are illiquid with 75% held by top holders.

And as with all lenders, do tread carefully - although I’m a huge fan of the value on offer in the sector, based on past experience I would not wish to have a very large holding in any one particular lender.

Raspberry PI Holdings (LON:RPI)

Up 6% to 497p (£970m) - Full Year Results - Graham - AMBER/RED

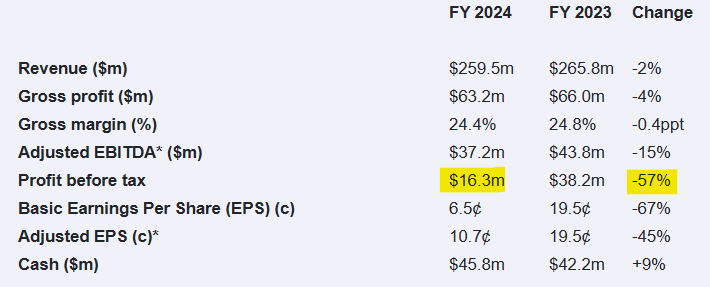

Raspberry Pi (LSE: RPI), a leader in high-performance, low-cost computing, is pleased to announce its audited results for the year ended 31 December 2024 ("FY 2024").

It always makes me wonder when I see a company describe its results as “resilient”, after posting a PBT movement like this:

If a 57% fall in PBT is “resilient”, then I shudder to think what a non-resilient result would look like!

Checking the financial notes, I see that the gap between adj. EBITDA and statutory profits includes a $6m charge relating to employee share schemes. So I certainly wouldn’t want to treat adj. EBITDA as the “real” profit figure - something halfway between adj. EBITDA and actual PBT might be fair.

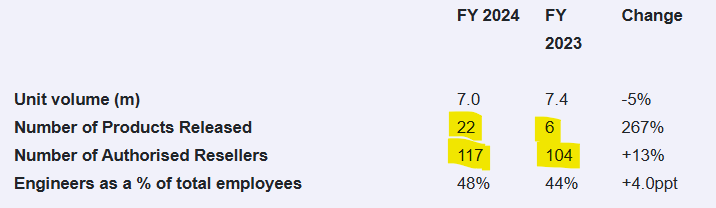

Operationally it was a busy year, with many new products released and more resellers signed up:

Remember that this has been listed for less than a year. The offer price was only 280p so investors at that level are still doing extremely well, despite the recent pullback:

A major seller at IPO was the Raspberry Pi foundation, still a 49% shareholder, which is a charitable organisation that promotes coding for young people.

Outlook:

With channel inventory now normalised, Raspberry Pi anticipates a steady build-up in demand throughout the year, positioning us strongly despite ongoing macroeconomic and geopolitical uncertainties. The projected pace of market recovery, coupled with the timing of embedded design wins, strengthens confidence in solid and sustainable sales growth in full-year 2025.

Given the planned product release schedule and mix of sales, gross profit per unit is expected to increase year-on-year. The Company has secured a sufficient supply of memory to meet expected demand into Q4, helping to sustain favourable unit economics for the year ahead. Medium-term fundamentals remain positive…

Graham’s view

This is currently categorised as a Momentum Trap due to a low QualityRank and ValueRank. The only bright spot is Momentum but even there, I wonder how long a positive Momentum score can last when the 3 month chart looks like this?

I understand that the Raspberry Pi brand has a devoted following - I’ve met some of them - and I have some appreciation of the immense value that this company provides to computing enthusiasts and students.

However, the valuation of the stock is not adding up for me:

I’m going to put an AMBER/RED on this to reflect that it seems excessively valued. I also note that it passes two bearish stock screens - both the James Montier “Unholy Trinity” screen and his “Cooking the Books” screen.

Mark's Section

Gattaca (LON:GATC)

Flat at 83.5p - Interim Results - Mark (I hold) - GREEN

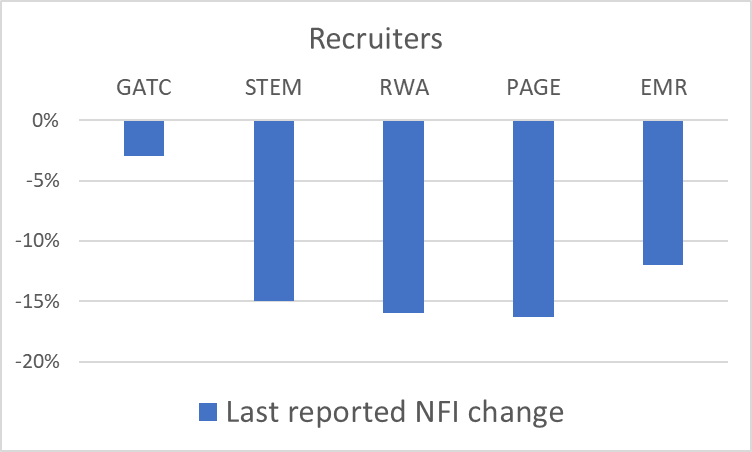

These don’t look like anything to write home about, with Net Fee Income down 3%, until you compare this with other recruiters:

