Good morning from Paul! Here's the last SCVR before Christmas. I'll pick up on a couple of items left over from yesterday, then look at the news this morning, which should hopefully be quiet.

New way to put in tickers - instead of using £TICKER, just type the "at" symbol, and then a box pops up, where you enter the company name or ticker. This seems to work better than the old £+TICKER arrangement.

Agenda

I reveal all the companies we've reported on here, in the last 6 months (more detail below)

Superdry (LON:SDRY) - news of a bank refinancing (with a specialist, higher cost lender) is excellent, and has greatly improved risk:reward. I'm not so impressed with the trading update though, and forecast profit for FY 4/2023 has been reduced to not much above breakeven. It's difficult to get excited about this share at the moment, but it could be a good recovery share at a later date, if the market sees more evidence of a consumer recovery - difficult to imagine now, but maybe later in 2023, who knows? (more detail below)

MS International (LON:MSI) [quick comment] - more good news for shareholders, with a big contract win announced today - overseas customer, buying an anti-drone gun. It’s £22.4m, expected to be recognised in calendar 2023, so straddling FY 4/2023 and FY 4/2024 by the sounds of it. Revenues in recent years have been between £50-80m, so this looks a material deal. I don’t know what the profit margin would be on this product. If it works well, there could be follow-on sales (this is the first sale of this new gun). Graham has mentioned MSI positively here twice, in June, and earlier in Dec, and from memory I think this one was a mystery share in one of my recent podcasts. After today’s announcements, I imagine shareholders will be holding tightly, with good reason. Thumbs up from me. (no section below)

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

How many companies have we covered in the SCVRs?

When I started this column, it was an experiment to see if it was possible to review the whole small cap market. The idea came to me in 2012, so I downloaded a spreadsheet of all listed companies from the UK Stock Market website, then sorted it into market caps, and sectors. One by one, I eliminated sectors with lots of companies that I didn’t understand (e.g. natural resources, biotech/pharmas, blue sky), and also anything below £10m mkt cap, and above about £500m (at the time originally, I think, or it might have been £300m at first?). This resulted in about 500 companies remaining, which meant that if I looked at 2 unique companies each working day, I could cover everything in a year. I then began publishing it as a daily blog, and Stockopedia decided they liked it some time later, and they’ve put up with me here ever since!

Anyway, I was twiddling my thumbs a couple of days ago on a quiet news day, so pondered to myself, I wonder how many companies we’ve actually covered this year? Let’s see how the actual number compares with the original universe of c.500 companies.

Also, I wondered if we are focusing too much on my favourite shares and sectors, and not covering enough of a spread of other companies? (as a handful of readers have alleged in the comments).

So instead of guessing, let’s actually measure it, and find out what the facts are!

I must have been very bored, as this spreadsheet I created shows all the companies we have covered since 1 July 2022 to date. It then uses the “CountUnique” function to count unique tickers written about, not the total number (which would be higher, once duplicates are counted).

Drum roll please, the grand total of companies we have reported on here in the last (almost) 6 months, is 384.

6 months took long enough to work out, so I reckon if I’d extended that to the 12 months whole of 2022, then it would be a good bit higher, probably not far off 500. 450 possibly, as an estimate?

Bear in mind also that we ignore anything we think looks uninvestable or seems to be going nowhere, then I think we’re covering a pretty big proportion of the market’s sensible small caps. So if you can’t find anything of interest in our reports, then that surprises me!

Paul’s Section:

Superdry (LON:SDRY)

118p (+17% yesterday)

Market cap £97m

Trading update covering the 26-week period (‘H1 23’) to 29 October 2022

Positive start to Autumn/Winter 2022 (“AW22”) season

New financing facility agreed, and auditors appointed

New financing - I think this is by far the most important part of the announcement, because as we’ve reported here before, the situation was looking decidedly dicey - the existing bank facility had not been renewed, and it was clear from the last update that SDRY’s old bank was not interested in renewing it. That made this share very high risk, and uninvestable for me, until new arrangements had been put in place. The 31 January deadline was looming.

