Good morning from Paul & Graham!

Today's report is now finished.

Agenda -

Paul's Section:

MJ GLEESON (LON:GLE) - excellent results for FY 6/2022, beating (previously raised) forecast. Bulletproof balance sheet, and the market cap is currently at par with NTAV, so you're really getting it at a discount, because the large land bank is probably worth well above book cost. Positive-sounding outlook. If I had to buy one housebuilder, this would be it. The average selling price is only £167k, all houses (not apartments), so this should be defensive, in any housing market downturn. This share looks exceptional value, in my opinion.

DFS Furniture (LON:DFS) - sorry it took me so long to crunch these numbers. I'm horrified at DFS drawing down most of its overdraft, to fund divis and buybacks. This seems incredibly reckless, given the rapidly deteriorating macro picture. The balance sheet remains horrible. I consider it uninvestable right now, much too high risk.

Hilton Food (LON:HFG) - is down 27% today, on a profit warning. The house broker lowers FY 12/2022 forecast by 23%, so this price reaction looks justified. Acquisitions have been fuelled by debt, which looks a bit too high to me. It's trying to expand, fund a lot of capex, and pay divis at the same time, which looks too ambitious. Overall, it doesn't interest me - the margins are too low, and inflation/costs/consumer retrenchment are all significant headwinds.

Graham's Section:

THG (LON:THG) (555m) - this e-commerce business issues a profit warning with its interim results. Rising whey prices have hurt margins at its myprotein business, and its beauty brands and websites are also suffering from the difficult consumer environment. THG has elected to “protect” and “shield” its customers from rising prices, in order to gain market share and improve customer retention. This has resulted in a large (£89m) loss in the six-month period, and a significant increase in borrowing far beyond that which would have been caused by normal seasonal outflows. This company had a much higher valuation at IPO, far higher than our market cap threshold. However, even at its current much reduced asking price, I am struggling to find any value or quality here. After today’s share price fall, the adjusted EBITDA multiple is still 6x-8x.

Avation (LON:AVAP) (£58m) (+4%) [no section below] - this aircraft leasing company provides an update for FY June 2022. The results will be published in full on September 29th, but for now it lets us know that it expects to have made a net profit, on revenues of c. $115m. This signals a recovery from the disastrous year that was FY June 2021 (see coverage by Jack here). As a footnote to the Virgin Australia collapse, Avation announces that it will receive 5.4 cents on the dollar from its AUD $101.4m claim against that company, with the possibility of additional payouts.

The fallout from Covid undid the financial gains made by this company over several years, but if that event can be considered extremely rare and unlikely to happen ever again, then these shares might be worth exploring - it has a long-term record of attractive returns on equity. Net assets per share were £1.64 as of December 2021 and although much will have happened in the intervening six months, the value on offer here could be substantial. Deserves further study. [no section below]

Explanatory notes -

A quick reminder that we don’t recommend any stocks. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps up to about £700m. We avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech).

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to.

Paul’s Section:

MJ GLEESON (LON:GLE)

464p (pre market open)

Market cap £271m

I’m a recent convert to the delights of this value share, and covered its “significantly ahead” trading update for FY 6/2022 here on 11 July 2022. Re-reading my notes, this low cost land developer & housebuilder (for first time buyers mainly) looked great value at 526p per share. The only uncertainty needing more research, being cladding costs.

There are some useful short videos here on the company's website, explaining what it does.

The good news is that results out today look great, the outlook seems fine, and the share price is now even lower, so should we be rubbing our hands with glee, son?! (Geddit?!)

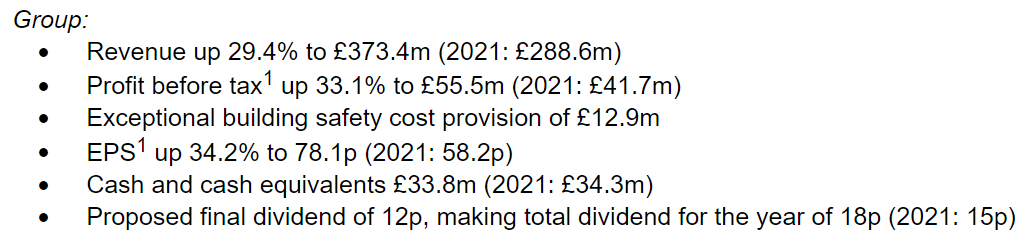

As you can see, the financial highlights look really good -

EPS looks like a beat, actual being 78.1p, vs broker consensus on the StockReport of 71.6p.

