Good morning. Well actually, it's not, it's been a horrible morning, as unfortunately I got caught on this one:

Plus500 (LON:PLUS)

Temporary suspension - the crazy thing is, I've never liked PLUS, and have always written negative things about it, saying how the figures looked too good to be true, or too good to be sustainable. However, in a rush of blood to the head, I decided to have a punt on it in my personal trading account a few days ago, and averaged down a few times, so that my average buy price is about 446p. This is now looking like a mistake. The shares have been temporarily suspended this morning at about 293p.

No details about the suspension are given, in terms of why, or the duration, with a statement today simply saying this;

It should be emphasised again, that my sensible, longer term stuff is what I write about in this blog, but to keep myself amused, I also do a bit of shorter term trading, of interesting & liquid shares that are moving a lot, e.g. Quindell was a share I was very active in last year, and made a terrific profit on it, being mainly short, but also sometimes long (for the rebounds).

Things have not worked out so well on PLUS. Chatting to my broker, he said that opinion on this stock is totally polarised (as it was with Quindell too). It might be worthwhile to recap on the bull and bear points;

Bear points

- Israeli company, listed on AIM

- Question marks over how the company has achieved such high profits & growth

- Sustainability of its business model under question

- Some negative reviews online from customers

- High profile short sellers (e.g. Gotham City) have attacked the company

- Recent freezing of some client accounts, due to inadequate paperwork, under regulatory pressure

- Repuational damage from freezing client accounts

Bull points

- Pays generous divis, including a large one paid a few days ago

- If the accounts are real, and sustainable, then the stock is now arguably cheap

- Former head of the FSA is a Non Exec

- The company claims to use clever online marketing to attract losing clients, who are highly profitable for them

- The company has had previous issues, which blew over fairly quickly

My opinion - it sounds like there could be more bad news to come out, but we don't really know at the moment. I've not seen anything concrete from the bears to support their allegations that the company is some sort of elaborate scam. The big divis paid suggest otherwise.

Maybe the Stock Exchange felt the shares had to be suspended, as the market was clearly becoming disorderly this morning? I've put a call in to the Nomad, so hopefully might get some more idea about what's happening, and if/when the shares are likely to resume trading.

Am obviously kicking myself for breaking my own rule of not investing in overseas companies listed on AIM. Or rather punting, not investing. So one to add to my "mistakes" book I think, although we don't know what the outcome will be yet. I fear things might get worse, before they get better though.

Breaking News!

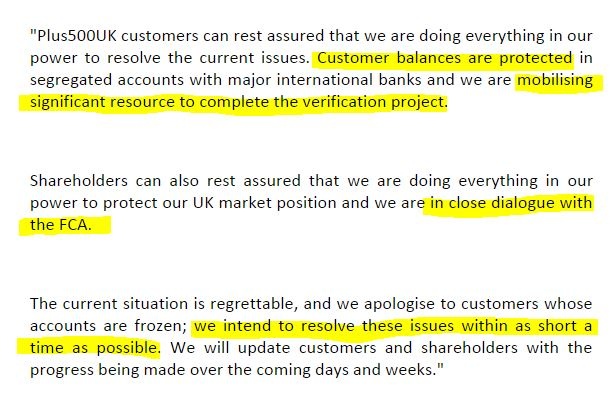

Clarification statement - PLUS has just issued a statement, which reads quite positively in my opinion, in terms of how it might affect market sentiment. It gives more detail about the regulatory problems it has run into in the UK, and what it is doing to sort them out.

The shares have gone into auction, so will be coming back from suspension any minute.

Here's a summary;

- On 9 Jan 2015 the FCA required PLUS to appoint a "Skilled Person" to review its regulatory procedures & controls.

- On 15 May 2015 the FCA required PLUS to prohibit transactions on customer accounts without correct documentation & cease opening new accounts.

- PLUS has put 40 staff onto rectifying the documentation issue.

- Client accounts are being unfrozen when they provide documents needed.

- New client accounts should be possible again "in the next few days".

- As an interim measure, new accounts are being diverted to its Cypriot & Australian subsidiaries.

- Further update at AGM on Wed 27 May (next week!)

- Confirms $65m special divi was paid in full on 15 May 2015.

- Confirms has >$88m in own cash, over & above client funds.

My (latest!) opinion - phew, this is nowhere near as bad as I feared.

It sounds as if the company is on the case, and getting things sorted out with respect to incorrect client documentation. My main worry is whether the regulatory problems get worse, and the FCA kicks it out of the UK market altogether. Although I can't see why they would do that, given that the fundamental issue is incorrect client documentation, which they are now sorting out.

Personally I am not convinced by the bear case (that the company is an elaborate fraud), so we could now see a recovery as shorts rush to cover their positions? I am minded to tough this one out, so I remain long in my trading account, but it's been a heart-stopping morning. Memo to self - stop doing these high risk trades, it's not good for your blood pressure!!

Tungsten (LON:TUNG)

Placing - I was slating Tungsten yesterday, but concluded that Edi Truell would probably pull something out of the hat, and he has done - a £17.5m (gross) Placing at 80p per share, which compared favourably with last night's close of c.70p, but compared very unfavourably with the much higher share price a few weeks ago.

The gross proceeds seem to be £17.5m, but yesterday's statement indicated a £15m net proceeds (after underwriting fees), so I will just clarify that point and update this article in a few minutes.

My opinion - raising fresh cash is clearly positive for the company, and 4 Board members have taken up stock in the Placing, although 3 are de minimis. Edi Truell has taken up 3,762,500 shares at 80p - so another big vote of confidence from him personally, so there's no denying his commitment to this company. Whether that actually has any predictive value, is very much questionable, based on previous similar big gestures.

My main concern is that the money raised doesn't look anywhere near enough, given the company's heavy cash burn. Although it sounds as if Tungsten Bank might be sold, which would raise more cash. Further talk from the company about creating a JV structure with a financier, is all very well, but that means giving away half of the upside potentially.

So whilst risk has reduced from raising fresh cash, it sounds like reward might end up reducing too. The sheen has very much gone from this wonder stock, and its management. I echo the remarks from Ben, in the comments section below, that experience with Tungsten is yet another example of how investing in story stocks is fraught with risk, and so many of them go wrong. Why on earth do we let ourselves get sucked into these story stocks, given the appalling end results in almost every case?! (this is very much a "memo to self" comment!).

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.