Good morning from Paul & Graham!

Agenda

Paul's Section:

Hotel Chocolat (LON:HOTC) - preliminary results for FY 6/2022, suggest the accounts department operates at a leisurely pace, but the figures are in line. Outlook comments are vague, but seem to be a mild profit warning. Balance sheet seems OK, although inventories running high does introduce some risk of future write-downs. Overall, I'm struggling to see value here. Aggressive forecasts for next year & beyond mean more profit warnings could be a risk. The story seems a little stale.

Creightons (LON:CRL) - I have a quick skim through the H1 results. Profit has almost evaporated, due to high cost inflation, and difficulties passing that on to customers, as with so many manufacturers right now. Outlook comments suggest it's making some progress though, with a better H2 expected. Balance sheet seems just about OK. Over time I think CRL should probably at least partially recover, so maybe one to just tuck away & forget about?

Tribal (LON:TRB) - noteworthy as shares have dropped 30% today, on news of a problem contract getting a lot worse. This means most of this year's profits are wiped out. Tribal has a history of erratic performance. It's difficult to see how a large contract could go so badly wrong. Shares might be attractive to a bidder, perhaps?

Graham's Section:

Peel Hunt (LON:PEEL) (£96m) - these H1 results are poor, as expected, but the company does succeed in achieving a breakeven result despite “multi-decade lows” in equity capital markets activity. The investment banking division saw a collapse in activity with only a handful of IPOs taking place in the UK market and with other fundraising deals only a fraction of what they were last year. The other revenue streams at Peel Hunt were more stable and thanks to a chunky reduction in pay/bonuses, this H1 result looks ok to me. I now think this share could be approaching value territory thanks to the strong balance sheet which includes £41m of cash and a very strong net current assets position.

Mortgage Advice Bureau (Holdings) (LON:MAB1) (£255m) - a profit warning is seen from this mortgage advice business. With the help of a franchise business model, it has earned excellent profits and returns in recent years. However, it is going to “slightly” miss its 2022 forecasts, and we now can’t expect it to make any progress in 2023, due to its having fewer mortgage advisers on its books and lenders imposing stricter criteria on new loans. Mortgage volumes have collapsed and MAB is hoping that this will recover by H2 of next year. I’m not sure when the recovery might happen but my perception is that this stock has some high-quality characteristics and could be a nice candidate for a recovery rally if and when normality resumes.

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

Hotel Chocolat (LON:HOTC)

145p (pre market open)

