Good morning!

The fun & games continues with the major indices and currencies. I'm running late today, because I had to see how the Chinese market would behave, and it opens at 1:15am UK time, and I was up anyway. So of course I got sucked into things, and hyped up, and ended up not having much sleep! Therefore I'll be updating this article throughout the afternoon, so please refresh this page later to see the full report.

US/China markets

Perma-bear Marc Faber was on CNBC yesterday, saying that the sharp falls in US markets have nothing to do with China, but are more being driven by poor US economic data, indeed he claimed that manufacturing is already in recession. There have been plenty of other figures showing that the US is entering a soft patch, and with profit margins so high, perhaps corporate earnings have peaked in the short to medium term, who knows?

He may be right to a certain extent, but the US Futures and the Chinese markets mirror each other's movements much of the time, although China is much more volatile.

I do increasingly get the impression that policymakers don't really know what they're doing, and are certainly not in control of events. My view is that the mother of all credit bubbles (in China) could end very, very badly - and drag the Western banking system down with it too. No idea when though. Like the Euro crisis, this issue seems to recur in waves, then get smoothed over, then returns - as arguably the underlying economic problems are being masked, rather than fixed.

They also said on CNBC that the first 4 days of 2016 saw the largest percentage falls ever over that time period. Who knows if that is a harbinger of doom or not, but it's interesting nonetheless. With so much automated trading, there's no doubt that markets can be very volatile these days - "flash crashes" now happening from time to time, e.g. Aug 2015.

Therefore my approach at the moment is to be more cautious than usual. I'm only opening new long positions if they seem compelling value, and/or where there's clearly been a clumsy seller, and the shares are just selling off for spurious, or no reason at all. As I've mentioned before, it's always good to have a pot of spare cash on the sidelines, so that you can deploy it picking up bargains (selectively) when other people are panic selling good stocks at too low a price.

This is the time when such bargains can occasionally crop up - nervous markets create good pricing anomalies that we can take advantage of.

Two retailers have put out mild profit warnings today, firstly;

Sports Direct (SPD)

Share price: 483p (down 5.6% today)

No. shares: 598.5m

Market cap: £2,891m

(at the time of writing, I hold a long position in this share)

Trading update - this has only hit the share price by about 5% at the time of writing, but that might be because it was issued at 11:30am, so maybe not everyone has reacted to it yet.

The company says;

Since our interim results on 10 December 2015, we have seen a deterioration of trading conditions on the high street and a continuation of the unseasonal weather over the key Christmas period. As a result, we are no longer confident of meeting our adjusted underlying EBITDA target (before share scheme costs) of £420m for the full year. In light of these factors, and in anticipation of similar trading conditions between now and the end of April, management's current expectation for the full year is for adjusted underlying EBITDA (before share scheme costs) of between £380m and £420m.

My opinion - The share price has moved down again since I typed the above, it's currently down 11.7% on the day at 445p. I've picked up a few at that level, as it looks interesting value now, as the price had already fallen considerably from a high of 800p last year.

This looks a mild warning, only lowering the guidance, on factors that are already known - weather & lower footfall has affected everyone.

Sentiment towards Mike Ashley is negative at the moment, but personally I'll take a modest valuation combined with negative sentiment any day, rather than a high valuation combined with positive market sentiment, for a business that has decent fundamentals.

Games Workshop (LON:GAW)

Share price: 456p (down 10.1% today)

No. shares: 32.1m

Market cap: £146.4m

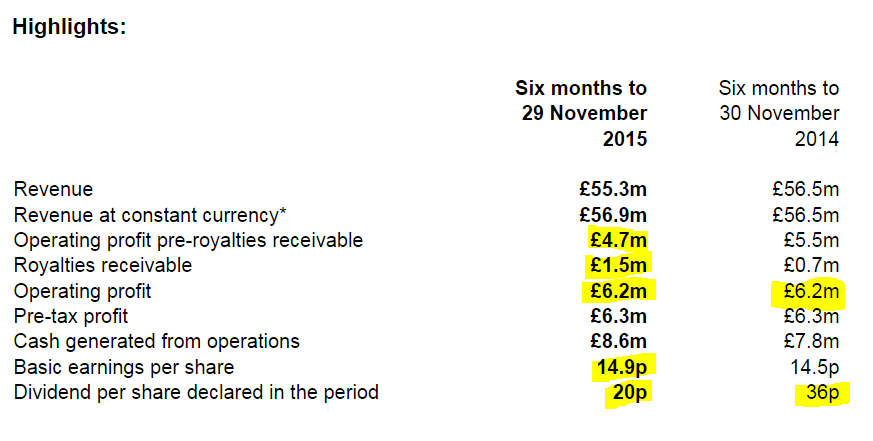

Interim results to 29 Nov 2015 & trading update - slightly lacklustre figures today from this quirky retailer (of miniature action figures, and games). Here is the highlights below, which I have further highlighted, to draw out a few points;

Note that operating profit is flat, for H1 TY vs H1 LY. However, this masks a 14.5% fall in operating profit, which was recouped with a big rise in royalties receivable, as marked above.

On reading the narrative (the section headed "Operating profit", it is explained that the company does not hedge foreign currencies, and the fall from £5.5m to £4.7m was entirely due to forex movements. That's encouraging, as it means the underlying performance of the business is actually alright - after all, forex movements are swings & roundabouts in the long term.