This is a significant outperformance versus the sector. At many times, recruitment is a scale business, and the largest players trade at the highest ratings, reflecting their bigger market share. However, in the current market conditions, being nimble and being able to increase contractor numbers has certainly paid off for Gattaca. They are suffering in the same way as the rest of the sector:

The persistent macroeconomic headwinds impacting the broader recruitment sector have demonstrably affected both client demand and candidate sentiment, reducing volume and extending recruitment timelines. This has acted as a headwind on our recent performance. Specifically, permanent recruitment remains subdued, and we anticipate this trend to continue in the medium term. In response, our strategic focus remains on expanding our contractor base, which has shown greater resilience, investing in core markets where we see growth opportunity, alongside rigorous proactive cost management.

The result is that they continue to guide in line with market expectations for the full year:

Group guidance for FY25 continuing underlying profit before tax remains at £3 million.

Research provider Equity Development turn this into 6p of adjusted EPS. Some caution is required, as included in the adjustments are restructuring costs, which appear to have a tendency to be recurring rather than one-off. However, the overall amounts are not huge for this half:

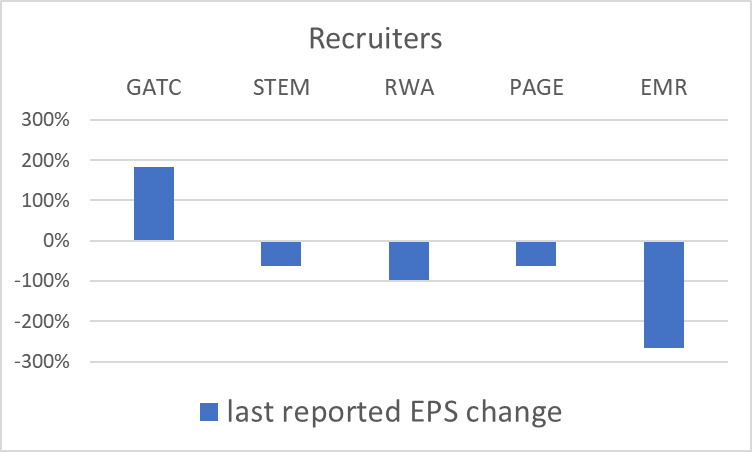

Even accepting the adjustments at face value, 6p EPS doesn’t make the shares look immediately cheap on around 14x earnings. However, again, the performance here is in stark contrast to other recruiters:

What also marks out Gattaca is the strength of the balance sheet. With net cash reported as £16.8m. This is down from £22.3m at the year end, but this is purely due to changes in working capital. This will vary during the year and even intra-month given the large pass-through revenue. However, with finance income dwarfing finance costs, I think we can conclude that the company is genuinely cash-rich:

It is also worth noting that unlike many companies’ reporting, they included IFRS16 lease debt in that figure. Excluding that, the cash balance is £18.6m, with no debt. Given that their leases don’t appear to be onerous, this figure is the one I would use in any valuation.

In comparison, Robert Walters reported £52.5m of net cash at their year end. However, this becomes £19.9m of net debt once lease liabilities are included.

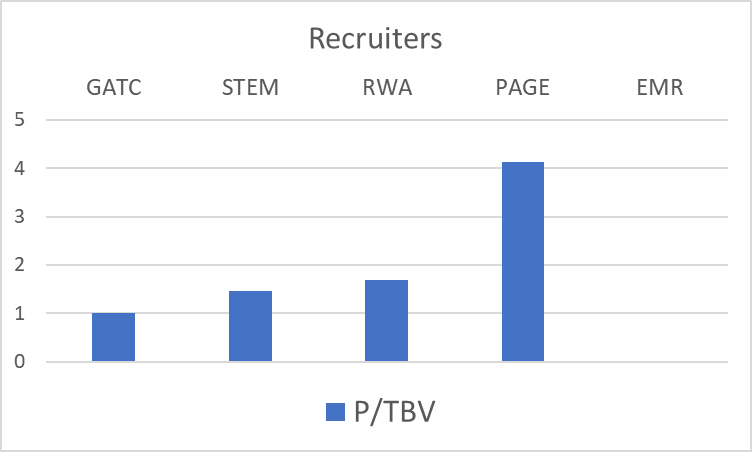

When working capital is included (there are few fixed assets for this type of business), I calculate that the company trades at around tangible book value. This is a material discount to listed peers:

Given the positive trading and cash balance they have re-instated the interim dividend at 1p. This is in line with Equity Development’s 3p forecast for the full year. However, the 3.6% yield isn’t really anything to get excited about in current markets. Given the large cash balance and forecast for profitable trading, I am disappointed that they haven’t chosen to buy back more of their shares.

