Good morning from Paul, Graham & Roland.

Explanatory notes -

A quick reminder that we don’t recommend any shares. We aim to review trading updates & results of the day and offer our opinions on them as possible candidates for further research if they interest you. Our opinions will sometimes turn out to be right, and sometimes wrong, because it's anybody's guess what direction market sentiment will take & nobody can predict the future with certainty. We are analysing the company fundamentals, not trying to predict market sentiment.

We stick to companies that have issued news on the day, with market caps (usually) between £10m and £1bn. We usually avoid the smallest, and most speculative companies, and also avoid a few specialist sectors (e.g. natural resources, pharma/biotech, investment cos). Although if something is newsworthy and interesting, we'll try to comment on it. Please bear in mind the "list of companies reporting" is precisely that - it's not a to do list. We typically cover c.5 companies per day, with a particular emphasis on under/over expectations updates, and we follow the "most viewed" list of readers, so if you're collectively interested in a company, we'll try to cover it. Obviously with the resources available, we can't cover everything! Add you own comments if you see something interesting, and feel free to discuss anything shares-related in the comments.

A key assumption is that readers DYOR (do your own research), and make your own investment decisions. Reader comments are welcomed - please be civil, rational, and include the company name/ticker, otherwise people won't necessarily know what company you are referring to, if they are using unthreaded viewing of comments.

What does our colour-coding mean? Will it guarantee instant, easy riches? Sadly not! Share prices move up or down for many reasons, and can often detach from the company fundamentals. So we're not making any predictions about what share prices will do.

Green (thumbs up) - means in our opinion, a company is well-financed (so low risk of dilution/insolvency), is trading well, and has a reasonably good outlook, with the shares reasonably priced. And/or it's such deep value that we see a good chance of a turnaround, and think that the share price might have overshot on the downside.

Amber - means we don't have a strong view either way, and can see some positives, and some negatives. Often companies like this are good, but expensive.

Red (thumbs down) - means we see significant, or serious problems, so anyone looking at the share needs to be aware of the high risk. Sometimes risky shares can produce high returns, if they survive/recover. So again, we're not saying the share price will necessarily under-perform, we're just flagging the high risk.

Others: PINK = takeover approach, BLACK = profit warning, GREY = possible de-listing.

Links:

Paul & Graham's 2024 share ideas - live price-tracking spreadsheet (2 separate tabs at bottom), Video update of results so far, June 2024.

** New SCVR summary spreadsheet for calendar 2024 ** This is the live one! (updated 6/9/2024)

Archive - SCVR summary spreadsheet for calendar 2023.

Paul's podcasts (weekly summary of SCVRs & macro views) - or search on any podcast provider for "Paul Scott small caps" - eg Apple, Spotify.

Phil Hanson's data analysis measuring performance of our colour-coding system in the SCVRs, from July 2023- Mar 2024 (with live prices). My video explaining/reviewing it.

My other video (June 2024) - How to screen for broker upgrades on Stockopedia. More stock screening strategies here (possible bargains?) - 21/9/2024.

