Good morning!

Writer's block has hit me this morning - it does sometimes, you just can't think of anything to write, or get your head round the numbers. So today's report may not be very good, I'm afraid.

HSS Hire (LON:HSS)

Share price: 82.25p (down 5.2% today)

No. shares: 154.8m

Market cap: £127.3m

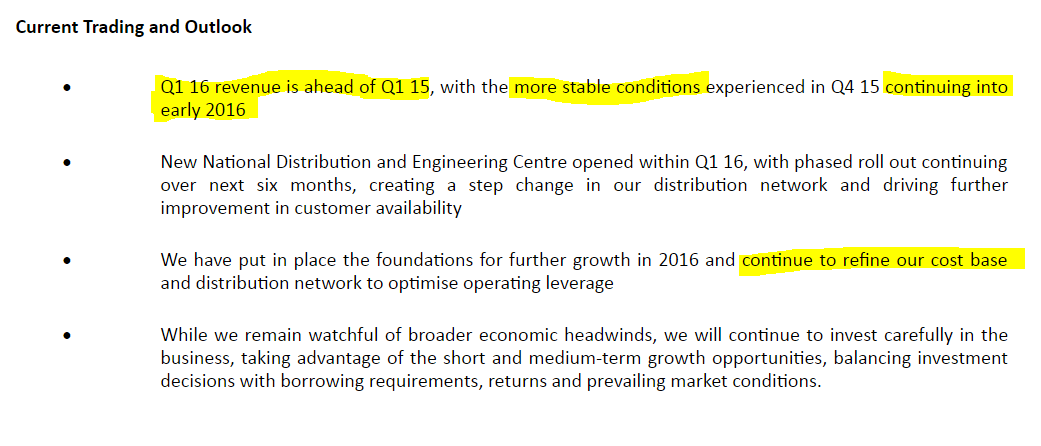

Results, 52 wks ending 26 Dec 2015 - the company says that it has performed in line with revised expectations. Although of course expectations have been dramatically lowered - from 11.5p EPS forecast for 2015 in Apr 2015, down to only 2.48p forecast EPS now.

Today the company reports 3.2p adj. EPS, so it looks as if they're a bit ahead, or possibly that the forecast data is prepared on a different basis, or hasn't been updated recently, which sometimes happens with smaller caps. Anyway, EPS has come in roughly where it was expected to, after the 2 profit warnings last year.

Outlook - sounds reasonably upbeat:

Directorspeak from the CEO says:

"We expect to see the full year benefit of the cost reduction programme implemented in H2 2015 delivered through 2016. We also expect to reduce our capital expenditure, following two strong years of fleet investment and the opening of our new National Distribution and Engineering Centre in H1 2016. Together with the cost reduction programme, we expect these actions to improve our cash generation and financial performance."

Dividends - this company has a very weak balance sheet, so it only pays modest divis. The final divi of 0.57p adds to an interim divi, to give 1.14p total dividend for the year - a yield of only 1.4% - very poor for this sector.

Balance sheet & net debt - you expect hire companies to have some debt, to finance part of their hire fleet. However, in this case, the company has no equity at all - it's actually negative NTAV of -£21.7m. So in effect, the entire hire fleet is funded with debt. That's a very imprudent capital structure, and makes this share uninvestable for me.

Net debt is an eye-watering £218.1m. That compares with £183.2m total property, plant & equipment. So it's effectively a LTV on the hire fleet of 119%. I would normally look for a LTV of about 50%. The difference works out at excess debt of £126.5m - which coincidentally is almost exactly the same figure as the market cap.

Therefore, to sort out this balance sheet, and make it safe, would need a 1 for 1 Rights Issue at no discount. Doubling the number of shares in that way would therefore take the forward PER from 13.1 to 26.2.

My opinion - I just think this share is the wrong price - it's too expensive, given the extremely weak balance sheet & excessive net debt. The whole business is financed on debt.

The market has ignored this issue in recent months, but that doesn't mean the problems have gone away.

In my view investors are over-paying for a lot of highly indebted companies, this isn't the only one by a long shot. The danger is, that we get so used to these bizarre conditions of ultra-low interest rates, that we start to think it's normal.

The next recession & banking crisis, is likely to plunge over-geared companies like HSS into deep trouble, which tends to kill the share price, and trigger emergency equity fundraisings at deep discounts, or even lead to insolvency. As an investor, why take that risk?

In my view, Speedy Hire (LON:SDY) and Lavendon (LON:LVD) have much more appropriate balance sheets (I hold long positions in both), although Speedy Hire seems to be beset with problems, much like HSS.