Dividend yield is nearly 4%, and the 18p total divis are more than 4 times covered, so the dividend paying capacity is much larger than the actual payout.

Balance sheet - is stupendously good, as a lot of housebuilders are. In previous downturns, the leveraged balance sheets resulted in housebuilders almost going bust, I recall. This time around, they’ve generally got superb, ungeared balance sheets. So the cyclical risk is probably lower than in past economic downturns.

NAV is £272m (NTAV is the same, as there are no intangible assets). That’s within a whisker of the market cap, at £271m. That strikes me as a terrific asset-backed bargain. Bear in mind there would be upside value on the land bank, in the books at cost. So you’re really getting this share at a discount to its net tangible asset value, which doesn’t make any sense to me.

Current assets are £353m, whereas ALL creditors total £95m! That’s astonishingly good.

I’d say this share looks a sitting duck for a takeover bid, on the basis that it’s priced well below its fundamental value, and is trading well, making good margins.

The best bit, is that its low price new homes are in strong demand, and the energy crisis is helping - because well insulated new homes will cost a lot less to heat than draughty old rental properties.

Average selling price is only £167k - which again makes this share so attractive, as new homes that affordable are not likely to see much, if any downturn in price, especially when incomes are rising strongly.

Outlook - pretty upbeat, considering the macro environment -

This is another excellent performance which reflects not only the strong operational capability of our business but also the continuing structural under-supply of affordable homes for first time buyers on low incomes.

As well as being affordable, our high-quality homes are also very energy efficient, costing significantly less to run than most houses in the UK, particularly in the rented sector. As a result, our homes are much sought after, and demand remains resilient.

Gleeson Land's market remained robust throughout the year and the business delivered a strong result. Demand in the South of England for quality sites with sustainable and implementable residential planning permission remains strong and the division is well-placed to drive further sustainable growth.

The Board has reviewed a range of macroeconomic forecasts and, notwithstanding the current outlook for the broader economy, remains confident that the Group, with its defensive qualities and unique position within the wider house building sector, is well-positioned to deliver further profitable growth in the current financial year…

Employment levels remain high and mortgage availability, supported by the recent relaxation of lending rules, is robust. Whilst the withdrawal of the Help to Buy scheme, which closes for new applications in October 2022, means no government support for homebuyers for the first time in over 20 years, it is not expected to impact the affordability of, or demand for, a Gleeson home.

The average selling price of a new build home in our geographic regions is £266,000, 59% higher than the average selling price of a Gleeson home at £167,300. Gleeson Homes is therefore uniquely positioned to serve customers who might previously have been considering a more expensive property but who, in the current environment, will look at more affordable price points. We are already seeing interest from these value-driven customers.

Cladding & fire remediation - more clarity & detail here -

In signing the Department for Levelling Up, Housing and Communities' ("DLUHC") pledge in April 2022, the Group gave its commitment to investigate and remediate any life-critical fire-safety issues on buildings over 11 metres in which the Group had some involvement in developing over the last 30 years. Following a detailed assessment of the buildings covered by the pledge, an exceptional provision of £12.9m has been recorded this year. This estimate of the life-critical fire-safety remediation costs for these buildings is based on reviews and surveys completed to date. We are in the process of undertaking a programme of intrusive inspections and fire risk assessments, where permitted by the building owners.

Like all housebuilders, we have also been subject to the additional 4% residential property developers tax ("RPDT") from April 2022, which was designed to raise at least £2bn over a 10-year period towards the government's cost of dealing with defective cladding. This comes on top of the planned rise in corporation tax from April 2023 from 19% to 25%.

(I thought the Govt was reversing the rise in corporation tax, or maybe I imagined that? Maybe it hasn’t yet been formally announced?)