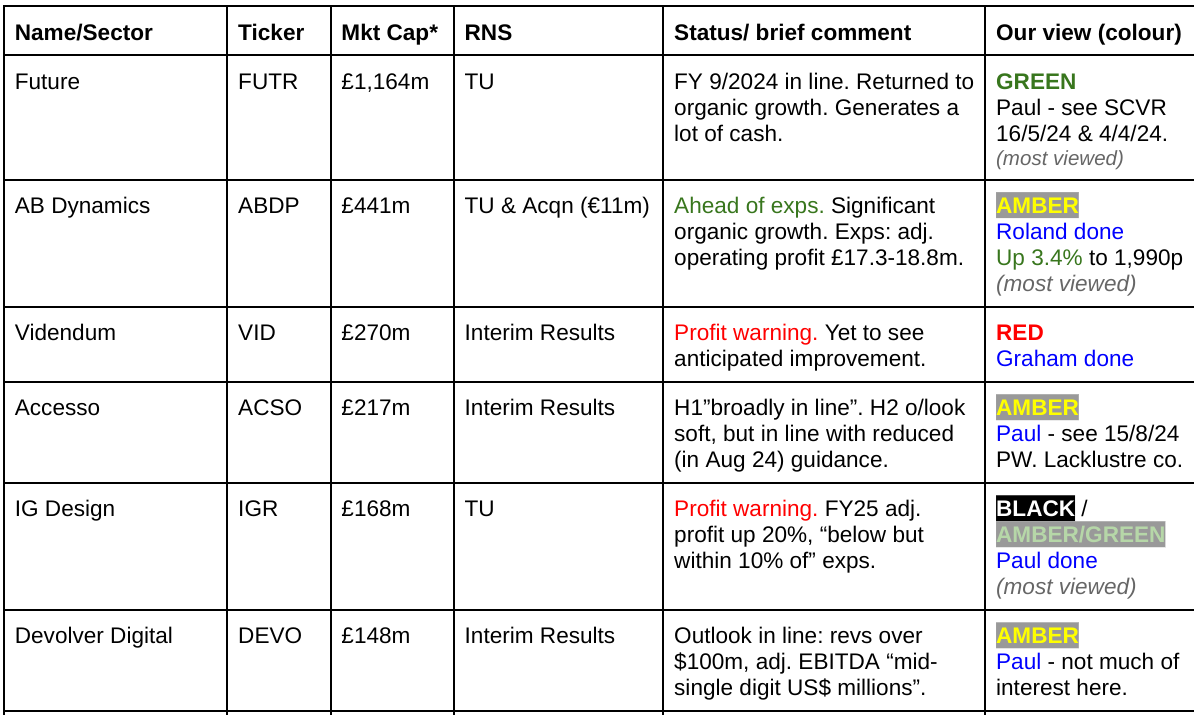

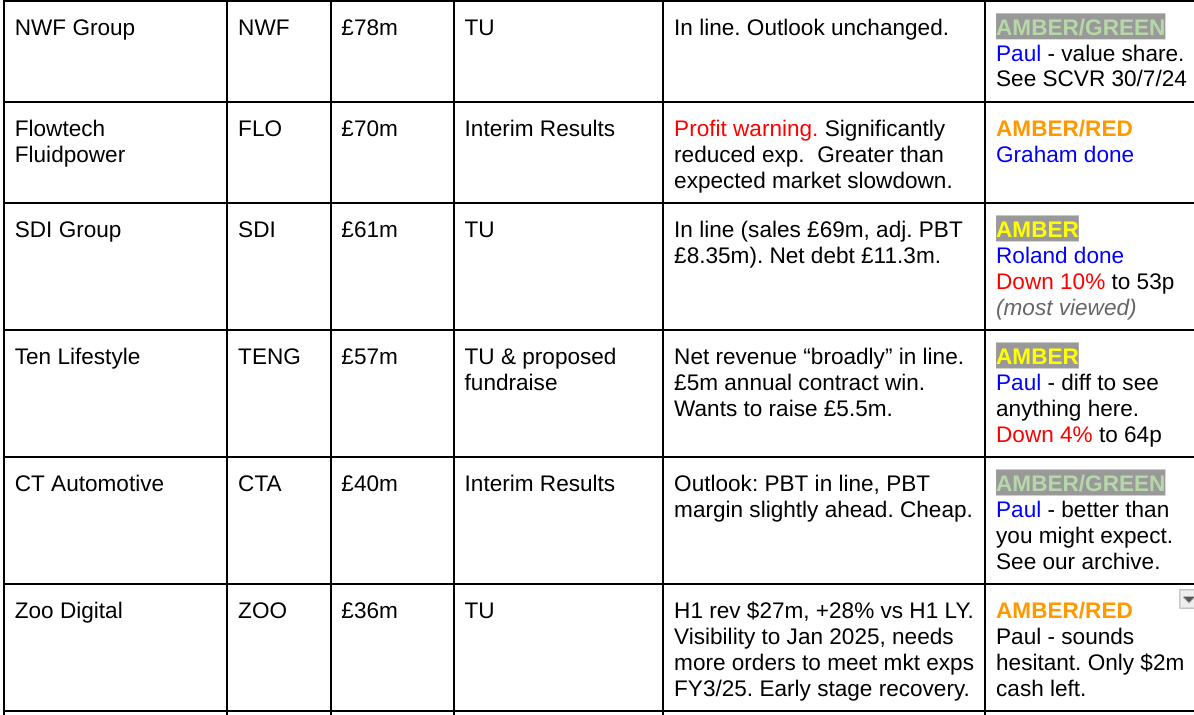

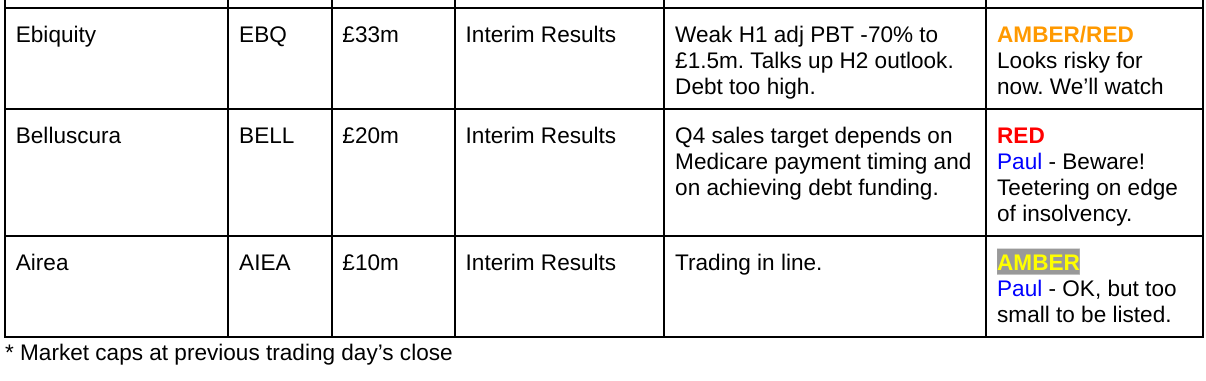

Companies Reporting

Summaries

IG Design (LON:IGR) - down c.21% to 136p (£130m) - AGM Trading Update [profit warning] - Paul - BLACK & AMBER/GREEN on fundamentals

Profit warning takes 9% off FY 3/2025 forecast profit, and 20% off subsequent years, so the -21% share price reaction seems about right. Sounds like there's still a fair bit of turning around to be done in its USA division, which lost its recent CEO. I suspect that trying to push up margins has caused some business to leak away to competitors. The price is now looking quite attractive on reduced forecasts, so I'm happy with AMBER/GREEN.

Flowtech Fluidpower (LON:FLO) - down 25% to 82p (£52m) - 2024 Half-year Report & TU - Graham - AMBER/RED

Bad news as EBITDA/PBT forecasts are both cut by £4m and the prospects for any meaningful profits in the current year take a big hit. Next year should be better as the recent Thorite acquisition should make a positive contribution and projects delayed in the current year will be delivered in 2025. I’ve been patiently neutral on this stock for some time but I feel obliged to take a mildly negative view on it now, after another disappointment.

Ab Dynamics (LON:ABDP) - up 3.4% to 1,990p (£456m) - FY update & Acquisition - Roland - AMBER

This automotive testing group seems to be making good progress and has upgraded guidance for the year just ended. A small acquisition announced today sounds sensible as well. However, the share price looks up with events to me, so I’m going to take a neutral view for now.

SDI (LON:SDI) - down 10% to 53p (£56m) - AGM Update - Roland - AMBER

This scientific instruments group has stopped short of a profit warning today, but has warned of a soft start to the year and greater H2 weighting than in FY24. I think the shares could be reasonably priced on 10 times FY25e earnings, but there’s clearly a risk of further problems. I’m taking a neutral view at this time.