Market cap £199m

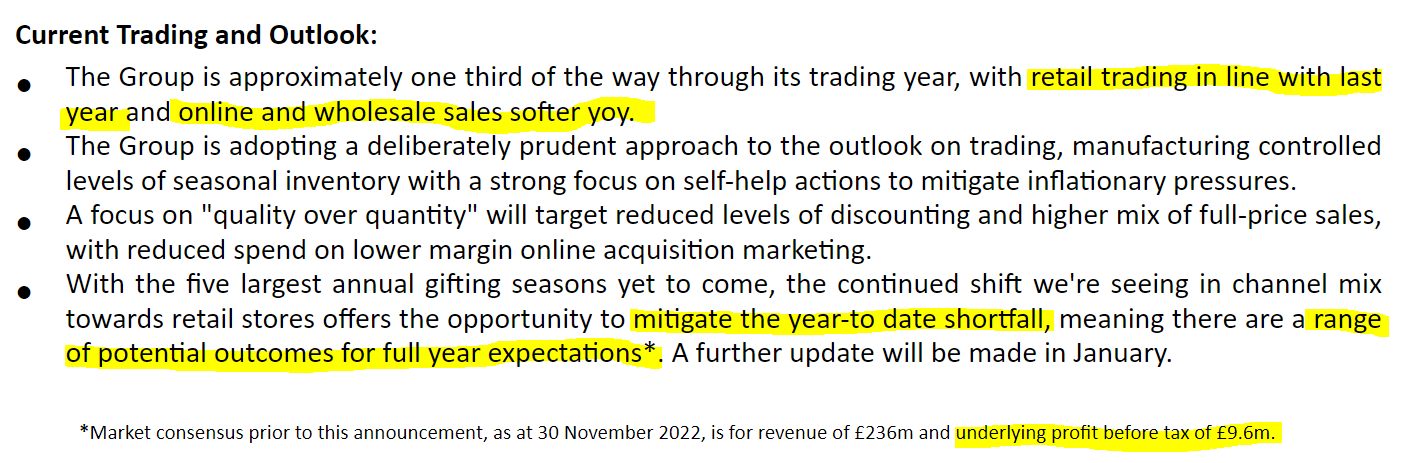

Hotel Chocolat Group plc, a premium British chocolate maker, today announces its preliminary results for the 52 weeks ended 26 June 2022 ("FY22").

It seems late, to be getting FY 6/2022 results, in early December. Also a long time since the last trading update in July. Although it has given us over 4 months to forget about the disastrous international expansion strategy, with the Japan JV being abandoned with heavy losses, and scaled back in the USA. Hence why the shares have rebased downwards, since it’s no longer an exciting international growth story, but instead now a UK-focused brand.

Japan - not a complete write-off it seems, with today’s update saying it is still trading, and may turn into a brand licensing model, which would be good to salvage something from the £30m write-off of previous investment.

FY 6/2022 results look as expected (from the July update) -

Revenue £226m

Underlying PBT £21.7m

Statutory loss of £(9.4)m, as expected due primarily to a big £30m write-off re Japan JV (as expected)

Current year trading/ Outlook - I don’t know about chocolate, this is more like fudge - and sounds like a profit warning to me -

Excess inventories - this is a common problem with many retailers at the moment, as they stocked up when supply chains were stretched, and now need to wind down those excessive inventories.

I am a bit concerned about this, because when inventories become this high, there’s an elevated risk of a write-off being needed for slow-moving items. Also, it would be worth checking the use by dates, to see if any of this is perishable -

Broker update - many thanks for Liberum for a detailed note today. It trims forecast earnings for this year from 5.6p to 4.8p. So over 100p is a high PER. 145p currently looks very difficult to justify.

The progression of forecast profitability looks too aggressive to me, being -

FY 6/2023: £8.3m

FY 6/2024: £20.5m

FY 6/2025: £32.7m

I’d be very surprised if HOTC achieves anything like that profit growth, but time will tell. So it all depends whether you believe in the revised strategy or not.

Management changes - both the Chairman and CFO intend stepping down in 2023, which doesn’t exactly inspire confidence. If they saw exciting growth ahead, would they be leaving?

Going concern note - nothing worrying in this.

Balance sheet - looks OK to me. NTAV was £96.6m at 6/2022. This was boosted by a £40m equity raise in the year.

My opinion - there’s nothing madly exciting in today’s update. So I can’t see any reason to anticipate a big recovery in the shares.

Based on expected performance for the current year, FY 6/2023, the shares look expensive.

Forecasts beyond that look very challenging, given tough macro conditions - I find it difficult to anticipate profit more than doubling in FY 6/2024, hence it seems to me the risk of profit warnings could be high, but we don’t know, it’s all educated guesswork really, trying to predict the future performance of any company.

You either believe in the product/strategy, or you don’t. Personally, I don’t like the product, so would never invest in any consumer product that I find poor value for money, and unappealing in taste. There’s a branch in Islington, so I’ll mystery shop it this afternoon & report back. Do any readers like the product? We should probably do a poll.

There's a danger of investors "anchoring" to previous, excessive share prices.

Also remember the share count has risen from 118m to 137m over the last 3 years.

.

Mystery shop - here is my experience of trying out Hotel Chocolat products in its Islington branch on 1 Dec. The short version - product is OK, average, nothing special, and too expensive. Exactly as I previously thought.

Creightons (LON:CRL)

29p (down 23% at 08:45)

Market cap £20m

Shareholders have had a torrid time with this share over the past year, which continues today with another lurch down.

