Good morning, we have Paul & Graham here today. I hope you're coping alright in this heatwave. Today's report is finished.

Mello Monday tonight - last one before the Mello team down tools for the summer! Details here.

Agenda -

Paul's Section:

Joules (LON:JOUL) (I hold) - a Sunday Times article reveals that KPMG debt advisory has been called in. An RNS from the company this morning confirms it. Clearly not good news, and this share is now a lot more high risk, unfortunately.

Hostmore (LON:MORE) (I hold) - another one of mine, which has crapped out due to the consumer downturn. Today's update is reassuring though - forecasts have been considerably lowered, and it's trading in line - that's the way to do it. I challenge the EBITDA numbers though, which translate into very little real profits this year!

MJ GLEESON (LON:GLE) - not a company I know well, but I'm very impressed on a review of today's positive trading update. This share looks really attractively priced right now, and with an average selling price of only £167k, its niche of affordable homes should be relatively insulated against macro headwinds. Uncertainty over cladding remediation costs looks the only negative.

Graham's Section:

Quartix Technologies (LON:QTX) (£161m) - A good trading update from Quartix, guiding full-year results in line with market expectations. Growth is according to plan, and H2 should show further improvement compared to H1. I remain impressed with this company’s transparency and see many attractions as a potential investment. Unfortunately, the valuation of six times annualised recurring revenues is very aggressive, especially when you consider that total revenues are only growing at a single-digit rate and the company continues to battle against underlying price erosion.

MPAC (LON:MPAC) (£54m) - A nasty profit warning and Mpac gets its earnings estimates slashed. A partial recovery is seen next year, with an almost full recovery in 2024. My concern is that recovery appears to be reliant on supply chain, economic and inflationary problems being fixed, which I’m not sure I’d be willing to bet on. Of course, many companies are in the same boat and also need these problems to be resolved. Mpac does at least have a decent net cash position, which should help to support the valuation.

Podcast - episode 2 of Paul's small caps podcast went up on Saturday - it's here. Sorry about the glitches with the phonetic alphabet, I seem to go blank once recording starts, so will practice this week. We'll get them onto a proper podcast platform at some stage. One step at a time.

The idea behind my podcasts, is to provide an easy to digest summary of the key companies covered in the week's written SCVRs. Also it's a chance for me to have a think & a ramble about market conditions/macro, etc. I jot down points on paper during the week, then run through them on the podcasts. Also, if they're shared widely by you, then hopefully it might drum up some new subscribers for here - as sadly some people do drift away in despondency - at exactly the time that the bargains are emerging.

As I keep saying, it's the hard work done now, researching the market for the bargains, that lays the ground for our multi-baggers of the future (timing unknown). Hence for anyone with cash, this is a tremendously exciting time. For everyone else - decent shares recover, in the long run, they always do. Note the emphasis on the word "decent"! That's key. StockRanks can be a great help there, which combined with my balance sheet analysis of practically every company I cover, gives you some good tools to deploy. Plus of course, the absolutely vital process of doing your own research.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Joules (LON:JOUL) (I hold)

33p (before market opens) - update at 09:44 - 26.5p (down 20%)

Market cap £37m - update at 09:44 - £30m

The Sunday Times is at it again! Last week it undermined AO World (LON:AO.) by reporting that a trade credit insurer had reduced cover. As it turned out, AO was in the final stages of organising a placing. I imagine (but don’t know for sure) the placing price probably had to be reduced, as a result of the S.Times article clobbering the share price.

Still, we can’t really shoot the messenger. This situation once again reinforces the madness of the UK system, where shares continue to trade, despite hundreds of people knowing that a discounted placing is going on in the background. This clearly creates a false market, and has to be stopped. It’s top of my (long) list of things that are wrong with the UK system. Shares should be suspended, and a fast fundraising process done online, with minimal fees. We’ve had the tech to do this for over 20 years. We need to lobby Govt over this - they want ways to make London more attractive for listings, surely rapid & cheap fundraising would be ideal? That’s one of the key reasons markets exist - to raise capital, as well as provide a market for secondhand shares.

Anyway, my Sunday roast at the Englefield (my favourite London haunt when I’m up here) was ruined after I spotted a small article on the front page of the business section, about Joules (LON:JOUL) (I hold), saying it had engaged accountants KPMG (debt advisory practice) “to help shore up its cash position”.