It isn’t all good news on the forecast front either. Equity Development reduce their adjusted EPS for FY26 from 10.2p to 8.3p, saying:

In view of the continuation of the challenging staffing markets, with low candidate and client confidence, we have reduced growth expectations. Nevertheless, we still expect profitability to improve by a third on NFI rising 5%, emphasising the operationally geared model and a return of perm volumes at some point during FY26.

To be honest, that 10.2p always looked a little optimistic given the market backdrop, and EPS is still forecast to rise by 38%. However, some caution is warranted, as this may be the start of a negative trend of reduced forecasts. While the forward EV/EBITDA of 1 looks far too cheap, the forward P/E of now 10 is less obviously good value.

Mark’s View

I bought shares in this company when it was trading at a discount to reported net cash, and the market was fearing that they would face a similar outcome to the sector. However, their recent trading has consistently outperformed larger peers, partly thanks to a more significant proportion of contractor recruitment. Given the strengthening share price and working capital movements, they no longer trade below net cash, but they do trade at around Tangible Book Value, which means they still trade at a significant discount to other listed recruiters. The bulletproof balance sheet means that they will be around for any recovery.

In summary, they are significantly outperforming their sector while still trading on a material discount to listed peers. Their superior balance sheet strength means that they will be around to benefit from the sector recovery when it arrives. This makes them continue to be GREEN, in my opinion, and I am in no rush to sell, despite some caution over reduced FY26 forecasts.

Gear4music (HOLDINGS) (LON:G4M)

Down 3% to 130p - Trading Update - Mark - BLACK AMBER/RED

All seems to be going well here, according to the management:

Despite a challenging consumer environment over the past 12 months, we are pleased to report that the Group's financial performance in FY25 is expected to surpass FY24. Our performance reflects higher revenues, stable gross margins and a continued focus on cost control resulting in increased reported EBITDA, and a £1.0m improvement in Profit Before Tax for the year.

Until you read the small print:

Prior to this update Gear4music believes that consensus market expectations for the year ending 31 March 2025 were revenues of £154.7 million, EBITDA of £11.7 million and profit before tax of £2.8 million.

Here’s what they expect to report:

· EBITDA expected to be £10.0m (FY24: £9.4m; FY23: £7.4m)

· PBT expected to be £1.6m (FY24: £0.6m; FY23: -£0.4m)

That’s a 43% cut to PBT expectations. The EBITDA reduction is much less, of course, but a quick check of their interim results shows that they are still capitalising significant intangibles, making EBITA a completely inappropriate measure of performance for this company.

Still, the management are optimistic about the future:

…we believe these strategic initiatives coupled with competitor developments in our market, position us well to maintain our recent positive momentum and drive accelerated commercial and financial performance in FY26 and beyond.

However, it seems that their paid-for research provider, Progressive, disagrees. As well as the 43% reduction to Fy25 EPS, they have taken 44% out for FY26 EPS. This is now 8.3p, down from 14.8p. So this is a huge multi-year warning.

Much of the price strength of the last couple of years was built on the good news about reduced debt as they have managed to cut inventories, plus the expectation that they will look cheap on forward earnings multiples:

Progressive now give these as a forward P/E of 25 dropping to 16 for FY26, making this look expensive on earnings. Struggling retailers in the current market are not only tending to trade on single-digit P/E ratios but discounts to TBV, making the current 1.8x also look far too high.

So this is a complete mystery to me why this hasn’t fallen further this morning. Typically, falls for this sort of update would reflect the size of the EPS revisions and almost halve the share price. As such, the only 3% drop looks a big under-reaction that more nimble investors may be able to take advantage of.

The only good news here is that the net debt has reduced again:

Net bank debt further reduced to £6.4m at 31 March 2025 (31 March 2024: £7.3m; 31 March 2023: £14.5m)

However, again, this is a miss against Progressive’s expectations of £4.9m. Progressive’s FY26 estimates go from no debt to £3.1m net debt. Like many retailers, they pick their year-end to be the seasonal low for working capital. At the half year, they had net bank debt of £14.4m. So the average net debt during the year will likely continue to be significant. If they want to grow sales again, they may have to invest in inventory, as a lot of their competitive advantage is around the immediate availability of stock.