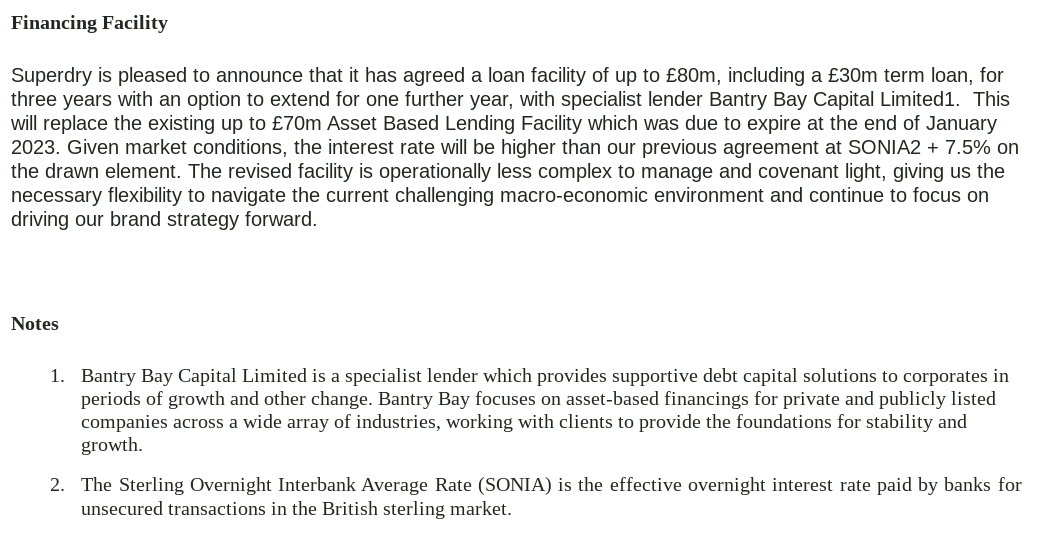

Here are the details in full -

We have to be careful when googling “SONIA”, because instead of taking me to the Bank of England website, I got information about the 80’s scouse pop singer, which wasn’t much help. Here’s the Bank of England website, which records SONIA as 3.43% last night, close to base rate of 3.5%. The historic graph is striking, at how suddenly interest rate policy has changed recently, after years of near-zero rates. No wonder there’s been a lot of market & economic turmoil this year.

SDRY will soon be paying SONIA + 7.5%, so that’s almost 11%, and likely to go higher (with markets forecasting peak interest rates of c.4.5% that would be 12% cost of borrowing to SDRY).

I’ll estimate the annual interest cost, as follows -

Term loan of £30m at 11.5% pa = £3.45m interest pa

£50m additional facility (presumably an RCF or similar), assume half used on average, half of the year = £25m * 6/12 months * 11.5% interest = £1.44m

Total estimated annual interest = £4.89m - so I’d say that’s an unwelcome expense, but it doesn’t look ruinously expensive. Although this is in the context of SDRY probably only making a tiny sliver of profit, if anything.

Net debt is only £13m at 20 December 2022, down £25m from 1 October 2022. That’s excellent, and it does reinforce what I’ve mentioned before here, that SDRY borrowing is genuinely seasonal, to fund peak stock intake, and then reduces or disappears altogether when seasonal cashflows improve. So it’s not a distressed level of debt in my view.

Bantry Bay Capital - that SDRY has had to go with an expensive specialist lender, suggests to me that the main UK banks probably weren’t interested in lending to it, or required onerous terms (e.g. tight covenants) that the company wanted to avoid.

I imagine that Bantry Bay’s phones won’t have stopped ringing from other UK companies eager to refinance problematic bank finance!

Overall though, my view is that the main risk for this share has now been dealt with. Although we don’t know what the arrangement fees are, nor the covenants (it only says covenants are “light”).

In this case, I can see the logic for paying more to a specialist lender, in order to have more secure lending facilities.

Auditors - new ones appointed, RSM, a well-known firm.

Remember that the old auditor resigned, and for several years has flagged in the Annual Report weak financial controls - so that is an ongoing risk. It wouldn’t surprise me if a large provision against inventories might be required at some stage. So this share could still be at risk from a plunge in price on a profit warning due to these poor financial controls.

To me, it also makes me feel management seem cavalier in their approach. It’s really not that difficult to control the finances of a business like this.

Trading update - we’re told this is positive, but I’m not convinced. H1 revenues are only up 3.6%, with decent store performance (up 14%) offset by lacklustre online growth, and poor wholesale revenue. Later deliveries are blamed for some of that wholesale shortfall.

Mild weather in Sept & Oct wouldn’t have helped either, as that suppresses sales of more expensive coats & jackets, but the more recent cold snap will have helped.

“Margin dilution” which presumably just means a lower gross margin, of over 200bps is bad news. For context, on £644m forecast revenues for FY 4/2023, that’s c.£13m lower gross profit, which would largely drop through to the bottom line. It’s not clear if this shortfall is against last year (probable), or forecasts.

Forecasts - many thanks to Liberum for publishing an update. This shows it reducing estimated profit from £16.2m to £10.4m, for FY 4/2023. So only just above breakeven really, on revenues of £643m, that’s only a profit margin of 1.6%

We are in a consumer downturn though, so tough conditions exist. Plus this sector has seen lots of upward cost pressures, and supply chain issues. Could some of those problems partially reverse in 2023 perhaps? Also remember SDRY has a long tail of loss-making shops (evidenced by the IFRS 16 entries on the balance sheet), so over time that should improve, with rents renegotiated downwards on renewal (or exit).

My opinion - given that competitors are in some cases really struggling, and in the case of Joules even collapsing, then SDRY’s performance so far looks OK, I think.

Renewing its essential bank facilities (albeit on more expensive terms) greatly improves risk:reward, so paying 120p now for SDRY shares seems to me far more logical than paying 100p a few days ago - when you were taking a risk of a 100% loss. That 100% loss risk has now gone.

It all boils down to what you think of the brand, and how likely a recovery in performance is?

Overall, I can’t decide, so am probably neutral on this share. At some stage though, the stock market might decide to get more bullish on it, anticipating a consumer recovery.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.