£BLTG

(this ticker may not work yet, it's the old Regenersis (LON:RGS) now renamed)

Share price: 229p (up 0.9% today)

No. shares: 79.0m

Market cap: £180.9m

Tender offer - I haven't seen one of these for a while. Regenersis has sold its legacy depot maintenance businesses, and now has a big pile of cash, plus the data deletion business which it bought not that long ago.

So cash is being partially returned to shareholders, through a tender offer, key details;

Maximum £50m cash being used

Shareholders can tender presumably some or all of their shares at a price they choose, within the range of 215p to 250p.

Given that the market price is currently 229p, then there's not any point in small investors tendering beow 229p - they might as well just sell in the market.

The strike price mechanism means that an order book is created of everyone's tenders, it's sorted in descending price order, and then the strike price is where exactly £50m of shares is reached. Everyone is paid the same strike price. So if not many people tender, then the price could be as high as 250p. In that scenario, everyone gets the same strike price - of 250p - even if they tendered at below that.

If loads of people tender their shares, then the strike price may be at the lower end of the range, or even scaled back if more than 29.4% of shares are tendered (that seems unlikely, but you never know). It's all down to what the Institutions decide to do basically. They might want to take advantage of the liquidity to exit, possibly?

This is a big tender offer, so I suspect it probably won't be fully taken up, which might mean that the tender price could towards the middle to top of the price range perhaps, but that's a guess - I don't know the intentions of the big shareholders. My worry would be if management decide to dump their shares in the tender offer, as that would be negative for the share price afterwards.

Remaining shareholders have to work out if the market cap, with the reduced number of shares (after the tender offer & cancellation of those shares has happened) is good value or not. I don't really know how to value Blannco.

Note that the remaining business will still have fair bit of cash.

If in doubt, talk it through with your stockbroker, to decide what the best course of action is for you personally.

I'm running out of time, due to technical glitches, and I'm having a late lunch in London, so need to jump on a train shortly. So a few quickies:

Cyan Holdings (LON:CYAN) - (I hold a long position in this share). Bonkers AIM stock of the day - it's up 124% today! This used to be a semiconductor company, but it never made any progress, so reinvented itself as selling smart meters for electricity. There's news today of a £10m contract from Iran. Cantors have put out a very interesting note today, saying that there is scope for very much larger orders from Iran.

Downside risks - bear in mind that Cyan has been strapped for cash, and cash burning, so a Placing is now very likely.

I allow myself a small pot of punting money, aside from my proper, sensible portfolio, and have picked up a few of these today. The Cantors note has certainly piqued my interest, but it's hugely speculative at this stage.

accesso Technology (LON:ACSO) - (I hold a long position in this share). Directors cashed in a lot of their personal shareholdings in a secondary placing last night. This concerns me - I usually advocate "following the money" - so when Directors cash out in size, I usually do too.

Although in this case, as I don't hold a lot, have decided to stick with it.

Styles and Wood (LON:STY) - very good results today, beating expectations, so this company's remarkable recovery from near-death continues. Although the balance sheet is still weak - negative NTAV. It's a very low margin contracting business, so not something that should ever be on a high rating - as this type of business often run into problems with major contracts going wrong. We've seen that in the past with CTO and ISG. There are no divis for 2015 or 2016 either. That said, the company is clearly on a roll, and if it continues demonstrating improved results, then the shares could have further to rise possibly? It's worth a look anyway.

ServicePower Technologies (LON:SVR) - The results out today look pretty poor. I don't see anything of interest in this company. Its balance sheet is weak too - NTAV of around zero. Difficult to see why it's listed?

Topps Tiles (LON:TPT) - quite a decent trading update today, with H1 LFL sales up 4.7% on last year. The valuation looks up with events - priced about right, I'd say. Nice company though, that's trading well, so might be worth a fresh look?

£RM2 - they seem to have changed tack, and are now getting a Chinese factory to make their innovative pallets. I'm not keen on this one - it's burned too much cash, and the business model is still unproven. Today's news pushes out the timing of volume production even further. It's too problematic, and the valuation is still pretty steep at £147m (at 37p per share). Not my cup of tea - this kind of speculative stock is where my main losses have tended to be in the past, so I find it best to try very hard indeed to avoid all blue sky type stocks. They hardly ever work out as planned.

Right, got to dash! See you tomorrow.

Regards, Paul.

(usual disclaimers apply)

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.