We already knew Joules was having trouble, after a series of profit warnings, supply chain problems, and resignation of its CEO. Also, previous broker notes indicated that the business was now being run for cash (it has excess inventories which are being wound down, so is constantly offering discounts online). I wouldn’t normally get involved with anything that needs extra cash, but took a risk here, because JOUL owns the substantial freehold to its new head office, the idea being this could be sale & leased back, thus easing the pressure on bank debt that’s not excessive to start with.

Although, as we know, once companies become loss-making, as JOUL will certainly be currently, then bank covenants are usually breached, and banks get jittery, and may withdraw facilities.

JOUL has responded promptly this morning, this is what it says -

Joules, the premium British lifestyle group, provides a statement in response to an article published in The Sunday Times.

My summary -

Confirms KPMG debt advisory have been appointed.

Provides the (now outdated, 7 weeks ago) year end liquidity position -

As at 29 May, the Group had net debt of £21.4m, giving £11.3m headroom within its banking facilities, in line with the Board's expectations.

This is reassuring, providing the bank facilities remain available -

Whilst the Group continues to manage its cash resources carefully over its seasonal borrowing peak, it expects to have sufficient liquidity to manage its working capital requirements over this time.

Strategy - this confirms what it has already said before -

The Group is making good progress against previously announced key initiatives aimed at simplifying the business and optimising the cost base to improve long-term profitability. This includes implementing significant changes to its wholesale operations to focus on fewer, profitable wholesale accounts and improving and simplifying the Group's end-to-end product process to reduce costs and shorten lead times.

My opinion - it feels as if JOUL seems a bit rudderless at the moment.

There’s tremendous upside potential, if it can be decisively turned around - look at previous profits when trading well. In my view that requires a drastic cull of the bloated central overheads - which are similar to Superdry (LON:SDRY) in terms of headcount, but JOUL is half the size in terms of revenues. That doesn’t make any sense to me.

Also, I don’t think the central overhead is doing a very good job - they seem to mess up supply chain at regular intervals, and the product is currently uninspiring & over-priced. Hence why I get daily emails offering big discounts.

We talk a lot here about pricing power, and if a brand is constantly discounting, then it hasn’t got pricing power, and the product isn’t good enough. Once customers get used to paying 50% less, it becomes addictive, and they just wait for the products they like to be reduced in price. All that set against rising costs, is an unhappy mix.

My other worry is that reporting accountants are often brought in at the behest of the bank - I have personal experience of this brutal process - and the report from the accountants is then used by the bank as cover to withdraw facilities, prompting an existential crisis.

It’s a bit different for listed companies though, as they have access to fresh capital from the market.

Hence I think a dilutive placing now looks highly likely, and that’s bad news for existing holders like me. It should be able to get a placing away, given that the founder holds a big stake, and has deep pockets from a previous large sale.

There has to be a risk that a pre-pack administration could be used to grab the business on the cheap, so that’s an increased worry now, as this wipes out all other shareholders - as we saw at Studio Retail recently.

On the upside, KPMG might be able to help arrange a sale & leaseback on the big freehold property, although I think about £9m of the existing bank debt is secured on that already.

This situation should be fixable, because it’s not actually that much debt, at £21m, and the bank has security on a freehold property in the books at about the same cost.

So a say £10-15m placing, and a sale & leaseback, would be more than enough to wipe out all bank debt. It’s doable, but that depends on current trading, which is not mentioned in this update.

Overall then, this has to be seen as higher risk, after the news of KPMG getting involved.

Apologies for getting this one wrong - I didn’t expect trading to deteriorate anywhere near as much as it has done. Fundamentally, the current crisis has been caused by poor management.

.

.

Hostmore (LON:MORE) (I hold)

34.5p (unchanged at 08:45)

Market cap £43m

Hostmore plc (the "Company" and, together with its subsidiaries, being the "Group"), the hospitality business focused on American-themed casual dining brand, 'Fridays', the cocktail-led bar and restaurant brand, '63rd+1st', and the fast casual dining brand 'Fridays and Go', announces an update on trading for the 26 weeks ended 3 July 2022.

It’s a calendar year end, which I’ll call FY 12/2022, but due to weekly accounting which retail/hospitality often use internally, period ends are typically a day or two either side of the month end date.

PR headlines look good -

Trading in line with expectations

Growth opportunities remain, despite consumer caution

This seems encouraging -

Guidance for the full year remains unchanged, with LFL revenues for the period since 23 May 2022 in line with the expectations set out in the trading update issued on 26 May 2022.