My opinion - there’s so much to like her, I only wish I had some spare cash to buy some. Not for a trade, but for a long-term position. It looks exceptional value right now, in my opinion. As always, please DYOR, because I might have missed something that explains why it's so cheap - do post your comments if you think I'm wrong, we want to hear contrarian views!

Note the share price is now well below the pandemic lows. The share count has only risen from 56m to 58m over that time.

A friend points out that other housebuilders also look cheap at the moment, Redrow (LON:RDW) in particular, but it's the defensive nature of GLE that I like, building really cheap starter homes for first time buyers. There's so much demand at that bottom end of the market.

.

.

DFS Furniture (LON:DFS)

117p (down 14% at 08:40)

Market cap £284m

The 14% drop this morning has wiped £47m off the market cap.

As regulars here will know, we like the business of DFS in itself, but detest its horribly stretched balance sheet. To make matters worse, reckless share buybacks are underway, with management seemingly unconcerned about the economy going into a recession.

This is despite the fact that they had to do an emergency fundraising when the pandemic began, so I just cannot understand why they’re being reckless again with the balance sheet, so soon into the next downturn.

Shares in the whole sector have been under pressure, with SCS (LON:SCS) dropping heavily, along with DFS, and of course the supposed disruptive challenger, Made.Com (LON:MADE) has been the biggest disaster, and looks to be heading to zero, in my view, due to the massive losses it’s now generating.

Note also that DFS, which had been doing well with online sales, has seen that fall back sharply from 34% of sales last year, to 22% this year - so (hardly a surprise) it seems that customers do mostly prefer to see, and touch furniture before they buy.

Anyway, let’s look at today’s update.

DFS Furniture plc (the "Group"), the market leading retailer of living room and upholstered furniture in the United Kingdom, today announces its preliminary results for the 52 weeks ended 26 June 2022 (prior year comparative period is the 52 weeks ended 27 June 2021, non Covid-19 disrupted comparative period is the unaudited pro-forma 52 weeks to 30 June 20191).

I don’t think the company headline adds much value -

OVERCOMING SIGNIFICANT COVID-RELATED CHALLENGES WHILST SECURING MARKET SHARE GROWTH AND REMAINING FOCUSED ON LONG-TERM VALUE CREATION

DFS gives very clear guidance, and on 5 July 2022 it sounded upbeat, saying FY 6/2022 adj PBT would be at the top end of its guidance for £57-62m. The actual figure today is £60.3m, so that’s just about as expected.

That’s a long way down on last year’s £109.2m PBT, which was boosted by people revamping their homes during the pandemic, and Govt support measures.

Pre-pandemic the adj PBT was £52.6m, so it looks as if the business has returned to making £50-60m profit p.a., which is similar to what it achieved in 2016 & 2017. So not really a particular growth story, at least in profitability terms.

The big drop in profit from LY, is due to the gross margin dropping from 56.3% to 52.7%, but mainly due to a huge increase in selling & distribution costs, up from £298m in FY 6/2021, to £368m in FY 6/2022. A lot of that is probably the unwinding of Govt support measures, such as business rates relief, plus wages & utilities rising.

In EPS terms, FY 6/2022 saw 17.5p achieved, so at 117p, the PER is 6.7 - low, but low for several good reasons, I would say.

Outlook - this is probably more important than the historic numbers now.

As I’m sure we would all expect, demand is now softening, this shouldn’t be a surprise to anyone -

In the fourth quarter of FY22 and first quarter of FY23, order volumes for the Group softened markedly relative to pre-pandemic levels, reflecting a trend seen widely across the furniture industry. The macroeconomic environment remains challenging, given the potential effects of the current high-inflationary environment on consumer behaviour. We therefore present three alternative scenarios for performance in the financial year:

As always, the guidance DFS gives is superlative. If only all companies (and broker research) would do this low/medium/high range of scenarios -

.

Note that, as we’ve seen this year with online competitor Made.Com (LON:MADE) there’s no guarantee that companies will necessarily achieve results within the guided range. MADE blasted through the downside scenario with a series of profit warnings earlier this year.

Plus remember that, by using order intake in the above table, that does provide something of a buffer to profits, since some of the downturn would be deferred, due to the time lag between placing an order, and recognising the revenue & profit.