Videndum (LON:VID) - down 18% to 229.5p (£216m) - Interim Results - Graham - RED

I didn’t expect to take a negative stance on Videndum today but shareholders have been warned at least twice that in a downside scenario, the going concern assumption is in doubt. The bank is still playing ball and the business can still plausibly turn around, but shareholders are at great risk.

Paul’s Section:

IG Design (LON:IGR)

Down c.21% to 136p (£130m) - AGM Trading Update [profit warning] - Paul - BLACK & AMBER/GREEN on fundamentals

Bad luck to holders here, some were wondering in the comments here whether bad news might be coming, due to the soft share price? It’s very tricky at the moment - do sellers know something, or are they selling for tax avoidance measures re the forthcoming budget? We don’t know.

In early trades this morning IGR is down c.20%, which looks about right to me, since Canaccord has helpfully updated us, with a 9% drop in forecast adj PBT from $36.0m to $32.7m for FY 3/2025. However, it’s also put through forecast drops of 19-20% for the following two years, which aligns with the 20% share price fall this morning.

Checking our previous notes here for context, I liked the turnaround at IGR at the start of 2024, and put it onto my top 20 share ideas for 2024, at a starting price of 148p. It had been a decent winner, but gone into a minus position today of -6%.

30/4/2024 - 157p GREEN (Paul) - Ahead exps TU after 5 months silence. Good value & strong balance sheet.

25/6/2024 - 225p AMBER/GREEN (Paul) - Good 3/2024 results. Plenty of net cash. Share price now up with events, so shift down from green to amber/green.

What’s gone wrong? Continuing revenue declines in USA, with 5-month sales (Apr-Aug 2024) down -14%. It talks about more cautious customer ordering, but I don’t believe that. No way are total industry sales down that much, so it says to me that shops are ordering products from IGR’s competitors instead. Maybe that’s a result of IGR focusing on raising profit margins - that some customers are finding better value elsewhere? IGR is only an intermediary after all, between Chinese factories, and Western retailers. Maybe it’s being squeezed out by some customers ordering direct from Chinese factories?

The US CEO left in July 2024 and they’re looking for a replacement.

International “performing well”, and in line with expectations. Europe good, offsetting UK & Australia “soft”.

Guidance & outlook - is nicely detailed and ties in with Canaccord’s update -

“Overall Group revenue has declined c13% in the period compared to prior year. Whilst the H1 versus H2 revenue split is expected to remain similar to the prior year, we anticipate an improvement in H2 profitability driven by the timing of benefits from strategic initiatives and mix improvements.”

“Outlook for the full year:

With the order book now c77% complete at this point (FY2024 equivalent: 77%), we anticipate Group revenue to decline c5% for the full year, mainly driven by the trends we are experiencing in DG Americas.

Notwithstanding the challenges in DG Americas, the Group's Operating Profit is expected to grow year-on-year, and the margin is still expected to return to above proforma pre-pandemic levels of at least 4.5%.

The Group expects to deliver in excess of 20% year-on-year adjusted profit growth, however, as a result of the lower expected revenue, the Group now expects results for the year to be below, but within 10% of, previous market profit expectations and towards the lower end of the Board's profit expectations… “

Turnaround of US operations - I’m quite surprised at these comments, which sound like there’s still some sorting out needed, and that the previous acquisition strategy wasn’t well executed -

“we continue with the turnaround of the DG Americas business, reducing the complexity that was built over successive acquisitions, and improving margins through more simplification and better leverage of its scale.”

Customer risk - this sounds as if IGR has turned away some business from poorly financed customers. This reassures me, as after all, sales are a gift until they’ve been paid for, and the impact of bad debts is large when you’re selling low margin product, as IGR does -

“In addition, we were carefully managing our credit risk exposure, which weighed on revenues, as some of our US retail customers gave us cause for concern.”