This is what the company said in that last update on 26 May (my summary) -

LFL revenues down 6% on pre-pandemic 2019 (for 20 weeks to 22 May 2022)

Guidance - LFL dine-in volumes expected to be down 8% for the rest of this year FY 12/2022. I take that to mean the volume of meals/drinks served, not the revenues generated.

That’s an important but confusing distinction.

Price rises to mitigate half the volume decline - which implies that LFL revenues (vs 2019) would only be down 4%. I've lodged a query with the company on this point, so will update this article once my query is responded to.

EBITDA margin (pre-IFRS 16) in low double digits for FY 12/2022 - which is actually quite good, given tough macro conditions for discretionary consumer spending (although I query the calculations below).

The market seemed to largely ignore this update in May, which struck me as a lot better than might have been the case, in current conditions.

Roll things forward to today, which I summarise -

- Full year guidance unchanged.

- Roll-out of new 63rd+1st restaurant/cocktail bar format is continuing, with 4 sites now operating. (Have any readers visited them? I’d love to hear a mystery dining report!)

- Bank facility increased from £25m to £30m, and extended by a year to Oct 2024.

Valuation - this is tricky. The only current research I can find is from Finncap - it has pencilled in these key numbers for FY 12/2022 -

Revenues £214m, Adj EBITDA £40.1m, Adj EBIT £17.0m, Adj PBT £3.5m, Adj EPS 2.3p.

Note how the massive EBITDA number has almost disappeared by the time we get to PBT!

At first I thought this might be a typo, but the c.£13.5m drop from EBIT (operating profit) to PBT, is consistent with other years in the forecasts table. It must therefore relate to a finance charge of £13.5m, which is far too big to be just bank interest, it must relate to the notional interest cost re leases, under IFRS 16.

I’ve worked it out now, from looking back to the FY 12/2021 accounts. Note 5 shows that of the £13.6m finance charges, £10.2m is “interest on lease liabilities”. Therefore any numbers above this line are meaningless!

Even the pre-IFRS 16 EBITDA number looks unrealistic, because it doesn’t seem to be adjusted for the finance charges related to leases.

For these reasons, I don’t think the EBITDA or free cashflow numbers quoted by the company look realistic.

The bottom line for me is that it’s only expected to make £3.5m PBT this year, just above breakeven.

Forecast EPS is 2.3p this year (PER 15 - in a tough year, so not excessive).

Forecasts for 2023 & 2024 are a big rise in EPS to 7.2p, and 11.2p. If it can achieve anywhere near those forecasts, then shareholders could be on to a future multibagger. It might be more prudent to assume a slower recovery in earnings perhaps?

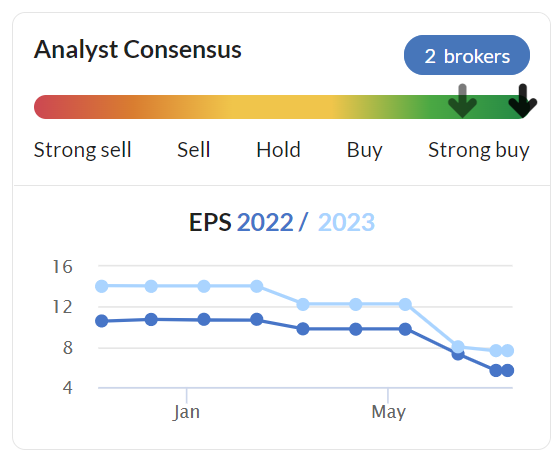

Note from the broker consensus graph from the StockReport below, forecasts have come down a lot - which is exactly what we want to see! More realistic, lowered forecasts, then an in line update. Other companies & brokers, please take note! Get the forecasts down to a realistic level, then we can invest!

.

My opinion - given where we are in the economic cycle, I am not at all keen on companies increasing borrowing facilities. However, it does mean the bank is happy, and will see the management accounts that we don’t get to see. Hence it is reassuring in a way.

My worry is that, the more debt that cyclical companies take on, then the less safety margin there is for investors if trading subsequently really hits a brick wall.

A bit more digging into the numbers has made me distrustful of EBITDA here. The curse of IFRS 16. I’m happier working on adj PBT, which is only £3.5m for this year. There’s a hefty depreciation charge of physical assets though, so it does mean decent cashflows being generated, to fund the roll-out of new sites, in 3 different formats.

Management are ambitious, and strike me as competent.

The valuation has collapsed mainly due to macro factors, not to company-specific problems.

