Good morning! It's Paul & Graham with you today. Today's report is now finished, and I'm off to visit my nearest CakeBox store, to mystery shop it!

Agenda -

Paul's Section:

Warpaint London (LON:W7L) £97m) - a positive H1 update from this make up company. It's coping well with inflationary pressures, actually increasing gross margins. Sales also up strongly. Looking good. With a strong balance sheet, generous (and growing divis) plus positive trading, and all at a reasonable valuation, this share gets a thumbs up from me.

Cake Box Holdings (LON:CBOX) (£74m) - sparkling results for this franchise cake business. Due to previous accounting issues, I've had a good rummage through the accounts, and flag up a few minor queries. Also, note that over half profits seem to come from selling new franchises, which are one-offs. So to maintain profits, expansion has to continue. Overall, I think the positives possibly now outweigh the negative, so it's looking tempting.

Caretech Holdings (LON:CTH) - a recommended takeover bid at 750p, with the founders buying it back. Recommended, and looks likely to go through.

Hyve (LON:HYVE) - this international trade show events group makes positive noises about recovery in today's trading update. However, on closer inspection the finances are very weak, with a hideous balance sheet, and problem debt - which has come down a lot, but refinancing discussions are still unresolved, so I suspect continued bank support might require more dilution from an equity raise. Risk:reward looks bad to me.

Graham's Section:

Ingenta (LON:ING) (£13m) - this small software company releases results for FY December 2021. The stock has some “value” features including a dividend, a well-aligned Chairman, and increasing profits. It also has a StockRank of 79. The company is attempting to diversify both its product set and the sectors it serves. The stock has been listed for over 20 years and readers may wonder if the company’s optimism is well-founded, or if this is just another false dawn for the stock.

Northern Bear (LON:NTBR) (£11m) - this building services company announces a trading update for FY March 2022. Adjusted profits have rebounded (and hopefully the adjustments won’t be too large). A new Chairman is looking to shake things up, with larger acquisitions and other possibilities on the cards. This is a “Super Stock” which may continue to attract value investors who can look past the unpredictable nature of the sector, especially now that there is a potential catalyst in the form of the Chairman.

Begbies Traynor (LON:BEG) (£236m) - [no section below] - this professional services company is known to be an insolvency specialist, but it has its fingers in many pies now across a range of activities. Today it announces the £2.4m purchase of a firm of chartered surveyors (including contingent consideration and cash earn-out). This will integrate with Eddisons, the property services division of Begbies.

Begbies shares have done very well in anticipation of increased insolvencies and its own successful integration of acquired business. Adjusted PBT for FY April 2022 is expected to be £17.8m (up 55%). The company is now priced at more than twice forecast sales, so perhaps the valuation will soon reach a ceiling?

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Warpaint London (LON:W7L)

126p (up 12% at 08:22)

Market cap £97m

Trading Update (AGM)

I have a generally favourable impression of this make up company. Although looking at the chart, the share price is not that much higher than the 97p placing price when it floated on AIM in Nov 2016.

Although divis have been generous over the last 5 years, totalling 20.3p, so if we add that to the current share price, the total shareholder return would be 146.3p, which is a 51% gain on the listing price - not too shabby actually. Wouldn’t it be great to have a share price chart that also included cumulative divis too? That’s top of my wish list for a new feature here!

Plus, the business now is considerably bigger than it was 5 years ago, so the shares are better value for money now, compared with when it listed.

I’m looking back at my previous notes here on 1 Feb 2022, when W7L issued a positive (ahead of market expectations) full year trading update for FY 12/2021, together with a positive outlook comment, indicating a good start to the new year FY 12/2022. Although I baulked at the valuation at 165p per share, with the PER into the twenties, which seemed too high at the time.

It’s usefully cheaper now, so do the shares appeal after today’s update? Clearly the market likes it, with the price up 12% as I type this.

Warpaint London plc (AIM: W7L), the specialist supplier of colour cosmetics and owner of the W7 and Technic brands…

Strong trading in 2022 to date - H1 sales ahead of the Board’s expectations at the start of the year - but note that market expectations have been raised since then, so it’s not clear if this is upgrading full year market expectations or not - I’ll have to see what the brokers say (as they’re steered by the company usually).

H1 2022 sales expected to be >£24m (up 30% on LY - this is also a similar uplift on the pre-pandemic H1 sales, which were c.£18-19m in both 2018 & 2019, as you can see here on this very useful table.