Their quoted net debt also excludes £8.7m of lease liabilities, which exceed their lease assets by around £1.4m, making their financial situation a little worse. This company has never paid a dividend, and with the current dynamics, I can’t see that changing any time soon.

Mark’s View

This huge profits warning hasn’t been reflected in the share price. Following this, almost all valuation metrics are looking stretched for this kind of business. The average net debt likely remains significant. The disconnect between the management narrative and the forecast revisions is particularly disconcerting. AMBER/RED

HSS Hire (LON:HSS)

Up 12% to 7p - Sale of HSS Ireland - Mark - AMBER

This is today’s announcement:

HSS Hire… announces that Grafton Group plc has agreed to acquire the entire issued share capital of HSS Hire Ireland….for a total gross consideration¹ of c.€31.6m (c.£26.2m), representing a transaction multiple of c.6.9x multiple of EBITA². The Disposal is subject to competition clearance in Ireland.

Looks like we haven’t covered this company on the DSMR, so this needs some background. I work out that the sale price here is around 1x sales, 7xEBITDA, 1.8xNet Assets. This compares favourably to the rating of the business as a whole and perhaps suggests there is hidden value here. These are the figures prior to today’s rise:

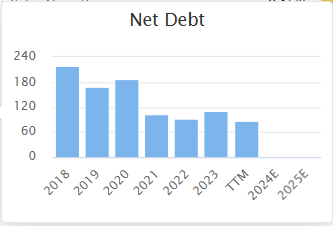

It is worth noting that the current “transformation program” feels like has been rather forced upon them. Net debt has been reducing over the last few years:

But this is largely through equity raises…

…and asset disposals. In H1 last year, they sold their Power business for £20m net. The risk is that they may well be selling off the best bits of the business. For Power, they said:

Power represented £34 million of Group revenues and £6 million of Group operating profit for the year ended 31 December 2022.

So an 18% operating margin for that business. Now, for HSS Ireland they say:

For the year ended 28 December 2024, HSS Hire Ireland had unaudited revenues of €31.9m (£27.0m) and unaudited EBITA of €4.6m (£3.9m).

So that’s a 14% EBITDA margin business. In the recent trading update, they said:

like-for-like revenues for the calendar year, excluding the Power business sold in March 2024, down 2% on prior year at £333m…The reduction in gross profit together with the net increase in costs over the prior year resulted in underlying EBITDA for the 12-month period of c.£48.5m

So, while Power may have had higher margins, HSS Ireland looks in line with the rest of their business, which has 14.5% EBITDA margins.

While trading is undoubtedly tough in their sector, they do pay a dividend, and these asset sales probably make what is forecast to be a 9% yield reasonably safe in the short term. There was a broker downgrade last year, but these forecasts appear to have been held after the recent trading update:

Thier NOMAD is Numis, so we can’t see the details, which looks a bit of a mismatch for a c£50m market cap business. They should probably engage a paid-for research provider if they want to retain Numis.

