Good afternoon!

Today I've covered::

- Filta Group (LON:FLTA)

- Premier Technical Services (LON:PTSG)

- Taptica International (LON:TAP) (added following request)

Cheers

Graham

P.S. It's Paul here - Graham has passed me the baton, and I have added some extra comments on the poor interim results from Telit Communications (LON:TCM) , plus additional comments on Graham's sections below.

Filta Group (LON:FLTA)

- Share price: 134p (+7%)

- No. of shares: 27 million

- Market cap: £36 million

This is a US & UK franchisor of services for restaurants and other food establishments. The main service is FiltaFry (see here) which recycles cooking oil and cleans industrial fryers. There are a bunch of other related services too, some of which are operated directly by the company itself in the UK, rather than by franchisees.

2016 results were hurt by AIM admission costs but otherwise it would have been profitable.

Obviously that makes it a new listing: it has only been listed since November 2016.

I've studied it before and come away with a positive impression: strong growth rates combined with the capital-light franchise model make for a happy combination, in my book.

This trading update (for the six months to June) continues the high growth story:

The Group has experienced revenue growth of some 38% over the same period last year with each of our primary operating segments experiencing double digit growth. We have seen strong performance in both the US and in the UK, with US growth being driven by increasing numbers of franchisees, increased royalties from our existing franchisees and the UK growth being due, principally, to a very strong performance from our owned businesses.

The shares are up today even though the company confirms that H1 growth is merely in line with expectations.

Perhaps the gains are due to the company re-iterating its view that growth is expected "for the foreseeable future", as it takes advantage of cross-selling opportunities to existing customers with more valuable services.

That is a really strong point in the company's favour: once you start selling a restaurant or public canteen services to do with their fryer, it's potentially quite easy to also sell them services to do with refrigeration, for example.

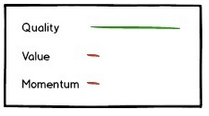

Filta is a Falling Star according to Stockopedia: High Quality, Low Value and Low Momentum:

I acknowledge that value is low here based on current financials but the company should turn consistently profitable when it is used to dealing with the costs of being publicly listed, and does appear to have a really strong growth runway to me - it's providing niche, boring services in an original way, to a fragmented market with predictable long-term demand.

Worth investigating.

Additional comments from Paul: Thanks to Graham for flagging up Filta. I've not looked at it yet, being a recent float. Its business model sounds interesting, and I like the franchise & cross-selling aspects which you flag up, which could drive growth.

I'm inherently very suspicious of all new floats - if the founders are happy to cash out some of their stake, then maybe there's something wrong? New floats often seem to be polished up, heavily promoted, and hence have a glamorous sheen to them initially - which can soon wear off!

So I'll wait until the first set of results come out, to assess it properly, on cold, hard numbers. However, it's certainly going on the watch list, for further research in due course.

Taptica International (LON:TAP)

- Share price: 405p

- No. of shares: 61.5 million

- Market cap: £249 million

More M&A activity from this Israeli mobile advertising firm.

This is a high-flying stock which has shown up on a couple of investor screens due to earnings momentum and a low earnings multiple, and the share price has been storming higher for the past year. Congratulations to anyone who has been holding it!

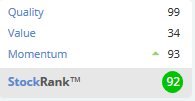

The StockRank remains extremely high even though value is not quite as compelling as it was earlier this year:

I wouldn't expect a company such as this to spill all of its secrets on its website, but it does tell us that it is handling 22 billion requests per day and has data on 220 million users in its database.

Today it announces its second acquisition in two months. The previous one was just $6 million for a Japanese mobile ads company. Today's deal is much more significant at $50 million (though it emphasises that the target has a large positive net working capital balance, i.e. is likely to be more than fully funded in its current state).

The asset being purchased has 180 full time employees working on it and sounds highly relevant. It is a:

"patented auto-optimisation solution for buying effective, programmatic cross-screen video brand advertising."

The idea is to create synergies by integrating this video platform with Taptica's mobile platform, and help to spread Taptica's global presence.