UK: strong growth.

Europe: particularly strong growth - interesting, I wonder what’s driving that?

Other regions: performing in line with mgt expectations.

Gross margin is up on 2021, despite inflationary headwinds for input, and transport costs - that is good news - pricing power is a key factor right now, so this is strongly positive, suggesting W7L has been able to pass on price rises without putting off customers, although that’s not explicitly stated, rather implied.

H2 weighting for 2022 expected, as in previous years - I’ve confirmed that on our useful table here, with both 2018 & 2019 seeing a split of around 18:30 in H1:H2 revenues, so that’s actually a strong H2 seasonality - driven by Christmas sales.

Final divi of 3.5p confirmed (up from 3.0p last year) - giving an expected 6.0p relating to FY 12/2021, a healthy, and growing yield of 4.8%.

Balance sheet - nothing is said today, e.g. about cash, but I’m checking all balance sheets anyway, for every company, given tough macro conditions. W7L is excellent - very healthy, with net cash and a very strong working capital position, so the finances are safe, and divi paying capacity is good.

Strong order book, ahead of last year (no figures provided)

Outlook (from the Chairman, Clive Garston) -

I am confident that the Group will continue to perform well for the remainder of the year.

Broker updates - we’re spoiled for choice, with both Singers and Shore publishing updates on Research Tree - very useful, thanks to both. I like to acknowledge brokers which help the private investor community by letting us access research. In my view, it’s a great shame that other brokers deny us their research notes, despite them having privileged access to the company, but then restricting research notes based on that (effectively inside information/guidance) to their favoured clients only - highly questionable, and obviously unfair, in my opinion.

Looking at Singers note, it’s only pencilled in an £8.0m rise in revenues for FY 12/2022, despite the company already having achieved a £5.6m uplift in H1. Therefore the target looks beatable, which is acknowledged in the commentary. Softish broker forecasts are essential right now before investing, in my view, as that should hopefully minimise the risk of a profit warning wiping 30% off the share price at some random point in future.

Hence I reckon the 8.1p EPS forecast for this year might turn out to be nearer 9-10p if growth continues, which it sounds like it’s likely to do, given upbeat outlook & strong order book.

EDIT: I see Shore is estimating 8.8p EPS for this year, which looks more realistic to me. End of edit.

Valuation - at 126p per share, with 9-10 EPS looking realistic, then the current year PER would be 12.6 to 14.0 - which looks pretty good to me, given that the company is growing strongly, despite tough macro conditions.

It mentions that the value for money product offer is appealing to customers.

My opinion - the valuation has come down a lot, despite improving fundamentals, and this share now looks a lot more appealing as a result.

It’s an excellent income share too, with generous & growing divis - very important, to help reduce the erosion of inflation on our investments, and giving a flow of cash whilst we wait for stock markets to recover at whatever point that happens, currently unknown!

I’m pleasantly surprised with the strength of current trading, and reassured that it’s coping with increased costs and clearly passing that on to customers, given stronger gross margins.

In current market conditions, I’m being generally a lot more sceptical, but W7L comes through with shining colours, trading well, and at an attractive valuation, hence it gets the coveted SCVR thumbs up! As always, this is never a recommendation, but it could be seen as a green light for readers to go on to do your own research. there's a decent StockRank (currently 73) to reassure that it's not a dud.

Thinking about downsides, I suppose there must be some fashion risk with make up, as companies in this sector do need to keep launching new ranges, which may or may not appeal to customers. Although there are also continuity products, which customers repeat buy, so the split of that would be a good question to ask management - hopefully they’ll do webinars - I recall watching a webinar before, but can’t remember which platform it was on. Management struck me positively, seeming to be hands on, down to earth entrepreneurs, which is what I look for in small caps.]

As an aside, management showed impeccable timing, with 2 Directors banking £2.9m each right at the all time high, in Oct 2018. Although they've not sold any shares since, and retain very large stakes (just over 50% combined). So I would watch carefully for any further, large Director sells, and bear in mind that they're very shrewd, so for me big Director selling after a strong share price move up, would be a sell signal for PIs too.

.

.

