Good morning! The American markets hit all-time highs last night, and with the S&P500 now up almost 27% since late Dec 2012, this is all starting to feel a bit crazy. Therefore I'm preparing myself for a sharp correction, which must be due at some point, and the stocks that will be hit hardest will be the over-priced growth/story stocks where price has detached from value.

We've seen with Globo (LON:GBO) how flaky these things are - yes it was subjected to a bear raid from Evil Knievil & others, but it seems that few investors had much conviction in the valuation, as they stampeded for the exit once it began falling, thus doing the job of the shorters for them. Whereas with the relatively safe, solid Value/GARP shares that I focus on, when they fall sharply, investors like me just buy more, as we know our research is correct, and that falls are buying opportunities. So the Bulletin Board maniacs hurling abuse at shorters should be questioning their own skill and actions, as well as the scare tactics of the shorters.

Also, as a long term investor, I am perfectly comfortable with the fact that every now and again my portfolio will take a (say) 10% hit on a market correction. It's not a problem, as my long term portfolio is not geared, indeed has surplus cash on the sidelines, waiting to buy the dips. Small caps can provide fabulous buying opportunities in a market correction - it only takes one clumsy seller, and you can see a small cap down 20-30% for no fundamental reason. If it's a good solid company, at an attractive price, then that's an opportunity, not something to worry about.

I also run a more racy, geared personal portfolio with generally shorter timeframes, and I'm increasingly worried about that, so have bought some insurance with S&P500 Put Options, and am easing back on a few position sizes, to ensure the gearing is not too high. What is too high? Personally I've found that 1.5 to 2 times equity is normally OK (other than in a proper bear market, where no gearing is the only safe option), if it's spread over plenty of different stocks, and they are all safe, solid companies, usually dividend paying & with net cash. Given how frothy the market is now though, I'll be de-gearing to the lower end of that range in the coming days & weeks.

Everyone I talk to is worried about the market being too frothy (most of my network are High Net Worth, savvy investors who've been doing this for a while), but most also see the opportunity - that we're in the most buoyant stage of a bull market, nobody knows when it will end, but there is fabulous money to be made, providing you get out before it all goes wrong & don't believe the hype.