If we take a gloomy view, then I reckon this could see EPS drop into single digits this new year, FY 6/2023. If you’re more optimistic about the macro picture, then profitability might be more robust, who knows!?

Going Concern note - tells us that everything will be fine, even in a severe but plausible downside scenario. However, what this assumes is that the banking consortium remains supportive. Previous recessions have taught me that you cannot rely on banks to be supportive, when things get difficult. They hate risk, and sometimes force listed companies to raise money from shareholders, at the worst time & price.

Note how the RCF is already mostly drawn down as of 12 Sept 2022, without much headroom -

The Group has a £215.0m revolving credit facility which has been extended to mature in December 2024, with an option to extend the facility for a further year, subject to mutual agreement with the consortium of lending banks. At 12 September 2022, £37.0m of the revolving credit facility remained undrawn, in addition to cash in hand, at bank of £5.5m.

Covenants applicable to the revolving credit facility are: 3.0x net Debt/EBITDA and 1.5x Fixed Charge Cover, and are assessed on a six-monthly basis at June and December.

The Directors have prepared cash flow forecasts for the Group covering a period of at least twelve months from the date of approval of these financial statements, which indicate that the Group will be in compliance with these covenants.

Bank financing carries risk, and DFS management seem dangerously complacent about this.

The facility has been extended by another year but only to Dec 2024, so it’s not secure, long-term funding. Yet the whole business is dependent on that bank facility.

Where are the customers’ cash? It’s been spent! On divis and buybacks, which DFS calls “surplus capital”, when it actually has a yawning deficit in capital, with heavily negative NTAV.

I think this is a horrendous situation actually, just an accident waiting to happen. Management strike me as absolutely delusional.

Balance sheet - very much the elephant in the room.

Furniture retailers have a negative working capital model - i.e. they get paid by customers, before they have to pay suppliers for making the product (usually made to order).

So there should be a big pile of surplus cash sitting on DFS’s balance sheet, as there is with smaller rival SCS (LON:SCS) , but there isn't any (significant) cash, it's gone!

Net bank debt has shot up from £17.1m a year ago, to £88.5m at 6/2022. Judging from the going concern note above, this seems to have further increased to £172.5m as at 12 Sept 2022, with only £35m headroom left on the bank facility.

Overall, the balance sheet is horrible. NAV is £268.9m, but that includes worthless intangible assets of £533.8m. That leaves a nasty NTAV deficit, of £(264.9)m. Remember that management think they have surplus capital, when they quite obviously don’t.

IFRS 16 entries are £338m RoUA, less lease liabilities of £445m, so a deficit of £107m. That suggests there must be some loss-making, onerous leases within the store estate.

If we eliminate all the IFRS 16 entries, that shrinks the NTAV deficit from £(264.9)m to £(157.9)m - still pretty awful.

Divis/buybacks - with such a ropey balance sheet, and going into a recession, DFS has borrowed to give £75m to shareholders - this is madness -

This 3.7p final ordinary dividend taken together with the 3.7p interim ordinary dividend and 10.0p special dividend paid in May and also the £35m of share buybacks will mean the Group will have returned over £75m of capital to shareholders during calendar year 2022.