Valuation - Canaccord has now got 21 US cents (down from 24) for FY 3/2025, and similar 22 cents next year. Converting into sterling (unfavourable forex moves recently too) at £1 = $1.334 gets us to 15.7p and 16.5p next year. What PER to use? Growth seems to have conked out, and it’s a low margin business with little pricing power, so I think 10x looks about right. Hence I get 157-165p valuation.

Remember there’s also excellent balance sheet support, eg at 3/2025 it has net working capital of $195m, including $95m of net cash (which I think excludes lease liabilities), and average net cash of $28m during the last full year.

Paul’s opinion - today’s profit warning has certainly knocked my confidence in the turnaround, and it’s undoubtedly a setback that reinforces reality that this really isn’t a very good business. It’s always going to be low margin (although getting to c.5% is a good improvement in recent years). The pandemic showed that it’s very vulnerable to supply chain problems/delays, since a lot of its products are time sensitive to specific dates, eg Christmas, so can’t be delivered late, as they would be worthless and rejected by the customers.

That said, after today’s fall, shares now look attractively priced again, particularly with lots of balance sheet support.

So on fundamentals, I’m happy with AMBER/GREEN.

Overall, it’s a setback, but not a disaster, and the share price reaction (before, and today) has I think allowed for disappointing trading.

Will investors get a second slice of cake with a renewed bull run? Or has the cake been left out in the rain too long?

Graham’s Section:

Flowtech Fluidpower (LON:FLO)

Down 25% to 82p (£52m) - 2024 Half-year Report & TU - Graham - AMBER/RED

This share has been on the road to recovery for some time, but today we have news of another pothole.

Share price chart as of last night:

And the bad news today: revenues are under pressure so that even with better gross profit margins, net profits are going in the wrong direction. The outlook for 2024 is significantly below market expectations.

In the company’s words:

Persistent headwinds in our marketplace have continued to impact top line growth ambitions with revenue reducing 5.7% compared to H1 23…

Gross profit margin up 290bps against H1 23 and 160bps up on FY 2023; results in higher gross profit in H1 24 v H1 23 notwithstanding the reduction in revenue

Underlying EBITDA of £4.7m, reduction limited to £0.3m despite £3.4m reduction in revenue compared to H1 2

The “financial highlights” table reveals more bad news, including H1 operating profit of only £1.2m (H1 last year: £2.4m) and a pre-tax profit of only £0.3m (last year: £1.6m).

So the road to recovery is taking longer than anticipated.

The big picture is that Flowtech has already posted a loss for three out of the last four financial years. And so far this year, it’s only trading at around breakeven.

Customers have reduced orders, i.e. have down-traded:

Down-trading is largely external market related with our expectation being that more than 75% of these down-traders will increase orders as the market improves. Northern Ireland revenues have been specifically impacted due to a small number of long-standing large OEM customers with the crushing & screening industry output reducing by over 20% over the last two quarters. Specific larger, major turnkey projects Flowtech has won have been delayed or pushed out for delivery into 2025.

And there is pressure on pricing:

We have maintained a consistent underlying order frequency but with reduced basket size as customers curb general expenditure and burn off held inventories. Larger projects are being delayed which is reducing expected volumes. The market slowdown has increased price competitiveness as customers seek cost reduction. Our strong commercial discipline has protected our gross margin, and, in some cases, we have actively chosen to walk away from lower margin business.

New estimates have been published by Panmure this morning (many thanks). They see an underlying sales decline this year of 5%, and cut their EBITDA forecast by £4m to £7m. Their new adj. PBT forecast also gets cut by £4m, to £1.7m.

Net debt has reduced slightly, despite difficult trading, to £13.5m. Debt reduction was boosted by a £4m reduction in inventories and the issuance of some new shares (an old warrant was exercised).

Outlook: the recent acquisition (we discussed it here in August) remains a source of positivity for 2025 and beyond, but it will negatively impact 2024. So while Flowtech is looking forward to a stronger performance in 2025 and 2026, the current year is trending “significantly below market expectations”.

Graham’s view

I’ve had a neutral stance on Flowtech in recent years.(e.g. August 2023). I have a lot of residual respect for the business, as I remember when it was profitable and seemed like a solid performer.

