Good morning!

Chime Communications (LON:CHW)

Share price: 273p (down 8% today)

No. shares: 100.7m

Market Cap: £274.9m

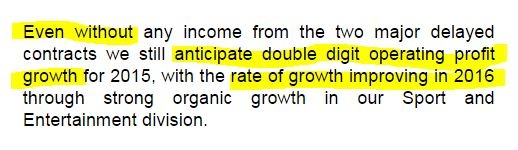

Profit warning - today's AGM update from this group of PR companies (with a specialism in sports marketing) is a mild profit warning. The key part of today's update says;

So the problems seem contained within one division - sports marketing - which made up about 41% of turnover and divisional operating profit in 2014.

Outlook - the rest of today's statement sounds quite positive, in particular this bit;

That sounds interesting, and makes me wonder if today's profit warning might be a blip, which is presenting a buying opportunity perhaps?

My opinion - personally, I'm not keen on PR businesses - they're too dependent on individuals, who can leave to set up on their own, or join competitors and take key clients with them. Also, this type of business usually has a weak Balance Sheet stuffed full of goodwill, and bank debt. So when bad times hit, there's nothing much to support the share price. Also, they are highly cyclical - PR and advertising are the first costs to be slashed when the economy turns down.

On the other hand, as I've been saying for a while, this is probably the right point in the economic cycle to be buying cyclical companies like this perhaps.

Balance Sheet - I don't like the Balance Sheet at Chime, but it's not disastrously bad. Net assets are £190.3m, but take off £243.6m goodwill & other intangibles, and the NTAV is negative at -£53.3m. That may sound bad, but in the context of a group that made an adjusted operating profit of £32.2m last year, and so could be heading for about £36m+ this year, it's bearable.

Dividends - this group has a good track record of growing divis by 10% p.a. compound since 2009, and the forecast yield for this year is about 3%, and that will be a bit higher now the shares are down 8% today, so a bit under 3.3% - not bad considering that's growing each year.

Overall - today's profit warning looks mild, and the outlook sounds promising, which combined with a valuation that now looks quite reasonable, means that I might have a closer look at this company over the weekend. As always, reader views are very welcome.

UPDATE (14:35) - I've just seen a revised EPS forecast for Chime, saying to expect 22.3p EPS for 2015 (consensus is currently 25.8p), and a revised forecast of 25.8p for 2016 (consensus currently 29.7p). That's a reduction of 13.6% and 13.1% respectively, so as I thought, not a disaster.

The share price has rebounded a little since I wrote the original report above, and now stands at 280p, so the PER is now 12.6 times for 2015, and 10.9 times for 2016. That looks a reasonable price to me, although there is some bank debt to take into account to.

Overall, it's not something I feel like rushing out to buy, but if you like the sector & the focus on sports, then it might be worth a look.

Tungsten (LON:TUNG)

Share price: 139p (down 4% today)

No. shares: 103.5m

Market Cap: £143.9m

Trading update - this company is really far too speculative to be included in these value-orientated reports, but seeing as I got caught up in the excitement last year, and have written about it extensively here, then it seems worth carrying on.

Recap - after being very positive about the blue sky opportunity in 2014, I turned neutral to mildly bearish on Tungsten shares earlier this year, and explained why in my reports here as follows;

16 Feb 2015 - at 212.5p - "I must admit to having gone a bit wobbly over it in recent weeks, as it became clear that things were taking longer, and costing more than planned".

24 Feb 2015 - at 161p - I flagged up the shorting attack on the company, and concluded that, "I'm sorry to say that my confidence in Tungsten appears to have been misplaced, at least in the short term". Also, I commented that, "I suspect Tungsten will need to raise more cash too, although that has been done with ease in the past, so may not necessarily be a problem".

I took a lot of flak at the time for changing my mind about this share, but as the facts had changed (a major reduction in broker expectations, slipped out without informing the market properly), then I changed my mind (to echo the famous phrase attributed to Keynes!).

Also it became increasingly clear that the CEO, Edi Truell, had over-hyped expectations for the whole thing, big time. This led to a valuation that was far in excess of what it should have been, peaking at 399p in Sep 2014.

It also became clear, on doing more research, that what Tungsten were doing - linking together an e-invoicing system, with financing to offer seamless early payment, i.e. invoice discounting, was not actually unique at all. Indeed, recently I stumbled by accident upon another UK listed company which is doing very much the same thing as Tungsten, although possibly on a smaller scale, and is already profitable, called Proactis Holdings (LON:PHD) (disclosure: I hold shares in Proactis).