Cake Box Holdings (LON:CBOX)

184p (up 10% at 10:40)

Market cap £74m

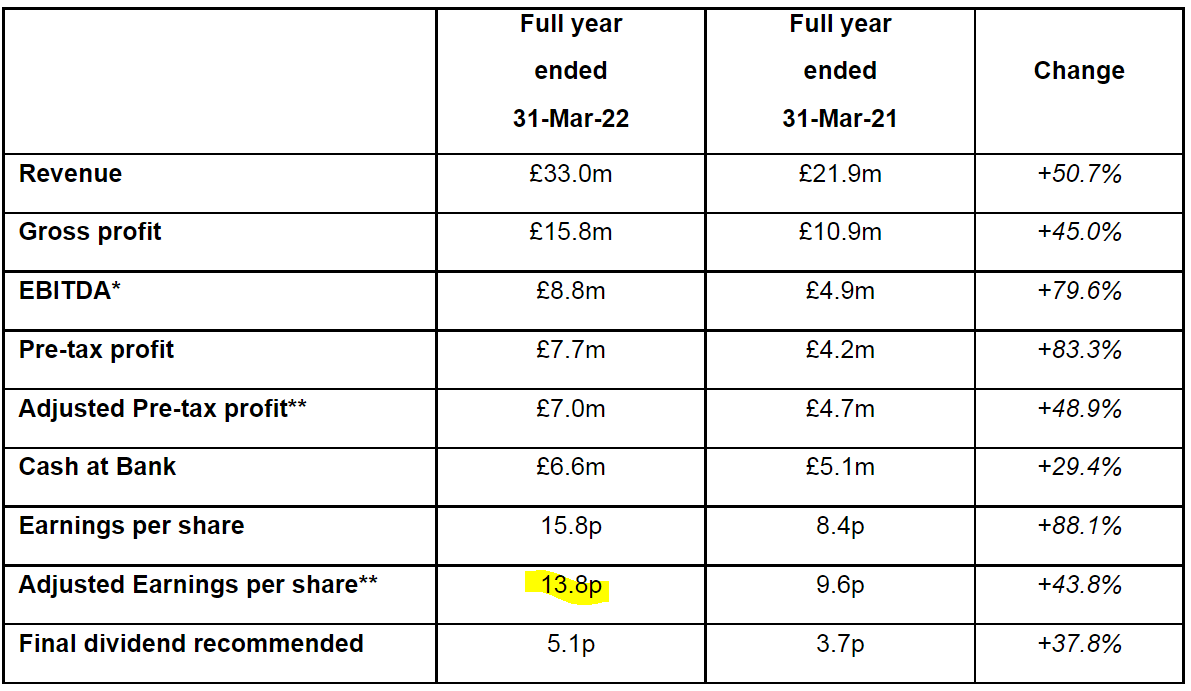

Cake Box Holdings plc, the specialist retailer of fresh cream cakes, today announces its audited full year results for the twelve months ended 31 March 2022.

PR headline -

Strong results and robust current trading, confident of further progress

Fantastic figures here, as you can see -

.

Valuation - that’s a PER of only 13.3, which is low for a rapidly expanding, and decently profitable franchise business (hence low revenues, but high margin, because the shop sales don’t go through CBOX’s accounts, because shops are operated by franchisees).

Adjustments to profit actually reduce profit, which is unusual! This relates to one-off gains from releasing provisions, and a credit due to share options lapsing. So the adjusted numbers look reliable.

Dividends - are up, total for the year is 7.6p - a yield of 4.1% - and the divis are rising rapidly too.

Current trading - covers Q1 of FY 3/2023 - sounds good -

Freehold property revaluations - I like revaluations of freeholds, providing the valuations are realistic, as that shows the current value of properties. Many companies opt for historic cost, which can lead to assets being undervalued on the balance sheet. Others may disagree, but it's good to have both disclosed, as happens here.

The commentary says its HQ was revalued upwards by £2.5m, but a gain of only half that is shown on the comprehensive income statement (note 13 seems to suggest that the other half was booked in the restated prior year figures) - i.e. it by-passes the profit & loss account, so profit, EPS, etc are not boosted by property revaluation, only the balance sheet is. That’s fine, and it’s transparently done (debit freehold property assets, credit revaluation reserve, both balance sheet entries). See note 13 for more details.

