Good morning, it's Paul here!

7-8am comments

Staffline (LON:STAF)

An update is given today.

Key points;

- Results for FY 12/2018 due out on 27 June 2019 - cutting it fine for the 6 month deadline - due to detailed investigation into compliance with minimum wage regulations

- Increasing related provision from £7.9m to £15.1m (a cash cost in 2019) - another example of how the initial assessment of accounting problems is usually the tip of the iceberg

- Total exceptional costs for 2018 now £32.6m

- Possible breach of bank leverage covenant - will require a waiver

- Operating within bank facility limit & expected to continue so

- Placing to raise £30m + £7m open offer

- No final dividend, which shouldn't come as a surprise to anyone

- On the positive side - underlying performance for 2018 in line with expectations, and same for 2019 - EBIT in range of £23-28m, and y/e net debt also expected to be in line (previously guided up sharply)

My view - Placings are normally done on the sly, and the first private investors know about it, is when the deal is announced. It's a terrible system, because information often leaks out, thus creating a false market in the shares.

What should happen is that shares should be suspended when a fundraising of any kind is taking place.

Pre-announcing a placing, as in this case, is an open invitation for traders to short the share. Emergency fundraisings like this can be done (if at all) at a deep discount, as new funders demand their pound of flesh. It all depends on the strength of the broker & its contacts, plus how convincing management are in the meetings that take place with possible funders. So this is a very uncertain situation until the deal is done. In an ideal world, existing institutional shareholders step up and support a fundraising, in order to defend the value of their existing shares.

For me, it's uninvestable until the placing & open offer complete. After that's done, I think it could be worth taking a fresh look at the refinanced company.

It's perfectly reasonable for the bank to require an equity raise, of a similar size to the exceptional costs.

I think shareholders will need to prepare for another potentially ugly day today. Let's hope the broker can get the placing done & dusted quickly - as the price could be potentially very low.

This situation has been incredibly badly handled. It's another example of how an acquisitive group borrowed too much from the bank, hollowed out its balance sheet with goodwill, and then did not have adequate financial strength to deal with an unexpected problem.

The previous CEO timed his exit & shares disposal almost to perfection. That happens quite a lot, doesn't it? Hence why for me, a major/total disposal by Directors, is probably the biggest sell signal you can get.

After 8's

Continuing the theme of financial distress;

Kier (LON:KIE)

Share price: 118.7p (down c.9% today, at 10:03)

No. shares: 162.1m

Market cap: £192.4m

Strategic review & indebtedness update

Kier is a sprawling, acquisitive group, covering infrastructure, building, and services. To learn more about the group (which I've not covered before, as it's not been a small cap until now), I've perused a useful presentation slide pack here, covering the interim results to 31 Dec 2018. Major infrastructure projects the group undertakes seem to be mainly public sector contracts, and utilities companies, e.g. constructing a lot of roads projects (e.g. so-called smart motorways).

I find complex groups like this very difficult to analyse, as there are so many moving parts. That's why generally I stick to smaller companies, whose accounts are easier to understand.

The other weekend, whilst stuck indoors during non-stop rain, I spent some time looking at Kier. I came to the conclusion that the shares looked dirt cheap, on a forward PER of 2.5, and that the net debt seemed relatively modest. The shares were 155p at the time, and I even put a "Buy Kier" note onto my calendar for the following Monday.

Thankfully, two things made me hold back from buying;

1) Sector - this infrastructure building/services sector has been a graveyard for investors. So many groups have gone wrong, often involving a collapse, a recent example being Carillion.

