Good morning!

And a truly good morning it is, with a US-Iran ceasefire having been agreed for the next two weeks.

The ceasefire is conditional on "the complete, immediate, and safe opening of the Strait of Hormuz".

- The FTSE is currently set to open up 300 points at 10,660.

- The German DAX is up 5.4%

- The S&P 500 is up 2.7% in overnight trading.

In commodities, Brent crude has fallen $14 to $92. US Crude oil is down by a similar amount.

Some of the biggest moves are in London Gas Oil (Diesel) (down 20%), UK Natural Gas (down 17%) and Heating Oil (down 17.5%).

Iran will reportedly charge fees for safe passage through the Strait of Hormuz. It will be possible for vessels to travel through it "via coordination with Iran’s Armed Forces and with due consideration of technical limitations".

It's excellent news, but markets are likely to remain on edge until we have confirmation that this two-week ceasefire is the start of a lasting peace.

Finished for today, thanks everyone. Spreadsheet accompanying this report: link.

Companies Reporting

| Name (Mkt Cap) | RNS | Summary | Our view (Author) |

|---|---|---|---|

Shell (LON:SHEL) (£201bn | SR88) | Gas production is expected to be lower as events in the Middle East have affected Qatari production. Trading profits are expected to be “significantly higher than Q4’25”. | ||

GSK (LON:GSK) (£85bn | SR93) | Exdensur (depemokimab) approved in China for the treatment of chronic rhinosinusitis with nasal polyps (CRSwNP). Trials have shown “clinically meaningful” improvements in polyp size and nasal obstruction. | ||

| Greatland Resources (LON:GGP) (£5.2bn | SR89) | March 2026 Quarter Production Update | Quarterly production of 82.7koz Au and 4.1kt Cu (prior quarter: 86.3koz AU & 3.5kt Cu). Greatland currently expects full-year FY26 production around, or slightly above, the upper end of the production guidance range of 260,000 - 310,000oz Au. | AMBER = (Roland) [no section below] The main takeaways from today’s update are that gold production is expected to be at the upper end of guidance this year and that Greatland’s cash position rose by $260m to $1,208m during the quarter. Although the company says it will now start making regular cash tax payments, this cash pile adds credibility to the company’s plans to self-fund $1,065m of pre-production capex on the Havieron project. The mature Telfer mine appears to be performing well and management note that it has some protection from energy market disruption due to long-term supply agreements for gas and diesel. As always, the wildcard here is what could happen to gold prices in the period between now and when Havieron moves into production. Greatland could still be cheap at current levels – or it might not be at all. I’ve no idea so I am remaining neutral – as are our algorithms. |

Renishaw (LON:RSW) (£2.6bn | SR61) | John Shipsey has been appointed CFO with effect from 13 April 2026. Previous experience includes Dyson Limited and Smiths Group. Interim Chair Sir David Grant has been appointed Chair for up to two years. | ||

Close Brothers (LON:CBG) (£587m | SR47) | Close estimates cost of FCA redress scheme at c.£320m, “broadly similar” to the existing provision of £294m. This would reduce the group’s CET1 capital ratio by 0.25% to 14.0%. | GREEN = (Graham) It's a relief that no major increase to the provision is likely to be needed. Checking the half-year results, I see that there was tangible net asset value per share of £8.70, far above the current share price. So this remains a GREEN for me, on value grounds. I admit that I’m out of line with the StockRanks (the StockRank is only 47), and it’s a complex situation. However, the new CEO has been in the job for only a year and seems determined to reinvigorate performance. Given the strength of the balance sheet, there is the potential for shareholders to see some serious returns if he succeeds. | |

Young & Cos Brewery (LON:YNGA) (£470m | SR91) | Acquired Cubitt House London Pubs comprising eight pubs in West London plus one under development. | ||

Tungsten West (LON:TUN) (£455m | SR36) | Targeting restart of phase one in Q3 2026; market conditions have “further strengthened project economics”. In the final stage of due diligence relating to the remaining project debt package of up to $85m. Reached settlement with Hargreaves Services and concluded a £22m equipment financing deal with McHale Komatsu. | ||