Those synergies look to be completely necessary as the asset being purchased was loss-making at the EBITDA level last year.

$20 million of bank debt will be needed to secure the deal.

My opinion: It's not easy for me to figure out whether Taptica is a good investment. Companies such as these have to be a little bit secretive by their nature. But the case studies on its website are without doubt very impressive: customers claim to get highly effective and focused marketing campaigns, as desired.

Acquisitions make me nervous but again it's possible that they can be executed well. The fact that this new asset was unprofitable last year would again suggest that a bit of caution is required.

Overall, I wouldn't be strongly tempted to invest here as it's still in my "too difficult" basket. Good luck to those who are involved, though!

Additional comments from Paul: the numbers for Taptica look great. So why are the original shareholders selling down? I'm more suspicious of overseas AIM companies, especially where founders are cashing in. That can often be a precursor to bad news.

Note comment no.9 below this article, from Stockopedia member "FREng", who wonders whether new EU rules on data protection might cause problems for Taptica? That's certainly something which investors should be aware of, and carefully investigate.

Premier Technical Services (LON:PTSG)

- Share price: 144p (-4%)

- No. of shares: 104 million

- Market cap: £150 million

Trading Update and Notice of Results

PTSG provides a range of niche building services - safety, electrical, high-level cleaning and training.

Today's update confirms that trading is in line with expectations for the full year.

The Group has previously announced that it was performing well in the first half. This performance has continued, PTSG has noticed an increase in compliance awareness among our 17,000 customers and we have experienced continuing sales growth and strong levels of orders in the year to date.

The expectations referred to above are as recently upgraded for a £20 million acquisition.

Yet again, we find the buy-and-build strategy is in vogue.

Despite raising money in a placing to pay for that acquisition, working capital requirements saw PTSG increasing its banking facilities from £14 million to £20 million.

So there is perhaps a little bit of financial strain here. Operationally it remains sound, so investors are sitting pretty. Momentum Rank is fantastic, with a score of 99, and it's hardly a surprise: the shares are nearly 50% above their 200-day Moving Average!

All of the companies I've mentioned today have talked about cross-selling opportunities from their increased range of services. PTSG is no different.

I suppose where I'd be a bit more sceptical of PTSG is that I'm not so sure about the originality of its services as compared to the competition.

Given my scepticism on that crucial front, I'm a bit wary of paying up significant multiples for the shares. So they're overheated now, in my book.

Additional comments from Paul: This is a very good group of niche companies, with excellent operating margins. The CEO is like a machine - stripping out cost, and focusing on operational efficiency in an almost fanatical way.

However, on the downside, I am concerned by slow collection of receivables - debtor days is too high, and I just don't buy the explanation given by management. Also, Bob Morton hold a big stake here, which these days is a negative for me, as his halo is long gone.

The shares have had a great run now, and the price looks up with events, or a bit ahead, perhaps? Mind you, after the Grenfell tragedy, one imagines that PTSG's services might be in more demand? Good thing too, as we cannot allow that kind of thing to happen again in this country.

Telit Communications (LON:TCM)

Share price: 162.25p (down 36.7% today)

No. shares: 129.8m

Market cap: £210.6m

Interim results – for the six months to 30 Jun 2017 are out today.

This company calls itself “a global enabler of the internet of things”. Whilst it operates internationally, I think I’m correct in saying that Telit was originally an Israeli company. Which combined with an AIM listing, is an automatic prompt for me to be on my guard.

I’ve warned readers here many times before (here is my archive on this company). In a nutshell, the problem historically, is that, in my view, the reported profits aren’t real. They were created by capitalising vast amount of costs into intangible assets on the balance sheet. That’s a clever way to create profits in the short term, and enables companies to boast of large (but essentially fictitious) EBITDA profits.

Anyway, these interim results today are really rather poor;

- Revenues – only modest growth of 6.9% to $177.6m

- Gross margin - down a little at 39.2% in H1 2017, vs. 40.1% in H1 2016.