Unfortunately, events have disrupted this point of view and perhaps now I have to take a more negative stance?

One point which perhaps I haven’t emphasised enough is that when looking at Flowtech’s products and services, I do have to conclude that Flowtech probably struggles to generate pricing power: its own branded products have to compete against both generic products and 3rd party branded products (both of which it also supplies to customers).

In isolation, that fact wouldn’t force me to take a negative stance on the stock but after several years of struggle, maybe I have to accept that this just isn’t a very high-quality business? The revenue decline might not be Flowtech’s fault, but when it’s already struggling to generate any profits then maybe we have to accept that this just isn’t a very good investment?

I’m reluctantly downgrading my stance on this to AMBER/RED, as the recovery has now taken too long.

The trend in the EPS forecast tells the story:

Videndum (LON:VID)

Down 18% to 229.5p (£216m) - Interim Results - Graham - RED

Another profit warning to look at this morning. Videndum is “the international provider of premium branded hardware products and software solutions to the content creation market”.

Before getting into the trading update, let’s check out the interim results.

H1 revenue is “broadly in line” with expectations. Revenue down 7% vs. H1 2023. Recovery from cinema/TV strikes is “taking longer than anticipated”.

We covered Everyman Media (LON:EMAN) here yesterday and have also covered Facilities by ADF (LON:ADF) recently (here). These have also suffered from the cinema/TV strikes and their H1 results reflected that.

Videndum, in addition to the cinema/TV industries, serves the consumer and “independent content creator” segments. They say today that the “continued challenging macroeconomic environment” is affecting these categories.

Videndum’s H1 financial results from continuing operations:

Adj. operating profit £11m (H1 last year: £16.2m).

Adj. PBT £6.9m (H1 last year: £11.1m)

However, the statutory results are much worse than this. Without any adjustments and including the results of subsidiaries that Videndum intends to sell, there was an operating loss of £9m. The pre-tax loss was £13m.

Net debt has at least reduced over the six month period, from £128m (Dec 2023) to £117m (June 2024).

The leverage multiple is 3.3x and I consider anything over 3x to be a red flag.

On the lending facility:

The Group renegotiated its committed Revolving Credit Facility ("RCF") with its lending banks. The facility has been extended, reduced in quantum, and its lending covenants improved

Reading through the statement a little, I see that the new covenants include a leverage multiple of 4.25x and interest cover of only 1.5x. These are weak covenants so when Videndum says that covenants have been “improved”, they mean that the covenants have been relaxed.

This is standard procedure when a company is trading poorly but when the bank is happy to continue backing it, at least for the time being, in the hope that trading will improve.

Outlook excerpts:

Cine and scripted TV market shows continued signs of post-strike improvement with commissioning of new productions starting to ramp up. However, the recovery is taking longer than anticipated…

Despite signs of a pickup in cine and scripted TV productions, and growth in the premium camera market, the Group, along with other companies in our sectors, has yet to see the anticipated improvement in orders. As a result, we now expect FY 2024 to be below our previous expectations…

The Board expects the cine and scripted TV market to return to higher levels of demand during 2025, and for our ICC segment to start to benefit from the increase in premium camera sale

CEO comment: emphasises the company’s focus on managing costs, capex, and working capital during this challenging period. A cost-saving programming will deliver “at least £10m in additional permanent savings” from next year.

Graham’s view

This is another stock where we were neutral the last time we looked at it, and where it’s having difficulty meeting its targets.

What’s truly devastating about this story is that Videndum already raised £125m in new equity last November (covered by Paul here). This was supposed to comprehensively deal with the company’s existing balance sheet problem.

Due to a very poor cash flow performance in 2023, the company still finished that year with net debt of £128m (down from £193m at the end of 2022).

Here we are looking at the results for June 2024 and there has been a modest reduction from that level, but it’s still not enough to enable the company to sit comfortably.

Again, this is not entirely the company’s fault: it could not have predicted the Hollywood strikes or the depressed conditions in the content creation segment. Although the company is to blame for getting itself over-leveraged in the first place, making it vulnerable to a downturn.