H1 key numbers are -

H1 revenue down about 1% to £29.7m

Operating profit largely disappeared, to £281k (H1 LY: £2.6m)

Profit after tax becomes a loss of £(385)k vs £2.0m last H1.

What’s gone wrong? It’s all about cost inflation, and struggling to pass this on to customers - a similar story we’re hearing from many manufacturers in lots of sectors. The way I’m thinking about this, is that over time, it should be possible to rebuild margins. That’s what usually happens after previous recessions, but it can take several years. More of a gradual rebuild, than a V-shaped profit recovery, is probably on the cards.

We can look back to 2008 for many examples of this, in company results generally improving over the next few years.

Outlook - it’s expecting an improved performance in H2, and the commentary mentions various initiatives to cut costs, improve efficiency, and cut supplies if customers refuse price rises - although that last one could be problematic if it means losing market share.

Is it going bust? Probably not - the going concern note doesn’t ring any alarm bells, although there is an element of marking their own homework with these notes, although I understand that auditors police them carefully.

In terms of financial strength -

Balance Sheet - NAV is £24.6m. Remove £13.7m intangibles (boosted by an unfortunately-timed series of acquisitions), and I’ll also remove £3.0m deferred tax, to give NTAV of £13.9m, which is probably adequate for the size of business. There’s quite a lot of working capital tied up in receivables and inventories though. Lease liabilities are modest.

Note 5 gives a breakdown of the £9.0m gross bank debt, of which £2.56m is a mortgage, which I usually disregard as it will be secured on freehold property, so that’s safe. Then there’s £4.1m in invoice financing, which looks reasonable compared with £14.5m receivables. So that leaves a fairly modest level of remaining debt. I’d like to see debt reduce, but it doesn’t look dangerous - particularly as the commentary says it has moved back into monthly profitability during H1. So the bank will be looking at an improving picture, hence probably not panicking.

Nothing is said about bank covenants, so that would need more research before considering a purchase of shares.

Dilution - note 3 shows what seems unreasonably high (over 10%) potential dilution from share options, so just a flag to check that out.

My opinion - neutral. I think CRL should be able to rebuild profits, so the question is how much, and how long will that take? If it gets back to historic peak profits, then £20m market cap would be great value. So it seems a credible recovery share, for patient investors, and I don’t see excessive risk here, providing it does turn in an improved H2 performance.

Who knows, at some point raw materials & energy prices could drop heavily, which would be exciting for this, and other companies. Although recent events have shown the flaws in their business models, in the vulnerability to supply & cost shocks.

Tribal (LON:TRB)

40p (down 29% at 09:23)

Market cap £85m

This has cropped up because it’s one of today’s top fallers - we try to cover big price movers every day, up or down, because that tends to be where the most noteworthy things are happening.

NTU Contract Update and Trading Outlook

Tribal (AIM: TRB), a leading provider of software and services to the international education market, today provides an update on the Nanyang Technology University ("NTU") contract and Group trading for the year ending 31 December 2022 ("FY22").

Trading for FY22, excluding the NTU contract, is in line with Board expectations.

NTU contract - sounds like it’s going badly wrong -

Expected to generate a £12m loss over the life of the contract (no specified how long)

Negotiations with client ongoing, not likely to be concluded this year.

£9m hit to EBITDA this year FY 12/2022

There’s also a profit warning for next year, FY 12/2023 -

The NTU contract combined with extra cost and wage inflation is expected to reduce anticipated EBITDA performance in the year ending 31 December 2023 by c£4m.

Some new contracts have been signed.

Expected to report reduced net debt at year end, and “comfortably within” bank facilities.

My opinion - Tribal has been accident-prone in the past, and it seems to have made a right mess of things with this big contract, so questions obviously need to be asked, how was this possible? Could it happen again? Management competence?

It’s got a weak balance sheet, with negative NTAV. Although software companies don't need much capital.

I wouldn’t touch it as a standalone investment, but software companies are often takeover targets at remarkably high valuations, since larger groups seem to value the way they are embedded, and mission-critical, to their clients.