I think long-term, this share should do well from this bombed out level. It's starting to find a level where people seem to be buying.

MJ GLEESON (LON:GLE)

526p (up 2% at 13:00)

Market cap £306m

I’m not familiar with this housebuilder, but thankfully Roland wrote an excellent summary in May last year, here. Comparing the figures that Roland mentioned then with now, in particular a Price to Tangible Assets ratio of 2.19 being a bit high, it’s now dropped to only 1.15 - very much more appealing to value investors.

So what’s the news today?

MJ Gleeson plc (GLE.L), the low-cost housebuilder and land promoter, today provides an update for the year ended 30 June 2022 ("FY2022").

This sounds good -

Full year results expected to be significantly ahead of expectations

Here are my notes -

2,000 house completions - hit target of doubling over 5 years.

Completions up 10.4% against tough LY comparisons.

Strong selling prices offset higher building costs - very good.

Key point - avg selling price really low, at £167k - highly affordable.

Availability of materials and labour has improved.

Reservations shortened to 34 days from release (LY: 49 days), showing strong demand.

Recent activity - reservations up 16% on LY, in last 8 weeks - (so no sign of a slowdown, or loss of confidence then).

Planning congestion a nuisance but not a disaster (my words!)

Land - available at “sensible prices” still, has pipeline of >8 years sales, owned or purchased subject to planning permission.

Cash of £33.8m, and no debt (flat vs LY).

Key point - Cladding - possible costs - this sounds a bit vague, as if they don’t really know, so this is a key point to clarify.

Overall trading significantly ahead.

Balance sheet - I exclaimed “bloody hell!” when I saw the last reported balance sheet as at Dec 2021. It’s incredibly good!

Total tangible assets of £308m, less total liabilities of only £65m, gives NTAV (no intangibles) of £260m. The market cap is £306m. But remember that everything is on the balance sheet at cost. So inventories in particular of £245m are likely to be worth considerably more than original cost.

Hence you could argue that this share might be trading at a real world values discount to NTAV. That’s quite exciting.

My opinion - this looks really interesting, and gets an SCVR thumbs up, for readers to do some more research for yourselves.

What I like most, is that this builder is making houses that are being sold for only £167k, and making good profits at that level. As the commentary says, this is so affordable that a couple earning just Living Wage could buy one, and it would be cheaper than renting. That strikes me as an excellent market position in current uncertain times.

The only negative I can see is the uncertainty over cladding remediation costs, which needs more clarity.

Of course, if you think house prices are likely to crash, then the whole sector is best avoided.

.

Graham’s Section:

Quartix Technologies (LON:QTX)

- Share price: 335p (+2%)

- Market cap: £161m

During my sabbatical, this company adjusted its self-description.

It used to call itself: a leading supplier of vehicle telematics services to the fleet and insurance sectors.

It now calls itself: a leading supplier of subscription-based vehicle tracking systems.

The reason for this isn’t too hard to understand: revenues from the insurance sector have been intentionally allowed to shrink for some time, as it focuses instead on the “fleet” business.

Let’s bring you up to date with today’s trading update for H1 (ending June 2022):

- New unit subscriptions +26% versus H1 in 2021.

- Revenue, adjusted EBITDA and free cash flow for the full year are expected to be in line with consensus market forecasts.

There’s an important point about Quartix which stands separately to its underlying business: it is a model for how small companies should communicate to shareholders.

I’d give Quartix a higher valuation than it might otherwise deserve, purely as a result of this factor. It is transparent, it publishes clean numbers, and it gives better information than most other companies do.

Looking ahead, the company expects H1 revenues of £13.3m, and then full-year revenues of £27.4m. That implies 6% sequential growth from H1 to H2 – not bad.

Similarly when it comes to adj. EBITDA and free cash flow, Quartix is expecting H2 to be a little better than H1.

I am reminded by previous SCVRs that Quartix doesn’t capitalise development spending. That being the case, the use of adj. EBITDA by Quartix is less objectionable than it normally is.

(When a company capitalises development spending, the cost of that spending isn’t counted until it is amortised – the “A” in EBITDA. If that company asks you to focus on EBITDA, it is asking you to pretend that development costs don’t exist. This is common practice.)

Continuing:

- Vehicle subscription base +9.4% to 221,800 vehicles.

- Annualised subscription base value +6.6% to £26m.

These percentage growth figures look quite disappointing compared to the 26% growth figure mentioned earlier.