Freehold property is now on the balance sheet at £8.7m, with mortgages totaling £1.4m. I am a huge fan of freehold property - it de-risks investments very well, and gives long-term asset value increases. I don’t care about freehold property suppressing some quality measures, that’s a red herring in my opinion. Especially in a potential downturn, investors need to focus on bulletproof balance sheets, stuffed with cash & freeholds, to reduce risk, in my opinion.

I’ve gone through all the notes to the accounts, for closer scrutiny, given the accounting problems unearthed by Maynard Paton in Jan 2022 - by far the most serious was the auditor resignation, which condemned CBOX’s financial controls, and dishonesty/incompetence (e.g. not disclosing a cyber security incident) of the former CFO.

Note 7 - staff costs - why does CBOX have 17 maintenance staff? Seems odd, because the stores are franchised, so surely the franchisees would look after maintenance? So this would be a good question for the webinar - and are any of these staff relations of the Directors? I can’t understand why this business would need 17 maintenance staff. Oh, maybe it includes cleaners for the production facilities? That’s possible.

Travel & entertaining costs (note 4) of £372k seems odd, and high - in admin exps (see note 4) - again, worth querying.

Sale of franchise packages - generated £3.8m (note 3). This is the first time I’ve seen the disclosure of fees generated from selling new franchises. This is a highly material figure, as it’s likely to be largely profit.

Given that adjusted profit before tax is £7.0m, then it seems 54% of total profit comes from expansion - selling new franchises. So for profit just to stand still, it has to keep selling the same number of franchises each year. Although ongoing fees would grow with each new store. The danger is that expansion could slow down or stop, which would cause profits to roughly halve.

On the positive side, it’s good to see an income stream of £938k described as online sales commission.

My opinion - these numbers look superb, and it’s very tempting to throw caution to the wind over the previous accounting problems, and just buy this share on the basis it’s too cheap, for a rapid roll-out of an obviously successful format.

Although I wouldn’t get too carried away with the PER, because half of the profits come from selling new franchises, which is not necessarily a permanent income stream.

Even so, I could see say possible 50% upside on the share price, if the market gets over the accounting issues and begins to trust management again. They do seem to be putting the house in order, but you never know how deep problems like this go, in terms of the culture of the whole business.

The other issue I’ve mentioned before, is that the big shareholders were practically all selling. So that could mean a big, and long-term overhang, suppressing the share price, possibly.

We also have to consider that small cap fund managers are likely to now be getting client redemptions, because many investors tend to take money out after market downturns (which is arguably the opposite of what makes sense!). So fund managers may become forced sellers in small caps, if markets remain in the doldrums. What do they sell? Low conviction, and problematic shares, which could include CBOX maybe? We don’t know though, but watching the “Holding in company” announcements from CBOX is particularly important.

Overall, I’m very tempted to buy a small position here, but am aware of the risks, hence important I think not to over-size it.

.

.

Caretech Holdings (LON:CTH)

739p (up 21% at 11:34)

Market cap £838m

Takeover bids are still happening, which I see as bullish. Note how a lot of them have been software companies, and companies providing some sort of infrastructure services (e.g. Menzies), with buyers often being overseas (especially USA).

This deal has been agreed by Caretech’s Directors, it’s a 750p cash bid, a premium of about 21% - not overly generous, but it’s just about an all-time high, so I don’t think anyone can complain.

Caretech has been in an offer period since March, so that also explains why the bid premium isn’t huge, as it would have been partly in the price already.

It looks as if a consortium has been formed by the founders, so they’re buying it back, funded by lots of debt.

So far it has indications of acceptance from 38.5% - not a certainty that it will go ahead, but it seems fairly likely to do so.

Given uncertainty in the markets, I think it probably makes sense to bank the profits now at 739p, rather than hang on for the last remaining 11p - because bids are more likely to fail in a bear market, maybe? But that’s a decision every investor has to make for themselves. It’s not binary either - sometimes I sell half in the market, and run the balance to competition of the takeover.

This is certainly an unusually positive chart at the moment -

.

Hyve (LON:HYVE)

71.5p (up 5% at 12:14)

Market cap £209m

Hyve Group plc, the next-generation global events business, today announces a trading update for the period from 1 April to 24 June 2022.

PR headline -

Faster than anticipated recovery continues

Improved net debt position

Running in-person trade shows has obviously been a horrible area during the pandemic. However, HYVE has received substantial insurance payouts re cancelled events, and it’s managed to survive this far, so it could now be a recovery situation.

