Good morning, it's Paul here.

Apologies for last week's poor service from me. Let's get this show back on the road.

Learning Technologies (LON:LTG)

Share price: 93.8p (pre market open)

No. shares: 667.8m

Market cap: £626.4m

Learning Technologies Group plc, provider of services and technologies for digital learning and talent management, announces the following trading update for the six months to 30 June 2019.

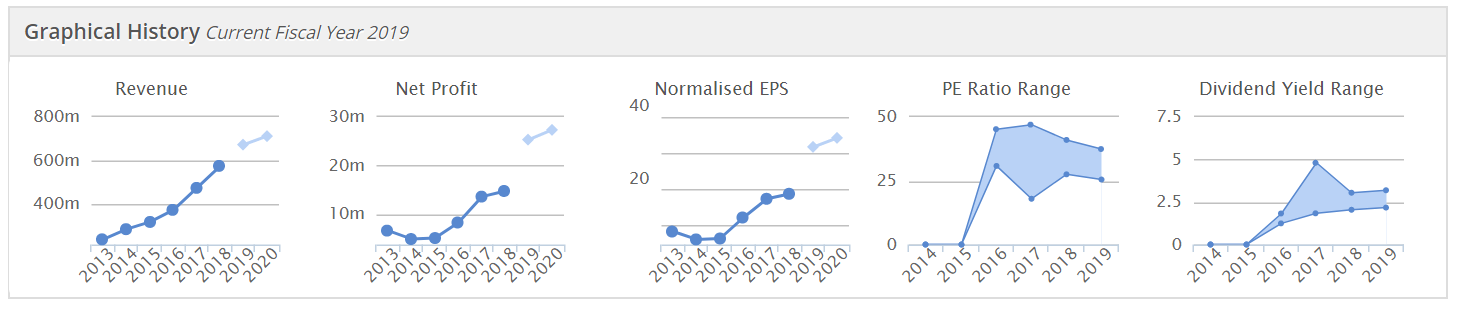

This acquisitive group was the subject of a shorting dossier c. Feb 2019. I've checked through the archive here, and can only find a brief mention from me here on 12 Feb 2019 saying that I thought the shorting dossier looked weak. I can remember printing it off, and struggling to read it by candlelight, in a rather dark local Italian restaurant! The crux of the shorting dossier was that the operating margin looked too high, and was likely to fall.

How wrong that looks today. There's a cracking update out today;

For the first half of the year, the Board expects Group revenues to be approximately £62.5 million (H1 2018: £33.8 million), an increase of c.85%.

Adjusted EBIT is anticipated to be ahead of expectations at not less than £20.0 million for the first half of 2019 (H1 2018: £8.9 million), representing an EBIT increase of c.125% and EBIT margin increase from 26.3% to c.32.0%.

The Board is confident that full-year adjusted EBIT will be materially ahead of current market expectations.

That seems to have comprehensively blown the shorters out of the water!

More detail is given, with one point about net debt of £13.9m looking modest.

My opinion - I actually bought some of this share, after the shorting attack had pushed the price down, as it looked good value. What a pity I didn't hang on to them, as the price is up about 50% since then (in 6 months).

The PER is currently about 23, but with forecasts now bound to increase, that should fall back somewhat (maybe to about 20?). Not cheap on a value basis, but a not unreasonable price to pay for a growth company that is exceeding expectations.

The operating profit margin of 32% is exceptionally high. Is that sustainable long term?

I imagine the share is likely to rise again today, perhaps 100p+ is on the cards? Well done to holders, for ignoring the background noise of a weak shorting attack. I think shorting dossiers are useful when they expose dodgy accounts, etc. However, in this case the shorting attack appears to have been ill-considered, and ultimately just wrong. So far from helpful.

EDIT at 09:37 - the share price has risen 19% this morning, to just over 111p. I wonder if this might partly be short sellers being forced to close out, having got it wrong? You can track short positions on various websites, but I'm not sure that is accurate, as it probably won't include shorts & longs netted off against each other within the spread betting companies' books.

Midwich (LON:MIDW)

Share price: 550p (pre market open)

No. shares: 80.0m

Market cap: £440m

Midwich Group (AIM: MIDW), a specialist audio visual distributor to the trade market with operations across the UK and Ireland, Continental Europe and Asia Pacific, is today providing a trading update for the six months ended 30 June 2019.

This reads positively, but the last sentence is the most important;

The Board's expectation of the Group's performance for the current full year remains unchanged.

Therefore this update should reassure shareholders, but doesn't justify any share price increase, as it's only in line with expectations. Although I note that the share price has been drifting lately, so sometimes an in line update can be enough to stem the flow of selling, who knows?

My opinion - neutral. Distribution businesses don't normally interest me, because they are so reliant on supplier relationships. It's the manufacturers which own the IP, and the risk is that in the internet age, they might decide to sell direct, cutting out the distributors.

Look at how software has gone down that route, so why not hardware as well?

Reviewing Midwich's StockReport here, I can see that the revenue growth has been impressive in recent years (from acquisitions presumably), and with greater scale would come more buying power from manufacturers. The operating profit margin is quite low, which might explain why manufacturers are happy to sell through this distributor?