Intuitive Investments (LON:IIG) (£413m | SR58) | Acceler8 Ventures (LON:AC8) has made a possible all-share offer for IIG of 2.6052 new AC8 shares per IIG share. Based on yesterday’s AC8 closing price of 80p, this values IIG at c.£600m, a 50% premium to yesterday’s close. IIG’s board is minded to recommend an offer at this level. | PINK | |

Hargreaves Services (LON:HSP) (£254m | SR97) | Hargreaves has now received the final £3m due from Tungsten relating to the 2019 sale of its mining lease. Tungsten has also notified the company of its intention to terminate the mining services contract and will pay £7m compensation to Hargreaves by 15 May 2027. | AMBER/GREEN = (Roland) [no section below] Under the 10-year mining services agreement with Tungsten, Hargreaves was originally expected to handle 100m of ore and crush 30mt of granite after the mine began operating. The company never put a value on this contract publicly, but COO Simon Hicks describes the £7m payment as “representing the acceleration and de-risking of several years of trading activity”. This suggests to me that the company will end up adequately compensated for the lost business. While not all that large, these numbers are not insignificant for a business that generated £23m of operating profit last year. In my view they demonstrate this company’s usual thorough and careful approach to contracts. I’m leaving our broadly positive view unchanged today. | |

Capricorn Energy (LON:CNE) (£222m | SR97) | Further to the announcement on 11 March 2026, the PUSU date has been extended to 5pm on 6 May 26 to allow Alamadiyaf al-Masiyyah additional time to progress funding arrangements. There is no certainty any firm offer will be made. | PINK | |

Aptitude Software (LON:APTD) (£119m | SR36) | Audited Results for Year Ended 31 Dec 25 & Synapse New Logo Wins & Strategic Review and Formal Sale Process | 2025 revenue down 7%, ARR -1%. Adj operating profit up 1% to £10m, EPS -17% to 7.3p. Have launched a strategic review to “assess the optimal path to accelerate the Group’s strategy”. This will consider options including a sale, raising additional equity capital and seeking a strategic partner. | |

Motorpoint (LON:MOTR) (£109m | SR36) | Retail volumes up 8% to c.65k in FY26m, a record level. Pre-tax profit expected to be +83% at c.£7.5m, with ROCE of c.70%. New store opening in Leeds in Summer 2026. | BLACK (AMBER/RED ↓) (Roland) I was ready to turn more positive on this used car supermarket group until I realised that the company’s house broker has cut FY27 EPS forecasts by 30% today due to higher interest rate expectations than previously forecast. Disappointingly, today’s RNS didn’t make this clear at all – only investors with access to broker notes are likely to realise the scale of this change in outlook. Today’s revised forecasts leave Motorpoint trading on a forward P/E of 17, which looks high enough to me. To reflect my concerns about valuation and today’s downgrade, I’ve moved my view down by one notch to be moderately negative, in line with Motorpoint’s low-ish StockRank. | |

Distribution Finance Capital Holdings (LON:DFCH) (£92m | SR67) | Loan book up c. 26%, including recently launched asset finance product. Stock days in the core inventory finance product extended “slightly” to 141 days (previously 129 days). Portfolio quality “strong and well within credit appetite”. “Whilst the macro-economic and geo-political landscape remains uncertain, the Group has not observed any immediate systemic or supply chain impact across its manufacturer, dealer and distributor customers.” | GREEN = (Graham) | |

Solid State (LON:SOLI) (£79m | SR57) | Strong trading, revenue and adjusted PBT for FY March 2026 ahead of consensus expectations. Open orderbook c. £106.5m, up from £97m four months ago, “primarily as a result of strong order intake in the Power division”. Order book to be mostly delivered over the next 18 months, subject to supply chain availability. Supply chain lead times “have started to extend significantly for certain components”. | AMBER/GREEN = (Roland) There’s evidence of improving momentum here, benefiting from defence-related demand. But the company also flags up the risk of supply chain disruption that could push back the completion of orders. It’s too soon to know whether this issue will recede following today’s ceasefire. Earnings forecasts for FY27 have been left unchanged and are now broadly flat versus FY26. On balance I’m encouraged by progress and am happy to remain broadly positive ahead of Solid State’s full-year results and FY27 outlook guidance. | |