Outlook - the company gives a trading update today, saying;

December sales were below expectations across the Group. At this stage in the Company's financial year, the Company's internal projections indicate that pre-tax profit for the year to 29 May 2016 is unlikely to exceed £16 million. A further update will be made when appropriate.

"Unlikely to exceed" is a cap - i.e. below £16m, but how much below? One assumes that the number is going to be reasonably close to that. I suppose by leaving it open ended on the downside, using that choice of words, it gives unlimited wiggle room to the downside!

Dividends - the main appeal of this share are the generous divis. The StockReport shows a fwd divi yield of 5.88%, but with the shares down 10% today, that just got a lot better, to about 6.5%. That's only just covered by earnings mind you, so it's a policy decision to pay out all the earnings as divis, which could change if things deteriorate further, so I wouldn't hang my hat on the divis, although the financial strength noted below is very good, so that means its ability to keep paying generous divis is good.

Balance Sheet - looks very good. There is no debt, indeed it has cash of £7.8m.

It ticks all my boxes - NTAV of £39.2m is strong.

The current ratio of 1.86 is healthy.

There's doesn't seem to be any pension deficit.

So it looks a clean, well-financed, stable company.

My opinion - after today's 10% drop in share price, I would say this share is starting to look quite attractive. It's a mature business, so little to no growth. So the big question is whether it's in long-term decline? Are people still going to be buying these products in 20 years' time?

In the meantime though, it looks a financially strong, reasonably priced business, paying wonderful divis. So something I would certainly consider buying, if it drops further after today.

Note that Stockopedia likes it too, with a StockRank of 99. Although that could fall now, after today's slightly disappointing numbers.

Churchill China (LON:CHH)

Share price: 792.5p (up 7.1% today)

No. shares: 11.0m

Market cap: £87.2m

Trading update - for the full year, 2015. This reads well;

Trading in the second half year has been ahead of earlier expectations with the levels of growth achieved in the first six months of 2015 being sustained in the second half year. The Board now expects that operating performance will be ahead of current market estimates and well ahead of 2014.

Valuation - broker consensus is for 33.6p EPS in 2015. All we know is that the company is ahead of that figure, but it doesn't give any particular steer on how far ahead. I hate all this guesswork, companies should just publish a range of outcomes, or a ballpark figure, not leave us in the dark, and struggling to interpret the wording of the announcement. That's a general whinge, as most small caps adopt the same approach.

So it looks to me as if we're probably looking at 35-40p EPS for 2015. That would put these shares on a PER of between 19.8 and 22.6. That really looks an aggressive valuation for this type of business, and I question whether the shares might now be a tad over-priced?

My opinion - it's a really nice company, which I like a lot, but the price is too high for a company with rather limited growth potential. Profits have been rising mainly from improved margins, but of course that would reverse when the next recession hits. So I'm nervous about the multiple being high, on earnings that are maybe quite far into the cycle.

That said, clearly the company has executed very well since the financial crisis, management are good in my view (having met them several times), the balance sheet is very strong too, although there is a small pension deficit.

Mind you, checking back to my previous notes on this company, I thought it looked a bit over-priced at much lower prices too, so what do I know? The market likes it, and is prepared to pay up for the shares. Good luck to holders. I'd look at it again if there was some kind of slip-up, but it's not of interest at the current valuation.

MySale (LON:MYSL)

Share price: 41.5p

No. shares: 151.3m

Market cap: £62.8m

(at the time of writing, I hold a long position in this share)

Statement re share price movement - I was quite surprised to see today's statement, as usually such statements are only put out when a share price really does a really huge price movement.

The company (an online fashion retailer, specialising in "flash sales") said;

MySale Group plc (AIM:MYSL) (the "Company") notes the movement in its share price this morning and can confirm it knows of no reason for this movement.

The Board remains comfortable with the update to shareholders provided back at the time of its AGM on 25 November 2015. The Company is due to provide a first half trading update for the six months to 31 December 2015 on Tuesday 19 January 2016.

Taking this at face value, it looks as if the falling share price has just been more general sellers than buyers in the market, rather than bad news leaking out.

Looking back at the AGM statement referred to above, the company said this in its RNS of 25 Nov 2015;

"We have made a good start to the new financial year. Our focus remains on re-establishing our profitability over the course of this financial year whilst continuing to invest in our technology platform and new markets in Asia. I am pleased to say that we are on track to achieve this - the business is profitable year to date, in line with our expectations, in contrast to the substantial losses incurred for same period last year.

''We are in good shape operationally for peak trading; the recently announced acquisition of the Grays Online businesses will give us an exciting opportunity to grow our active customer base and widen our online offer; and the customer acquisition model we have been following in Asia is beginning to prove itself. Whilst there is still much to do, this has been a very encouraging start to the year.''

Note that the company has a 30 Jun year end.

My opinion - this is an interesting turnaround - an online retailer which shot for the moon, incurred heavy losses, and is now doing things more sensibly.

I think this will be one of the winners in the online fashion space - it's all down to management, and this company has experienced rag traders in it, and also has the legendary retail mogul Philip Green as a backer.

Depending on what the markets overall do, I might pick up a few more of these shares in the future, as today's update sounds reassuring.

That's me done for the week. Have a relaxing weekend, and I'll see you back here on Monday morning!

Regards, Paul.

(of the companies mentioned today, I have long positions in SPD and MYSL, and no short positions.

These opinions are my personal opinions only, and are NEVER recommendations or financial advice. My opinions are subject to change, without notice. Please always DYOR).

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.