- Adjusted EBITDA - this is a totally meaningless figure for this company, as they capitalise an enormous amount of development costs onto the balance sheet. EBITDA ignores both that capitalised expenditure, and the amortisation of previous such expenditure. So it's a nonsense, fantasy number, best ignored. For what it's worth, adj. EBITDA fell from $21.4m in H1 2016, to $14.7m in H1 2017.

- The company explains that it increased "investment" in 2 recently acquired businesses. This should reduce from H2 2017 onwards. So, if you believe the company, then there could be good upside as profits may rebound in H2 onwards.

- Profit before tax worsened badly, from $4.7m profit in H1 2016, to a $6.7m loss in H1 2017. Clearly a poor result.

So far, so bad! On to the balance sheet, which as mentioned here many times before, I very much dislike.

Placing at 340p per share, raised $49.7m (net of fees. It was $51m gross). This was in May 2017. The participants in that fundraising must be feeling total mugs now - having lost over half their money in under 3 months.

Perhaps that's why Telit has announced today that it's retained FinnCap to act as Nomad & joint broker, alongside Berenberg? Possibly they need a fresh group of contacts to tap for another fundraising? I don't suppose the clients of Berenberg & Cannacord, which pumped in the $51m in May 2017 at more than double the current share price, would particularly welcome another call to gauge their interest in injecting more funds still, if that is required?!

Net debt of $9.3m doesn't look too bad - down from $17.7m at 31 Dec 2016. Until you remind yourself that the company raised $51m from shareholders during that 6 month period. Where has all the money gone? Acquisitions, divis, and working capital absorption. In my experience, a company that claims to be highly profitable, but seems to soak up cash from investors at an alarming rate, is usually an accident in progress, let alone an accident waiting to happen.

Dividends - the interim divi of 2.5 cents last time has been passed this time. So that's another sign of a cash-strapped business. It's a bit daft to raise money from placings, pay some of it out in divis, then face another placing because you're running out of cash! The company says it will consider a final dividend, depending on circumstances.

Full year guidance - this section of the RNS today is very useful, but the key question is whether we can believe it or not? I'm sure the company gave guidance to the mugs who participated in the 340p placing just 3 months ago, and have already lost over half their money. So personally, I'd take it all with a pinch of salt. Anyway, this is what Telit reckons it will do for the full year 2017;

- Revenues of $400-430m, suggesting a good improvement in H2 vs H1.

- Beyond that, it's confident of over 15% revenue growth in 2018.

- The business is naturally H2-weighted, so certification delays for products have worsened the seasonality this year. ".. confident of a strong H2 performance"

My feeling is that the outlook guidance seems pretty good. So if you like this company, and believe management assurances, then maybe this share price plunge today could be a good buying opportunity?

Personally, given the history of very aggressive accounting, I'm not prepared to believe the guidance. If I miss out on a big winner from here, so be it. There are plenty of other good companies to invest in.

Amortisation charge for development spending - has shot up, by 80.7%, to $8.0m in H1 2017. This is the problem with pimping up your accounts, on speed, by capitalising a ton of development costs. It creates nice profits for a few years. However, then the amortisation charge explodes upwards, and wrecks your future years' profits. So previous aggressive capitalisation does come back to bite, longer term, as in this case.

Balance sheet - has certainly improved after the big placing. NAV of $169.9m is best ignored. NTAV is a better measure of reality, and looks OK at $46.1m.

However, there are red flags on this balance sheet, and I don't like the look of it one bit.

Inventories seem to have risen sharply, to $37.9m.

Trade receivables also look too high to me, at $97.3m (well over half H1 revenues - that's too high, and suggests there could be some nasties in there, maybe?).

"Other current assets" of $18.1m - looks odd to me. I hate stray debits on the balance sheet, as they can often be signs of profit being inflated, as happened at Globo.

Note that $17.9m of costs were capitalised into intangible assets in H1 - an enormous number, and another red flag.

Director selling - my attention is drawn to massive Director selling, very recently, in late May 2017, at 340p, just after the Placing. What a marvellous coincidence that the CEO managed to bank £24m in disposal proceeds (apparently to pay off a loan) just before a profit warning & share price crash! Who would have thought it?!