It gives a positive update today, on recovering bookings. It’s not simple to work out how the business is likely to perform in future, because performance pre-pandemic was erratic, and there’s been a lot of restructuring since.

The disposal of its Russian business for example received very little cash up-front, and proceeds will mainly be 10-years of earn-outs. Hmmm, let’s see how much of that is actually received in cash from Russia. It’s probably safest to assume zero!

There are continuing lockdown-related problems in China, affecting HYVE.

Net debt has come down nicely, to £53m, but the balance sheet overall is a car crash - when last reported, NTAV was negative £(139.6)m, so it clearly needs refinancing with fresh equity. Therefore I wouldn’t go near this, until it’s properly fixed the balance sheet.

Although the business model receives fees up-front, so it probably could run with negative working capital, but not this much.

Although with a market cap of just over £200m, if it were to do a (say) £40m equity fundraise at the behest of the banks, then that might be 20% dilution, which is a fair bit, but not ruinous. However, fund managers can name the price, especially in hard times, so they might insist on a deep discount. It’s such a big risk, and one I wouldn’t want to take. Why invest in any company with wobbly finances, given macro problems?

I can’t find any broker research either, which doesn’t help.

Looking back at the interims, there are alarm bells over balance sheet weakness, but also in the going concern statement, which talks about possible bank covenant breaches & waivers, and that the company is trying to refinance its bank facilities.

Today it says this about refinancing the bank facilities -

The refinancing process is in progress, with the Group in discussions with existing and prospective lenders.

My opinion - until it sorts out the balance sheet, with fresh equity, possibly as part of a deal to renew the bank borrowings, then I would treat this as too risky, and best avoided.

It’s not even cheap. On current broker consensus forecasts, there’s minimal profitability this year FY 9/2022, and the PER for next year is 29.5 - that’s very high for a company with a desperately weak balance sheet. Hence anyone buying or holding this share would need to be very confident it’s going to thrash forecasts, and successfully refinance. Hence for me, risk:reward looks very poor.

On the upside, in-person events look to be coming back, and maybe HYVE could be valued on a sum-of-the-parts basis for each show?

Note the share count has shot up from 75m in 2017, to 292m now. So that's a huge headwind for the share price, meaning previous highs are now unlikely to be recovered.

Graham’s Section:

Ingenta (LON:ING)

- Share price: 84.90p

- Market cap: £14m

This is a small software company that serves the publishing industry.

It has been knocking around AIM for a long time, by the standards of the junior market. It first listed by means of a reverse acquisition in April 2000.

Profitability has been sporadic over the years, and you can see yourself from the market cap that the company is still deep in micro-cap territory.

Today’s results are for FY December 2021, and are as follows:

· Revenues down slightly to £10.1m, “reflecting a focus on core software offerings”.

· Net profit of £1.8m (up from £0.4), but this includes a £1.2m tax credit. So net profit of £0.6m, excluding the tax credit.

· Good cash flow from operations (£2.0m), helped by working capital movements. The company’s cash balance improves from £2.3m to £3.0m.

As this is a small company with business customers, contract wins and “go-lives” are measured in the single digits. Ingenta saw four customers going live during the year: three on a web publishing platform called “Edify” and one on a music public platform called “Conchord”.

Current trading – since the results shown are for the period that ended nearly six months ago (!), shareholders will be more interested in a report for the current period.

The current year is said to be “strong”, with “growth in revenues and profit over the prior period”. This is said to be “driven by existing customer base with extended sales cycles persisting for sales to new customers”.

How would you feel, as a shareholder, if your company was only very slowly finding new clients, but was deepening its relationship with existing clients? My view is that this is ok, particularly in a difficult economic environment.

In a tough economy, it makes sense that sales cycles would be longer. But if the existing customer base is happy with the products, and wants to buy more of them, then that says a lot for customer satisfaction!

Anyway, results for the current year are tracking ”comfortably in line with market expectations”.

Company strategy – Ingenta wants to broaden the scope of the markets it sells into, beyond its traditional IP management for publishers. The contract win in music publishing is its first success from this growth strategy, whereby it can serve new customers from a wide range of industries.

Two of its new web publishing customers were NGOs, which is a step forward in this customer diversification plan.

While some of Ingenta’s revenues are non-recurring in nature, it wants to focus growth efforts on recurring revenues where possible, i.e. “Software-as-a-Service”.