Anyway, getting back to today's update from Tungsten, here are a few comments on each section;

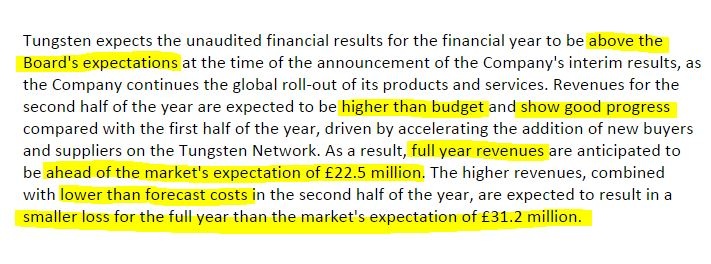

Trading for y/e 30 Apr 2014 - this sounds encouraging until you get to the very last word (or figure);

It's difficult to get excited about the company being ahead of expectations, when the expectations were for a dire performance of £22.5m turnover, and a loss of £31.2m! Although having said that, everyone understands that Tungsten is in the rapid growth, cash burning stage of its development.

Tungsten Network - there's lots of detail about this growing. That's all fine, but the invoice processing is basically a loss-leader for what we hope will be the profitable activity of invoice discounting, so this section can safely be ignored I think.

Tungsten Bank & early payment - Tungsten seems to have made a mistake in buying its own bank, since funding for the invoice discounting was arranged elsewhere through Insight Investments. So Tungsten Bank stopped taking deposits last week, as basically it doesn't need them - the existing arrangement with Insight is providing adequate financing for now.

It's still early days, as the invoice financing only started recently, but a total of £32m invoices having been financed so far is chicken feed. They're only financed for say 30-60 days remember, so that's next to nothing in income for TUNG.

The penetration rate is a key number, and that is reported at 6.6% for SMEs targeted. That's lower than the 10% rate suggested some time ago. Although it does at least show there is some demand for the service, and this number could perhaps be improved on over time. So 10% doesn't look out of the range of possibilities at all.

The "average yield" on invoices financed is disclosed as 4.5% for large corporates, and 12.4% for SMEs. Trouble is, it's not disclosed what proportion of that Tungsten receive after paying Insight.

A very encouraging statistic however is that "customers using Tungsten Early Payment finance repeatedly use the service, financing an average of 79% of the value of their available invoices".

Other comments relate to teething problems about the length of time, and perhaps laborious set-up process.

Tungsten Analytics - the company continues to make positive noises about this service, to analyse invoices and find cost savings, but there's not really anything to measure progress yet. There are 40 customers trialing it at the moment.

International expansion - the company talks about breaking into the Indian market, and Japan, and setting up local offices. More cash burn, in other words!

Funding - as I correctly anticipated, Tungsten needs more cash, which they admit today, and is likely to be the main reason the shares have fallen recently;

I recently learned an expensive & painful lesson with Synety (LON:SNTY) where I assumed that a small fundraising would be easy, but actually it turned out to be a nightmare, with the share price halving. So my view now is to keep well away from any loss-making company which is going to need more cash.

Having said that, Edi Truell might be able to pull it off, if he can rekindle excitement in the company with deep pocketed investors. Although I reckon he'll find it a lot harder, as the sheen has very much come off this share, as the original targets were missed by a mile, and it seems likely to be heavily cash burning for several more years.

Board changes - there have been some board changes, with Edi Truell stepping down as CEO, and becoming Vice Chairman - it sounds to me like he's going to be out & about, schmoozing clients & financiers, in order to get some more dosh raised! That's what he's good at, so it makes sense.

Outlook - bascially says they're going to continue expanding, and and even look at acquisition opportunities.

My opinion - it's very interesting what they are trying to do, but I can't help feeling that they are using a sledgehammer to crack a nut. I think Tungsten is going to need a LOT of fresh cash - I'm thinking something like £100m, to continue with the current, very expensive business model of heavy cash burn up-front, in the hope that customers' suppliers will then use the invoice discounting.

There are some encouraging, but very early stage signs that the invoice discounting might work well.

However, the key issue for now is cash. The company needs to do a substantial capital raise, and I'd rather sit on the sidelines and wait for that to happen. There's a risk the share price could spiral down, and investors may demand a deep discount for putting in fresh cash, now the story is somewhat tainted from having failed to achieved what was originally promised.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.