Cashflow statement is just terrible - awful. At best, this company seems to be trading around breakeven, in cash terms. Although maybe an improved H2 performance, and new contracts such as the Tesla Model 3 contract, could improve that?

My opinion - I'm trying very hard to find a form of words that will not result in my being sued.

I'd just say that, for me, as explained above, these accounts have more red flags than a popular beach in a storm, with a rip tide, and the danger of a passing typhoon. Plus the possibility of sharks, and jellyfish.

On the other hand, if you're prepared to believe management assurances, then the business could recover nicely in H2 - which they are pointing towards. The IoT sector seems an exciting growth area to be in.

Therefore, I think opinion is likely to be polarised with this share. I don't like it at all, but there's some good stuff in today's update (on the apparently positive outlook for H2 & beyond), which if it comes to pass, could result in a nice rebound in the shares, who knows?

So it's up to you, dear reader - do you see positives or negatives here, or a mixture of the two? Let's have a heated debate!

A couple of quickies to finish off with, before I explode with anger about Twitter, and Jeremy Corbyn's attitude towards brutal, socialist dictatorships like Cuba, Venezuela, and every other country that has tried out socialism - pretending in that calm, avuncular style that nothing is wrong! Democracy is under threat! Why aren't people concerned? They bloody well should be.

UP Global Sourcing Holdings (LON:UPGS) - here's a potentially interesting company. It was recently featured in a well-known tip sheet. I've subscribed for nearly 20 years, and I think it's a great source of ideas in a bull market. The writer takes a lot of trouble to visit, or at least talk to companies. Also he seems shrewd, and the long-term track record is amazing.

So I have a lot of respect for this publication, although as with everyone (including me), plenty of mistakes are made.

The share price has spiked up today, on the back of an interesting write-up. I like the sound of it, but it's not really for me. The company seems a sourcing conduit, between British retailers, and Chinese factories.

It's worth a look, in my view. In the past though, price spikes on tipsheets could be a sign of a very toppy market. Sometimes 10-20% price spikes can create lovely liquidity to sell into (thank you, several times, Simon Thompson!)

I don't like all that share tipping nonsense. People should do their own research, then have the courage of their own convictions, not follow the utterings of some guru, telling them what to do. You will never get buy or sell tips here! Why the hell would I want to advise or tell people what to do? I cannot think of anything worse. It's actually all about learning from each situation, and becoming better decision-makers. I think we all help each other do that. Hence the value of our wonderful comments section here, with some remarkably brilliant commentators, like Jane (who spotted IQE a long way back), and bestace (who's brilliant, on a daily basis), and many others.

My brief skirmish into fund management, put me off it for life! The clients expect superb, faultless, performance, all the time. Some of them constantly badger you when things aren't working out as planned. Forget it! I don't need their money anyway, as I can make it myself with my own limited little pot of money. For tiny amounts of fees, people expect personal attention. Would they expect that from a lawyer or accountant?

Overall, life is much simpler, if you have: no clients, no employees, and no hassle! I heartily recommend it to everyone, if you can figure out a way to make a living that way, then do it. Also, that gives you the freedom to say what you want. I frequently criticise companies in which I hold shares. So what? If the share price goes up or down, it doesn't matter to me. It's the long term prize that matters, most of the time.

The best way, in my view, is to have few financial needs. If you don't need much money, then you don't need to earn much money. A modest income from doing something you like, such as writing a marvellous blog for the UK's top financial website, is a good place to start!

Other than that, who needs a car? When my lease expires, I'm handing it back. If I need a car, I can rent one from Avis for 4-days, for £79 - an Astra. Perfectly adequate. That's not per day, that's for the full 4 days. A bargain, I reckon!

SuperGroup (LON:SGP) (in which I have a long position - this looks quite good too, topped up today. GARP, I reckon. Although VISA data today sounded negative for clothing retailers. So maybe we need to keep our options open?

Best wishes, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.