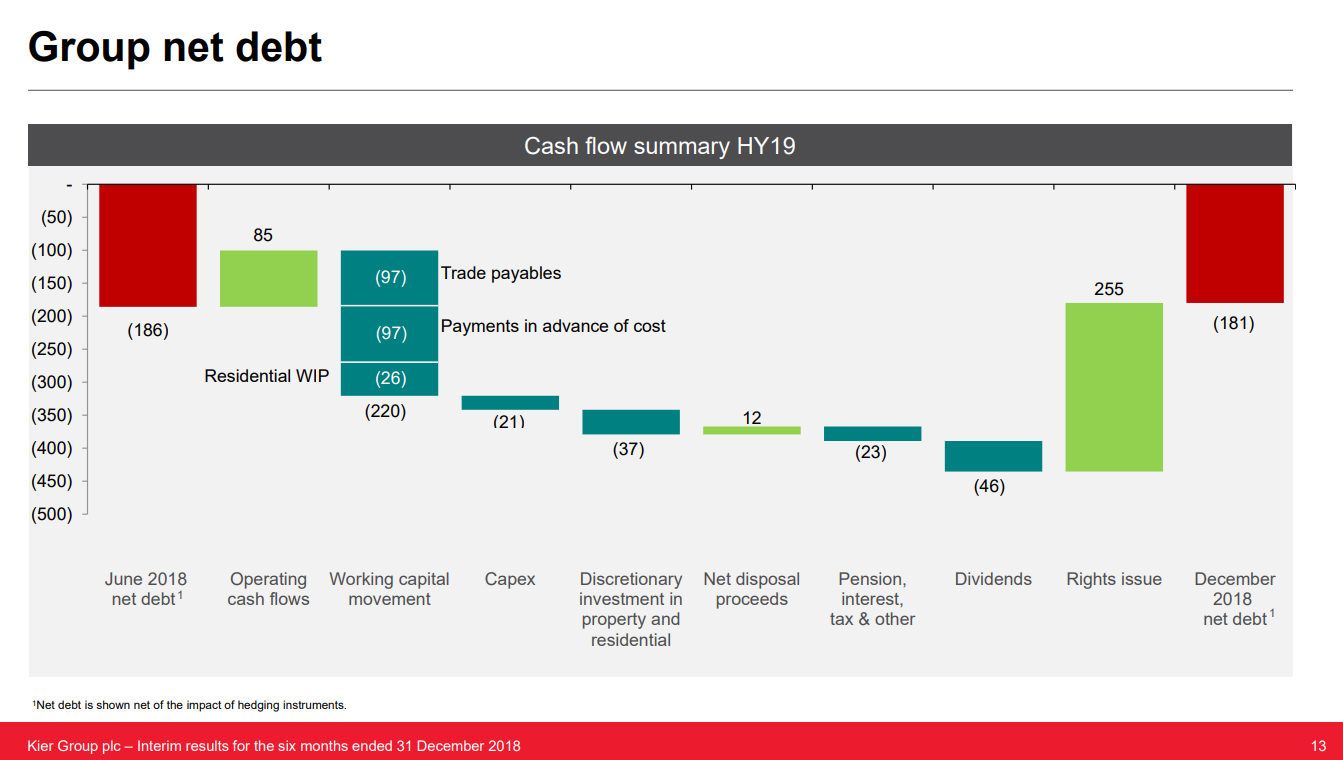

2) A horrible cashflow graphic in the presentation pack linked to above. This reminded me that I'm increasingly coming round to the view that I should treat the balance sheet & cashflow statements as the most important. The P&L is really the least important statement, as it's the easiest to massage to present a favourable picture. Therefore, maybe as investors, we're getting it all wrong by concentrating on earnings-based valuation measures such as PER?

The above graphic shows us that the proceeds of the £250m (net of fees) Rights Issue in Dec 2018 was entirely consumed within just 6 months, by adverse working capital movements of £220m, and paying divis of £46m.

Trade credit insurance - very recent press reports suggest that trade credit insurers have been withdrawing cover for Kier's suppliers. This is an often-overlooked, but crucially important point. Trade credit insurers such as Euler, guarantee that suppliers get paid, even if their customer goes bust. This enables suppliers to extend credit to their customers (such as Kier), without having to worry that the customer might go bust, leaving them with a bad debt. It also satisfies banks that the supplier may be borrowing from, that it also won't go bust from suffering a bad debt.

