Good morning from Paul & Graham!

Agenda

Paul's Section:

Zotefoams (LON:ZTF) - a positive, ahead of expectations, update for FY 12/2022. I explain why this is one of my favourite GARP shares (no holding personally, unfortunately). More detail below. Thumbs up from me.

Carclo (LON:CAR) [quick comment] - down 20% to 12p this morning (at 08:12), so market cap now tiny at £9m. It says H2 (of FY 3/2023 I assume, the RNS looks like a typo, saying FY 3/2022) will be “materially lower” than previously expected. Bank remains supportive, and in discussions about amending bank covenants. I went through the FY 3/2022 accounts here in some detail, explaining why the expensive debt, and pension scheme cash outflows use up all the profit. There does seem to be significant freehold property though, which could be why the company hasn’t already gone under. Very high risk of a dilutive equity fundraise (which could be on ruinous terms, as we saw yesterday with Trackwise), hence I would say this share looks too risky for now. (no section below)

Currys (LON:CURY) - Interim results from this £10bn pa revenues electrical retailer, making a surprising appearance within our small caps universe. The seasonally slower H1 has been soft, and full year guidance is trimmed, but still guiding a decent FY profit. The balance sheet concerns me - it's weak, and completely reliant on massive trade credit for buying the stock - if trade credit insurers get cold feet, that could kill the business. Divis look unsustainable. Thumbs down from me, as it's too risky if we see an extended consumer downturn.

DX (Group) (LON:DX.) [quick comment] - nothing particularly noteworthy in this AGM update. Trading continues to be in line with expectations for FY 6/2023 so far. Pipeline of new business opportunities is “very healthy”. Liquidity good, with “significant net cash”. The valuation metrics on the StockReport here look good - fwd PER of 7.6, and divi yield of 5.2%. There’s been a big improvement in profitability here, so it looks a successful turnaround. My view - might be worth a fresh look, after a troubled past.

STV (LON:STVG) [quick comment] - this is called a trading update, but it seems more like a PR release, talking up the good bits, but without giving figures for overall performance or outlook. Other than saying that it “performed strongly in 2022”. Thanks to Shore Capital for a note today which reduces FY 12/2022 EPS by 5% to 39.9p, and a thumping reduction of 18% in forecasts for 2023 & 2024. So this is a 2023 profit warning that’s been slipped out via the broker, and not explained at all in the RNS. That’s really bad. Remember that STVG has a huge pension scheme issue, so that’s why the shares are on a low PER. Although the accounting deficit did reduce a lot in the recent interims. Deficit recovery payments were £7.1m just in H1. So make sure you fully understand the pension schemes before investing here.

Graham's Section:

Science (LON:SAG) (£183m) - FY December 2022 is trending slightly ahead of expectations thanks to dollar strength that was subsequently locked in by the clever use of financial derivatives. The company is successfully navigating both cost inflation and a slowdown in demand from the consumer-oriented sectors it serves. If it acquires the consulting and engineering business TPG, as planned, then it will enjoy further diversification with exposure to the aerospace and defence indutries. Based on its financial track record, Science looks like a better-than-average company in its sector, so I can get behind the market’s valuation at a PER in the mid-teens.

Hunting (LON:HTG) (£444m) - the order book at Hunting has grown to nearly $500m, most of it to be delivered next year, and the company accordingly increases its guidance for FY 2023 EBITDA to $85-90m (previously: $80m). I don’t believe that EBITDA is a useful measure of profits at this company but I still prefer to see upgrades rather than downgrades! The business appears to be doing very well. I note the very volatile historic results - this company has a tendency to perform very well or very badly. Hopefully the oil and gas industries can continue to boom, and Hunting’s shareholders can experience the former instead of the latter!

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul's Section:

Zotefoams (LON:ZTF)

298p (pre market open)

Market cap £145m

15 December 2022 - Zotefoams, a world leader in cellular materials technology, today provides an update in respect of its financial year ending 31 December 2022.

Continued positive momentum through Q4 and full year profit ahead of market expectations

Positive trading - this looks good -

As communicated in the Group's trading update of 13 October, performance over the nine months to 30 September 2022 had been strong, with revenues approximately 24% ahead of the comparable prior year period.

Encouragingly, trading during October and November has remained strong, with both the Polyolefin Foams and High-Performance Products businesses continuing to deliver year-on-year growth as well as a continued focus on cost and efficiency.

As a result, based on current FX rates, the Board now expects Group FY22 adjusted profit before income tax to be ahead of current market expectations*, with the extent of the outperformance primarily dependent on the timing of customer shipments in the final weeks of the year.