Mark’s View

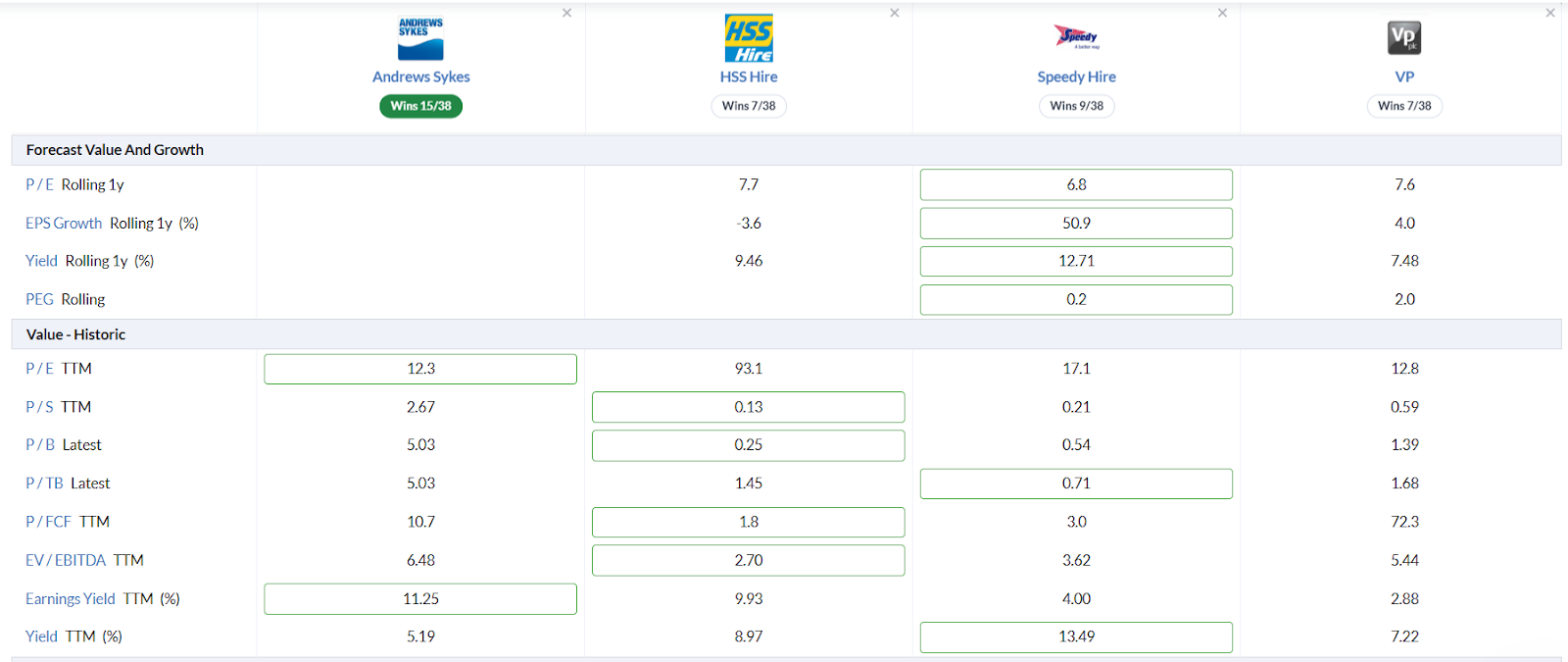

Overall, I think this sale indicates that the company is undervalued versus what an acquirer would pay for a similar business. However, it doesn’t really stand out from a cheaply rated sector:

The reason is that none of these have particularly good short-term outlooks, nor acceptable returns on capital at the moment (apart from specialist Andrew Sykes). HSS has a rather checquered past of high debt and equity raises. While that seems to be now behind them, we have yet to see any material improvements from their “transofrmation programme” apart from the asset sales. So I’m giving this an AMBER for the moment.

Topps Tiles (LON:TPT)

Down 5% to 32p - First Half Trading Update - Mark - AMBER

This company reports to the end of September, so Q2 here is the three months to the end of March:

Underlying like-for-like sales within the Topps Tiles brand were 3.7% higher year-on-year in the second quarter and like-for-like sales were 3.0% higher in the first half overall.

The same split seems to be occurring as sales to homeowners were weak, but sales to trade were strong. The accelerating sales growth may mena that the worst is now behind them. However, they flag cost pressures and a significant H2 weighting, which seems to have caused the shares to drop this morning:

The external cost environment remains challenging, including the forthcoming increases in National Living Wage and National Insurance which will collectively increase the Group's cost base by c. £4 million on an annualised basis from April 2025. As announced in the 2024 results, the timing of holiday pay accruals (exacerbated by the later Easter year on year), seasonally higher energy usage in the first half, investments in strategic growth and the timing of the sales recovery will result in the Group's profits in 2025 being weighted significantly towards the second half of the financial year.

These were expected by the brokers, with Zeus leaving forecasts unchanged. Although they say:

Today’s announcement is encouraging, albeit there remain risks to forecasts regarding H2 profitability, which is highly dependent on continued volume recovery in H2. That said, should, as our forecasts assume, the business grow profitability substantially due to operational gearing, then investors willing to be patient in what remains a challenging market should be rewarded through both increasing dividends and equity value.

Edison take a similar tack:

Our FY25 estimates are unchanged but they need the March trends to continue in order to deliver the required c 7% underlying revenue growth excluding the contribution from CTD Tiles in H225.

So it seems the brokers are setting us up for the chance of a cut in the future. So this isn’t a warning, but it sounds a lot like a pre-warning warning.

Mark’s View

I was tempted to upgrade this from Roland’s AMBER after Q1 trading given that the forecasts are held and the shares have dropped 20% since then and are on a forward P/E of 9. However, reading the significant H2-weighting and caution in the brokers’ commentary, it seems wise to keep it as is for the moment. This company is a good niche operator that benefits from the scale their specialisation gives. They will look cheap if and when the cyclical recovery in consumer spending returns. Brokers are no doubt including at least some of that in their 2026 and 2027 estimates. It is just that we could say the same about almost every UK small cap at the moment.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.