Good morning.

I'm taken aback by just how far & fast MySale (LON:MYSL) has fallen from grace. As reported in yesterday's report here, the company issued a nasty profit warning, due to flat sales in its core market. Just look at the chart below - it's crashed from about 175p to only 73.5p in a little over 24 hours.

With 150.6m shares in issue, I make that a market cap of £110.7m - still hardly a bargain, although it did report cash of £33.5m yesterday. Am not sure what level I'd start to take an interest - possibly sub-40p? I'm convinced there will be plenty more large falls from over-priced early stage growth companies - it very rarely pays to chase fancy valuations in trendy sectors, especially when a lot of the hype rests on having a big name backer - that's no guarantee of commercial success.

Optimal Payments (LON:OPAY)

Share price: 324p

No. shares: 162.6m

Market Cap: £526.8m

This stock is a bit larger than the usual stuff I look at, but I must mention it as extreme volatility has once again hit the company - which could be either a worry, or a buying opportunity, depending how you look at it.

I've marked on the 6-month chart below two events which triggered a substantial fall in share price. The first one was when news broke of the CEO having used the now discredited EFH facility to sell/buy back part of his personal holding, which was dressed up to look as if it was a purchase of shares, to uproar from investors (rightly so!). There were about 5 companies where Directors did the same thing, and their share prices were whacked to varying extents.

A number of people, including myself, saw this as a buying opportunity, and it was a successful trade, as the shares almost immediately recovered by about 20% over about a week, in late Nov 2014. The company issued a positive trading update at the time, which helped propel the shares back up again.

Well, a similar thing has happened again! It was announced on Friday that the CFO is leaving. That can rattle investors, especially (as in this case) where there has been some other cloud over the company. People start worrying whether there is something amiss behind the scenes which led to the CFO resigning?

Although in this case what is interesting is that a new CFO has been appointed, and the old one is staying on as a consultant until 31 Mar 2015. That suggests to me that the change was planned, rather than spontaneous, and that there probably isn't anything awry, given that the old CFO is staying on.

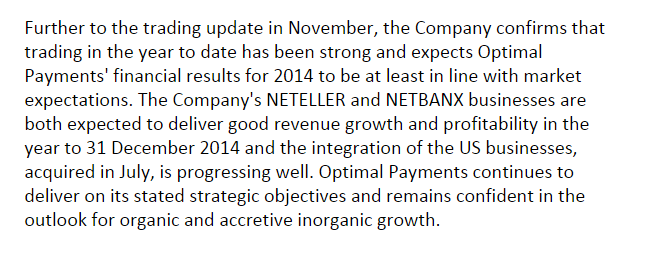

Trading update - furthermore, the company has again obliged with a positive trading update today, as follows;

As other companies have discovered this year, when you put out a positive trading update after every wobble in share price, it does become subject to the law of diminishing returns!

However it's difficult to argue with this one, and hence I am once again leaning towards treating this as a buying opportunity. A change in the CFO surely does not justify a drop in share price from 400p to 320p?! Barring any unforeseen bad news, I suspect these shares might well recover again. We shall see.

Redde (LON:REDD)

Share price: 79.3p

No. shares: 385.3m

Market Cap: £305.5m

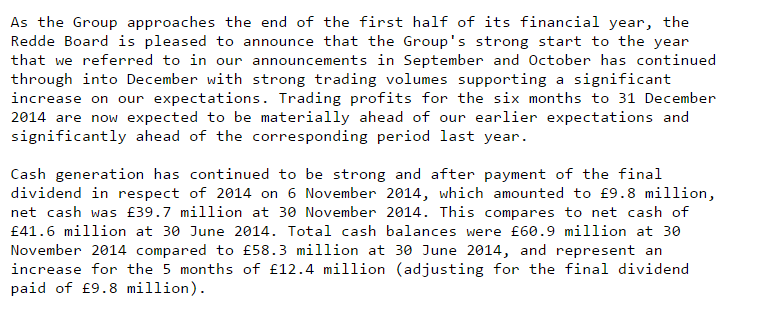

Trading update - very strong, see the "materially ahead" of both expectations and prior year;

This ambulance chaser seems to have made it work, and is strongly cash generative, and paying good divis - the forward divi yield is over 7%. The Balance Sheet is strong too.

Perhaps they are picking up new business as a result of the high profile meltdown of a major competitor? Anyway, the figures all seem to stack up here very nicely, if you can cope with investing in this sector.

Avesco (LON:AVS)

Share price: 111p

No. shares: 18.9m

Market Cap: £21.0m

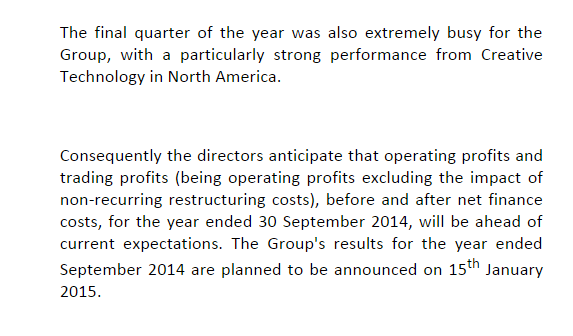

Trading update - announced today reads very well, with the key excerpt reproduced below;

Valuation - So "ahead of current expectations" is the crux. Stockopedia shows broker consensus as being EPS of 18.3p for the year ended 30 Sep 2014, putting the shares on an extremely cheap PER of just 6.1. Before we get too excited, I should point out that the company has alternate year profit surges, due to particular events which happen every two years (the company provides staging & other equipment for outdoor events).

Dividends - note the excellent progression in divis in recent years. 6p is forecast for this year, which would put the shares on an attractive (and growing) divi yield of 5.4%.

My opinion - I hold a few of these in my long term portfolio, and like the shares for the divi yield, and the turnaround potential, which seems to be going well. Results are due out on 15 Jan 2015, so I'll report back then with more detail. The bid/offer spread here is nasty, and the shares are very illiquid unfortunately, but it looks a good company in my opinion.

888 Holdings (LON:888)

Share price: 138p

No. shares: 354.4m

Market Cap: £489.1m

Trading update - the company today says it is trading in line with expectations, for full year adjusted EBITDA. I wonder how that translates into profit?

I'm giving online gambling companies a wide berth at the moment, until the regulatory/taxation position becomes clearer for UK operations. As demonstrated in the past, there is always scope for big regulatory upsets, so this sector can be a bit of a minefield.

I note there is a 3.8% (i.e. fairly good) divi yield here.

GVC Holdings (LON:GVC)

There's a positive trading update too from this online gambling company.

They expect to at least match full year expectations for 2014.

Note that there is a remarkable 8%+ yield, and the PER looks good value too.

Although the company does note the imminent "point of consumption" tax change in the UK, and the fact that 2015 lacks a major sporting event such as the World Cup, thus reducing likely bets by customers I suppose.

Interesting to note that the shares still look cheap, even after a very good run in the last two years;

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.