* Current Company-compiled consensus expectations for adjusted profit before income tax and separately disclosed items, for the year ending 31 December 2022, is £10.7m.

Outlook - this sounds fine to me, given that ZTF has successfully mitigated challenges (such as raw materials cost inflation, and energy costs) in 2022 -

"Whilst we expect a number of the challenges experienced this year to continue into 2023, we are confident in our ability to respond and we continue to see significant opportunity for the Group."

Broker updates - nothing unfortunately. I’ve nagged the company’s adviser on this, saying that they need to get some broker research out there to PIs, via Research Tree or commissioned research, otherwise we’re in the dark without any guidance.

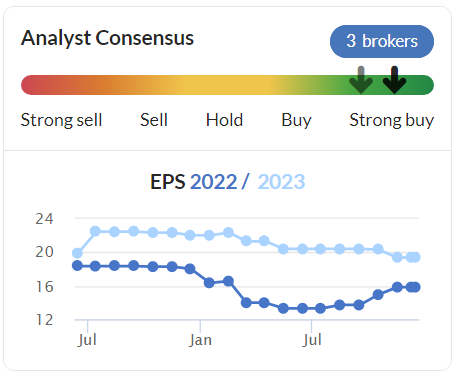

This is what Stockopedia has for broker consensus, from 3 brokers that feeds into this data -

This is where we have to use some educated guesswork. We have 15.8p broker consensus now, so “ahead of expectations” probably means anything between 17-20p EPS for FY 12/2022. The fairly upbeat outlook comments also make me comfortable with the existing forecast of 19.3p for FY 12/2023.

At 298p per share, that means a PER probably between 14.9 and 17.5, which looks reasonable - neither cheap, nor expensive really.

Dividend yield (forecast) is modest, but worth having, at 2.5%.

Balance sheet - is strong, with freehold factories in at cost. There’s a fair bit of debt, but it’s expected to fall rapidly, due to a large capex programme now being complete, with well invested factories, so the company is now in cash generation, de-gearing mode. This point is confirmed today here -

Cash generation also continues to be positive. The better than anticipated earnings performance should contribute to an appreciable reduction in leverage compared with that reported in the interims at 30 June 2022.

My opinion - this is one of my favourite GARP (growth at reasonable price) shares. So I interviewed the CEO in late Oct 2022 - audio here, written summary here.

It’s been particularly impressive how the company has been able to raise selling prices considerably this year, demonstrating that its products are in demand, and have pricing power. It’s a specialised niche, with little competition, that’s why.

There’s also the blue sky project Re-Zorce, which is thrown in for free. If this takes off (and early signs sound encouraging) then it could trigger a re-rating, and higher profits - this is innovative fully recyclable food/drink containers, a huge potential market.

I think the shares are a long-term buying opportunity right now, at less than half the peak share price in 2019. It’s proven very resilient this year, and today’s positive update confirms that, so I think the downside risk on this share looks pretty low, with good longer term upside. So a thumbs up from me.

Currys (LON:CURY)

60.4p (down 8% at 09:15)

Market cap £681m

It’s not often I review companies with £10bn revenues in these small cap reports! Currys has popped its head around the small caps door, and requested permission to enter.

These are quite large & complex accounts, so it would take me too long to report in detail here, so I’ll just draw out what seem to me the key points -

H1 figures for the 26 weeks ended 29 October 2022 -

H1 revenues £4,473m (down 6.5% vs H1 LY)

Weak LFL (like-for-like) revenues, at -8%

H1 looks the seasonally weaker half

Impairment of goodwill of £511m (I’m happy to ignore that)

Statutory loss before tax £(548)m - mainly caused by the goodwill write-off

Adjusted H1 loss before tax £(17)m

Guidance: FY 4/2023 a profit of £100-125m (PBT) - this is lower than previous guidance of £125-145m

UK - profits up, from increased gross margins, and cost cutting (offsetting sales decline)

International - more problematic, with sector excessive inventories & heavy discounting. CURY says these are temporary negatives.

Medium-term - targeting a 3% adj EBIT margin, realistically it’s always going to be a very low margin business.

Going concern note says it can operate within bank facilities & covenants, even in a downside scenario (but that’s only a -5% sales fall, which doesn’t look harsh enough to me)

Balance sheet - looks horrible. NAV of £1,847m contains an absolutely bonkers £2,670m of worthless intangible assets. Deleting that, results in NTAV of £(823)m. Note that the lease entries combined show a deficit of £(251)m, which indicates there must be quite a few loss-making sites that need to be closed, if and when leases expire. So I would expect the business to continue shrinking from store closures.