Dividend – this company is a dividend payer, and proposes an increased dividend of 2p for the year, giving a yield of c. 2.4%.

Outlook – confident:

With our newly established operating fundamentals firmly in place and generating returns, the Group can look forward with optimism to the next stage of its development - generating revenue growth and leveraging our expertise in the wider IP management arena.

My view

I’ve not studied this one before, but have done some groundwork this morning which will enable me to comment on it in future, should it start to pick up some momentum.

While the growth aspirations are commendable, the lack of sales growth in 2021 is noteworthy. An interim report should be out in September (judging by last year’s release dates), and hopefully this will prove that 2022 is more positive.

The 2021 numbers do show an improvement in margins and good control over operating expenses, and hopefully that will continue.

Some other positives:

· The Chairman is the largest shareholder, so alignment with external shareholders should be very good.

· A nice recent history of dividends, and I appreciate the company’s move to buy back some shares.

· KPI metrics used by the company include a focus on cash flow.

· Stockopedia calculations have also noticed the numerical attractiveness, and have given the company a StockRank of 79.

The only major negative, from my perspective, is that the company has been around for so long and has presumably had many false dawns in the past, all under the current Chairman.

I think it will be worth our while continuing to monitor this one.

.

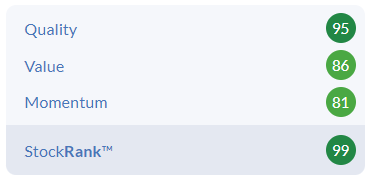

Northern Bear (LON:NTBR)

· Share price: 58p (-4%)

· Market cap: £11m

This building services company tends to offer a cheap multiple against prospective earnings. It’s in a tricky sector – things can go wrong (e.g. bad weather!), it’s labour-intensive, and of course highly competitive.

Services provided by the company include construction, roofing, electrical installation, fire protection, etc.

In FY March 2021, Covid was the big problem, although the company also mentioned “uncertainty surrounding Brexit” and supply chain issues. Northern Bear reported an operating loss for the year, after it took a big impairment at a commercial interiors subsidiary.

If interested, you can find a list of Northern Bear’s subsidiaries here.

The company will release FY March 2022 results soon, and this is the main subject of today’s trading update.

Despite ongoing supply chain/inflation problems, we learn that the second half of the year has gone well:

..the Group has generated strong operating results that continue to exceed those from the prior year to 31 March 2021 ("FY21"), as well as those from the comparable pre-pandemic year to 31 March 2020 ("FY20").

The Board's current expectation, subject to audit finalisation, is that operating profit for FY22, stated before amortisation, one-off costs and other adjustments (in the format used in prior years' results), will be in the range of £2.5 million to £2.6 million.

The adjusted profit figure was £1.4 million in 2021, and £2.2 million in 2020.

So FY March 2022 is shaping up to be a nice improvement over both prior years.

Cash at year-end was £2.2 million, although the company acknowledges that this is a seasonal high. The company has been using its £1 million overdraft and up to £500k from an RCF.

That’s another complication in this sector: huge cash swings, as large lumpy payments come and go. But Northern Bear’s headroom, given the presence of the overdraft and a £3.5m RCF, seems comfortable.

Strategy – under the leadership of a new Chairman, the company has recently considered two acquisitions “of a more substantial size than those we have made previously,” though neither of them came to anything. Interesting stuff!

The new Chairman (since 2021) is a Toronto-based investor who first got involved with the company in 2019. He currently has a 25% stake and doubtless has ideas about how to drive shareholder value – watch this space.

My view – if it hadn’t been for Covid-related issues, this company may have proven that the low rating attached to its shares was just far too cheap.

However, the same might be said of many companies! The fact is that the Covid disaster did happen, that Northern Bear was exposed to its consequences, and that the company continues to be exposed to the supply chain and inflation issues that have flowed from it.

But despite these trying circumstances, the company is now performing well again, and it has a Chairman and major shareholder who will bring a new perspective on how to unlock value for shareholders.

It would be remiss of me not to mention that this is a Super Stock, with a StockRank of 99:

So whether as part of a diversified StockRank-based portfolio, or as a speculation on what the new Chairman might achieve, or simply as an investment in a company that is cheap relative to potential earnings, there is a lot to be said for this one. Worth researching.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.