Kooth (LON:KOO) (£39m | SR59) | SP +4% Revenue falls 5%, or 2.7% at constant currencies, after doubling in the prior year. Results are “broadly in line” with market expectations. Adj, EBITDA falls 28% to £11.3m. PBT £4.4m (prior year: £9.9m). Outlook: in line. | AMBER/GREEN = (Graham) Mark has been moderately positive on this one (see here) and I'm happy to leave that unchanged after today's "broadly" in line results and an "in line" outlook statement. They express some disappointment that revenue fell in 2025 , even if this is partly due to currency movements against them. The main US contracts are still intact but they saw lower US revenue from "contractual product development activity". UK revenue also fell by a few percentage points, and the combination of softer revenue with higher marketing expenses resulted in a sharp drop-off in profitability. I also note that management enjoyed £1.1m of share-based payments (last year: £1.2m) despite the company only generating an operating profit of £3.3m. But what really stands out to me is net cash of £21.6m, with no debt. Given that cash backing relative to the market cap, I'm happy to leave our moderately positive stance unchanged today. | |

Coiled Therapeutics (LON:COIL) (£36m | SR5) | Clinical trial update for AO-252, “a first-in-class TACC3 inhibitor”. TACC3 is a protein found in cancer. 80% Clinical Benefit Rate for twice-daily dosing, vs. 40% Clinical Benefit Rate for once-daily. 80% achieved tumour stabilisation or regression, with treatment durations exceeding six months. | ||

Solvonis Therapeutics (LON:SVNS) (£18m | SR19) | Granted a second U.S. patent by the US Patent and Trademark Office covering a further monoamine modulator compound series arising from its proprietary PTSD discovery programme. | ||

Sunda Energy (LON:SNDA) (£11m | SR22) | Agrees to buy Matahio NZ which owns and operates a group of production and exploration permits within the onshore area of the Taranaki Basin on the west coast of New Zealand's North Island. Has conditionally raised up to £6.7m to fund the acquisition. |

Graham's Section

Close Brothers (LON:CBG)

Up 17% at 456p (£688m) - Update in relation to motor finance commissions - Graham - GREEN =

In addition to the general market euphoria today, there is some positive company-specific news at Close Brothers:

As set out below, the estimated cost of the scheme as published is c.£320 million, broadly similar to the group's existing provision, and can be comfortably absorbed by existing capital resources, leaving the group well positioned to continue delivering its strategy.

I gambled on this one on October 14th, marking it “GREEN” when the company updated its provision for motor finance redress to £300m.

My reasoning was pretty simple: tangible NAV per share was £9.10, and the increased provision would only reduce that by about 90p. The share price was about 450p.

Given that the FCA had already provided quite a lot of detail on the proposed redress scheme, it seemed there was a good chance that the provision might be reasonably accurate.

The CBG share price has unsurprisingly been rather volatile since then:

Today’s announcement in a little more detail:

The redress scheme as currently proposed would result in a c. £320m provision, vs. the actual provision of £294m.

The CET1 safety cushion would reduce by 0.25% to 14%, comfortably ahead of the group's medium-term target of 12-13%.

It’s assumed there are c. 720k loans written from 2007 to 2024 under which are likely to qualify for redress.

Average redress payment per customer assumed to be c. £500 including interest.

Estimated claim rate of 75%. For every 5% change in the claim rate, this changes the provision by £18m.

So if the claim rate was somehow 100%, the provision would increase by £90m. But a 75% claim rate is what the FCA has assumed and there must be historical precedent for this.

Conclusion:

The group is well positioned and remains confident in its ability to deliver against its strategy, as outlined at the Half Year Results and business update on 17 March 2026, underpinned by a resilient business model, a strong capital position and a clear focus on execution to deliver long-term value for shareholders.

Graham’s view

I think I’ll stay positive on this. The half-year results show tangible net asset value per share of £8.70, far above the current share price.

In terms of profitability, H1 adjusted operating profit of £65m was down 19% as the business repositioned itself; it’s cutting 600 jobs and massively simplifying itself.

The statutory pre-tax loss was £65m but this included the additional motor finance provision (£135m) which I’m happy to treat as a one-off event.

Therefore, this remains a GREEN for me, on value grounds. I admit that I’m out of line with the StockRanks (the StockRank is only 47), and it’s a complex situation.