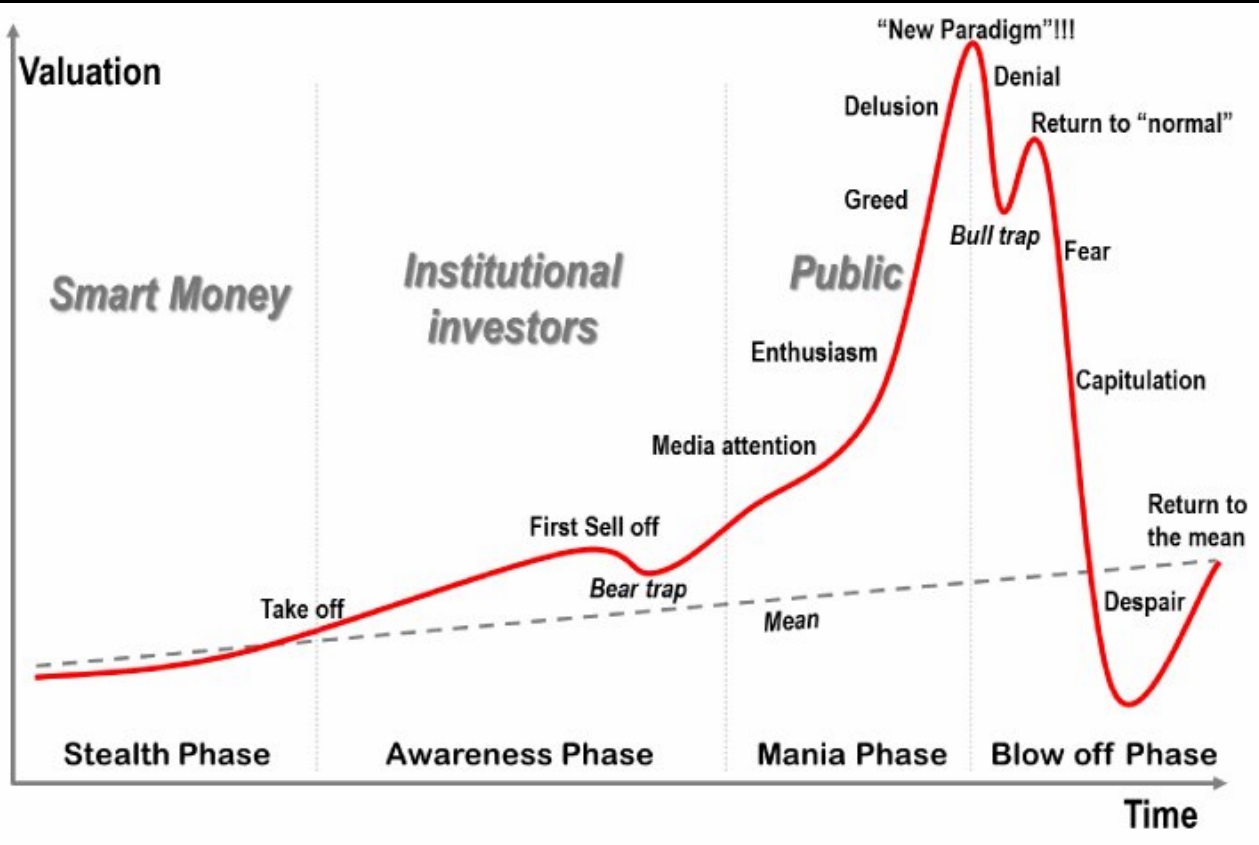

Thank you to the member here who posted this fantastic chart of market sentiment:

I've seen it before, but good to have a reminder, and I've set this picture as my desktop background, to remind myself every day of the time-honoured market cycle. The key question being, where are we now? I think we are already in the "Mania Phase", but possibly somewhere between the "Media attention" to "Enthusiasm" stage. Nobody in real life has given me any share tips (a classic sign of a market top). My personal litmus test is that when kebab shop owners want to swap share tips with me, that's when we're at the top of the market.

Thinking back to 1998-2000, the bull market went on far longer than anyone thought it would, to a point where anyone who wasn't putting money into crazily over-priced tech stocks was considered a fool. This wasn't just private investors, it was Institutions too remember, the whole market collectively took leave of its senses for a couple of years, I remember it well.

So overall my market view is that we are now in the later stages of a bull market, which could go on for a year or two longer, and get considerably more frothy as new retail investors join in the fun. Story stocks will do best (in the short term), so I'm beginning to position myself partially into some more racy growth companies, but only if the valuation is still reasonable, and the potential is real - so zero turnover companies don't interest me, neither do heavily loss-making story stocks. However, companies where growth is taking off, losses are small (or it's moved into profit), and the potential market is large, are where the best potential gains are in this type of market.

In terms of price, I'm prepared to pay a bit more than usual, but not go crazy. So the sub-£30m market cap level is where I'm looking hardest for good growth stories. That's where the multi-baggers of next year are probably sitting currently, as they are off the radar. Once these shares are picked up by the press, tipsheets, etc, and naive novice investors (who come into the market in droves at this stage of a bull market - that was where I began in 1998!) begin hoovering up the shares, the gains can be spectacular. Then top-slicing into strength both locks in the gains, and recycles the money for the next one. Repeat until the bubble bursts, then get the hell out of them all, and into cash, ASAP. The challenge will be seeing if I can pull it off this time & not get caught up in all the hype that fooled me in 1998-2000 as a naive novice investor!

Thalassa Hldg (LON:THAL) has announced a relatively large Placing. Its market cap is about £45m, yet they have today announced a Placing of £18.1m, which is to issue 7.24m new shares (there are about 16.36m currently in issue). I think that's wrong. Existing shareholders should not be diluted to that extent - this is a 44% increase in the number of shares, so they should have done it properly through a Placing & Open Offer, so that existing holders could also take part.