So it’s anybody’s guess what happens in future.

Graham’s Section:

Peel Hunt (LON:PEEL)

Share price: 78p (-5.5%)

Market cap: £96m

Here are Peel Hunt’s results for the H1 period to September 2022:

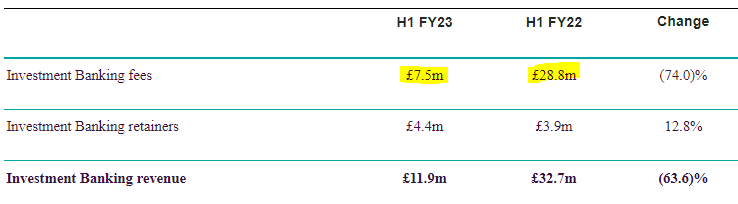

- Revenues £41.4m (H1 last year: £71.4m).

- PBT £0.1m (H1 last year on an equivalent basis: £21.6m).

- Staff costs as percentage of revenue 58.5% (last year: 45.8%).

Based on these numbers, staff costs have reduced from £32m to £24m.

What I’m looking for with a stock in this industry is the ability to reduce variable pay aggressively so that in the tough years, they can at least avoid making a loss. Peel Hunt has just about managed to do this, despite what they describe as “a multi-decade low for equity capital markets activity”.

Most of the revenue reduction, predictably, was seen in the Investment Banking division:

But they are looking ahead to when corporate deal-making and equity issuance might be back in vogue:

We continue to receive new mandate enquiries and we have a number of pipeline deals that we expect to execute when market conditions permit. Our retained corporate clients typically transact every three to five years and challenging market conditions have resulted in delayed activity that may lead to deal flow as markets normalise.

The number of corporate clients has increased slightly to 165, of which 35 are in the FTSE-350.

Research Payments & Execution Commission revenue: this is down by a much more modest percentage amount (6.8%) to £13.7m, in a performance described as “resilient”.

These tend to be more stable activities - the demand for equity research and for trading in the secondary market is still there, even when there are very few IPOs taking place.

And the company continues to pick up awards for their equity research work:

Execution Services revenue: down by 35% to £15.5m. Even the market-makers feel the pain in falling, quiet markets with less trading activity taking place.

Balance sheet: another thing I look for with these stocks is a giant cash pile and a strong balance sheet. They need this for regulatory reasons anyway, but it’s also a good way to anchor the valuation.

Peel Hunt’s balance sheet shows net assets of £96m, nearly all of which are tangible.

Or another way of looking at it: net current assets (current assets minus current liabilities) are £106m. From that figure we could deduct the long-term portion of a loan outstanding (£18m) to get a financial net worth for the company of £88m.

So my own estimation of the balance sheet is that it’s worth in the region of £90m. If the market cap traded significantly below that level, while the balance sheet remained this strong, I’d start to think that we were being offered a bargain.

CEO comment: Peel Hunt’s CEO naturally points to the unusual decline in overall activity, which he argues is “due to several factors including investor redemptions, institutional investors building up cash positions and retail investors being more cautious as equity markets responded to rising inflation, the cost-of-living crisis and the possibility of a lengthy UK recession.”

As a reminder, here is the performance of the FTSE Small-Cap Index this year:

And here is the AIM All-Share Index:

He notes that there were only five UK IPOs in the first six months of 2022 (vs. 37 in the same period last year). Fundraisings and other equity capital markets activity saw only 97 deals (vs. 257 deals in the same period last year).

He takes a positive medium-term view on the attractiveness of the UK equity market, arguing that higher rates spell the end of private equity dominance, that pension funds have abandoned equities and left them under-owned, and that HM Treasury and regulators are working to make UK financial markets more competitive and attractive.

While I agree with him that UK equities are “under-owned” and are attractive over the medium-term, nobody knows when this situation might correct itself - it could be 2 years, or it could be 5 years or longer!