Note from the Stockopedia graphs below, that the PER has been very high since listing in May 2016. That has since come down to a more reasonable level, currently 17.3, based on consensus forecast for 2019.

The 3% dividend yield is worth having, and is growing modestly, at about 5% p.a..

Looking at Midwich's website, it seems to be a trade only distributor, and the items are quite high value. So maybe having a distributor as intermediary might make sense in this sector? e.g. having premises with product demonstration rooms, could add value.

Where are we in the economic cycle? It's increasingly looking as if we might be entering an economic slowdown, not just in the UK, but elsewhere. Therefore, I'm not convinced this is a good time to be buying any shares which are subject to cyclical fluctuations in demand.

I've checked the last balance sheet, as of 31 Dec 2018, and it looks OK. The key things to check for acquisitive groups, are excessive bank borrowings, and deferred consideration liabilities (for previous acquisitions). In this case, both look OK to me. Although a more recent acquisition announced in Feb 2019, does involve a significant increase in deferred consideration liabilities, so the next balance sheet as of June 2019 is likely to have deteriorated somewhat.

Overall, it looks an OK business, but I can't get excited about this share, and it looks priced probably about right - so why buy or hold them?

On the other hand, the EPS growth in recent years has been superb. Buying up other distributors (and extending its international scope, as with the recent acquisition in Italy), without taking on excessive debt, looks a good strategy.

I can't really make up my mind on this one, so will just say I'm neutral on it.

Tristel (LON:TSTL)

Share price: 300p (unchanged today, at 10:01)

No. shares: 44.6m

Market cap: £133.8m

Tristel plc (AIM: TSTL), the manufacturer of infection prevention products, provides a trading update for the year ended 30 June 2019.

No surprises here, it's an in line update;

The Company confirms that results will be in line with market expectations and it expects to report turnover of £26m (2018: £22.2m), with pre-tax profit (before share-based payments) of at least £5.5m (2018: £4.7m).

Revenue from overseas markets increased by 26% and contributed 55% of total revenues - a record level (2018: 51%). Revenue in the UK rose by 9%. Sales of products using the Company's core chlorine dioxide technology grew by 22% compared to non-core products which decreased by 5%.

Cash - fell to £4.2m (£6.7m a year earlier), but that's fine because it is after spending £4.9m acquiring its 3 distributors in W.Europe. I presume that these acquisitions are likely to have contributed to at least some of the increase in revenues & profits, although the split between organic & acquisitions is not stated.

Balance sheet is strong, with the company being prudently financed (no interest bearing debt). Even after acquisitions made in H1, the balance sheet still looks fine to me - I've just reviewed it as at 31 Dec 2018.

Cashflow - again looks good. The profits look real, not inflated with accounting trickery. Although as CAKE showed us, you can never be 100% sure with any company's accounts. That's a general point, I certainly don't see anything untoward in TSTL's accounts.

Acquisition - another small acquisition is announced, of its distributor in Italy. This does make me wonder why Tristel doesn't seem to be able to sell much through distributors? Maybe the products are too niche? Selling in multiple countries, and achieving global sales of only £25m, does rather suggest either that the company isn't doing particularly well in selling, or that maybe there isn't a mass market for its products? There again, it makes a decent profit margin, so niche isn't necessarily a bad thing.

USA market approval - this has been dangling, like a particularly large & attractive carrot, in front of TSTL shareholders for some time. Today's update doesn't give any information on timing (probably wisely, as it's out of their hands);

...This includes progressing the submission to the USA FDA for pre-market approval of Tristel's Duo high-level disinfectant under the De Novo pathway. At the suggestion of the FDA, a Usability and Human Factors pilot study has been completed and their review is awaited before progressing further with the remainder of the submission.

It doesn't sound as if FDA approval is likely to happen in the short term, but who knows?

I also note that in April 2019, regulatory approval in China & S.Korea was announced.

Shareholder open day - is being held tomorrow, a nice idea, which this company has done for several years now. Although a cynic might suggest that the £multi-million Director selling in recent years is a good reason why they might want to drum up buying interest in the shares. Significant Director selling certainly makes me cautious. If the upside potential really is huge, then why would they be substantial sellers?

Outlook comments sound positive:

Paul Swinney, CEO of Tristel plc, comments: "We are very pleased with the performance of the Company during the year. The balance of our business continues not only to shift towards our higher growth overseas markets, but also towards our higher margin chlorine dioxide technology."

My opinion - it's a solid update today. The company seems to operate in a nicely profitable niche. I can't see any funnies in its accounts, and it's prudently financed. When USA approvals come through, that could give the shares a boost - although maybe this is already factored into the price?

On the downside, the big Director sales worry me. Also, the company seems to be struggling to gain much traction in multiple markets. Buying its own distributors suggests to me that the product doesn't sell itself. Sales seem rather low, considering it operates in multiple countries. Maybe this company needs to be part of a bigger group, with a much larger sales & marketing setup?

