Good morning!

Firstly a couple of investor events to mention. People sometimes complain that everything seems to be in London, so just for a change here is an event in Manchester, on Wed 25 Feb, starting at 12:30 lunchtime. The event is a private investor lunch with VP (LON:VP.) which is free to attend, but you have to book in using this link. The company is a group of niche equipment hire businesses, is consistently profitable & dividend paying. It's on my watch list, and is starting to look reasonably priced again. Hence my being happy to mention this event here.

A tech event hosted by Bloomberg in London, is on 12 Mar, organised by David Stredder, with some excellent keynote speakers, including Mark Slater, who's always well worth listening to in my opinion, so I shall be attending this event. The booking link is here. This one has a small charge, which is even smaller using a special discount code that we secured for our readers - that code is DISCSTOCK (now corrected. Sorry it was incorrect earlier).

Shaft Sinkers Holdings (LON:SHFT)

Suspension - We wave a tearful goodbye today to this African excavator, as the shares are suspended with any remaining shareholders suffering a 100% loss, as expected. The company says;

This is likely to be one of many small resources stocks that de-list. Not before time, as there have been dozens of no-hopers clogging up the market for the last few years. So a good clear-out will make it a lot easier to focus on the good companies. Sorry if that sounds uncharitable, but there we go, capitalism is all about the survival of the fittest.

Mecom (LON:MEC)

De-listing - This European newspaper group also de-lists today, with the shares no longer trading from 8am today. Shareholders will receive 155p per share in cash, in an agreed takeover which has dragged on quite a while since being announced on 30 Jun 2014.

This looks a good outcome for shareholders, given that the company's shares were as low as 30p in 2013, and I recall trading being poor in Holland some time ago.

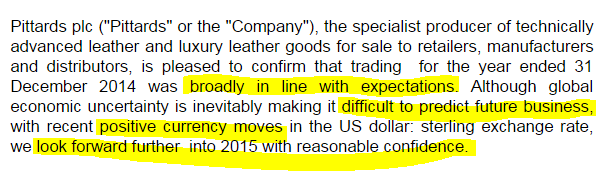

Pittards (LON:PTD)

Share price: 135p

No. shares: 9.3m

Market Cap: £12.6m

Trading update - I've (badly!) highlighted the key bits in today's update below. Sounds alright to me overall, especially given that the shares are on a modest forward PER of 9.2.

It has a StockRank of 75, so reasonable. There are no divis, and the balance sheet has a bit more debt than is ideal, although that is to finance stock.

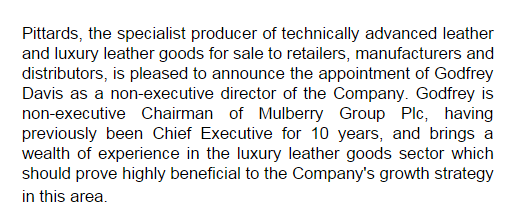

My opinion - the wild card with this share, which is a speciality leather goods manufacturer, selling globally, is if they can crack the luxury handbags market. Mulberry (LON:MUL) did that between 2010-2012, and their shares roughly 30-bagged. I mention this because the Chairman of Mulberry was appointed a Non Exec at Pittards in Feb 2014, when at the time Pittards said this;

So if Mr Davis points Pittards in the right direction, who knows what might happen?

Note that Pittards was recently included in Investors Chronicle's "2015 bargain portfolio", so that has caused a recent flurry if buyers in the stock. Although in my experience people who buy on magazine tips have the attention span of a goldfish, so half of them have probably already sold! However, the recent move from 110p to 140p on the back of the magazine tip would have given any stale bulls a nice opportunity to exit at a more favourable price, if they wished.

Sinclair IS Pharma (LON:SPH)

Share price: 33.6p

No. shares: 497.4m

Market Cap: £167.1m

Interim results - these are quite tricky accounts to interpret, and pharmaceuticals is not a sector I'm comfortable analysing, so will keep this brief.

The headline figures look good (e.g. EBITDA up 200% to £3.3m, for the six month period), but heavy finance charges (some related to deferred consideration for acquisitions), and amortisation charges, took it to a £10.8m loss for H1.

Balance sheet - this looks too highly geared, in my opinion. Net debt is reported at £44.2m, and the £2.7m interest paid (shown on the cashflow statement) uses up most of the £3.3m EBITDA generated.

However, there is a further £85.8m in deferred or contingent payments relating to acquisitions, and from what I can see, the company doesn't have the money to pay those creditors. So where is that money going to come from? There are only 3 options - profits (which would need to massively increase in order to generate the necessary surplus cash), more debt (is that wise?), or an equity fundraising (dilution).

My opinion - this is only a quick review, so I've not gone into any depth about what products they have, etc. However these numbers have scared me off. The company already has a lot of debt, but the deferred consideration liabilities are even bigger. So if something didn't go to plan, this is a balance sheet that looks like it could implode quite readily. Hence the shares are not for me.

Hargreaves Services (LON:HSP)

Share price: 501p (down 12% today)

No. shares: 32.1m

Market Cap: £160.8m

Interim results for the six months to 30 Nov 2014. This group is primarily a coal distributor, and surface coal producer. The distribution business has been decently profitable in the past, but the huge problem the company now has, is that coal is being phased out as a form of electricity generation. Therefore it's effectively a last puff on the cigar butt type of stock.

Turnover in H1 is down 23.7% to £351.2m, and underlying operating profit fell 29.1% to £21.9m. So it's a decent sized (and still profitable) business, but we don't really know how many more years of profitable trading there will be, Maybe not very many at all, as EU policy has led the British Govt to schedule the closure of a number of coal-fired power stations, and these are major customers of HSP.

Net debt has fallen dramatically, by 57.6% to £40.4m, and there is some hidden property value in the company too.

My opinion - without access to detailed forecasts of how demand & costs are likely to pan out in future, it's impossible to value this share. Note that the company is disposing of non-core assets, and paying out surplus cashflow in divis. The interim divi rose 13.6% to 10.0p. So this share is likely to come up on high yield screens for a while, but the trouble is the profits to pay divis are rapidly declining, on a structural decline in the use of coal in the UK. Therefore it's difficult to see this share as being anything other than a value trap. Sustainability of earnings is everything when valuing shares, and there isn't any long-term sustainability of earnings at all here.

Unless UK Govt policy changes, to embrace coal again, which seems unlikely, then these shares seem doomed to further long term decline.

All done for today.

Regards, Paul.

(of the companies mentioned today, Paul has a long position in PTD, and no short positions. A fund management company with which Paul is associated may also hold positions in companies mentioned)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.