My view: this stock listed in late 2021 at 228p, and is now at 78p. If there is one thing that Peel Hunt understands, it’s the equity markets - and they got the timing right when it came to making their IPO.

Looking forward, with the shares down by 66% from their IPO valuation, I think we could be getting close to value territory. I will always come back to that balance sheet value of around £90m (give or take).

The company has shown, at least in H1, that it was able to withstand terrible conditions and still just about avoid making a loss.

This provides some comfort that their net asset value is unlikely to deteriorate, at least not by much.

And as they enjoy a large surplus over their regulatory capital requirement, it’s reasonable to expect that future profits will get passed onto shareholders without difficulty (they have a target payout ratio for the basic dividend of 40% of profits).

With H1 out of the way, and the results not being so bad as they might have been, I’m now more comfortable with this stock than I was when I first looked at it in October. Around or below a market cap of c. £90m, I think it might be considered a value investment.

Mortgage Advice Bureau (Holdings) (LON:MAB1)

Share price: 448.6p (-20%)

Market cap: £255m

The Mortgage Advice Bureau (MAB) was at the epicentre of the recent drama in the mortgage market, which saw rates rise and products being pulled from the market overnight:

These extreme market and lending conditions severely impacted activity levels across all of the Group's product lines, with written business in October and November circa 50% below expected levels. The reduction in mortgage activity and new house sales is expected to persist until early 2023, after which activity levels are expected to start to slowly build.

Mortgage volumes are now at “exceptionally low levels”, and this is affecting recruitment: mortgage advisors are not being onboarded as planned, and leavers aren’t being replaced.

We also get some interesting colour on the latest state of the market:

Buyers with mortgages reserved prior to the mini budget are strongly motivated to complete their purchase at the lower mortgage rates they have secured. Where mortgage offers expire, typically after six months, there is a risk of some transactions aborting if they are not renegotiated. Pipelines are still holding together reasonably well, but we do now expect slightly higher fallout rates than usual.

Outlook

FY December 2022 is now expected to be “slightly below market expectations”, despite a growing market share of 7% (from 6.1% last year).

For next year, MAB acknowledges that H1 will be poor, due to lower adviser numbers, but expects “a second-half weighted recovery” - this seems like a courageous call. How can we be confident, as MAB claims, that the economic and interest rate outlook will be more stable then? I don’t think we can!

MAB can point to 1.8 million borrowers whose mortgage deals will expire in 2023, and this provides an opportunity for work on transfer deals.

As far as profits next year are concerned, we “may see no improvement on 2022”, even assuming that the H2 recovery materialises.

The September 2022 mini-budget gets the blame from MAB for what has happened. With their army of mortgage advisers no longer growing, and with stricter underwriting criteria for borrowers, it is going to be a tough year for the company to make any progress. MAB finds comfort in the knowledge that “transactions are delayed, they are not lost”.

My view

This company has, on the face of it, a very nice track record of profitability:

The quality metrics are very good too, which is probably related to the fact that MAB uses a franchise style model. The stock gets a QualityRank of 96.

So I wonder if the disruption caused by recent events might possibly provide a buying opportunity?

MAB was supposed to earn adjusted net income of £24-25m this year.

It will miss that, slightly, and could do worse again next year.

There will also be bigger adjustments to the numbers, after an acquisition: MAB bought 75% of mortgage broker Fluent Money in March, for a cash payment of £73m.

The integration of that company has been successful, but I wonder about the timing of the deal and the valuation. From the announcement RNS:

In the year to Mar-22E, Fluent is expected to generate £38.5m revenue (+45% yoy) and adjusted EBITDA of £4.2m (+118% yoy)

MAB said that they expected Fluent’s adjusted EBITDA to double this year, but it still feels like they paid a very heavy price for it.

On balance, I reckon it’s worth keeping an eye on this one: if they maintain their track record of profitability, despite the downturn, and are ready for the upturn when it eventually comes, then their shareholders could do very nicely indeed. The elimination of any short-term growth prospects is unfortunate but could be priced in already at these levels.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.