Going back to the Annual Report for 2023, I find an acknowledgment by the Directors of a “material uncertainty” when it comes to Videndum’s ability to continue as a going concern.

Today’s interim results contain a similar warning, so shareholders cannot say they weren’t warned:

…the Board has concluded that while the Group has a reasonable expectation of its ability to renegotiate the terms of the RCF if required, take other actions to avoid a breach of covenants or to obtain a waiver, these financial projections do indicate the existence of a material uncertainty which may cast significant doubt about the Group's ability to continue as a going concern.

In these circumstances, I have to go RED on Videndum. I hope it pulls through, but the position isn’t safe for current shareholders.

The share price has been saying this for a while:

Roland’s section

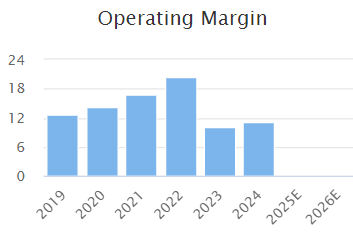

Ab Dynamics (LON:ABDP)

Up 3.4% to 1,990p (£456m) - Pre-Close Update & Acquisition - Roland - AMBER

full year adjusted operating profit is anticipated to be ahead of current market expectations

This high-tech engineering group specialises in testing, simulation and measurement products for the transport industry. It’s been a spectacular multibagger over the last decade, but progress (or at least market sentiment) has been more mixed in recent years:

Today’s trading update includes details of an acquisition but leads with the news that adjusted profits for the year ended 31 August 2024 are now expected to be ahead of expectations.

Management says that demand for Testing products has been strong, driven by growth in driving robots and self-driving systems (ADAS).

The Testing Services business is said to have returned to growth as various headwinds have eased (vehicle shortages, China pandemic restrictions).

The company doesn’t provide any indication of how far ahead profits might be, but we do have some information to work with:

Revenue is expected to “exceed £110m”, which is the consensus figure shown on the StockReport

The previous consensus range for adjusted operating profit was £17.3m - £18.8m

ABDP enjoyed “robust margin performance” during the second half of the year

The company’s half-year results did indicate an H2 weighting, so it’s reassuring to see the business has delivered this result.

H1 adjusted operating margin was 17% and H1 revenue was £52.3m.

Assuming full-year revenue of perhaps £115m would imply H2 revenue of c.£63m. Applying an 18% margin to this gives a figure of £11.3m. Adding this to H1 adj operating profit of £8.9m suggests to me that the company might now be report an adjusted operating profit of c.£20m for the full year.

Unfortunately there are no updated broker notes available to us today.

Using £20m as my updated estimate gives AB Dynamics an EBIT/EV yield of just under 5%. In my view that’s not outrageous for a growth business, but not especially good value either.

One concern for me is that this company is quite a heavy adjuster. H1 adjusted operating profit of £8.9m only dropped out to a statutory operating profit of £5.5m. The majority of this is amortisation of acquired intangibles, so it’s up to individual investors to form a view on this.

It may be worth noting that reported operating margins remain well below pre-pandemic levels:

However, despite my reservations about profit adjustments, there don’t seem to be any problems with cash generation. Net cash was £28.6m at the end of August (FY23: £32.0m). This has been a consistent feature of the balance sheet in recent years and should hopefully prevent the need for any dilution:

Acquisition: the other piece of news in today’s update is the acquisition of German firm Bolab Systems for up to €11.0m (£9.3m), with an initial payment of €5.0m (£4.2m).

Bolab is said to be a niche automotive power electronics testing products business that was founded in 2012. AB Dynamics is acquiring Bolab from its founder, who will remain in the business.

Bolab is expected to report revenue of €4.0m and an adjusted operating profit of €0.8m for the current financial year, implying a 20% operating margin. It sounds a logical fit to me, and small enough to bolt on easily.

If ABDP pays the full €11.0m consideration, then the implied EBIT/EV yield is 7.3%, which doesn’t seem unreasonable to me. Based on these figures, I would expect the deal to provide a modest boost to AB Dynamic’s overall operating margin.