However, the new CEO has been in the job for only a year and seems determined to reinvigorate performance. Given the strength of the balance sheet, there is the potential for shareholders to see some serious returns if he succeeds.

Distribution Finance Capital Holdings (LON:DFCH)

Up 6% at 59p (£99m) - Q1 Trading Update - Graham - GREEN =

Distribution Finance Capital Holdings plc (AIM: DFCH), a specialist bank providing financial solutions that support manufacturers, dealers and distributors across the UK, provides a trading update for the first quarter ended 31 March 2026.

We had full-year results from DFCH recently, which I covered here.

In addition to providing inventory finance for dealers and manufacturers, the company now offers loans to individual buyers of caravans and motorhomes. Funding comes from retail deposits (website: dfcapital.bank).

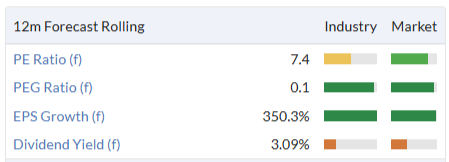

I’ve been positive on this stock due to its perceived cheapness (PE less than 7x, tangible NAV 75.9p per share).

Today’s brief update confirms that it remains on track. Highlights:

Loan book up 26% year-on-year (it was up 27% at the full-year results). Now c. £895m.

Retail deposits over £1bn (sharp increase from £841m at the full-year results).

Portfolio quality “strong and well within credit appetite”.

Some data is provided on portfolio quality and none of it seems particularly concerning (e.g. 0.6% of the loan book is now in legal recovery, vs. 0.9% at the end of 2025).

There’s a possible warning light in the form of an increase in the average age of loans outstanding in the core inventory finance product - from 129 days to 141 days. But DFCH says this is “well within sector tolerances as the Group closes the traditional dealer re-stocking period”.

Trading conditions are ok:

Whilst the macro-economic and geo-political landscape remains uncertain, the Group has not observed any immediate systemic or supply chain impact across its manufacturer, dealer and distributor customers. The Group remains vigilant and considered in its approach to managing credit risk and its lending portfolio.

CEO comment:

It is pleasing to report strong ongoing momentum in lending since the start of the year, demonstrating continued progress against our 2028 and 2030 targets. Whilst the macro-economic and geo-political environment remains uncertain, we are well positioned to navigate this, providing appropriate support - where needed - to our diversified customer base, whilst also drawing on our deep expertise and strong credit stewardship as demonstrated through the economic cycle and most relevantly since authorisation as a bank in 2020.

Graham’s view

I see no need to change my positive stance here.

The discount to tangible NAV is 22% - not huge, but enough to keep me interested. And the growth rates remain impressive.

The usual disclaimers apply: all small lenders are risky.

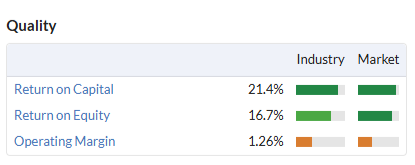

Checking the StockReport, I see favourable scores for Value and Momentum, although not yet for Quality:

If 2030 targets are hit, I trust that Quality will improve:

Loan book in excess of £1.5bn

Cost to income ratio in the range of 45%-48%

Return on required equity of c.20%

Roland's Section

Solid State (LON:SOLI)

Up 17% at 163p (£92m) - Trading Update - Roland - AMBER/GREEN =

Solid State plc (AIM: SOLI), the specialist value added component supplier and design-in manufacturer of computing, power, and communications products, announces a trading update for the year ended 31 March 2026 (FY25/26) and provides an update on its trading outlook.

This small-cap electronics business has been out of favour since a big profit warning in late 2024. But today’s year-end update is ahead of expectations, suggesting the outlook may be improving.

Reading the company’s trading commentary suggests to me that Solid State is benefiting from increased demand for some defence-related products.

Let’s take a look.

FY26 trading update - key points:

A strong end to FY26, “building on the positive momentum achieved in the first three quarters”.

FY26 revenue is expected to be “not less than £150m” (previous consensus: £145m).

FY26 adjusted pre-tax profit is expected to be “ahead of consensus market expectations” of £7.2m.