Overall, I'm neutral on it. I could see this share going higher, if it is able to really scale up sales, from the current not madly exciting growth. Existing operations are decently profitable, so that should underpin the downside somewhat.

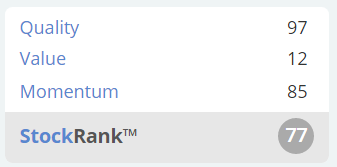

The StockRank neatly sums it up - high quality, but expensive;

Judges Scientific (LON:JDG)

Share price: 3540p (down 1.1% today, at market close)

No. shares: 6.2m

Market cap: £219.5m

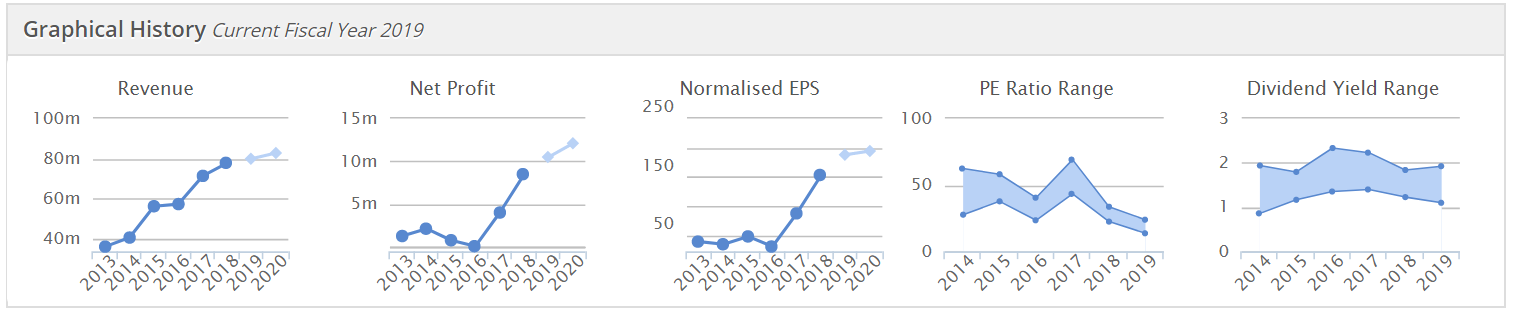

The Directors of Judges Scientific (AIM: JDG), a group engaged in the buy and build of scientific instrument businesses, update shareholders and the market regarding the Group's trading performance for the six month period ended 30 June 2019.

Introduction - this share is popular with private investors, and I can see why. It seems to be one of the few buy & build type of acquisitive groups that has stood the test of time. The key to success here seems to be down to 3 things;

- Excellent management - who don't seem to have put a foot wrong,

- Buying cheap, but decently profitable small businesses, to create a group which looks like a growth company, and is therefore awarded a much higher PER than the companies it buys.

- Using cashflow to pay for cheap acquisitions, thus largely avoiding bank debt & dilution from fundraisings.

This strategy has worked an absolute treat.

Trading update - sounds solid;

The strong sales performance throughout the Group and continued positive influence of exchange rates have helped to deliver a sound performance and the Board expects the interim results to show strong progress in revenues, EBIT and earnings per share.

Outlook - sounds like it's in line with expectations, maybe with scope to exceed?

The Group has enjoyed a good first half, partially helped by consumption of some of the order book; the outlook for the year remains positive and the Board is confident that market expectations for the year will be achieved.

Order book - has reduced, but this doesn't seem to have spooked the market;

On 30 June 2019, the order book stood at 13.2 weeks of sales against 14.4 weeks at the start of 2019 and 15.0 weeks at 30 June 2018.

Valuation - looking at the usual Stockopedia summary graphs below, you can see that the EPS growth (3rd graph) has been stunning since 2016. Hence why the share price has soared. That this has been achieved with only a small increase in share count, and little bank debt, whilst also paying rising divis, is extraordinary.

It's currently priced at about 19 times forecast earnings for FY 12/2019, which doesn't strike me as particularly expensive, given the terrific track record above. Remember that the group is largely debt-free as well, which makes a PER of 19 a lot more palatable.

My opinion - what has been achieved here is very impressive. Obviously I cannot predict what will happen in the future.

If you think that the group can continue making excellent acquisitions, and thereby driving up earnings growth (plus quite good organic growth), then this share could be worth a closer look. Given the outstanding track record, especially since 2017, I certainly wouldn't want to bet against this share.

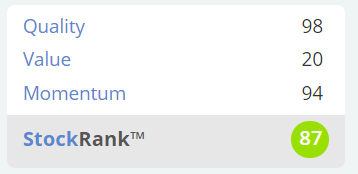

Neatly summarised by the StockRank system - high quality, with strong momentum, but not cheap (with such a good track record, I wouldn't expect it to be cheap):

Appointment of Liberum as Joint Broker - this can sometimes be a precursor to some kind of deal - maybe a fundraising for a large acquisition? Or a placing of existing or new shares? Who knows. I'm just flagging it as an additional announcement today.

That's all for today.

Regards, Paul.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.