Net bank debt is modest at £105m, but the business is mainly financed by the trade creditors of £2,856m. Therefore the main risk here is not so much the bank getting the jitters, but trade credit insurers withdrawing cover.

An excellent disclosure here, we need all companies to provide this information -

The average net debt for the half-year period was £(114)m, compared to an average net cash position of £290m in H1 2021/22.

I’m not sure why the previous average net cash position has worsened so much in the last year?

Pension schemes - big numbers, see note 5, with assets of £987m, and liabilities of £(1,237)m, so a deficit of £(250)m. It's astonishing to see how asset values have crashed in the last year. Trouble is, liabilities have not reduced, it's just that the way they're calculated (referencing bond yields) has technically reduced liabilities. So I'm uneasy about big pension schemes generally.

Cashflow statement - pension scheme deficit recovery payments are running at £78m pa, so highly material.

The operating cashflow last year was all consumed by capex, and finance costs (including big lease liabilities). Dividends and share buybacks were funded through increased borrowings.

Therefore I would say the dividend yield looks unsafe, and should probably be pulled, as the company really cannot afford to be paying divis at all, in my opinion. So I wouldn’t buy this share for the generous divi yield, as it could disappear quite easily.

Outlook - I've focused mainly on the downside risks above, but for balance, the company also gives the upside potential in the guidance section -

We are confident that the improvements to UK&I gross margin and ongoing cost control will continue to deliver robust profitability despite our expectation that market conditions will not improve in the second half.

In International, the high market shares and our long track record of growth in sales and profit, together with self-help action on margin and costs, give us confidence that profitability will recover robustly when market conditions normalise. The timing and extent of this will depend on when demand normalises, but especially on how long competitors need to clear excess stock, and how long they sustain unprofitable pricing.

My opinion - I’m not at all keen on this. The balance sheet is too weak, and the whole business relies on trade creditors extending almost £3bn of financing. There’s no reason to expect those credit lines to be pulled, but it’s a huge exposure. Investors often forget that trade credit (i.e. suppliers delivering goods before they get paid) is the main way that many businesses are financed.

Due to this financial weakness, dividends look unsustainable to me.

It doesn’t look in any immediate risk of going bust, but if trading gets a lot worse, say in the event of a deeper consumer downturn in 2023, then things might get difficult. Although management says it has levers to pull, which I’m guessing would be curtailing capex, cutting the marketing budget, staff cuts, etc. So there is some flexibility in the cost structure.

Meanwhile there are online-only competitors, where nobody has any pricing power, as many consumers compare prices and go with the cheapest.

For me, this one’s an avoid.

Stockopedia gives it a fairly decent StockRank of 69, so maybe I'm being too cautious?

The share price is right back down to pandemic lows of early 2020. Opportunity, or a worry? That's your call!

Graham’s Section:

Science (LON:SAG)

Share price: 404p (+6%)

Market cap: £183m

This calls itself “an international science, technology and consulting organisation”.

Paul has covered it on numerous occasions this year - see the archives - and in general has looked favourably on it.

This morning brings a pre-close trading update that is slightly ahead of expectations.

As anticipated, while some market sectors, particularly medical, are continuing to invest, consumer-oriented sectors in both services and products have been impacted by the global economic slowdown. With a significant proportion of income generated in US Dollars, the Group has benefitted from the relative strength of the Dollar, offsetting the significant increase in energy prices and other cost inflation. In aggregate, the Board anticipates that revenue and adjusted operating profit for 2022 will be slightly ahead of current Board expectations.

I’m impressed that Dollar strength has been enough to offset cost inflation. I wonder if Science Group has been successful at pushing through its own price increases to customers?

Balance sheet - gross cash of £44.5m, net funds of £30.1m. The company’s £25m RCF is undrawn and its term loan has been fixed using an interest rate swap. So the company has “limited exposure to future interest rate increases”.

Currency cap - the company has used another derivative to protect itself from US dollar weakness until the end of 2023. It looks to me like this trade has already been incredibly successful as they’ve capped $1.25m of monthly revenue at a GBPUSD rate of 1.20. But GBPUSD has already risen to 1.24!

If, for example, GBPUSD trades at an average rate of 1.30 for the duration of next year, then my quick calculations suggest that this derivative will pay out in the region of £1m to Science over the course of the year. There will have been some costs to set it up, of course. It’s a lovely bit of business to have done.