Open order book at 31 March 2026 of c.£106.5m (30 Nov 25: £97.0m, 30 March 2025: £108.5m)

The order book has grown since November, but remains below the level seen one year ago. Recent growth has been driven by c.$20m of order intake for the Power division since December. The company expects “the majority” of the open order book to be delivered over the next 18 months, but notes potential supply chain constraints:

In recent weeks lead times have started to extend significantly for certain components due to the demand arising from the adoption of AI and the impact of geopolitical instability. The Group is pro-actively engaged with customers to manage any potential impact going forward.

All three divisions have “performed strongly”:

Components: year-on-year improvement benefiting from new design wins in the UK/US.

Power: improvements following restructuring and investment in capabilities – “strong demand from the drone and other autonomous technology applications with significant new and emerging defence opportunities.”

Systems: “continuing strong demand for communications products”, combined with “building opportunities for its antenna and integrated systems capabilities”. These underpin the expected improvement in sales mix going forwards.

Outlook & Updated Estimates

With thanks to Cavendish and Zeus for sharing today’s updates on Research Tree, we have updated earnings estimates for FY26 and FY27 today.

Cavendish:

FY26E adj EPS: 10.3p (+8% vs 9.5p previously)

FY27E adj EPS: 10.5p (unchanged)

Zeus:

FY26E adj EPS: 10.2p (+6.8% vs 9.6p previously)

FY27E adj EPS: 10.3p (unchanged)

There’s no comment from the company today about the outlook for FY27, so I expect forecasts will be refreshed when Solid State publishes its full-year results, which I expect in early July.

Today’s update leaves the stock trading on a forward P/E of around 15.

Roland’s view

I’m relieved to see that I upgraded our view on Solid State to AMBER/GREEN in December following a confident-sounding set of half-year results.

Today’s commentary highlights the risk that supply chain disruption could affect trading this year. I think it’s too soon to say whether the likelihood of this has receded following today’s ceasefire. As things stand, earnings are expected to be flat in FY27, with no growth, which could limit further near-term gains.

However, Solid State has maintained stable expectations since March last year and has upgraded them today.

I think it’s reasonable to assume the company’s 2024 issues are now in the past and would speculate that we could see upgrades to FY27 guidance as the year unfolds, assuming supply chain conditions remain manageable:

I’m comfortable maintaining my AMBER/GREEN view today ahead of the company’s full-year results.

Motorpoint (LON:MOTR)

Up 4% at 136p (£114m) - Full Year Trading Update and New Store Opening - Roland - BLACK (AMBER/RED ↓)

We’ve been neutral on this leading used car supermarket chain over the last year (here & here) and this has proved to be an appropriate view – today’s share price is almost unchanged on one year ago:

The tone of today’s update is bullish and highlights an impressive recovery in profits last year.

Unfortunately, it turns out that today’s update is our least-favourite type of RNS – the hidden profit warning.

While FY26 looks likely to be in line with expectations, broker earnings forecasts for FY27 have been cut by c.30%.

Full-year trading update

Demand for Motorpoint’s competitively-priced used cars was strong last year:

“Record retail volumes”, up 8% to c.65,000 units, outperforming the market;

Motorpoint achieved 6% volume growth in calendar 2025, compared to 2.2% for the overall used car market (SMMT figures).

The company says that market dynamics are returning to normal, allowing more bulk purchases. Use of data and AI is supporting record margin performance and aiding sales from reactivated historic quotes.

New store: no new stores were opened last year, but one is planned – in Leeds – for this summer.

The financial performance reported today is expected to drive much-improved results for FY26:

Profit before taxation is expected to be c.£7.5m, up 83% (FY25: £4.1m), aided by record metal margin performance, which helped offset inflationary pressures.

This appears to be in line with expectations. With thanks to Shore Capital for providing an updated note today, I can see that Motorpoint’s house broker has left its FY26 adj EPS forecasts unchanged at 6.6p (Stockopedia consensus: 6.8p).

Profitability

CEO (and 10% shareholder) Mark Carpenter expects to report a return on capital employed of c.70% for FY26, “demonstrating the continued effectiveness of our capital light model”.