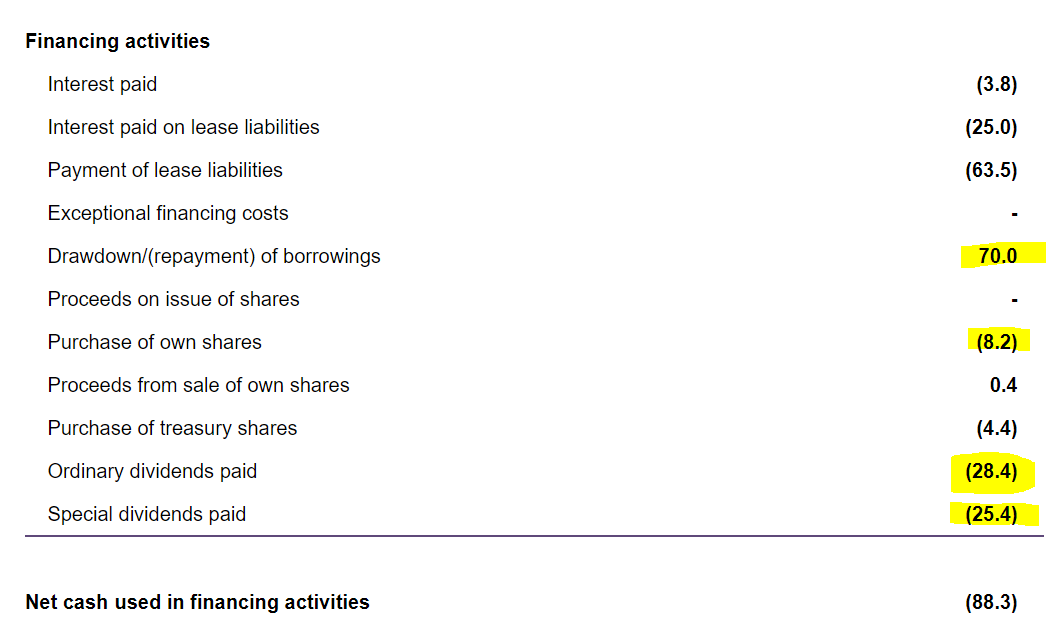

Cashflow statement - is complicated. The way I look at it, there wasn’t any free cashflow, since adverse (normalising?) working capital consumed cash, and what was left was spent on capex.

The financing section is the most revealing, which shows that all the shareholder returns were financed from bank borrowings -

.

My opinion - if the good times were still rolling, then I could maybe overlook the horrible financing structure, which reminds me of how private equity strip out cash & load companies up with debt.

However, it seems to me that, given very tough macro conditions, DFS management seem to be doing a Titanic - and speeding up as they approach the icebergs.

Special divis, and share buybacks, are things that should only be done when there’s surplus cash sitting around. To finance them from a big increase in bank borrowings, at a time when customer demand is softening, just seems an unimaginable thing to do. It’s asking for trouble.

If the economy really turns sour, then people curtail big ticket spending. Surely DFS know that? Hence they should be hoarding cash, not maxing out the overdraft.

Given all the above, I’m putting DFS on my uninvestable list, because it’s too high risk. It might be a false alarm, but the last thing I want to be invested in, going into a probable recession, is a big ticket consumer-facing company, that’s loaded up with debt. It’s not just the bank debt either, remember that trade creditors often rely on trade credit insurance, which can be withdrawn in the blink of an eye.

Hence a thumbs down from me, mainly due to the wobbly funding structure, but also deteriorating forward outlook.

.

Hilton Food (LON:HFG)

697p (down 26% at 13:09)

Market cap £623m

Mr Market has just thrown HFG back into our small caps space, and it’s currently lying on the floor, groaning!

It’s given up the previous 5 years’ upward share price momentum in the last 5 months, including today’s move.