Having said that, the 250p Placing price is not far below the 266p market price, but it's still annoying for smaller shareholders that they have to pay up 266p in the market to buy more shares, when Institutions are getting in at a 6% discount.

The growth potential must be pretty convincing though, for WH Ireland to have successfully done such a relatively large Placing at a modest discount. I wonder why Thalassa needed to raise so much cash? The statement today doesn't say what it's going to be used for. They do seismic data, so perhaps it's for a new ship? Would have been helpful to give more detail in the announcement I think.

Albemarle & Bond Holdings (LON:ABM) has successfully gained more time from their Bank, as reported in a financing & trading update this morning. On reflection, I think this situation has overall been a colossal cock-up. It's the job of management to anticipate the level of funding any business requires, and put the necessary equity and debt facilities in place in advance, with the necessary headroom to be flexible. So this company running headlong into a funding crisis that should have been prevented, just strikes me as poor management. On the other hand, how many good managers would actually want to work for a pawnbroker? I wouldn't, would you?

The shares have bounced 18% this morning to 50p on news that the Bank are extending the date for deferring testing of covenants to 3 Feb 2014. One imagines that should give ABM enough time to raise some equity, and agree a reduced bank facility. So I think it's unlikely they will go bust - mainly because their Balance Sheet has enough reasonably liquid assets (stock and the pledge book) to cover the Bank debt.

I had a quick trade on the initial bounce from 24p a little while ago, which worked very well, but this is not a share I'd want to hold for more than a couple of days, so am happy to be out now.

Just look at the destruction of shareholder value in the last six months:

Going back to my point about small caps out-performing, just take a look at the FTSE100 over the last 2 years, with the FTSE SMALL CAP INDEX XIT (FTSE:SMXX) plotted against it. As you can see below, if the FTSE100 had kept pace with small caps, then it would be about 9,400 now! So make no mistake, this has been a spectacular bull market for small caps in the last two years, and it's very difficult to see how the market overall can go much higher - it will now all be about stockpicking, rather than a rising tide lifting all boats, in my opinion.

Audited results for Utilitywise (LON:UTW) have been issued today, for the year ended 31 Jul 2013. This is rather unusual, in that the company issued preliminary results on 15 Oct 2013, which I reported on here. Some changes have been made, relating to revenue recognition, which has resulted in diluted EPS rising from 7.9p to 8.5p.

The shares have been on a remarkable streak upwards, and are now 214p. Sorry, but I just thnk that is too high, at a PER of 25 times. Sure there is more growth in the pipeline, but this is really not a very robust business model at all. It's entirely dependent on commissions from the utility companies, and that landscape could change at the drop of a hat, if the utlility companies decide to cut back on commissions paid for new business.

So I would say that the market is ignoring the potential risks here, and getting carried away with the growth, so it's not for me - risk/reward is not attractive at the current share price in my opinion.

Although I did spot the potential at 102.7p per shares, when I added it to Paul's Value Picks (my online notes of potentially interesting Value/GARP shares to research further) back in February 2013, so a nice 114% gain chalked up there.

Non-fiction publisher, Quarto Inc (LON:QRT) issues its Q3 IMS (Interim Management Statement). Operating profit is flat against last year at $9.5m for the nine months to 30 Sep 2013. However, almost a third of that is consumed with interest cost. A glance at the last Balance Sheet shows that this group has far too much debt, so it's not for me.

They present EBITDA of $24m for the nine months, which sparked my interest, but that looks a pretty meaningless figure, since it ignores the huge amortisation charge of pre-production costs. As usual, EBITDA just leads people up the garden path, so one needs to be very careful about putting any reliance on it.

If I was going to invest in a publisher, it wouldn't be Quarto, it would be Bloomsbury Publishing (LON:BMY), with their bulletproof Balance Sheet, and it's not expensive either, despite big recent rises.

Right I'm done! See you tomorrow morning as usual!

Regards, Paul.

(of the companies mentioned today, Paul has no long or short positions)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.