This would represent a significant improvement compared to the trailing 12-month figures:

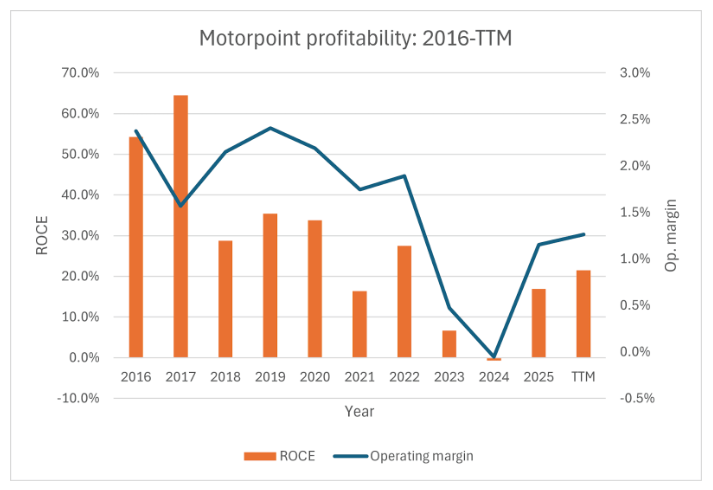

I’m not sure if the company’s methodology for calculating ROCE is the same as Stockopedia’s, but it is certainly true that Motorpoint can be fantastically profitable when conditions are good. The reason for this is that its stockholdings are largely funded using a finance facility, most of which is included under current liabilities on the balance sheet.

Apart from some long-term leases on its sites, the company doesn’t have any other structural debt or significant assets. This results in a very capital-light business; the half-year accounts show £1.3bn of annual sales supported by around £75m of capital employed.

ROCE has previously topped 50%:

The flipside to this is evident from the chart above. Margins are extremely slim and profitability can be very volatile. Used car price volatility, fluctuating volumes and rising interest costs have all put pressure on margins and ROCE in the post-pandemic period.

Unfortunately the issue of rising interest rates has resurfaced today.

Outlook: FY27 profit warning!

I had thought that the negative impact of higher interest rates on Motorpoint’s business might now have passed. But the war in the Middle East appears to have changed this, as house broker Shore Capital explains today:

Whilst current trading momentum remains unaffected, we do have to consider our expectations for the UK interest rate environment, with even the most dovish of forecasters now anticipating rate increases through the next 12 months rather than the previous 25-50bp reduction baked into forecasts.

As a result, ShoreCap has cut its FY27 and FY28 forecasts significantly today:

FY27E adj EPS: 7.8p (-28% vs 10.8p previously)

FY28E adj EPS: 12.1p (-13% vs 13.9p previously)

This is a big downgrade and appears to be wholly-related to expectations for higher interest rates. Perhaps this highlights a key risk in the business model – and the reason why Motorpoint did so well during the post-2009 period, when interest rates only ever really moved downwards.

Roland’s view

While I think Motorpoint is operating well, today’s cut to FY27 forecasts continues the negative trend seen over the last year:

Only investors with access to broker coverage are likely to realise the scale of today’s downgrade to expectations for the current year. I would argue that today’s comment on this topic from CEO Mark Carpenter was far too vague to indicate a c.30% cut to FY27 earnings expectations (my bold):

Whilst the macroeconomic uncertainty in recent weeks leads to a degree of caution due to the risks of increased inflation and interest rates, our superior customer service, omnichannel business model and exciting growth plans mean we are well placed to take advantage of opportunities to further increase market share and build long term value for shareholders.

The path of interest rate rises this year seems likely to depend on events in the Middle East.

As things stand, this cut to forecasts leaves Motorpoint trading on a FY27E P/E of 17, compared to c.13x prior to today.

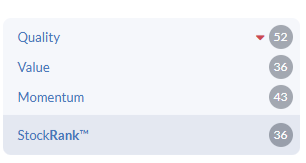

For a business of this kind – whose profits are volatile and sensitive to macroeconomic conditions – I think the share price looks up with events. Our algorithms appear to agree, with a Neutral styling and somewhat low StockRank:

I was originally going to leave my previous neutral view unchanged today, but on reflection I’ve decided to downgrade one notch to AMBER/RED. I think this better reflects the size of the cut to FY27 forecasts, my view on valuation and what I see as poor shareholder communication.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.