I've had a lot of dealings with trade credit insurers, and they can be trigger-happy (understandably, as they're taking large risks) in withdrawing cover, when any doubts arise about the solvency of a company. Such withdrawal of insurance cover can tip a struggling company over the edge, and lead to it going bust - since without insurance cover, many suppliers refuse to send in fresh deliveries, thus causing the struggling company's business to grind to a halt.

... Kier is in regular dialogue with its largest customers who continue to be supportive during this period of volatility.

Kier understands that certain suppliers have experienced a reduction in the level of trade credit insurance available to them; Kier is working with those suppliers to mitigate the impact of this...

Update today - where do I start with this? There's so much information to process.

Here are what strike me as the key points;

1) Improve cash generation & reduce debt;

... insufficient focus on cash generation and that the Group today has debt levels that are too high...

Well done to Kier for being straightforward about the problems. The net debt looks fine, but it's the gross debt that's too big. A reminder that balance sheets are often window-dressed to present an artificially favourable picture on one day.

Hence why reform is needed of accounting standards, to focus on average net debt throughout the year, not a snapshot on the year end date. Kier does give average monthly net debt, but I wonder if that is calculated on month end dates, or a daily average? If any readers know, perhaps you could post a comment accordingly. This excerpt today is very good;

... Going forward, Kier will focus on managing its retained businesses to deliver long-term profits and a sustained reduction in the Group's underlying debt levels rather than targeting lower debt positions at reporting dates.

2) Simplify the group through disposals

3) Cost cutting - staffing is in the process of being reduced by 1,200 people, saving £55m p.a.

Borrowing facilities - not repayable for a while, but bank facilities could become repayable on demand, if bank covenants were to be breached;

The Group has committed debt facilities of £920m, with its bank debt not maturing until June 2022 and the majority of its private placement debt maturing between 2021 and 2024.

While some of the recent external commentary has had an adverse effect on confidence, with a consequential impact on the Group's working capital position, the Group's liquidity headroom is able to absorb the volatility that this has caused.

However, it will result in reported net debt at 30 June 2019 being higher than current market expectations and an increase in FY2019 average month-end net debt to £420m-£450m.

It looks as if I've answered my own question there, in that average net debt seems to be the month end figure - i.e. not necessarily typical of the net debt at other times during each month.

On the upside, the above strategy is going to reduce net debt, therefore I imagine the banks would remain supportive as this process is implemented;

The Board considers that the revised strategy outlined above, together with the related actions which are now underway, will result in a significant reduction in the Group's net debt during FY2020.

Dividends - the yield was ridiculously high, at about 20%, which already indicated that the forecast divis are not going to happen!

This is confirmed today;

The Board is suspending dividend payments for FY2019 and FY2020. The Board will continue to review dividend policy for future financial periods.

Balance sheet - last reported as at 31 Dec 2018 (interim period end).

NAV: £713.6m. Deducting intangibles (goodwill) of £829.9m, gives;

NTAV: Negative, at £-116.3m - I try not to invest in anything with a negative NTAV, unless it's super-cash generative. Kier seems to be super cash-absorptive, as noted above.

JV investments are on the balance sheet at £238.3m - I don't know how realistic this is, and how much off balance sheet debt might be included within that?

Pension deficits - there's a pension asset of £33.4m, and a pension deficit of £49.9m. I tend to ignore the balance sheet entries, and look at the actual cashflows. In this case, Kier paid £11.9m deficit contributions into its pension schemes, in H1, so almost £24m annualised (assuming H1 & H2 are the same). That's clearly a big issue.

My opinion - I had a close shave with this share - almost buying a few days ago, as it looked remarkably cheap on a PER basis, and the net debt didn't look too bad.

Lessons learned;

- A very low PER means the market thinks there are deeper problems, yet to emerge. The market was right.