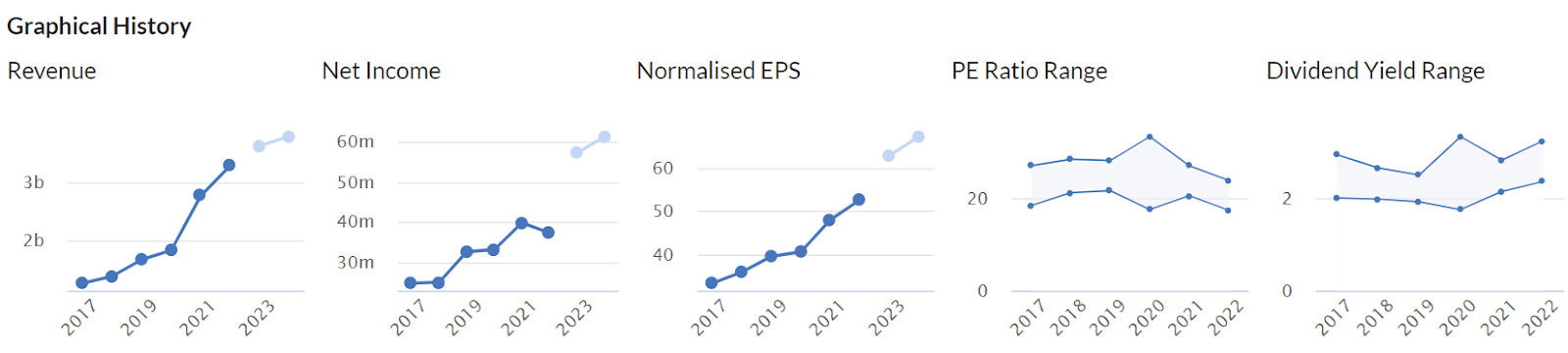

I last looked at this 6 years ago, so my previous notes here are outdated. Especially as the business seems to have tripled in size since then.

As you can see, there’s been a fairly good progression in profits & EPS too - although today’s market move suggests the forecast (lighter coloured blobs below) might be coming down somewhat -

Is it a bargain? Let’s find out.

Hilton Food Group plc, a leading international protein producer, is pleased to announce its interim results for the 28 weeks to 17 July 2022.

Key points from interim results -

Big H1 revenues of £2.04bn (up 19%, or 20% at constant currency)

Wafer thin margins though, with operating profit only £30.8m (up slightly)

Finance costs & tax both look quite high, so statutory PAT is only £14.5m (down 15%)

Adj basic EPS for H1 is down 12% to 28.0p

Small cut in the interim divi to 7.1p (H1 LY: 8.2p)

Adjusted numbers look a bit more respectable, removing goodwill amortisation, and making adjustments for IFRS 16 it seems (see note 16): adj EBITDA £66.6m, and adj PBT £34.4m.

Balance sheet - it’s a capital intensive business, and notice it also seems to rely on a lot of leased properties, with big IFRS 16 entries.

Net bank debt is high, after acquisitions, at £221m. That looks a little too much for comfort, in an economic downturn.

Going concern note is reassuring, well within banking facilities, which are committed until 2027.

Outlook - is a profit warning, but not quantified -

While we benefit from the strength of our diversified business model and continue to grow volumes internationally, Hilton has not been immune from the impact of macroeconomic headwinds. Across our markets, we have seen volumes come under pressure with the cost of living increasing and consumers becoming ever more cost-conscious. In our Seafood business these trends have been exacerbated with world events leading to unprecedented raw material price increases.

Given these factors, and combined with the impact of start-up costs and rising interest rates, the Board now anticipates that profitability for the year will be below expectations. However despite these short-term challenges Hilton's well-invested business, the recent acquisitions of Foppen, Dalco and Fairfax Meadow and our investments in Agito, Foods Connected and Hilton Food Solutions provide a strong platform for medium-term growth. We continue to explore opportunities for both geographic expansion and growth in our existing markets across the five pillars of our proposition.

Forecasts - many thanks to Shore Capital for letting us see its revised forecasts, up on Research Tree. This lowers FY 12/2022 EPS forecast by 23%, to 50.8p (a PER of 13.7). This is a drop of 16% against FY 12/2021 actuals.

I suppose it’s to be expected that a meat producer or distributor would come under pressure from consumers reining in household budgets, combined with inflationary cost increases.

I wonder why the company didn’t get brokers to gently guide down forecasts earlier, when these cost pressures & consumer hesitancy first started? It doesn’t look terribly well handled.

My opinion - it looks an OK business, but the trouble with low margin companies, is that it doesn’t take a lot to knock the profit numbers heavily. Profit is the small difference between 2 very large numbers (revenues, and costs).

Given the heavy debt, and a balance sheet that’s only really adequate, I don’t think I’d want to pay more than a single digit PER for this share at the moment. So it’s not of interest to me fundamentally, nor on valuation (which isn’t particularly cheap, even after today’s fall).

StockRank is only middling -

.

Graham’s Section:

THG (LON:THG)

Share price: 39.8p (-19%)

Market cap: £555m

This one has dipped below our market cap threshold, after a 94% share price decline from the peak that it reached early last year.

It’s a stunning loss of value from a company whose IPO valuation was £5.4 billion - it was the biggest UK IPO since Royal Mail. And that was less than two years ago.