During the mini-Budget panic, Cable fell as low as 1.07, so this explains why it was possible to get a cap at 1.20.

Monthly revenues in excess of $1.25m aren’t hedged, so Science will still have some exposure to dollar strength or weakness.

And by early 2024, the hedge will have expired - it’s easy to forget that hedges don’t last forever. For example, many companies who have benefited from energy fixes in 2022 will be unprotected at some point over the next 12-18 months. Something to watch out for!

TP Group acquisition - the company continues to anticipate that it will take over TP (LON:TPG) “early in 2023”. TPG’s financial track record looks quite bad, so hopefully the influence of Science on it will be a positive one!

How to pay for it:

The Board does not anticipate that the cash outflow (including repayment of TPG bank debt, fees and integration costs) will exceed £25 million and therefore the acquisition will be funded through Science Group's existing cash resources and finance facilities.

With net funds of £30m, perhaps Science will barely need to use its RCF to pay for this?

Outlook - TPG will give Science “ entry into the defence market, together with synergistic opportunities for growth in the medium term”.

My view - Science is a diversified consultancy business that includes a digital audio company. With TPG, it is seeking to add another branch of consulting, plus some engineering services.

To me, the market is pricing this one about right. Having been burned by professional services companies in the past, I would never want to overpay for them again. But Science has a financial track record that says it’s a better-than-average consultancy company, and in any case it is more than just a consultancy. So perhaps a PER in the mid-teens is fair?

Before I wrap this up, I’d like to reiterate that I’m genuinely and deeply impressed that they bought a GBPUSD cap at a rate of 1.2. What a clever bit of business!

At market extremes, banks don’t price long-term derivatives correctly - remember that Warren Buffett sold many billions of dollars worth of put options on stocks during the great recession (a bullish bet that paid off handsomely). It takes highly opportunistic traders and investors to exploit this.

Hunting (LON:HTG)

Share price: 269p (+2%)

Market cap: £444m

This is an “international energy services group”, with a year-end trading update. They provide “innovative products enabling oil and gas extraction worldwide”. Oil and gas producers have had a good year, so I would assume that Hunting has done well, too!

2022 is trending in line with expectations for EBITDA of c. $50m. The company reports in US dollars.

Key points:

- Order book is still improving and approaching $500m.

- 2023 expectations raised for EBITDA of $85-90m (previously $80m).

- New sales group focused on “Energy Transition” (“carbon capture, geothermal and other low carbon technologies”).

The order book is short-dated and will be delivered mostly next year, although some products won’t be delivered until 2024/2025.

North America - “steady sales” and “strong momentum” reported across Hunting’s various business units.

South America - “New opportunities continue to be pursued… with drilling and completion activity accelerating as unconventional resources are developed…”

EMEA - “improving results”.

Asia Pacific - “steadily improving performance since the middle of the year…”

Balance sheet - net assets of $847m (November), although this will include a large amount of goodwill and illiquid equipment. Cash of $24m, reducing to $20m by year-end.

2023 outlook - the raised EBITDA guidance is a result of the strong order book performance which, as I’ve said, mostly consists of sales that will be delivered during 2023.

My view

I’m not a sector expert when it comes to oil and gas, but I can make a couple of observations.

Firstly, I know that many investors like to take the “picks-and-shovels” approach to energy, i.e. investing in the associated tools, equipment and technology rather than in the energy producers and the energy assets themselves.This way, you can still get positive exposure to the industry but perhaps without some of the more extreme cyclicality and the other risks that come from owning energy assets. Hunting appears to be a good example of a “picks-and-shovels” stock.

Secondly, and more negatively, I note that Hunting reported nearly $40m of depreciation last year. It has a range of capital-intensive manufacturing facilities and therefore in my view the EBITDA number must be thrown out as irrelevant. Upgrades to EBITDA estimates are still better than downgrades, but the EBITDA number itself is too far removed from profitability to be of interest to me. Depreciation is a real cost and is a significant one at Hunting.

Overall, I’m not sure how to justify Hunting’s current market cap of nearly £450m. The estimates for 2023 are good, and it appears that investors are willing to give the company the benefit of the doubt that it will hit these forecasts.

Perhaps the Hunting share price also reflects a belief that commodity prices will continue rising over the next few years, as inflation remains a key issue. Oil and gas are booming industries these days and it should not be difficult for Hunting to make money in this environment.

If we look back to 2018/2019, Hunting was amazingly profitable. Perhaps the company can get back to that kind of performance in the next few years, if the oil price stays high?

Given the volatility of historic results, this one is offering lots of opportunity, with lots of risk.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.