- Net debt can conceal a much worse gross debt figure, through window-dressing to get debt down for reporting dates.

My over-arching feeling from trying to dissect the last accounts, is that it's way too complicated for my pay grade. There must be plenty of analysts covering the company, who will understand it better than me. The trouble is that city analysts are not independent, and are almost always under pressure to show things in a positive light. Therefore, all research needs to be seen through sceptical glasses, were there to be such a thing.

I can only conclude that this is way too complicated for me.

It's also high risk, as there's an admitted issue with bank funding, and trade credit insurance.

I think on balance, this situation looks salvageable. If you compare Kier's negative NTAV of £-116m, it's vastly better than (slightly larger in revenues terms) Carillion's negative NTAV of £-1,956m at 29 Sept 2017 - accounts here. Carillion was hopelessly insolvent, as pointed out here in our SCVRs, long before it went bust. Whereas Kier is not in anything like that degree of financial distress.

I think, if it's well-handled, that Kier could get through these problems. That needs continued support from the banks (usually forthcoming, if they trust management & the accounts). It probably also means another rights issue is likely to be needed, once the ship has been steadied.

Would I want to gamble on the equity at the moment? In a word, no. This is for high risk special situations investors, who've done their homework properly, or for complete punters. I think Kier is not a basket case, but that doesn't necessarily mean the equity makes a good investment.

Overall then, too high risk for me.

Premier Technical Services (LON:PTSG)

Share price: 98p (up c.3% today, at 13:41)

No. shares: 126.3m

Market cap: £123.8m

AGM statement (trading update)

...the niche specialist services provider...

Updates us on its progress to date, for FY 12/2019.

"I am pleased to report that the Group has seen continued sales growth and strong levels of orders in the year to date. In addition, working capital utilisation, margin and profit levels are in line with the Board's expectations.

The recent acquisitions of Guardian and Trinity are performing ahead of management expectations. This underscores our confidence in achieving a successful full year result in 2019.

I wonder what "working capital utilisation" means? Nice and vague. Cash is king.

The big question mark over this group's accounts, is excessive receivables (debtors). This can often be a sign of underlying problems, and for me it's a major red flag here. Directors talk about the group being highly efficient, and managed very tightly, yet they take nearly 90 days to collect in receivables. I don't buy it. There are some adjusting factors, but even after the best possible light is shone on the numbers, the trade receivables number is still way too high.

There are several other red flags with this share, in my view - e.g. completely inappropriate benchmark (EBITDA), and excessive management rewards for hitting that target - i.e. providing a multi-million pound incentive to adopt aggressive accounting techniques.

Numerous acquisitions can also increase risk - as it's more difficult to understand, compare with prior years, or otherwise rely on, the accounts.

I don't accept the explanation given about booking a large, one-off profit for consultancy fees, for a company that was shortly afterwards acquired. The commercial substance of that accounting entry seems to me, to have one purpose only - to boost reported profits.

Bear raid - an interesting shorting dossier was published early this year. It contained some interesting points, but like all such dossiers, was intended to rattle investors, inducing them to sell, so that the short seller(s) could close their positions at a profit. Therefore all such dossiers have to be viewed in such a light - i.e. as hatchet job, not fair & balanced commentary.

My opinion - if I don't trust the numbers (and therefore management), I don't invest.

This last paragraph today is interesting;

The Board is currently involved in a review of the Group's internal and corporate governance structures. This review follows the substantial growth in the size and scale of the Group's activities since IPO in 2015. The Board will update shareholders on progress in due course."

This begs the question that, if I don't trust management, why would I want them to conduct or even oversee a review?

This one's definitely not for me. I'm happy to be proven wrong on it, but experience has taught me that if the numbers just don't look right to me, then keeping clear is usually the right decision, in the long run.

Thanks for dropping by! I'll leave it there for today. There are updates from a couple of tiddlers, but they're too small for me to cover here.

See you tomorrow.

Best wishes, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.