Roland’s view

AB Dynamics was trading on around 30 times forecast earnings ahead of today’s update, and the modest share price gain suggests to me that this multiple will remain broadly unchanged following today’s news.

I think this is probably a good quality business with attractive long-term growth opportunities, but the valuation seems up with events to me, with plenty of growth priced in.

The risk/reward balance doesn’t seem all that attractive to me at current levels, so I’m going to maintain our previous AMBER view on this business.

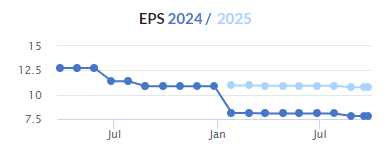

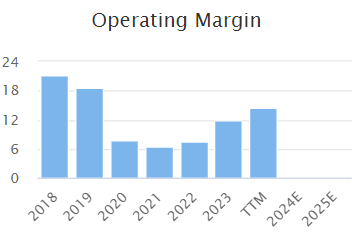

SDI (LON:SDI)

Down 10% to 53p (£56m) - AGM Update - Roland - AMBER

The Company expects to deliver full year results in line with market expectations

Shares in this buy-and-build scientific instrument group are down by 10% following today’s AGM update, less than two months after SDI published its full-year results.

Sure enough, while SDI has maintained its full-year guidance today, management now says that a slow start to the year means that results will be more heavily H2-weighted than last year:

Profit and revenue delivery in FY25 will be weighted more towards H2 than in FY24 due to the current financial year starting slowly, reflecting conditions in certain customer markets.

Checking back to July’s final results, management said then that as a result of “a conservative view on certain sales opportunities, adjusted EBIT guidance for FY25 has been revised”. So there were already signs of weakness.

Stockopedia’s excellent analyst consensus trend chart shows how the company’s broker has cut its forecasts twice over the last year. FY25 eps estimates have fallen by more than 25% in total:

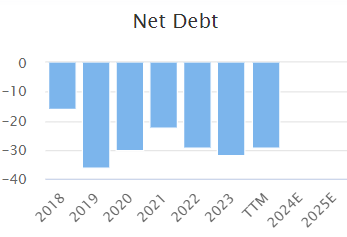

Debt reduction: the other item of interest in today’s update confirms that cash generation has remained positive. Net debt at the end of August was £11.3m, down from £13.2m at the end of April 2024.

This seems a comfortable enough level of debt to me, given this year’s expected net profit of c.£7m.

Roland’s view

SDI shares have now fallen by 75% from their pandemic highs, when the group benefited from exceptional sales of high-margin COVID-19 testing related products.

At its peak, SDI was trading on c.30 times forecast earnings and was being talked of by many investors as the next Judges Scientific (LON:JDG).

Where does that leave us today? SDI shares certainly look more reasonably priced, on less than 10 times FY25 forecast earnings.

However, I think it’s sensible to assume there’s some risk of a profit warning later this year, given the weak tone of today’s update.

In addition, I can’t help feeling that SDI may be struggling to replace its high-margin pandemic sales. House broker Cavendish (many thanks) has left its current year forecasts unchanged today, but has previously predicted that operating margins will weaken slightly this year.

Creating a successful buy-and-build group like Judges – with high margins and high returns on capital employed – is not easy.

I’m not sure SDI has the durable quality that’s needed to justify a premium valuation, regardless of the risk of an H2 profit warning.

However, at current levels this business does look reasonably valued to me. I would probably share Stockopedia’s view that this could be an interesting Contrarian situation:

Overall, I’m going to take a neutral view. I can see risk and potential reward, but would need to do further research to form a stronger conviction.

See what our investor community has to say

Enjoying the free article? Unlock access to all subscriber comments and dive deeper into discussions from our experienced community of private investors. Don't miss out on valuable insights. Start your free trial today!

Start your free trialWe require a payment card to verify your account, but you can cancel anytime with a single click and won’t be charged.