But the IPO valuation is in the past. Those who went ahead and bought shares from the private equity sharks at KKR must surely regret their decision, but it can’t be changed. Let’s see what today’s interim results have to say about the future of the business.

What it does - THG says that it has built an “ecosystem”. If you want a quick rule of thumb to avoid overpriced puffery, then run (don’t walk) from any company that claims to have made an “ecosystem”. An ecosystem is a rainforest or a lake - not a business.

More seriously, this is what THG does:

Since 2004, we have grown from a British start-up to a globally renowned end-to-end tech platform specialising in taking brands direct to consumers worldwide, powered by our propriety (sic) technology platform, THG Ingenuity

The group includes a collection of beauty brands and beauty websites, the nutrition brand “Myprotein”, the e-commerce platform Ingenuity, and a collection of smaller, related businesses.

Results highlights for H1 2022

- Revenue +12% to £1.1 billion

- Adj. EBITDA minus 60% to £32m

- Operating loss £89m (last year: operating loss £17m)

The financial loss is said to reflect “consumer price protection investment strategy” (yuk!).

Gross margin declined because of the company’s strategy “to partially shield consumers from adverse macro-economic conditions and a period of unusually high raw material costs (principally whey).”

This is nonsense, isn’t it? Since when does a company selling lipstick and protein powder decide to lose money, out of a desire to protect and shield its customers?

THG argues that the “investment” is helping to drive consumer retention, but so what? Losing money isn’t sustainable, so THG is only going to have to raise prices sooner or later, anyway.

Balance sheet

There is little tangible balance sheet value here. The company has equity of £1.7 billion but that includes nearly £1.6 billion of intangibles. Strip them out and tangible equity is about zero.

Also, while the working capital position looks comfortable (£1 billion of current assets vs. £600m of current liabilities), the company has had to take out £500m of long-term borrowings. Net debt is £226m.

The company says there are seasonal effects here, but the company had a large net cash position a year ago. It’s the non-seasonal investment decisions that have mainly driven the plunge into debt.

At least the banks are happy to lend and THG has headroom of £170m in undrawn facilities, plus a new £156m facility. But where is all of this going to lead for shareholders? I like to invest in businesses which generate lots of cash, and have surplus cash to send to shareholders - no sign of that here.

Outlook

The company cuts its adjusted EBITDA forecast for the year (previously, it expected to achieve around £160m).

Noting the impact of rising interest rates and energy prices on consumers, it says (emphasis added):

Despite this outlook, the Group anticipates a strong H2, with another period of double-digit growth. This performance is expected to be supported by increasing growth rates in both Nutrition and Ingenuity, comparatives easing, stable AOV's, new customer acquisition and repeat rates.

Pricing power across THG's own brands allows inflation to be partially mitigated through increased prices, albeit the Group remains committed to raise slower and lower than inflation to protect consumers and drive market share gains.

Whilst inflation is easing in core areas such as commodities, the majority of margin benefits will be realised in the fourth quarter due to forward buying plans. Therefore the Group now expects FY 2022 adjusted EBITDA between a range of £100m to £130m…

Looking out beyond the current year, THG expects its EBITDA margin to recover. It thinks that lower whey prices will help to normalise its margins.

Courtesy of nasdaq.com, I’ve found a long-term chart of the whey price:

My view

Despite its hard work in selling its story, I’m not sure if there is any high-quality business among THG’s large assortment of enterprises.

In theory, myprotein should be a valuable brand. But it’s being run as if whey prices hadn’t increased, on a theory that commodity prices will come back down to their 2019-2020 averages. If they don’t come back down, what then? The company - and by extension its shareholders - will be saddled with hundreds of millions of pounds of bank debt.

It already owes the banks £500m, and judging by its eagerness to open a new credit facility, this number may be set to increase.

Therefore, even at a price/sales multiple of only 0.5x, I’d be wary about getting involved. Add on the bank debt to get the enterprise value, and you’ll find that enterprise value/sales is closer to 1x.

Another metric we could use is enterprise value divided by adjusted EBITDA. For THG this year at the latest market cap, I think this is in the range of 6x-8x. That could make sense for a high-quality, profitable enterprise. It does not make sense for THG.

This is a falling knife that I would not be interested in catching.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.