But you have to remember that 26% was the growth in new subscriptions. It doesn’t reflect the growth in overall subscriptions or total revenue, and it’s not adjusted for any loss of customers. It’s a second derivative!

Quartix does focus quite a lot on this second derivative. Here are new unit subscriptions by region:

The USA is set to benefit from “new strategic initiatives in the region”.

Price erosion

This has been a theme at Quartix for a while. I’m always looking for quasi-monopolistic companies with a great deal of pricing power, so price erosion is definitely not something that I like to see. Quartix says:

Price erosion over 12 months calculated at constant currency rates continues to improve and was 5.6% compared to 6.5% in the same period in 2021.

It’s comforting that there’s an improvement in this regard, but the fact that price erosion is still occurring would certainly trouble me, if I was a shareholder. With prices falling over time, is it not natural to conclude that Quartix’s technology is being imitated or even improved upon by competitors?

Annualised revenues are growing at a slower pace than the growth in subscribers. I’d really like to see price erosion come to a halt, to boost my confidence in the uniqueness of what Quartix is offering.

Quartix has launched a new product for electric vehicles, and is about to launch a new product to assist with vehicle checks. Maybe these will help to reverse the price erosion trend?

My view

I can accept that subscription-based businesses with predictable recurring revenues and strong margins are worth a multiple of sales. Quartix does have predictable recurring revenues and its margins are even better than you get from the headline figures, because it expenses many of its costs upfront.

I also believe that Quartix deserves a valuation uplift for the quality of its shareholder communication, its historic cash generation and its willingness to pay cash out to shareholders. Dividends have been paid every year since 2015, albeit with a few cuts in the tough times:

My difficulty is with the valuation multiple of six times annualised recurring revenues. Given the underlying price erosion and the single-digit growth in sales (in a highly inflationary environment), I worry that investors might be getting carried away with the impressive second derivative figures which the company publishes.

At two or three times recurring revenues, I might be able to argue that this was a bargain. At six times, I have to admit that I’m sceptical.

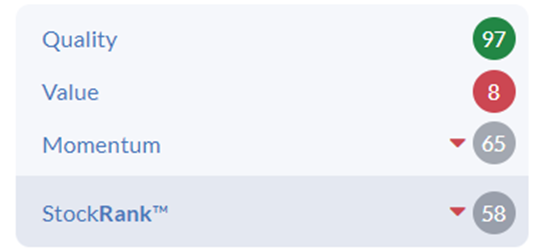

The computers at Stockopedia agree with me, and see very little value on offer here. Although Quality is excellent, as expected, and momentum is ok:

.

.

MPAC (LON:MPAC)

- Share price: 267p (-30%)

- Market cap: £54m

An almighty share price drop for this packaging/automation company, on a nasty profit warning.

In May, the company warned of “supply chain uncertainties and operational challenges amplified by transportation delays at global ports and increased macro-economic uncertainty”.

Mpac maintained that “prospects remain positive”, and the share price survived intact on that day, though it did drift lower in the weeks that followed.

Today’s announcement is much worse. The supply chain and economic problems “have become more acute in recent months resulting in extended lead times and cost inflationary pressures which are impacting the Group’s operational efficiencies and margins”.

As a consequence, FY 2022 profits will be “significantly below current market expectations”.

Mpac follows the usual pattern of not saying what current market expectations are, and also not saying what the new market expectations should be.

But the company’s broker previously had an adj. EPS forecast of 34.5p. It has today reduced that forecast to 13.7p, or by 60%.

The forecast for next year is reduced by 26%, to 27.4p.

As Paul has said, it is unfortunate when forecasts aren’t gradually revised lower, and instead we get these awful share price collapses when the estimates get slashed.

The company itself thinks that the big-picture problems it faces will ease in 2023, but on what basis?

Supply chain and operational challenges are likely to continue for the remainder of 2022, before easing in 2023.

I hate to rain on anybody’s parade, but I’m not convinced that inflation is set to ease in 2023. Granted that some of today’s supply chain problems might be fixed, and that price pressures for certain components and certain products may ease, but I would be very cautious before betting on a “return to normal”.

If we put a positive spin on it, Mpac’s adjusted PE ratio for 2023 is now less than 10x, and is lower again if we see a full recovery happening in 2024.

And this does not adjust for the net cash position (£14.5m at the end of 2021).

With that cash, Mpac does enjoy some flexibility in how it responds to its challenges. Hopefully, this will put a floor on how bad things can get for the company and its shareholders.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.